RSS Feed

RSS Feed by Calculated Risk on 3/23/2006 09:37:00 PM

Thursday, March 23, 2006

FDIC: Scenarios for the Next U.S. Recession

From the FDIC: Scenarios for the Next U.S. Recession. On housing:

The risk of a housing slowdown is another area of concern going forward. The recent housing boom has been unprecedented in modern U.S. history.2 It has been suggested by many analysts that the housing boom has been a significant contributor to gains in consumer spending in recent years. Indeed, a number of the FDIC roundtable panelists pointed to the apparent connection between rising real estate wealth during the past four years and the sustained strength in consumer spending during that period. Because consumer spending accounts for over two-thirds of U.S. economic activity, any shock to consumer spending, such as that which might be caused by a housing slowdown, is a concern to overall economic growth.Much more in article.

It is very likely that housing wealth has been a significant factor behind growth in consumer spending. Through the use of cash-out refinancing, increased mortgage balances, and greater use of home equity lines of credit, as well as through owners selling homes outright and cashing in on their accumulated equity, it is estimated that anywhere from $444 billion to $600 billion was liquidated from housing wealth during 2005.3 Whichever estimate one uses, the total almost surely eclipses the $375 billion gain in after-tax income for the year. While probably not all of the home equity liquidated during 2005 fed consumption spending (much of it was invested into other assets, including second or vacation homes), these statistics illustrate how important home equity has become as a source of household liquidity.

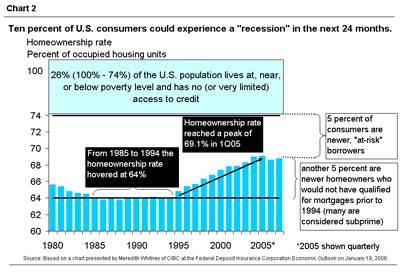

There are concerns, however, that changes in the structure of mortgage lending could pose new risks to housing. These changes are most evident in the rising popularity of interest-only and payment-option mortgages, which allow borrowers to afford more expensive homes relative to their income, but which also increase variability in borrower payments and loan balances. To the extent that some borrowers with these innovative mortgages may not fully understand the potential variability in their payments over time, the credit risk associated with these instruments could be difficult to evaluate. In addition, the degree of effective leverage in home-purchase loans has risen in recent years with the advent of so-called “piggy-back” mortgage structures that substitute a second-lien mortgage for some or all of the traditional down payment. Meredith Whitney noted at the roundtable that the recent use of revolving home equity lines of credit in lieu of down payments has enabled an increasing number of first-time buyers to qualify for homes that they otherwise could not afford. (Click here to link to the complete text of Ms. Whitney’s remarks in the transcript.)

Overall, Ms. Whitney’s research suggests that a group that includes approximately 10 percent of U.S. households may be at heightened risk of credit problems in the current environment. This group mainly includes households that gained access to mortgage credit for the first time during the recent expansion of subprime and innovative mortgage loan programs. Not only do many borrowers in this group have pre-existing credit problems, they may also be more vulnerable than other groups to rising interest rates because of their reliance on interest-only and payment-option mortgages. These types of mortgages have the potential for significant payment shock that occurs when low introductory interest rates expire, when index rates rise, or when these loans eventually begin to require regular amortization of principal including any deferred interest that has accrued (see Chart 2).

Because of the importance of mortgage lending to bank and thrift earnings, the large-scale changes that have taken place in this sector will clearly have implications for the banking outlook. Bank exposure to mortgage and home equity lending is now at peak levels. As reported in the FDIC’s latest Quarterly Banking Profile (http://www2.fdic.gov/qbp/index.asp), 1-4 family residential mortgages and home equity lines of credit accounted for a combined 38 percent of total loans and leases in fourth quarter 2005, well above the roughly one-third share maintained at the beginning of the decade.

Housing analysts are in disagreement as to whether or not recent signs point to a moderation in housing activity or the beginning of a more significant correction. Currently, inventories of unsold homes and sales volumes are among the indicators pointing to a housing slowdown. Inventories of unsold existing homes rose from under four months of supply at current sales volume in early 2005 to 5.3 months of supply as of January 2006. Meanwhile, the pace of existing home sales has been trending lower since last summer. A clear trend in the direction of home sales and prices may not be evident until the completion of the peak spring and summer selling season later this year.

Many analysts argue that home prices in the hottest coastal markets, especially in the Northeast and California, could be poised to decline in the near future. For example, PMI Mortgage Insurance Company analysts place essentially even odds that home prices will decline during the next two years in a dozen cities in California and the Northeast.4 Should home prices either stop rising or begin to fall in these areas, local banks and thrifts would need to look to non-residential loans to support revenue growth.

Art McMahon of the OCC outlined the banking industry’s reliance on mortgage lending during his remarks at the FDIC roundtable. (Click here to link to the full text of Mr. McMahon’s remarks in the transcript.) Mr. McMahon acknowledged that previous historical episodes of large metro-area home price declines were generally the result of severe local economic distress.5 Should some regional housing market downturns occur, banks may be hard-pressed to generate non-residential loans in great volume. Historically, regional housing price declines have tended to be associated with a slowdown in small business activity, with banks making fewer commercial and industrial loans in addition to suffering mortgage and consumer portfolio stress.