RSS Feed

RSS Feed by Calculated Risk on 2/13/2007 03:00:00 PM

Tuesday, February 13, 2007

Home Mortgages and the Trade Deficit

"Interestingly, the change in U.S. home mortgage debt over the past half-century correlates significantly with our current account deficit. To be sure, correlation is not causation, and there have been many influences on both mortgage debt and the current account."The Census Bureau reported "today that total December exports of $125.5 billion and imports of $186.7 billion resulted in a goods and services deficit of $61.2 billion."

Alan Greenspan, Feb, 2005

Click on graph for larger image.

Click on graph for larger image.The red line is the trade deficit excluding petroleum products. (Blue is the total deficit, and black is the petroleum deficit).

Looking at the trade balance, excluding petroleum products, the deficit has been fairly stable since the second half of 2005.

Brad Setser reviews the 2006 trade data and points out several key stories:

The first is that US exports grew quite strongly in 2006. ... The second is that the pace of non-oil import growth slowed. ... The third is that higher oil prices do lead even the US to cut back on its use of oil. ... The fourth big story -- one that is somewhat controversial for reasons that elude me -- is that exchange rate adjustment works.Another possible key story is the relationship between the trade deficit and mortgage debt. As Greenspan noted, "correlation is not causation", but it is possible that a slowdown in the U.S. housing market has also led to a reverse in the U.S. trade deficit. This could have significant implications going forward.

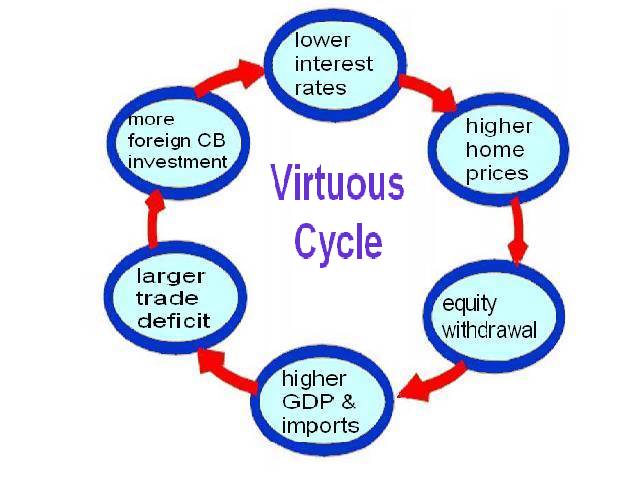

Perhaps we have seen a Virtuous Cycle as depicted in the following diagram:

Starting from the top: There is no question that lower interest rates led to an increase in housing prices. And those higher housing prices led to an ever increasing equity withdrawal by homeowners - until very recently (See Kennedy-Greenspan MEW graph). Based on research by Greespan, it appears a large percentage of this equity withdrawal has flowed to consumption (maybe 50%), increasing both GDP and imports over the last few years. Then, to finance the current account deficit, foreign Central Banks (CBs) have been investing heavily in dollar denominated securities. Some analysts have suggested that these investments have lowered interest rates by between 40 bps and 200 bps.

Starting from the top: There is no question that lower interest rates led to an increase in housing prices. And those higher housing prices led to an ever increasing equity withdrawal by homeowners - until very recently (See Kennedy-Greenspan MEW graph). Based on research by Greespan, it appears a large percentage of this equity withdrawal has flowed to consumption (maybe 50%), increasing both GDP and imports over the last few years. Then, to finance the current account deficit, foreign Central Banks (CBs) have been investing heavily in dollar denominated securities. Some analysts have suggested that these investments have lowered interest rates by between 40 bps and 200 bps. The result: a Virtuous Cycle with higher housing prices leading to more borrowing and more consumption, leading to lower interest rates, followed by higher housing prices.

The following diagram depicts the possible unwinding of the current cycle.

As housing cools down (prices do not need to collapse), this will lead to lower equity withdrawal. In turn this will lead to a slow down in GDP growth and lower imports.

Lower imports might lead to a lower trade deficit, depending on the strength of exports. This could lead to less foreign CB investment in dollar denominated assets. And this could lead to higher interest rates followed by lower housing prices and the cycle repeats.

This is why I'm predicting a decline in the trade deficit, and an increase in long rates.

Dr. Setser doesn't see the trade deficit decreasing in 2007.

"Here though I am a bit of a holdout. I am not convinced that it makes sense to project out current trends -- at least not the current y/y growth rates.Of course I'm looking at the trade deficit from a housing centric view, and I realize that view might be too narrow.

The monthly trends seem to me to suggest a slowdown in the pace of export growth (look at the first graph in the BEA data release). Conversely, there are some tenative signs that non-oil import growth is picking up a bit (December imports were $134b, up from $131-132b in October/ November). My personal view is that the trade deficit is more likely to stabilize at roughly its current level than to shrink."