RSS Feed

RSS Feed by Calculated Risk on 5/26/2010 06:28:00 PM

Wednesday, May 26, 2010

Toll Brothers: Orders Up, Cancellation Rates Way Down, Toll buying Lots Again (Uh, Oh!)

This post is from housing economist Tom Lawler:

Toll Brothers, the self-proclaimed “leading builder of luxury homes,” reported that net home contracts totaled 866 in the quarter ended April 30th, up 40.9% from the comparable quarter of 2009. Gross orders were up 16.6% from a year ago, while sales cancellations were down 71.4%. The company’s sales cancellation rate expressed as a % of gross orders was 5.3%, the lowest rate since the third quarter of FY 2005, and close to the time that Toll CEO Robert Toll made his infamous comment in the summer of 2005 that “(w)e’ve got the supply, and the market has got the demand; it’s a match made in heaven” right before housing demand started to fall. Home deliveries last quarter totaled 543, down 16.2% from the comparable quarter of last year, while the company’s order backlog as of 4/30/10 was 1,738, up 9.9% from a year ago. The company’s increase in orders came despite a 21% drop in Toll’s community count from last year.

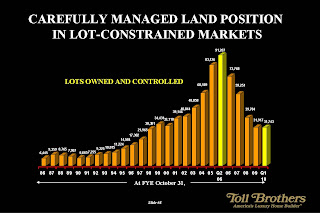

In its press release, new Toll CEO-designate Doug Yearley, Jr. noted that “with demand increasing in many areas, we are now focused on growth,” and said the company increased its lot count for the first time in four years – scaring more than a few folks.  Click on graph for larger image in new window.

Click on graph for larger image in new window.

[This graph], by the way, is some history of Toll’s land/lot position from one of its presentations, with one of the most misleading headlines known to man.

This chart, as well as Bob Toll’s statements, highlights how Toll completely and totally misread the housing markets during the middle of last decade, accelerating land/lot acquisitions right near the peak – a move that eviscerated shareholders, though the company’s relative low leverage saved it from extinction.

What scared folks is that the company’s new push to growth was based on an assessment, echoed by Bob Toll in the press release, that the rebound in orders/demand was not simply the result of the home buyer tax credit, but was also driven “by an increase in confidence among our buyers in their job security, their ability to sell their existing homes, and general trends in home prices." He based this assessment in part on the fact that “(i)n the three weeks since the start of our third quarter on May 1st, which coincided with the expiration of the homebuyer tax credit, our per community deposits and traffic were up 23% and 11%, respectively, over last year's comparable period.”

Note, though that (1) he referenced activity per community, and the company’s community count was down 21% from a year ago, and last quarter’s YOY increase in gross orders per community were up 47.2% YOY (and net orders 78%!); and (2) a year ago wasn’t exactly a strong housing market!!!! But…you know Bob!!!!

An amusing thing in today’s press release that actually suggests the company is highly uncertain about housing demand for the rest of this year was CFO’s Joel Rassman’s “limited” guidance he offered for the company’s home deliveries in FY 2010 (which is half over). He said the company estimates that it will deliver “between 2,200 and 2,275” homes in FY2010. Given the 1,139 homes already delivered in the first half of FY 2010, that means the company’s “guidance” is that it expects to deliver between 1,061 and 1,611 homes from May 1st through October 31st !!!! Now THAT’S a huge range, and one consistent with a view that “well, I think demand may have rebounded, but BOY, maybe it really WAS the tax credit!!!”

Of course, the tax credit probably was NOT as much of a factor for buyer’s of Toll’s homes relative to other builders – after all, Toll’s average price is in the $560,000 - $570,000, and the federal tax credit was capped at $8,000. And, in fact, there IS some anecdotal evidence that in some markets the demand for “Toll-like” homes has improved a bit. However, given Bob Toll’s track record of reading the housing market since the turn of the millennium ...

Bob Toll, by the way, will step down as Toll’s CEO effective June 16th, though he will “remain active” as Executive Chairman of the Board.

CR Note: this was from economist Tom Lawler.