RSS Feed

RSS Feed by Calculated Risk on 4/26/2005 12:54:00 AM

Tuesday, April 26, 2005

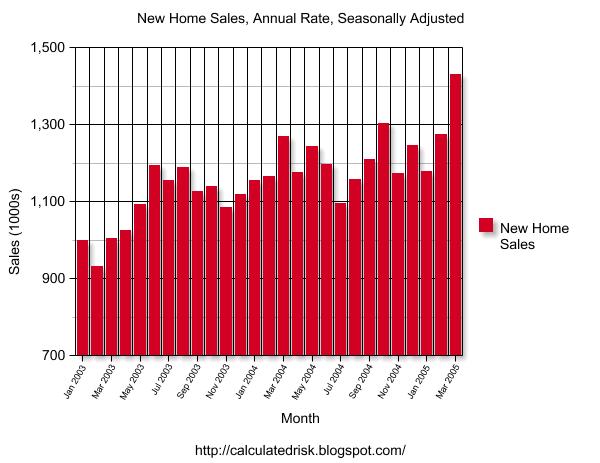

Record New Home Sales

According to a Census Bureau report, New Home Sales set a record in March to a seasonally adjusted annual rate of 1.431 million vs. market expectations of 1.19 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in March 2005 were at a seasonally adjusted annual rate of 1,431,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 12.2 percent above the revised February rate of 1,275,000 and is 12.7 percent above the March 2004 estimate of 1,270,000.

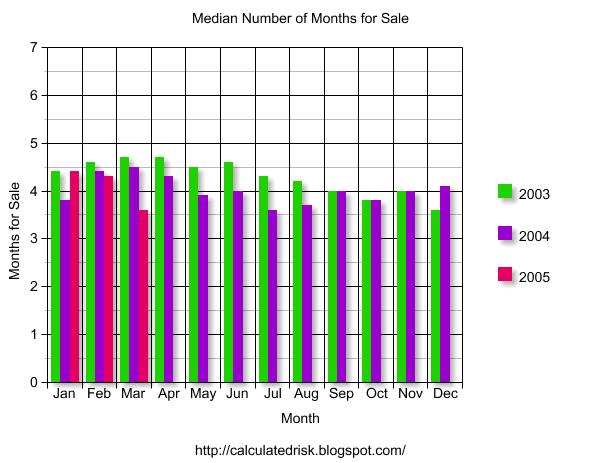

The median sales price of new houses sold in March 2005 was $212,300; the average sales price was $281,300. The seasonally adjusted estimate of new houses for sale at the end of March was 433,000. This represents a supply of 3.6 months at the current sales rate.

There is a seasonal pattern to supply and 3.6 months is below the normal level of supply as compared to 2003 and 2004. Months of supply is based on sales, and the record sales in March makes the months of supply number smaller.

Monday, April 25, 2005

Lau and Stiglitz: China's Alternative to Revaluation

by Calculated Risk on 4/25/2005 07:40:00 PM

In a Financial Times commentary, Lawrence Lau and Joseph Stiglitz argue that an export tax would be a better choice for China.

"If China were to contemplate a revaluation, it should consider as an alternative the imposition of a tax on its exports. Export taxes are generally permitted under WTO rules. Indeed, China has already moved in a limited way in this direction on textiles. There are several reasons voluntary imposition of a tax on its exports may be preferable to a renminbi revaluation. Both would have similar effects on Chinese exports - they would make them appear more expensive to the rest of the world. Because of this similarity, an export tax would provide an empirical answer to the question of whether a revaluation would work. But it would do this without some of the significant costs attendant on revaluation.It seems a 5% export tax would just increase the US trade deficit with China and might lead to more inflation in the US. I'll be interested in Setser and Roubini's views on this proposal!

One of the advantages of an export tax is that, unlike a revaluation, it would not lead to financial losses for Chinese holders of dollar-denominated assets, such as the People's Bank of China or commercial banks and enterprises. China's central bank currently holds about $640bn (£334bn) in foreign exchange reserves. Assume that only 75 per cent is held in dollar-denominated assets. A renminbi revaluation of 10 per cent would result in a loss of $48bn or about 400bn yuan for the central bank.

Another cost of revaluation would be possible further deterioration in the distribution of income, including increasing the already large rural-urban wage gap. Revaluation would put downward pressure on domestic Chinese agricultural prices; an export tax would not. An export tax, by contrast, would have a beneficial side effect: it could generate substantial government revenue for China. Given the high import content of Chinese exports to the US, a 5 per cent export duty would be equivalent to a currency revaluation of some 15-25 per cent, generating about $30bn-$42bn a year.

Finally, an export tax would not reward currency speculators. It may even discourage the speculation that has complicated macro-economic management of China's economy. If potential speculators can be convinced that China would rather impose an export tax than revalue, less "hot money" will flow into China. By contrast, nothing encourages speculators more than a "victory", especially where, as here, it is likely to do little to correct the underlying problems."

Q1 2005: Housing Vacancies and Homeownership

by Calculated Risk on 4/25/2005 11:29:00 AM

The Census Bureau released their Housing Vacancies and Homeownership report for Q1 2005 this morning.

National vacancy rates in the first quarter 2005 were 10.1 percent in rental housing and 1.8 percent in homeowner housing, the Department of Commerce and Census Bureau announced today. The Census Bureau said the rental vacancy rate was not different from the first quarter rate last year (10.4 percent) or the rate last quarter (10.0 percent). For homeowner vacancies, the current rate (1.8 percent) was also not different from the rate a year ago (1.7 percent), or the rate last quarter (1.8 percent). The homeownership rate (69.1 percent) for the current quarter was higher than the first quarter 2004 rate (68.6 percent) but not different from the rate last quarter (69.2 percent).

Click on graph for larger image.

Rental vacancies are still over 10% and homeownership rates are still climbing when compared to Q1 2004.

More on Housing

by Calculated Risk on 4/25/2005 01:55:00 AM

My most recent post, "After the Housing Boom: Impact on the Economy", is up on Angry Bear.

On Tuesday, New Home Sales will be released. I believe New Home Sales is a better leading indicator than Existing Home Sales (to be released on Monday). It appears that Sales for March were still strong, so I'm not expecting a significant drop-off in sales volumes reported this month.

Also the Census Bureau will release their quarterly Housing Vacancies and Homeownership report tomorrow.

A busy week for housing stats.

Best to all!

Friday, April 22, 2005

Fed's Kohn: Imbalances, Risks

by Calculated Risk on 4/22/2005 05:08:00 PM

Fed Governor Donald L. Kohn spoke today at the Hyman P. Minsky Conference in New York. Kohn made several cautionary comments on global imbalances. A few excerpts:

... beneath this placid surface are what appear to be a number of spending imbalances and unusual asset-price configurations. At the most aggregated level, the important imbalance is the large and growing discrepancy between what the United States spends and what it produces. This imbalance, measured by the current account deficit, has risen to a record level, both in absolute terms and as a ratio to GDP.

...

The sustainability of these large and growing imbalances has become especially suspect because it would require behavior that appears to be inconsistent with reasonable assumptions about how people spend and invest.

...

The current imbalances will ultimately give way to more sustainable configurations of income and spending. But that leaves open the question of the nature of that adjustment. Ideally, the transition would be made without disturbing the relatively tranquil macroeconomic environment that we now enjoy. But the size and persistence of the current imbalances pose a risk that the transition may prove more disruptive.

And on Real Estate:

A couple of years ago I was fairly confident that the rise in real estate prices primarily reflected low interest rates, good growth in disposable income, and favorable demographics. Prices have gone up far enough since then relative to interest rates, rents, and incomes to raise questions; recent reports from professionals in the housing market suggest an increasing volume of transactions by investors, who (along with homeowners more generally) may be expecting the recent trend of price increases to continue.In other words, a BUBBLE!

I take some comfort from the continuing disagreement among close students of the market about whether houses are overvalued, and, given the widespread press coverage of this issue, from my expectation that people should now be aware of the risks in the real estate market.

A very interesting speech and an extension of recent hard landing discussion. (see macroblog for a summary here, here and here)

Oil Prices Hurting less Developed Countries

by Calculated Risk on 4/22/2005 11:26:00 AM

It appears that oil prices have started to slow the US economy. But less developed countries are really feeling the pinch. Speaking at the Asia-Africa summit in Jakarta, Indonesia, Philippine President Gloria Macapagal-Arroyo warned that oil prices could lead to a "global recession".

Arroyo told the meeting in Jakarta, featuring some of the world’s leading oil consumers, that unsustainable prices were driving many countries to the brink of financial instability.

“There’s no question that the rising price of oil has the potential to put the brakes on economic expansion,” Arroyo said, urging delegates to work together to “prevent such a crisis”.

The rising trend of oil prices could worsen to levels that could halt economic growth or even prompt global economic recession, Arroyo said.

“It is stripping oil-importing Asia and Africa of our ability to manage for global competitiveness. It is preventing us from pursuing our economic development programmes with vigor. It is requiring us to face the spectre of economic decline,” she said.

Philippine Foreign Affairs Secretary Alberto Romulo made similar comments at the ministerial meeting of the conference.

"The current trend in oil prices points toward a situation that could halt global economic growth and further widen the gap between the rich and poor countries," Romulo said.

Spot oil prices reached $55 per barrel earlier today.

Thursday, April 21, 2005

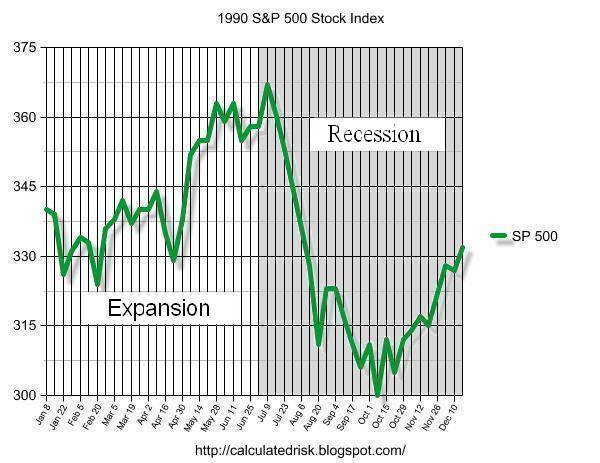

Markets and Recessions

by Calculated Risk on 4/21/2005 09:01:00 PM

It is common wisdom on Wall Street that the market predicts recessions. This story today quoted a market analyst as saying: "The market typically turns down six months to a year before a recession. We could be seeing a recession in 2006."

We might see a recession in 2006, but the markets are not a good predicting tool.

Click on graph for larger image.

Here is the DOW's performance before and after the start of the last 5 recessions. For each recession, the DOW's value was normalized to 100 12 months prior to the start of the recession. The graph shows the median value, and the minimum and maximum for the DOW.

The best that can be said for the market is that it is a solid coincident indicator of a recession.

Here is a graph from a previous post about recession indicators. This shows the SP500's performance and the 1990's recession. The SP500 rallied into the recession and only sold-off after the recession started.

This is another common Wall Street "wisdom" that is incorrect. UPDATE: Fixed typo on graph.

"There are serious pocketbook issues lurking in America"

by Calculated Risk on 4/21/2005 02:36:00 AM

"There are serious pocketbook issues lurking in America," said Rep. Jim Leach (R- Iowa).

On the front page of Thursday's Washington Post is this analysis by Weisman and Balz, "Economic Worries Aren't Resonating on Hill" The authors make the argument that main street concerns are being ignored by Washington and the media.

The disconnect between pocketbook concerns of ordinary Americans and the preoccupations of their politicians has helped send President Bush's approval ratings on the economy down, while breeding discontent with Congress.And more:

"Many are rather upset at the Terri Schiavo issue," [Rep. Vernon Ehlers (R-Michigan)] said, even "moderately pro-life" voters. "I'm getting a lot of the, 'Why are you spending time on that when we don't have jobs?' type of thing."And this piece only scratches the surface of the serious economic challenges facing America.

In Michigan, jobs and the economy have vaulted to the No. 1 concern of 34 percent of voters, with the closest other issues, health care and education, at a distant 15 percent, said Ed Sarpolus, an independent Michigan pollster. "I haven't seen anything like that since the early '90s and crime," he said.

Wednesday, April 20, 2005

RE Executives: The Boom that won't Bust

by Calculated Risk on 4/20/2005 10:04:00 PM

At the Milken Institute Global Conference 2005 in LA, several Real Estate executives argued that there is no real estate bubble. A few comments from the "Real Estate: Investing for the Future" panel:

"We're in a market with real depth and real legs on it," said M.D.C. Chief Executive Larry Mizel.

"The big boom of the last 10 years was not seen all through the United States," KB Home Chief Executive Bruce Karatz said. "There's a supply-and-demand balance that I think will stay good for many years."

"The housing bubble has been created more by the business press than reality," said Sam Zell, chairman of Equity Office Properties Trust and Equity Group Investments LLC. "You can't have a crash without oversupply."

I will address the supply issue in a future post. But the final comment from the article is worth highlighting:

"The executives pegged the southwestern U.S. and Florida as best real estate buys"Enough said.

The Economist on House Prices

by Calculated Risk on 4/20/2005 05:36:00 PM

The Economist asks: Will the walls come falling down?

A few excerpts:

The increasing riskiness of mortgages is not the only sign that America is experiencing a housing bubble. The ratio of house prices to rents is well above its historical average, as is the ratio of prices to median incomes. And people seem increasingly to be basing their house-buying decisions on the notion that the large capital returns of the past few years—house prices in America are up by 65% since 1997—will continue indefinitely. As with a stockmarket bubble, if this confidence is shaken, prices could begin to fall rapidly.More likely prices will deflate slowly over a multi-year period. Housing: After the Boom on Angry Bear looked at the impact on prices and volume transactions in previous busts. Prices deflated slowly, but transactions dropped precipitously.

A fall in American house prices could be bad news not just for American homeowners, but for the rest of the world. Robust American demand has supported export-driven growth in many economies, particularly emerging markets and Asia. If American consumers have to raise their abysmal savings rate, exporting nations will feel the pinch.

And finally this:

Most worryingly, a collapse in American export demand could trigger a vicious cycle. In order to keep their currencies low against the dollar, and thus boost exports to America, Asian central banks have been accumulating dollar reserves, which they have poured into Treasury bonds. This has increased the supply of capital in America, and thus been at least partly responsible for the borrowing binge that fuelled the housing boom. If house prices fall, and suddenly poorer Americans have to cut back on their purchases, this will shrink the supply of cheap credit from Asian central banks, pushing up interest rates and causing house prices to fall even further. Those who thought that housing was a haven may be in for a nasty surprise.Emphasis added.

For a diagram on how this might work, see Housing and Trade: Virtuous Cycle about to Become Vicious? Check out The Economist article and the interesting chart on the global nature of the housing boom.