RSS Feed

RSS Feed by Calculated Risk on 6/02/2005 07:08:00 PM

Thursday, June 02, 2005

Free Money: Part II

A couple of months ago, I wrote that they were giving away free money in The OC (Orange County, CA). At that time the median home price in OC was $555,000.

According to the OC Register, the mediam home price is now $585,000. That is a gain of $30,000 in just two months.

Prices are well on their way to local RE Broker Gary Watts' prediction of $70,000 in gains this year. Amazing.

Wednesday, June 01, 2005

No Housing Bubble?

by Calculated Risk on 6/01/2005 11:36:00 PM

Last week, Barry Ritholtz of The Big Picture wrote: "Don't Buy Housing Bubble Propaganda". I recommend it.

Today, Dr. Richard Rosen (Senior Economist Chicago Federal Reserve Bank) release a Fed Letter: "Explaining recent changes in home prices". Also worth reading.

Speculation, excessive leverage, loose lending practices are all evidence of a bubble.

Price Rent Ratio Update

by Calculated Risk on 6/01/2005 05:03:00 PM

OFHEO released their Q1 2005 report showing a 12.5% annual housing price increase nationwide over the past year. Kash on Angry Bear breaks down the data by key metropolitan areas and provides a graph of inflation adjusted house prices: New House Price Data.

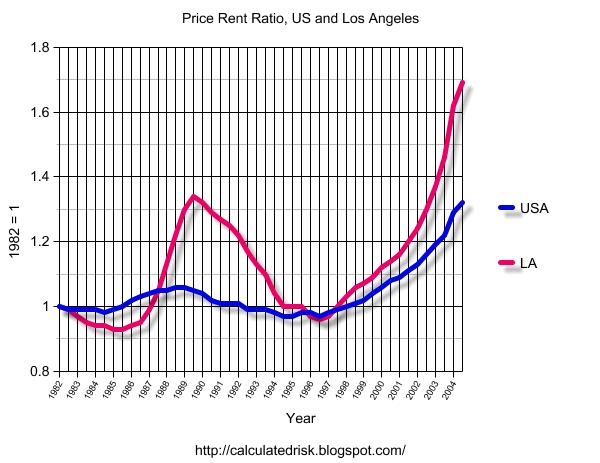

Another way to look at the data is to compare house prices vs. equivalent owner's rent for different areas of the Country. This measure of fundamental housing value, called the price-rent ratio, was suggested by the Federal Reserve's Krainer and Wei in "House Prices and Fundamental Value". The following graph shows the U.S. and Los Angeles price-rent ratios since 1982. The price component is from the OFHEO home price index and the rent series is from the BLS owner's equivalent rent index.

Click on graphs for larger image.

The LA housing bubble of the late '80s is very clear. After the bubble burst, it took several years for the Price-Rent Ratio to return to normal. For a graph of the LA bust see "After the Boom".

Krainer and Wei "found that most of the variance in the price-rent ratio is due to changes in future returns and not to changes in rents. This is relevant because it suggests the likely future path of the ratio. If the ratio is to return to its average level, it will probably do so through slower house price appreciation."

The owner's rent equivalent data series from the BLS starts in '97 for many areas. Using (1997 = 1) the following graph compares the Price-Rent ratio for Los Angeles, Washington D.C., Miami and Wichita / Peoria.

It should come as no surprise that LA, DC and Miami house prices are all significantly above the Owner's equivalent rent.

But is there a bubble in Peoria? The data suggests that housing in Peoria, Wichita, and Indianapolis are all about 15% overvalued. However I don't expect nominal price decreases in those areas. More likely is slow appreciation (below the inflation rate) for a few years until rents catch up with house prices.

The Price-Rent ratio suggests that housing is overvalued in most of the United States and significantly overvalued in the larger metropolitan areas.

OFHEO: House Prices Continue to Rise Rapidly

by Calculated Risk on 6/01/2005 11:13:00 AM

OFHEO released their Q1 2005 report: "House Price Index Shows a 12.5 Percent Increase Over the Past Year"

WASHINGTON, D.C. – Average U.S. home prices increased 12.50 percent from the first quarter of 2004 through the first quarter of 2005. Appreciation for the most recent quarter was 2.21 percent, or an annualized rate of 8.82 percent. The new data represent the largest four quarter increase since the third quarter of 2004, when appreciation surpassed any increase in over 25 years. The figures were released today by OFHEO Acting Director Stephen A. Blumenthal, as part of the House Price Index (HPI), a quarterly report analyzing housing price appreciation trends.

“The House Price Index shows the rise in house prices continues at an extremely strong pace and raises the potential for declines in some areas later on,” said OFHEO Chief Economist Patrick Lawler.

More to come ...

Tuesday, May 31, 2005

UK: Retail Sales Continue Slide

by Calculated Risk on 5/31/2005 09:00:00 PM

UK's retailers suffered their third consecutive month of declining sales, according to the Independent.

'...the CBI said retailers suffered their third successive monthly fall in sales - making it the worst quarter since the early recession of the early Nineties.More from the Independent:

There was a further blow for retailers from a survey showing the Bank Holiday weekend provided a lacklustre kick-start to half-term holiday trading. John Butler, the UK economist at HSBC, said: "Households no longer intend to make a major purchase. The big-ticket durable boom is over along with the boom in mortgage equity withdrawal."'

'The CBI survey, which covered 226 companies representing four out of 10 shops across the UK, said the number reporting a fall in sales compared with a year ago outweighed those seeing a rise by 7 per cent. This was an improvement from the balance of minus 14 per cent in April but left the rolling three-monthly average at its lowest level sinc e August 1992.

FootFall said the number of visitors to Britain's major shopping centres over the three-day weekend was 1.3 per cent lower than a year ago, driven by a 7 per cent slump in footfall on Monday.'

For more on the UK retail slump:

Times: Retailers expect slowdown to stay for summer

Financial Express: ‘UK retail sales fell again in May’

"Broadly speaking, the categories of goods most closely correlated with housing transactions have fared worse than the average over the past year," said John Longworth, executive director of ASDA and chairman of the CBI's survey panel.Retail Week: Retail sales fall for the third month

Asda executive director and chairman of the CBI's DTS panel John Longworth said: “Sales volumes improved between April and May, but volumes remain a little lower than a year ago and prices are on a downward trend.”It is possible that the UK is leading the US into an economic slowdown. On Angry Bear I presented a chart showing that the US Fed rate increases are about 6 to 8 months behind the BoE. In the UK it started with a housing slowdown and has now moved to retail.

"Sales of groceries, books and stationery are up on a year ago, but those of big ticket items, furniture, carpets, DIY goods and clothing are down,” he added.

Monday, May 30, 2005

Housing and M3

by Calculated Risk on 5/30/2005 01:47:00 AM

My weekly post is up on Angry Bear: Housing, the Fed and M3

Earlier I linked to Federal Reserve Vice Chairman Ferguson's remarks on housing.

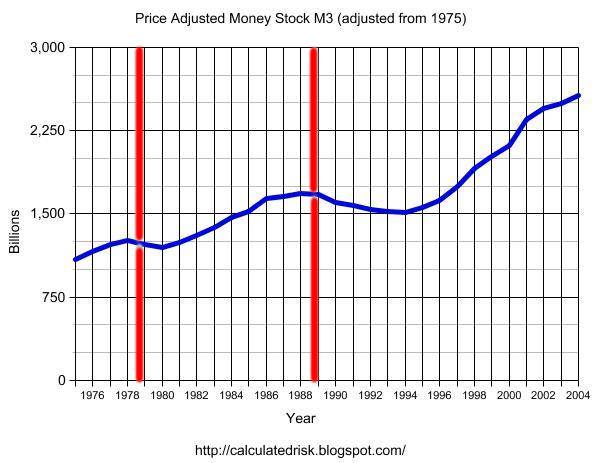

Click on graph for larger image.

Expanding on Dr. Ferguson's analysis, this graph shows price adjusted M3 since 1975. The vertical lines indicate when housing peaked in the previous cycles.

It is important to repeat Dr. Ferguson’s caution regarding not confusing correlation with causation, but it does appear that housing has peaked in the past when price adjusted M3 has peaked.

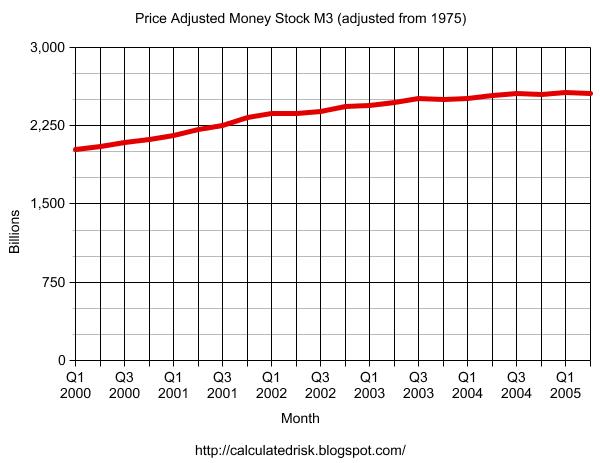

And the second graph shows price adjusted M3 since Q1 2000. It appears that M3 is peaking right now.

We will have to wait to see if housing is peaking. But one thing is certain, the number of articles on housing is setting new highs!

See my previous posts and Patrick's links for a list of recent articles.

Sunday, May 29, 2005

More Housing Articles

by Calculated Risk on 5/29/2005 02:20:00 AM

This weekend has seen a plethora of articles on housing. I posted some links earlier, and you can always check Patrick's site for housing related links.

UPDATE2: A Bane Amid The Housing Boom: Rising Foreclosures

"Philadelphia, its suburbs and indeed much of Pennsylvania have experienced a foreclosure epidemic as low-income homeowners take on mortgage debt they cannot afford. In 2000, the Philadelphia sheriff auctioned 300 to 400 foreclosed properties a month; now he handles more than 1,000 a month. Allegheny County, which includes Pittsburgh, had record auctions of foreclosed homes, and officials speak of a "Depression-era" problem."

UPDATE: See General Glut's comments on another NY Times housing article.

Here are four more:

University of Michigan: Back to the future

Home sales have again reached new peaks as consumers have seamlessly shifted from the irresistible enticement of record low mortgage rates to the equally irresistible temptation of purchasing in advance of rising mortgage rates and home prices. More consumers favored buying homes in advance of anticipated increases in mortgage rates and prices in the May survey than at any other time in the last decade. "Attitudes toward home buying conditions have recently displayed nearly all of the characteristics of earlier bouts of advance buying, a reaction that has typically generated an economic bust following an extended boom," Curtin said. The last time the survey recorded a comparable number of references to advance buying was in 1988-89, more than two years before home prices began to decline in some areas of the country.

LA Times: It's Not a Bubble Until It Bursts

The chief economist for the Mortgage Bankers Assn. is worried enough about the torrid housing market to get out of it.And more:

"I'm going to rent for a while," said Douglas Duncan, who expects "significant reversals" in regions that have enjoyed strong home price appreciation, including Washington, D.C., Florida and California. He plans to sell his suburban Washington home, which has tripled in value since he bought it a dozen years ago, and move into an apartment.

A widely followed University of Michigan consumer survey, released Friday, showed that 24% of respondents nationwide said it was a good time to buy a home because prices would rise. That was the highest percentage since 1988 — right before prices peaked in the previous real estate cycle.

"These are powerful engines creating a boom in home sales, and all booms end the same way," Richard Curtin, director of the survey, said in a statement.

WaPo: The Interest-Only Trap

There's another group of home buyers opting for interest-only loans -- people looking for the lowest mortgage payment possible who probably wouldn't qualify for the house they want with a loan payment that included the interest and principal.

It's that last group of people that worries me the most -- home buyers who are just barely squeezing into a house with an interest-only loan.

"I am not sure that any loan which enables someone to dig their financial grave is good, and I wish that underwriters would realize that," Armstrong said.

Boston Herald: Bank on a bust, not longer boom

The problem: The dynamic of "advance buying" - that rush to buy homes before spiking prices and interest rates make it too late.

It's a tell-tale sign of a coming collapse, Curtin (director of the University of Michigan's Survey of Consumers) says.

"Attitudes toward home-buying conditions have recently displayed nearly all the characteristics of earlier bouts of advance buying,'' Curtin said in a press release Friday, calling it a reaction that has ``typically generated an economic bust."

Saturday, May 28, 2005

NYTimes: Hear a Pop? Watch Out

by Calculated Risk on 5/28/2005 11:35:00 PM

Earlier, on Angry Bear, I tried to quantify the impacts of a housing slowdown on the general economy (See: After the Housing Boom: Impact on the Economy). This NYTimes article asks the same question:

"[W]ould a real estate crash really matter to the country as a whole?Then the article does an excellent job of discussing some of the impacts of declining prices: declining wealth effect, end of equity withdrawal, and much more ...

In a word, yes. To understand why, first look at how pervasive the effects of real estate are throughout the economy."

"But that's not all. The housing sector has even broader effects on the economy, by some estimates accounting for 25 percent of all activity. A decline in property values would most likely lead to declines in other industries, like construction, brokerage, banking and insurance. And these are important for future growth. Construction, for example, amounts to 4 percent to 5 percent of the economy, according to the Bureau of Economic Analysis.For these reasons I'm concerned about the impact of the coming housing bust on the general economy.

Then there's banking. Because of the leverage associated with real estate, a fall in values would affect banks and other lenders. It would probably lead to tightened credit standards, less lending and higher interest rates. If lenders begin to suffer steep losses, there is always the danger of financial contagion, in which problems at one institution ripple out to others it does business with.

And there's a new wild card for the economy. In 2004, adjustable-rate mortgages made up a third of new mortgage originations. No one knows what the effect of the widespread use of A.R.M.'s would be in a down market. A climb in interest rates, of course, would put downward pressure on real estate prices, but A.R.M. borrowers would feel the pinch rapidly. If those borrowers started to default, lenders would be hurt."

Friday, May 27, 2005

Fed's Ferguson: Housing Prices High

by Calculated Risk on 5/27/2005 07:03:00 PM

"In a scenario of collapse, the damage to balance sheets and private wealth could go as far as undermining the soundness of the financial system and threatening stability of the real economy." Federal Reserve Vice-Chairman Roger Ferguson, May 27, 2005

Federal Reserve Vice-Chairman Roger Ferguson made several comments on housing in prepared remarks to a conference sponsored by the Bundesbank in Berlin. A few excerpts:

"A particular phenomenon that touches on all these issues is the movement of asset prices, especially the prices of equities and residential real estate. Because these assets are the most widely held by the general public, price changes, even when not exceptional, can significantly affect the macroeconomy. Rising asset prices support household consumption, whereas falling asset prices damp consumption. In a scenario of collapse, the damage to balance sheets and private wealth could go as far as undermining the soundness of the financial system and threatening stability of the real economy." ...

"For housing, rent-to-price ratios and income-to-price ratios are commonly used measures to assess valuation. Over the past several years, both measures have decreased sharply in many countries, and they currently are well outside historical ranges in some countries. In 2004, U.S. home prices increased 11.2 percent, their fastest pace since 1979, and right now, housing prices in many markets in the United States are relatively high when judged by conventional valuation measures"See Speech for more.

And UPDATE: a few articles on the housing market:

Economists Wary of Interest-Only Loans

Is Your House Overvalued?

Is There a Bubble In Florida Waiting to Burst?

Is U.S. housing market a 'bubble' waiting to burst?

Thursday, May 26, 2005

WSJ: House of Cards?

by Calculated Risk on 5/26/2005 11:00:00 PM

UPDATE: Recommended reading: Running Out of Bubbles by Paul Krugman, NYTimes.

Original post:

The first paragraph is priceless:

Watching the housing market is sort of like a game of Clue before the murder. The victim is still alive and well, but we know he's going down. After the housing market is cold, it should be easy to finger the perpetrator. But for now, we're left to guess (Colonel Greenspan in the conservatory with the lead pipe?), and the perp might not be whom we expect.The last line is a reminder of the difficulty in calling a top:

The Wall Street Journal, March 6, 2000:

"... for now, the frothy buying conditions in some of the nation's biggest housing markets, especially for high-end-homes, worry economists, who remember how the housing market crashed in the late 1980s after some markets overheated."I wasn't concerned about housing in 2000; there was little or no speculation. I am concerned today.