RSS Feed

RSS Feed by Calculated Risk on 1/30/2006 02:04:00 PM

Monday, January 30, 2006

30 year Pleasure Boat Loans

The LA Times reports: Sales of Pleasure Boats Buoyed by Soaring Home Values

California's hot real estate market has helped power a rise in boat sales by allowing people to borrow against the soaring value of their homes to buy boats and other big-ticket items.A couple of comments: I guess a 30 year loan on a pleasure boat is better financial planning than a 30 year loan for a hamburger!

In California, retail sales of recreational boats — from runabouts to $4-million luxury yachts — rose about 8% last year to a record $540 million, continuing a growth trend over the last five years, according to the Southern California Marine Assn. A similar increase is expected in 2006.

Though some economists worry that too many people are overextending themselves, the boating industry considers itself lucky that business is humming despite high gasoline prices.

"A lot of people are taking money out of their homes and buying different things, and one of them — fortunately — is boats," said Dave Geoffroy, executive director of the marine association, the organizer of the L.A. Boat Show.

But what happens when mortgage equity withdrawal slows?

... some dealers worry that boat sales could fall if real estate values drop, which happened in the early 1990s.I wonder if the slowdown in Q4 (1.1% annualized growth in GDP) was related to a slowdown in equity extraction? The Federal Reserve's Flow of Funds report (due March 9th) will help answer that question.

"I'm moderately concerned," said Michael Basso Jr., general manager of Sun Country Marine, which sells family boats and has locations in Castaic, Dana Point and Ontario.

He noted that half his buyers last year paid in cash, often from money they pulled out of their homes.

Friday, January 27, 2006

December New Home Sales: 1.269 Million Annual Rate

by Calculated Risk on 1/27/2006 12:16:00 AM

According to the Census Bureau report, New Home Sales in December were at a seasonally adjusted annual rate of 1.269 million vs. market expectations of 1.225 million. November's sales were revised down slightly to 1.233 million from 1.245 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

The Not Seasonally Adjusted monthly rate was 86,000 New Homes sold, essentially the same as the 85,000 in November.

On a year over year basis, December 2005 sales were 3.6% higher than December 2004.

The median and average sales prices are trending down.

The median sales price of new houses sold in November 2005 was $225,200; the average sales price was $283,300.

The seasonally adjusted estimate of new houses for sale at the end of December was 516,000. This represents a supply of 4.9 months at the current sales rate.

The 516,000 units of inventory is the all time record for new houses for sale. On a months of supply basis, inventory is above the level of recent years.

This report is still reasonably strong.

Thursday, January 26, 2006

Lenders ask for Extension on New Mortgage Guidance

by Calculated Risk on 1/26/2006 01:14:00 AM

In December the FDIC, Office of the Comptroller, the Federal Reserve and other agencies issued a new proposed guidance on nontraditional mortgage products.

Now Reuters reports: US banks seek more mortgage proposal comment time

Lenders this week asked U.S. regulators to extend a comment period on a proposal that urged tighter underwriting on new mortgage products that may pose greater risks for banks and borrowers as interest rates rise.

Comments were due Feb. 27, but lenders have asked the Federal Reserve and other regulators for 30 more days.

"The proposal is extremely complex and has far-reaching consequences for our members, as well as for the nation's mortgage markets," wrote Janet Frank, director of mortgage finance in America's Community Bankers' government relations office.

"We believe that it will take an additional 30 days to complete the necessary evaluation and collect comments and data from our membership," Frank told regulators in a letter.

The Consumer Mortgage Coalition and HSBC North America Holdings Inc. also requested an additional 30 days.

Spokesmen for the Fed and Office of the Comptroller of the Currency were not immediately available to comment.

Wednesday, January 25, 2006

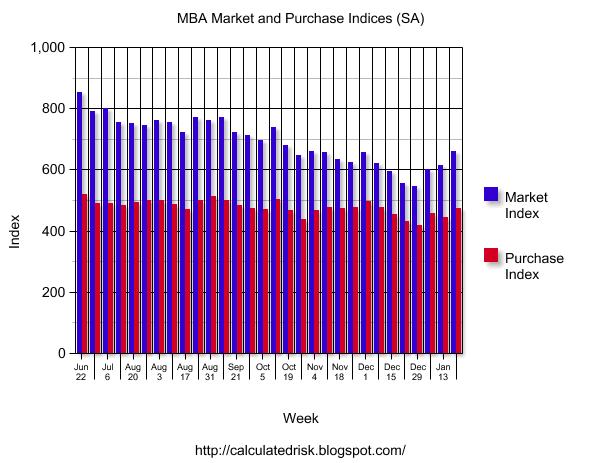

Mortgage Application Volume Up

by Calculated Risk on 1/25/2006 10:46:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Up In Latest Survey

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 660.5 -- an increase of 7.7 percent on a seasonally adjusted basis from 613.3 one week earlier. On an unadjusted basis, the Index decreased 0.2 percent compared with the previous week and was down 0.4 percent compared with the same week one year earlier.Rates on fixed mortgages decreased slightly again, but ARM rates increased:

The seasonally-adjusted Purchase Index increased by 6.7 percent to 473.7 from 443.9 the previous week whereas the Refinance Index increased by 7.8 percent to 1773.9 from 1645.2 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.04 percent from 6.07 percent on week earlier ...The MBA survey indicates RE activity is still at a fairly high level and rebounding in January.

The average contract interest rate for one-year ARMs increased to 5.44 percent from 5.39 percent one week earlier ...

Existing Home Sales Fall

by Calculated Risk on 1/25/2006 10:27:00 AM

The AP reports: Existing Home Sales Set Record but Cooling

Sales of existing homes set a record for a fifth straight year in 2005 even though the year ended on a weaker note with three straight monthly declines, sending a strong signal that the nation's housing boom is beginning to cool.From the NAR:

The National Association of Realtors reported that sales of previously owned homes and condominiums dropped by 5.7 percent in December compared to the sales pace in November. It marked the third consecutive monthly decline, something that has not occurred in more than three years.

Existing home sales fell to a 6.6 million annual rate in December, 3% lower than December 2004.

Inventories fell to 2.796 million units, from 2.924 units in November, as sellers took their houses off the market for the holidays. However, inventories are up 26.3% compared to December 2004. This represents of 5.1 months of supply at the current sales rate.

The average and median prices fell to levels not seen since May 2005. Average prices were up 7.4% for the year, and median prices up 10.5%.

Tuesday, January 24, 2006

Fed Economist: Current Account Deficit near Optimal Levels

by Calculated Risk on 1/24/2006 08:54:00 PM

Federal Reserve economist John Rogers (Chief, Trade and Financial Studies Section) and University of Wisconsin Professor Charles Engel, in a new paper "The U.S. Current Account Deficit and the Expected Share of World Output", Journal of Monetary Economics suggest the US Current Account Deficit may be near optimal levels.

From their conclusions:

We have asked whether the U.S. current account deficit could be consistent with expectations that the U.S. share of world GDP will increase. Under assumptions about the growth in the net GDP share that are not wildly implausible, the level of the deficit can be consistent with optimal saving behavior. But, in making this assessment, we emphasize that there are many difficult issues to deal with, and the conclusion is sensitive to how one handles these questions.

First, our findings are sensitive to how we treat two problems: the high saving rate in East Asian emerging economies, and the "exorbitant privilege" (the term used by Gourinchas and Rey (2005)) that allows the U.S. to receive a much higher return on its foreign investments than foreigners earn on their U.S. investments.

On the first point, most forecasters predict that the emerging market's share of world GDP will be increasing over time. Our empirical work does not include these countries, and if it did, the forecast path of the U.S. share of world GDP would not be as rosy. But, according to themodel, these countries ought to be borrowers in international capital markets. They are not -- they are large net lenders. It is puzzling that they are net lenders. Bernanke (2004) refers to this as a "savings glut", and hypothesizes that these countries are in essence building up a nest egg in order to protect them against a possible future international financial crisis such as the one that beset East Asia in 1997-1998.

We are not sure how to handle this in our model. It may be that these countries will continue to be high savers, in which case their saving will hold down world interest rates and the U.S. deficits will be more justifiable. On the other hand, their saving rate may fall and real interest rates may rise, which works toward the U.S. optimally having a smaller deficit.

We make the "heroic" assumption in our work that these countries are not contributing to net world saving at all. On the one hand, this is a conservative assumption (if one is trying to explain the large U.S. deficits), because the countries are in fact large net savers. On the other hand, if their net saving is reversed, the assumption is too optimistic.

It does seem like markets favor the position that these countries will maintain their positions as large savers, because long term real interest rates are very low. However, much of the recent scholarly and policy-oriented research on the U.S. current account deficit has taken the position that the markets may not be correctly foreseeing events.

Finally, it is possible that the saving rate is high in East Asian countries because of demographic factors. It has been noted that because of the one-child policy, the ratio of old to young is increasing rapidly in China. There are other countries for which demographic factors may be very important as well, and this deserves further study.

We take a similar neutral position on the exorbitant privilege. One possibility is that the U.S. will continue to receive higher returns on its foreign investments than it pays out on its foreign borrowing. On the other hand, that privilege may disappear, and worse, it may disappear not only for future borrowing but also for our outstanding debt when it is refinanced. Our work takes a somewhat neutral position by assuming future borrowing and lending takes place at the same rate of return, but that there is no additional burden to be encountered from refinancing existing debt at less favorable rates of return.

There really are a variety of scenarios that could play out. As Gourinchas and Rey (2005) demonstrate, it is not only that the return on U.S. assets within each asset class is lower than on foreign assets (implying the market views U.S. assets as less risky), but also that the mix of U.S. investments abroad favors riskier classes of assets. It is possible that the U.S. net return will fall in the future both because the risk premium on U.S. assets rises (as in Edwards (2005) or Blanchard, Giavazzi and Sa (2004)), and because foreigners shift toward investing in more risky U.S. assets. But, again, it is notable that markets do not reflect any increasing riskiness of U.S. assets.

With these major caveats in mind, we find that the size of the U.S. current account deficit may be justifiable if markets expect further growth in the U.S. share of advanced-country GDP. The growth that is needed does not appear to be implausible.

But, what the model cannot explain is why the U.S. current account deficit continues to grow. If households expect the U.S. share of world GDP to grow, they should frontload consumption. The deficits should appear immediately, not gradually.

We have allowed in our Markov-switching model for the possibility that there was a shift in regime that U.S. households only gradually learned about. But that turned out not to be able to explain the rising U.S. current account deficits. However, our simulations and estimation assumed that households understood that if a regime shift took place, the U.S. share of world GDP in the long term would be much higher than it was in the early 1980s. In practice, it may be that markets only gradually learned the U.S. long-term share. Examination of the model when there is only gradual learning about the parameters of the model will be left for future work. It is possible that because U.S. households only gradually came to the realization that their share of advanced country GDP was going to be much higher in the long run, they only gradually increased their borrowing on world markets.

This possibility is supported by our examination of the consensus long-term forecasts of U.S. GDP relative to G-7 GDP since 1993. These forecasts have consistently underestimated U.S. GDP growth relative to other countries, by wide margins. The current forecasts for the future, however, show that the markets expect a large increase in the U.S. share of GDP – almost precisely the amount that we calculate would make the current level of the deficit optimal.

There are at least two other possible explanations to explain this gradual emergence of the current account deficit. One possibility is that it takes time for consumption to adjust. This could be modeled either with adjustment costs, or, as is popular in many calibrated macro models, with habit persistence in consumption.

Another possibility is that there has been a steady relaxation of credit constraints for many U.S. households, as well as increased access to U.S. capital markets for foreign lenders. The relaxation of credit constraints was one of the possibilities that Parker (1999) explored in his study of the decline in U.S. saving. He found that it could explain at most 30% of the increase in consumption from 1959 to 1998.

The starting point of Parker's back-of-the-envelope calculation is the observation that the consumption boom is the equivalent of three-quarters of one year's GDP in present value terms. The rise in debt, as measured by the difference in ratios of household total assets to income and net worth to income, was about 20 percent over the period. Therefore, debt can explain at most .20/.75 < 30 percent of the increase in consumption. Since the time Parker wrote his paper, debt has continued to rise, by another 25% through 2005Q2 when the ratio of total assets to income exceeded the ratio of net worth to income by 1.24.

Of course, the other obvious candidate for the increasing U.S. current account deficit is through the effect of U.S government budget deficits. It is useful to note that what we are really talking about is the effects of tax cuts. In the first place, government spending as a share of GDP has not changed dramatically, so could not account for the large current account deficit. Moreover, our analysis allows for the effects of increases in government spending. An increase in current spending above the long-run spending levels would lower the U.S. share of GDP net of government spending and investment relative to future shares, thus inducing a greater consumption to net GDP ratio.

But our model assumes that the timing of taxes does not matter for household consumption -- that Ricardian equivalence holds. Obviously that might not be correct. Recent empirical studies do not show much support for Ricardian equivalence, though the point is debated.8 We note that to the extent that credit constraints have been relaxed in recent years, Ricardian equivalence becomes a more credible possibility. It may be that in more recent years, lower taxes do not boost consumption as much, and instead allow households to pay off some of their credit card debt or prepay some of their mortgage. It may be interesting to pursue empirically the hypothesis that the effects on national saving of tax varies change with the degree of credit constraints in the economy.

Another argument that needs to be explored is the distributional effects of the recent tax cuts. It has been argued that the tax cuts were less stimulative than previous cuts because they accrued mostly to wealthy individuals, who simply saved the additional after-tax income. (That is, the rich act more like Ricardian consumers.) But if that is the case, then it is more difficult to make the case that the tax cuts are responsible for the decline in U.S. national saving.

Finally, we cannot reach firm conclusions about the future path of U.S. real exchange rates. We have calibrated a model that is essentially identical to the one examined by Obstfeld and Rogoff (2004), but one in which the consumption path is determined endogenously as a function of current and expected discounted real income in each country. We found that under one set of baseline assumptions, there should not be much change in the equilibrium real exchange rate as the U.S. current account adjusts. Our model assumes the U.S. will experience higher growth in productivity in both traded and non-traded sectors, and that there is factor mobility between the traded and non-traded sector. On the one hand, if traded/non-traded productivity growth in the U.S. is slightly higher than in the rest of the world, the price of non-traded goods will rise in the U.S. from the Balassa-Samuelson effect. On the other hand, the U.S. terms of trade should fall as the supply of its exports increases. If there is home bias in consumption of tradables, that would work toward causing a U.S. real depreciation. In our baseline calibration, these two effects approximately cancel.

But as we have noted, the conclusions about the real exchange rate depend on assumptions about parameters of the model. Particularly, if the elasticity of substitution between imports and exports in consumption is much lower than our baseline simulation assumed, the U.S. could experience a substantial real depreciation over the next 25 years.

The basic message of our paper is that there are many aspects of the current account adjustment that are just not possible to predict. Under some scenarios that we do not regard as entirely unreasonable, we find that the U.S. current account deficit can be explained as the equilibrium outcome of optimal consumption decisions. But some of our modeling simplifications and assumptions might be wrong in important ways, and so it may turn out, as many have been warning, that the deficits have put the U.S. on the path to ruin.

Dr. Setser on Rubin and a Hard Landing

by Calculated Risk on 1/24/2006 06:23:00 PM

Dr. Brad Setser excerpts from Robert Rubin's Wall Street Journal OpEd and adds some interesting commentary. Setser writes:

Thomas Palley is right: "Foreign flight" (a shock to the United States ability to borrow savings from abroad) is very different from "Consumer burnout" (a slowdown in US demand growth). In both the foreign flight and the consumer burnout scenarios, the US economy slows and the dollar falls. But in the foreign flight scenario, as Palley notes, the fall in the dollar and rise in US (market) interest rates triggers the US slowdown, while in the consumer burnout scenario, the US slump triggers dollar weakness. Foreign flight would combine dollar weakness with higher US (market) interest rates, consumer burnout combines dollar weakness with lower interest rates.A housing market slowdown, and lower mortgage equity withdrawal, might lead to "consumer burnout". This is a potential problem right now for the US economy. But the addition of "foreign flight" might lead to a vicious cycle on the downside.

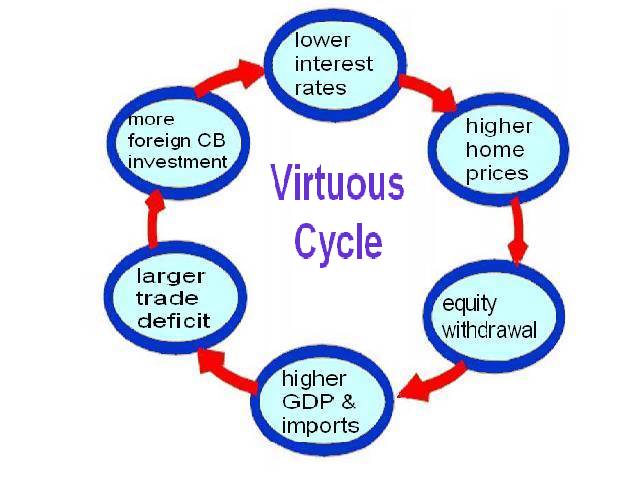

Click on diagram for larger image.

Click on diagram for larger image.This diagram is from an earlier post. The diagram depicts a virtuous cycle that might have been occurring over the last few years. Lower interest rates leads to higher housing prices and this leads to more equity withdrawal, higher consumption and more imports. Flush with cash, foreign CBs invest in dollar denominated bonds leading to lower interest rates ... and the cycle repeats.

Unfortunately, as the second diagram depicts, this has the potential to become a vicious cycle as housing slows. As Dr. Setser concludes:

But as US rates start to fall, foreign investors lose interest in lending even more to the US. Rather than adding $1 trillion or so to their portfolio of dollar denominated bonds at 4.5%, they want to add only say $600 billion or so ... Reduced foreign demand for US dollar assets ends up pushing US interest rates up.Of course, this was my top economic prediction for 2006:

At least those interest rates that are set in the market. The Fed's response to consumer burnout could trigger foreign flight.

That is a bad scenario. It implies that the US economy wouldn't benefit from some of the stabilizers that normally buffer the US from really bad (economic) outcomes.

I think long rates will start to rise when the Fed starts cutting the Fed Funds rate.Also, see Dr. Kash's post today: Will the Fed Overshoot?

This will be Bernanke's "conundrum"! As the economy slows, this will reduce the trade deficit and also lower the amount of foreign dollars willing to invest in the US - the start of a possible vicious cycle.

Monday, January 23, 2006

HSBC Economist: Housing Slowdown Could lead to US Recession

by Calculated Risk on 1/23/2006 08:48:00 PM

From a Financial Times article: Prospect of housing downturn casts pall over US economy

The ratio between average income and the costs associated with buying a home has risen to record levels. "Strong price growth momentum has resulted in very high prices relative to incomes across the country," says Ian Morris, chief US economist at HSBC.The article offers other views too. The data later this week might be interesting.

...

Mr Morris says a "bubble zone" has been created where house prices are overvalued by 35-40 per cent, equivalent to $6,000bn. Although this bubble could take time to deflate, Mr Morris warns that "the consequences of a punctured housing bubble could be traumatic". Even a soft landing of zero house price growth, he says, will dry up the mortgage equity withdrawal that has fuelled consumer purchasing. Consumer spending makes up two-thirds of the US economy.

So could a bursting of the housing bubble pull the US economy into recession?

Mr Morris says yes. "If this adjustment can be managed over many years, the economy can avoid recession. If the process is squeezed into a shorter time-frame instead, then recession is probable."

Gallup: America Turning Blue

by Calculated Risk on 1/23/2006 05:16:00 PM

On Angry Bear, I reported the newest Bush Approval (actually disapproval) ratings.

Now Gallup reports: Many States Shift Democratic During 2005

Click on map for larger image.

Note: Gallup doesn't normally interview in Hawaii and Alaska. I added both states.

This shift is probably due to the dissatisfaction with Bush's policies. It will be interesting to see if this translates to Democrat victories later this year.

Sunday, January 22, 2006

WaPo: Debt makes Greenspan's Legacy Unclear

by Calculated Risk on 1/22/2006 10:24:00 PM

In Monday's WaPo: As U.S. Economy Has Thrived, So Has Debt

"The jury is out on his legacy in large part because of the debt" and the trade deficit, said Stephen S. Roach, chief economist at Morgan Stanley. "You will not be able to truly judge his accomplishments until we see how this plays out in the post-Greenspan era."The article offers these examples:

· U.S. household debt hit a record $11.4 trillion in last year's third quarter, which ended Sept. 30, after shooting up at the fastest rate since 1985, according to Fed data.The debt binge has definitely contributed significantly to the current recovery. The big question is what happens next?

· U.S. households spent a record 13.75 percent of their after-tax, or disposable, income on servicing their debts in the third quarter, the Fed reported.

· The trade deficit for last year is estimated to have swollen to another record high, above $700 billion, increasing America's indebtedness to foreigners.