RSS Feed

RSS Feed by Calculated Risk on 2/07/2006 07:46:00 PM

Tuesday, February 07, 2006

WSJ Econoblog: Stitching a New Safety Net

Economics Professors Andrew Samwick and Mark Thoma discuss retirement and health insurance in today's WSJ econoblog: Stitching a New Safety Net.

Dr. Polley's take on the debate:

I really enjoyed reading this Econoblog, and I'll tell you why. Mark Thoma and Andrew Samwick do an outstanding job of showing the Wall Street Journal readers how economists can have a debate on a controversial subject like this. The reader can clearly identify the points of agreement and disagreement. Mark nails the question: How much social insurance should be provided by the government and how much should be provided by markets. They both note the market failures in health insurance. Samwick calls attention to the way the tax code distorts the private insurance market. By identifying the questions and highlighting specific economic issues of incentives, efficiency, and equity, they generate a lot of light and surprisingly little heat.I believe the two most pressing financial problems facing America are the structural General Fund deficit and health care. This discussion provides an excellent starting point for any debate on reforming health care.

Housing: PLEASE Buy this house

by Calculated Risk on 2/07/2006 12:16:00 PM

The Pioneer Press offers a few cautionary tales: Sellers juggle mortgages in tough market

[Bonnie] Cordy and her husband moved to Tennessee last year for his job. They rented an apartment until their new $325,000 house was ready in June. All the while they were making a mortgage payment in Minnesota.

The Apple Valley town home they'd originally listed at $329,900 in December 2004 wasn't selling, even after they dropped the price more than $20,000.

"I felt nervous as we were finishing up the house down here," she said. "There was no way to swing it all."

They dipped into retirement savings for the month or two they had double mortgage payments and taxes.

Then they switched to another agent, who slashed the price another $30,000. It finally sold at the end of August for $291,900, which was about $35,000 less than what they paid in 2003. She figures they lost another $5,000 in retirement savings.

"It's money we'll never get back again," said Cordy, 48.

Monday, February 06, 2006

National Debt: $10 Trillion When Bush Leaves Office

by Calculated Risk on 2/06/2006 03:39:00 PM

Today Bush submitted a budget for fiscal 2007 projecting a budget deficit of over $600 Billion. From AP:

The administration in its budget documents said the deficit for this year will soar to an all-time high of $423 billion, reflecting increased outlays for the Iraq war and hurricane relief.The article is referring to the Enron style unified budget deficit. The on-budget or General Fund deficit will be approximately $200 Billion more reflecting the surplus from Social Security Insurance. This means the projected General Fund deficit for 2007 will be over $600 Billion.

National Debt

The current National Debt is $8.195 Trillion. At $600 Billion per year, the Bush Administration will add $1.8 Trillion to the National Debt over the next 3 years. That will put the National Debt at approximately $10 Trillion when Bush leaves office - a stunning legacy.

Friday, February 03, 2006

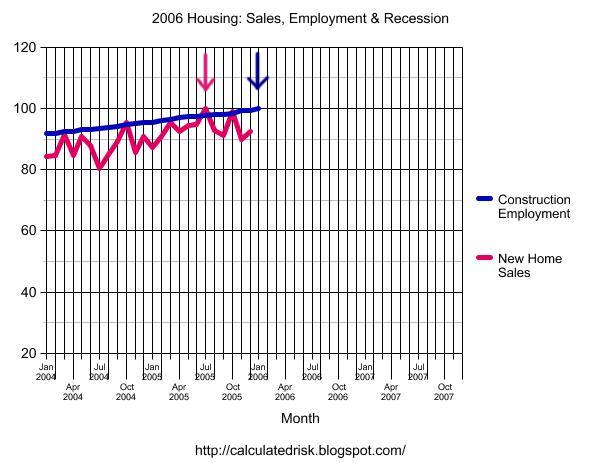

Housing: Sales, Employment and Recessions

by Calculated Risk on 2/03/2006 09:06:00 PM

Today's BLS employment report once again showed strong gains for construction employment. Dr. Kash noted this in his post: Job Growth by Industry

"Interestingly, construction employment still seems to be growing robustly, despite some concerns that the real estate market is cooling off; 46,000 of the new jobs created last month were in construction."Here is a look back at the last consumer recession (1990-1991):

Click on graph for larger image.

NOTE: New Home Sales and Construction employment were normalized to 100 for each peak (see arrows). The '90/'91 recession is in gray according to the NBER dates.

New Home Sales peaked in July of 1989 and construction employment peaked six months later in January of 1990. The recession started in July of 1990.

The 2nd graph is looking at the current situation. It appears New Home Sales peaked in July 2005, although October 2005 was very close. It might take a few more months and a few revisions to determine the actual peak.

If the peak did occur in July 2005, then January 2006 would be six months later - a similar lag in employment just like the early '90s. Of course, no two slowdowns are exactly alike.

So far the housing market is following a predictable pattern: rising inventories followed by a decrease in transactions and finally falling prices (like the early '90s in California, Massachusetts and other bubble areas). Housing related employment lags the peak in housing sales.

There are other factors that make the current situation more dangerous: a larger area of "frothy" prices, more leverage and use of exotic loans, and far more equity withdrawal (that supported consumer spending). On the other hand, in the early '90s, there was a huge shift away from defense work (the "peace dividend") and that impacted both California and Massachusetts.

I'll be watching construction employment over the next few months, and I expect to see a reduction in housing related employment.

ISM Report

by Calculated Risk on 2/03/2006 02:50:00 PM

Institute for Supply Management reports: Business Activity at 56.8%.

"Non-manufacturing business activity increased for the 34th consecutive month in January," Kauffman said. He added, "Business Activity and New Orders increased at slower rates in January than in December. Imports, Employment and New Export Orders also increased at slower rates while Prices increased at the same rate as in December. Eight of 16 non-manufacturing industry sectors report increased activity in January compared to 11 that reported increased activity in December. While in almost all indexes growth declined in January, they are still above the value of "50" indicating that growth continues, but at slower rates of growth. Members' comments in January continue to be generally positive concerning current business conditions. Several members mention concerns about the continued high level of energy prices and rising interest rates. The Prices Index held steady this month, but remains in a historically high range for the ISM Non-Manufacturing Business Survey. The overall indication in January is continued economic growth in the non-manufacturing sector, but at slower rates of increase."The weakest industries were: Agriculture; Wholesale Trade; Real Estate; Retail Trade; and Construction. This might be a hint of the housing slowdown, although the BLS numbers showed construction employment was solid in January.

Some of the details are interesting:

| Index | Jan. | Dec. | Change | Direction | Rate |

| Business Activity / Production | 56.8 | 61.0 | -4.2 | Increasing | slower |

| New Orders | 56.0 | 62.2 | -6.2 | Increasing | Slower |

| Employment | 51.1 | 56.9 | -5.8 | Increasing | Slower |

| Supplier Deliveries | 54.5 | 56.5 | -2.0 | Slowing | Slower |

| Inventories | 55.0 | 56.0 | -1.0 | Increasing | Slower |

| Prices | 67.2 | 67.2 | 0 | Increasing | At same rate |

| Backlog of Orders | 52.5 | 54.0 | -1.5 | Increasing | Slower |

| New Export Orders | 58.0 | 61.5 | -3.5 | Increasing | Slower |

| Imports | 49.5 | 56.5 | -7.0 | Decreasing | From Increasing |

| Inventory Sentiment | 63.0 | 59.0 | +4.0 | "Too High" | Greater |

Many activities are still increasing, but at a slower rate than in December. Employment is barely increasing (51.1) and prices are perceived to be a problem. Inventory sentiment is to too high and increasing at a greater rate. And imports are now decreasing (slightly). All signs that the expansion may be past its peak.

Employment Report

by Calculated Risk on 2/03/2006 01:32:00 PM

The employment report was mostly ho hum. The exception was the drop in the unemployment rate to 4.7%.

Click on graph for larger image.

This graph shows employment growth for Bush's second term. So far job growth has been about as expected. So why has the unemployment rate decreased?

The answer has to do with the employment participation rate. Over the last 5 years, the civilian noninstitutional population has added about 2.7 million people per year (those 16 years and over). Over the last 12 months the population has added 2.716 million - in line with previous years.

However, over the last 5 years, only about 1.2 million people per year have joined the civilian labor force. This is very puzzling, especially since it is unlikely that the baby boomers are retiring in significant numbers yet. More likely there is a fairly large group of people that would choose to join the labor force with higher incentives. Therefore I think, even with a 4.7% unemployment rate, there is still substantial slack in the labor market and the US will not see wage inflation pressures in the short term.

Once again, construction played a significant role in employment gains. For more, see Kash's Job Growth by Industry.

Thursday, February 02, 2006

US housing bubbles: Half froth?

by Calculated Risk on 2/02/2006 03:06:00 PM

The New Economist reviews the HSBC report: A Froth-Finding Mission: detecting US housing bubbles

The report itself concludes that the "glass is half froth":The New Economist is not overly concerned:

We suggest that about half of the US housing market is frothy and that this ‘bubble zone’ may be overvalued by as much as 35-40%, after taking into account low interest rates and tax advantages. Current valuations imply a large permanent reduction in the risk premium and/or a sizable step up in future capital gains, not all of which, we think, is justified. ... Therefore, when these housing bubbles begin to deflate, it is likely to have substantial macroeconomic consequences.

I do not consider this to be the greatest threat facing the US or global economy. As I have argued before, the experience of both the Reserve Bank of Australian and Bank of England is that housing bubbles can successfully be deflated over a 2-3 year period by steady rate hikes and clear, consistent messages to investors. If the Federal Reserve is able to follow their example - and there's no obvious reason why they can't - that would detract around 1.0 to 1.5 percentage points a year from GDP growth. Enough to drag annual US growth below trend, but nowhere near recession territory.I'm not quite as sanguine.

Fed's Bies Warns on Nontraditional Mortgages

by Calculated Risk on 2/02/2006 12:58:00 PM

Here are FED Governor Susan Schmidt Bies' comments on nontraditional mortgage products, from her speech today at the Financial Services Institute:

The U.S. banking agencies have also issued draft guidance on certain mortgage products. Over the past few years, the agencies have observed an increase in the volume of originations for residential mortgage loans that allow borrowers to defer repayment of principal and, sometimes, interest. These mortgage loans, often referred to as “nontraditional mortgage loans,” include “interest-only” (IO) mortgage loans, in which a borrower pays no loan principal for the first few years of the loan, and “payment-option” adjustable-rate mortgages (option ARMs), in which a borrower has flexible payment options--and which also could result in negative amortization.Recently mortgage lenders have asked for an extension of the comment period to respond to the new guidance. I haven't seen if this extension has been granted.

In 2005, option ARMs and IOs were an estimated one-third of total U.S. mortgage originations. By contrast, in 2003, these products were estimated to represent less than 10 percent of total originations. Despite the recent publicity, however, it is estimated that these mortgages still account for less than 20 percent of aggregate domestic mortgage outstandings of $8 trillion. While the credit quality of residential mortgages generally remains strong, the Federal Reserve and other banking supervisors are concerned that current risk-management techniques may not fully address the level of risk in nontraditional mortgages, a risk that would be heightened by a downturn in the housing market.

Nontraditional mortgage products have been available for many years; however, these types of mortgages were historically offered to higher-income borrowers only. More recently, these products have been offered to a wider spectrum of consumers, including subprime borrowers who may be less suited for these types of mortgages and may not fully recognize their embedded risks. These borrowers are more likely to experience an unmanageable payment shock at some point during the life of the loan, which means they may be more likely to default on the loan. Further, nontraditional mortgage loans are becoming more prevalent in the subprime market at the same time that risk tolerances in the capital markets have increased. When risk spreads return to more “normal” levels, banks need to be prepared for the resulting impact on liquidity and pricing. Supervisors have also observed that lenders are increasingly combining nontraditional mortgage loans with weaker mitigating controls on credit exposures, such as allowing reduced documentation in evaluating the applicant’s creditworthiness and making simultaneous second-lien mortgages as competition in the mortgage banking industry intensifies. These “risk layering” practices have become more and more prevalent in mortgage originations. Thus, while elements of the product structure may have been used successfully by some banks in the past, the absence of traditional underwriting controls may have unforeseen effects on losses realized in these products.

In view of these industry trends, the Federal Reserve and the other banking agencies decided to issue the draft guidance on nontraditional mortgage products. The proposed guidance emphasizes that an institution’s risk-management processes should allow it to adequately identify, measure, monitor, and control the risk associated with these products. The guidance reminds lenders of the importance of assessing a borrower’s ability to repay a loan, including monthly payments when amortization begins and interest rates rise. Lenders should recognize that certain nontraditional mortgage loans are untested in a stressed environment; for instance, nontraditional mortgage loans to investors that rely on collateral values could be particularly affected by a housing price decline. Bankers should ensure that borrowers have sufficient information so that they clearly understand, before choosing a product or payment option, the terms and associated risks of these loans, particularly how far monthly payments can rise and that negative amortization can increase the amount owed on the property above what was originally borrowed. These products warrant strong risk-management standards as well as appropriate capital and loan-loss reserves.

Wednesday, February 01, 2006

Fiscal 2006: Record YTD Increase in National Debt

by Calculated Risk on 2/01/2006 03:02:00 PM

"By passing these reforms, we will save the American taxpayer another $14 billion next year, and stay on track to cut the deficit in half by 2009." George W. Bush, SOTU Address, Jan 31, 2006After four months, Fiscal 2006 continues to set new records for the YTD increase in National Debt. For the first four months of fiscal year 2006, the National Debt increased $263.4 Billion to $8.196 Trillion as of Jan 31, 2006.

Click on graph for larger image.

The previous record for the first four months was in fiscal 2005 with an increase in the National Debt of $248.7 Billion.

Each month I will plot the YTD increase in the National Debt and compare it to the proceeding years. I expect fiscal 2006 to set a new record for the annual increase in the National Debt.

NOTE: I quoted the SOTU address last night for two reasons: first, $14 Billion is an inconsequental amount compared to the US budget, and second, there is no way the US will "cut the deficit in half" by 2009. George W. Bush has no credibility on the budget:

"... our budget will run a deficit that will be small and short-term" George W. Bush, SOTU Address, Jan 29, 2002

Mortgage Application Volume Declines, Rates Rise

by Calculated Risk on 2/01/2006 11:01:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Declines In Latest Survey

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 626.8 – a decrease of 5.1 percent on a seasonally adjusted basis from 660.5 one week earlier. On an unadjusted basis, the Index increased 9.1 percent compared with the previous week but was down 12.1 percent compared with the same week one year earlier.Rates on mortgages increased:

The seasonally-adjusted Purchase Index decreased by 8.0 percent to 435.7 from 473.7 the previous week whereas the Refinance Index decreased by 1.5 percent to 1747.2 from 1773.9 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.20 percent from 6.04 percent one week earlier ...Activity is still high, but falling again as mortgage rates are once again rising.

The average contract interest rate for one-year ARMs increased to 5.48 percent from 5.44 percent one week earlier ...