RSS Feed

RSS Feed by Calculated Risk on 3/06/2006 07:54:00 PM

Monday, March 06, 2006

Financial Times: A chart for Japanese monetary policy

The Financial Times is free this week.

From A chart for Japanese monetary policy By Takatoshi Ito

Toshihiko Fukui, governor of the Bank of Japan, has been sending a signal through speeches and testimony ... that the time is ripe for ending quantitative easing (QE).

...

The BoJ considers that the self-imposed conditions for an exit from QE – positive inflation, reflected in the consumer price index ... as an actual rate ... and as a forecast – have been satisfied.

It is widely expected that the BoJ will abolish QE in April, if not as early as this week. The drive for an early termination seems to have received strong encouragement after the government’s announcement on March 3 that the inflation rate for January 2006 (compared with January 2005) was 0.5 per cent.

Last autumn, when Mr Fukui and other BoJ policy board members hinted at the exit from QE, the government sent a strong signal not to do it hastily. But in the past few weeks, Heizo Takenaka, the interior minister, Hidenao Nakagawa, chairman of the LDP policy research council, and Junichiro Koizumi, the prime minister, have all changed their tone, suggesting they may not oppose the abolition of QE.

Although terminating QE in the near term seems to have become a foregone conclusion, it is not clear why the BoJ is in such a hurry, given that the level of inflation – 0.5 per cent – is still very low. The core inflation rate, excluding energy prices as well as food, is a still more modest 0.1 per cent.

Deflation risks remain, if energy prices stop rising or if the US economy slows down later this year. ... As the end of QE nears, a future path and guidelines for monetary policy are needed.

...

Inflation targeting is a popular framework for answering these questions. It is now practised by a majority of central banks among advanced countries.

...

Adopting inflation targeting will ensure independence, which will be essential when the BoJ contemplates raising the interest rate in cases where the government opposes the move. As the policy interest rate starts to become positive, medium-term and long-term interest rates will rise.

...

As Mr Fukui leads the termination of QE, he should set out the direction of future monetary policy definitively, with a numerical range. By defining the BoJ’s commitment and accountability, the path forward will be cleared.

Sunday, March 05, 2006

Home Economics: A Profile of Edward L. Glaeser

by Calculated Risk on 3/05/2006 02:05:00 PM

The NY Times Magazine has an excellent article on economist Dr. Edward L. Glaeser: Home Economics. (hat tip to Dr. Thoma).

On the impact of the durability of housing:

... when cities grow, they expand significantly in population, but housing prices tend to rise slowly; even as Las Vegas grew by leaps and bounds in the 1990's, for instance, the average home there cost well under $200,000. When cities decline, however, the trends get flipped around. Population diminishes slowly, but housing prices tend to drop markedly.Although Dr. Glaeser believes restrictive regulations have played an important role in surging house prices, he also thinks there has been a psychological component:

Glaeser and Gyourko determined that the durable nature of housing itself explains this phenomenon. People can flee, but houses can take a century or more to finally fall to pieces. "These places still exist," Glaeser says of Detroit and St. Louis, "because the housing is permanent. And if you want to understand why they're poor, it's actually also in part because the housing is permanent." For Glaeser, this is the story not only of these two places but also of Buffalo, Baltimore, Cleveland, Philadelphia and Pittsburgh — the powerhouse cities of America in 1950 that consistently and inexorably lost population over the next 50 years. It is not just that there were poor people and the jobs left and the poor people were stuck there. "Thousands of poor come to Detroit each year and live in places that are cheaper than any other place to live in part because they've got durable housing still around," Glaeser says. The net population of Detroit usually decreases each year, in other words, but the city still attracts plenty of people drawn by its extreme affordability. As Gyourko points out, in the year 2000 the median house price in Philadelphia was $59,700; in Detroit, it was $63,600. Those prices are well below the actual construction costs of the homes. "To build them new, it would cost at least $80,000," Gyourko says, "so there's no builder who would build those today. And as long as those houses remain, the people remain."

Glaeser ... says, "I'm comfortable with the notion that we're going to have a substantial correction over the next five years."

Friday, March 03, 2006

Rising Rates

by Calculated Risk on 3/03/2006 02:26:00 PM

The yield on the Ten Year note has risen to 4.68%. This is about the same level as the second quarter of 2002.

Click on graph for larger image.

For the Ten Year, I plotted today's yield as Q2 2006. This shows yields on the Ten Year are close to Q2 2002 and probably means mortgage rates will rise next week close to Q2 2002 levels.

It will be interesting to see if the MBA purchase index shows another decline in activity.

Thursday, March 02, 2006

Fiscal 2006: Record YTD Increase in National Debt

by Calculated Risk on 3/02/2006 02:15:00 AM

After five months, Fiscal 2006 continues to set new records for the YTD increase in National Debt. For the first five months of fiscal year 2006, the National Debt increased $337.2 Billion to $8.27 Trillion as of Feb 28, 2006.

Click on graph for larger image.

The previous record for the first five months was in fiscal 2005 with an increase in the National Debt of $334.1 Billion.

Currently Treasury Secretary Snow is struggling to keep the debt under the "debt ceiling". The Charlston Gazette editorialized:

TREASURY Secretary John Snow says Congress must raise the federal debt limit to nearly $9 trillion by mid-March or the U.S. government will default on its obligations. This will be the fourth large hike in the debt ceiling in five years.Each month I will plot the YTD increase in the National Debt and compare it to the proceeding years. I expect fiscal 2006 to set a new record for the annual increase in the National Debt.

Washington Republicans are in a sweat, because the impending vote may spotlight outrageous overspending that has occurred under President Bush, who insists on gigantic tax giveaways to the rich amid gigantic military spending.

As we’ve noted before, the federal debt was only $1 trillion under Democratic President Jimmy Carter — but it quadrupled during the Republican Reagan-Bush years — then the U.S. budget was balanced again under Democratic President Bill Clinton.

During the 1990s, Congress followed pay-as-you-go rules, banning new spending that lacked revenue to pay for it. This discipline slowly wiped out yearly deficits. But the businesslike policy was abandoned under Bush, to allow more militarism and more tax cuts for the affluent.

To avoid the embarrassment of voting for higher debt limits, House GOP leaders adopted a sneaky rule that lets the ceiling climb automatically, without a House vote. But the Senate must vote for the $9 trillion level. Some national observers expect Senate GOP leaders to stifle debate in an attempt to accomplish the action quietly.

We hope West Virginia’s senators draw public notice to this new plunge into the hole. Americans need to know that the current one-party rule in Washington lives on credit cards — and today’s children will be stuck with the tab.

Wednesday, March 01, 2006

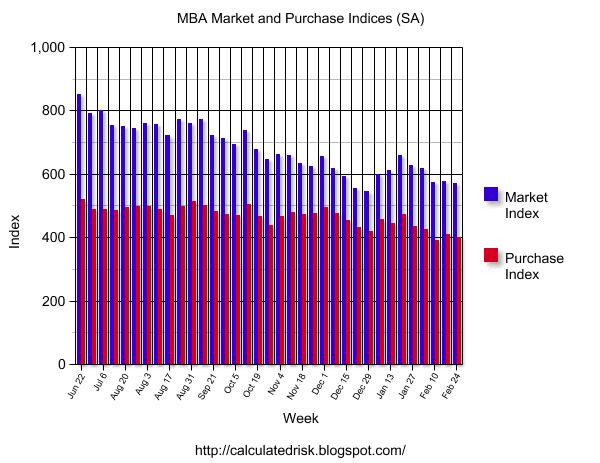

MBA: Mortgage Purchase Applications Steady

by Calculated Risk on 3/01/2006 10:31:00 AM

The Mortgage Bankers Association (MBA) reports that mortgage applications decreased slightly for the week ending Feb 24th.

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 571.5 – a decrease of 1.2 percent on a seasonally adjusted basis from 578.5 one week earlier. On an unadjusted basis, the Index decreased 9.6 percent compared with the previous week and was down 18.9 percent compared with the same week one year earlier. There was an adjustment included in the seasonally adjusted indexes to account for the President’s Day holiday.Mortgage rates declined slightly:

The seasonally-adjusted Purchase Index decreased by 1.9 percent to 400.8 from 408.7 the previous week, whereas the Refinance Index increased by 0.1 percent to 1573.5 from 1571.4 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.18 percent from 6.22 percent ...Activity is still fairly high though off from the peaks of 2005.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 5.84 percent from 5.87 percent ...

OFHEO: House Price Appreciation Continues at Robust Pace

by Calculated Risk on 3/01/2006 10:00:00 AM

The Office of Federal Housing Enterprise Oversight (OFHEO) released the Q4 2005 House Price Index.

HOUSE PRICE APPRECIATION CONTINUES AT ROBUST PACEUPDATE: From a bubble perspective, three of the most closely watched cities have been Boston, Sacramento and San Diego - all three have shown signs of a housing slowdown.

OFHEO House Price Index Shows Annual Rise of Nearly 13 Percent;

Unprecedented Increases in 26 Metropolitan Areas

WASHINGTON, D.C. – Average U.S. home prices increased 12.95 percent from the fourth quarter of 2004 through the fourth quarter of 2005. Appreciation for the most recent quarter was 2.86 percent, or an annualized rate of 11.4 percent. The increase during 2005 is similar to the revised increase of 12.55 percent for the year ended with the third quarter of 2005, showing no evidence of a slowdown. The figures were released today by OFHEO Acting Director Stephen A. Blumenthal, as part of the House Price Index (HPI), a quarterly report analyzing housing price appreciation trends.

"Despite recent indications that a slowdown may be forthcoming, house price appreciation during 2005 continued to hover at near-record levels," said OFHEO Chief Economist Patrick Lawler.

House prices continued to grow considerably faster over the past year than did prices of non-housing goods and services reflected in the Consumer Price Index. House prices rose 12.95 percent, while prices of other goods and services rose only 4.3 percent.

"While deceleration continues in some areas, appreciation generally is still extremely strong," said Lawler. "Mortgage rates climbed significantly during the second half of last year, but the effect of that increase on price appreciation so far appears to be limited."

This HPI report ranks 10 additional Metropolitan Statistical Areas (MSAs) due to an increase in the number of mortgage transactions in those areas.

Significant findings in the HPI:

1. Four-quarter appreciation rates were at record levels in 26 metropolitan areas including Orlando-Kissimmee, FL; El Paso, TX; and Myrtle Beach-

Conway-North Myrtle Beach, SC.

2. Phoenix-Mesa-Scottsdale, AZ continues to be the MSA with the greatest appreciation rate of 39.7 percent.

3. Appreciation in Arizona continues to surpass price growth in other parts of the country by a wide margin. Appreciation was 34.9 percent between the fourth quarter of 2004 and the fourth quarter of 2005. This is more than eight percentage points greater than the rate in Florida, the second fastestappreciating state.

4. The Mountain Census Division became the fastest appreciating area of the country, edging out the Pacific Census Division. The area with the slowest price growth continues to be the East North Central Division, which includes Michigan, Wisconsin, Illinois, Indiana and Ohio.

5. Price growth in the South Atlantic Census Division which includes East Coast states from Maryland to Florida, was at its highest rate since 1975, the beginning of the period covered in OFHEO’s House Price Index. Home prices grew by 17.81 percent between the fourth quarter of 2004 and the fourth quarter of 2005.

6. For the first time since the third quarter of 2003, one of the MSAs included in OFHEO’s appreciation-rate ranking experienced a four-quarter price decline. Prices in Burlington, NC fell by approximately one percent between the fourth quarter of 2004 and the fourth quarter of 2005.

Boston prices increased 1.5% in Q4 2005 and 7.3% for 2005.

Sacramento prices increased 2.7% for the quarter, and 18.7% for the year.

San Diego prices increased 2.2% for the quarter, and 11% for the year.

Any housing slowdown for these areas is not evident in the Q4 House Price Index.

FED's Geithner Warns Financial Tools Outpacing Controls

by Calculated Risk on 3/01/2006 01:14:00 AM

The Washington Post reports: Fed Official Warns of Changes

A top Federal Reserve official warned yesterday that the U.S. financial system is evolving faster than the ability of investors, lenders and regulators to evaluate and manage the risks involved.Geithner's speech: Risk Management Challenges in the U.S. Financial System

... he said, "there are aspects of the latest changes in financial innovation that could increase systemic risk" -- the danger that the losses of a few investors could set off a chain reaction of events that disrupts the broader financial system, as did the near-collapse of a heavily leveraged hedge fund in 1998.

...

"The complexity of many new instruments and the relative immaturity of the various approaches used to measure the risks in those exposures magnify the uncertainty involved," he said.

...

Many analysts have worried that the Fed's success in managing ... financial crisis ... during Alan Greenspan's 18-year tenure as Fed chairman have lulled many investors into underestimating financial risks.

...

Geithner said recent financial innovations have helped the economy absorb various financial shocks, "but they have not eliminated risk." He added, "They have not eliminated the possibility of failure of a major financial intermediary. And they cannot fully insulate the broader financial system from the effects of such a failure."

Tuesday, February 28, 2006

Standard Pacific Corp.: Declining Sales

by Calculated Risk on 2/28/2006 12:39:00 AM

Standard Pacific reported declining year over year New Home Orders Through February 26.

New home orders companywide for the year-to-date period ended February 26, 2006, excluding joint ventures, were down 13% from the level achieved a year ago. The overall decline in orders resulted from the slowing of demand in some of our markets from the unsustainable pace of the past few years, a trend that we began to experience in the fourth quarter of last year. This slowing of sales activity is particularly evident in markets which have experienced significant price increases and investor-driven demand in recent years, such as California and Florida.

New home orders were down 24% year over year in Southern California on a 29% increase in active selling communities. The lower level of sales activity in Southern California was due to: (1) a softening in buyer demand, most notably in San Diego and, to a lesser degree, in Orange County, (2) reduced product availability, particularly in our Los Angeles division, and (3) an increase in the cancellation rate. New orders were up, however, year over year in the Inland Empire, our largest and most affordable division in the region.

In Northern California, new home sales were down 60% on a 12% lower active community count. The year-over-year decrease in new home orders during the period reflected a slowdown in order activity which began in the latter half of 2005 from the robust pace experienced in 2004 and the first half of 2005, combined with a reduction in the number of active selling communities. The decrease in community count is particularly pronounced in our South Bay division where we experienced rapid sellouts in 2004 and 2005, and where a number of our new projects are targeted for 2006. While the Company saw a noticeable slowing of demand in Sacramento in the second half of 2005, orders for the year-to-date period ended February 26, 2006 were up slightly compared to the year earlier period.

New home orders were down 37% in Florida on a 12% decrease in community count. A number of factors contributed to the year-over-year decrease in Florida order activity: (1) reduced product availability in certain divisions, particularly in Orlando and Jacksonville, (2) a softening in buyer demand, most notably in South Florida and Southwest Florida, (3) continued intentional slowing of orders to better align production and sales, particularly in Tampa, and (4) a modest increase in the cancellation rate. The Company has 73% of its 2006 targeted deliveries for the state in its backlog or closed as of February 26, 2006.

...

The Company's cancellation rate for the year-to-date period ended February 26, 2006 was 26%, up from the year earlier rate of 18%.

Monday, February 27, 2006

January New Home Sales: 1.233 Million Annual Rate

by Calculated Risk on 2/27/2006 10:26:00 AM

UPDATE: For more on housing, please see my Angry Bear post: Slowing, but Not Crashing.

According to the Census Bureau report, New Home Sales in January were at a seasonally adjusted annual rate of 1.233 million. December's sales were revised upwards slightly to 1.298 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

The Not Seasonally Adjusted monthly rate was 93,000 New Homes sold, slightly higher than the 89,000 in December.

On a year over year basis, January 2006 sales were 1% higher than January 2005.

The median and average sales prices are steady.

The median sales price of new houses sold in January 2006 was $238,100; the average sales price was $291,600.

The seasonally adjusted estimate of new houses for sale at the end of January was 528,000. This represents a supply of 5.2 months at the current sales rate.

The 528,000 units of inventory is another all time record for new houses for sale. On a months of supply basis, inventory is above the level of recent years.

This report is still reasonably strong, except for the record inventory and months of inventory.

Sunday, February 26, 2006

Merrill Lynch's Rosenberg: Five Macro Misperceptions

by Calculated Risk on 2/26/2006 06:03:00 PM

Merril Lynch economist David Rosenberg discusses (pdf): Reassessing Hard Landing Risks

... I’d just like to go through briefly what I took away from a week-long marketing swing through Europe last week, because everywhere I went, I was greeted with these five macro beliefs, or what I call major macro misperceptions:See the link for Rosenberg's discussion and many interesting graphs. Here are his comments on the US consumer:

(i) that the U.S. economy is booming;

(ii) the consumer is going to remain underpinned by record wealth even as the Fed raises rates and the housing market slows;

(iii) that high-end retailing stocks will be safe because the ‘well off’ homeowner did not play a role in the housing boom;

(iv) interest rates are still far too low to generate any weakness in the economy;

(v) the tight labor market is on the precipice of triggering wage inflation, and therefore the Fed has much more to do.

Misperception #2 – "don’t worry about the consumer; the level of household net worth is at a record high."

We heard that all the time, household net worth is over $50 trillion, and the level of bank deposits and money market fund holdings, are at record highs and somehow this accumulated savings will keep the consumer afloat even if the Fed tightens further. Well, we went back into the history books and found that U.S. household net worth hit a RECORD level in the quarter before every recession in the post-war era. Not only that, but in every recession outside of the 2001 episode when the equity market melted, household net worth rose throughout the entire period of negative GDP growth. So basically, net worth goes up before, during and after recessions, and it would make sense that with personal income setting new records practically every quarter, that the level of savings would too. In other words, the level of net worth is a pretty useless leading economic indicator, and the notion that households will draw down their level of savings – savings hopefully intended to fund retirement – to satisfy current consumption instead sounds pretty spurious to me.