RSS Feed

RSS Feed by Calculated Risk on 3/15/2006 11:05:00 AM

Wednesday, March 15, 2006

MBA: 30-year Fixed Rate Increases to Highest Level Since July 2002

The Mortgage Bankers Association (MBA) reports that the 30-year fixed rate mortgage increased to the highest level since July 2002. Mortgage application volume was steady for the week ending March 10th.

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 574.4 – a decrease of 0.2 percent on a seasonally adjusted basis from 575.6 one week earlier. On an unadjusted basis, the Index increased 0.2 percent compared with the previous week but was down 20.4 percent compared with the same week one year earlier.Mortgage rates increased:

The seasonally-adjusted Purchase Index increased by 1.0 percent to 403.0 from 399.0 the previous week whereas the Refinance Index decreased by 1.9 percent to 1583.6 from 1614.4 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.42 percent from 6.31 percent...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 5.64 percent from 5.69 percent ..

| Total | -20.4% |

| Purchase | -13.1% |

| Refi | -30.2 |

| Fixed-Rate | -16.1% |

| ARM | -29.3% |

Purchase activity is off 13% from the same week in 2005 and overall mortgage activity is off 20%. Those are significant declines in activity.

Tuesday, March 14, 2006

O.C. home prices rebound to $617K

by Calculated Risk on 3/14/2006 10:29:00 AM

The OC Register reports: O.C. home prices rebound

Orange County home prices rebounded in February, as the median sales price reached $617,000 – tying the second highest on record.

DataQuick reported early Tuesday that February's price was $35,000 higher than January's $582,000 – and 11.2 percent above year-ago prices. The record of $621,000 was set last December.

All told, 2,672 homes sold last month, down 7.5 percent from a year ago.

For more details, see Jonathan Lansner's real estate blog.

Monday, March 13, 2006

NAR: Housing Market Readjusting

by Calculated Risk on 3/13/2006 02:02:00 PM

The National Association of Realtors reports: Housing Market Readjusting to Normal Balance.

A lower level of home sales expected this year will create a more level playing field for buyers and sellers on the heels of a five-year sellers’ market, according to the National Association of Realtors®.

David Lereah, NAR’s chief economist, said the number of homes on the market has been improving nicely. "The cooling from overheated sales conditions in recent months is helping to bring inventory levels up to the point where buyers have more choices than they’ve seen in the last five years," Lereah said. "Annual price appreciation is still running at double-digit rates, but the cause of those sharp increases is going away. As the market readjusts, price appreciation should return to more normal rates of growth this year."

The national median existing-home price for all housing types is projected to rise 5.8 percent in 2006 to $220,300. The median new-home price should increase 5.4 percent this year to $250,200.

Existing-home sales are expected to fall 5.7 percent to 6.67 million in 2006 from the record 7.08 million last year. At the same time, new-home sales are forecast to decline 7.7 percent to 1.18 million from a record 1.28 million in 2005 – each sector would be at the third highest year following the tallies for 2005 and 2004. Housing starts are likely to total 1.98 million this year, down 4.3 percent from 2.06 million in 2005.

NAR President Thomas M. Stevens from Vienna, Va., said some home buyers and sellers have unrealistic expectations. "Some sellers in markets that have had rapid appreciation are listing the price of their home too high, but those homes are just languishing on the market," said Stevens, senior vice president of NRT Inc. "At the same time, some buyers who have believed hype about a housing bubble are hoping prices will drop, but that’s not happening either."

...

The 30-year fixed-rate mortgage should increase gradually to 6.9 percent in the fourth quarter.

Friday, March 10, 2006

Mortgage Debt and the Trade Deficit

by Calculated Risk on 3/10/2006 09:18:00 PM

"Interestingly, the change in U.S. home mortgage debt over the past half-century correlates significantly with our current account deficit. To be sure, correlation is not causation, and there have been many influences on both mortgage debt and the current account."

Alan Greenspan, Current account, Feb 4, 2005 Click on graph for larger image.

Click on graph for larger image.

With the release of the Fed's Flow of Funds report, we can look at the relationship between the annual increase in household mortgage debt and the trade deficit.

Note: I'm using the trade deficit instead of the current account deficit, since the current account for '05 has not been released yet.

I expect the annual increase in mortgage debt to decline in 2006. This is because I expect new and existing home purchases to decline, and homeowners to extract less equity from their homes in 2006.

The drop in mortgage activity is is one of the reasons I expect the trade deficit to stabilize in 2006. From my 2006 predictions:

Trade Deficit / Current Account Deficit: I could be wildly wrong here too, but I think the trade deficit will stabilize or even decline slightly next year. As the economy slows, I think imports will slow.I should have been more clear. There is no way the trade deficit will decline on an annual basis in 2006, but I was expecting the deficit to stabilize or decline from the September to December level of $66 Billion per month.

The record January deficit of $68.5 Billion was a little disheartening, but mortgage extraction has just begun to slow. So far I've been wrong - but its early.

Drs. Brad Setser and Menzie Chinn are more pessimistic ...

Brad Setser: January trade data

Menzie Chinn: The downward march of the trade balance

Thursday, March 09, 2006

Geithner: U.S. Monetary Policy in the Global Financial Environment

by Calculated Risk on 3/09/2006 04:27:00 PM

New York Fed President Timothy Geithner spoke today on U.S. Monetary Policy in the Global Financial Environment

I will focus on two features of what is happening in the world economy and financial markets today ... These are, first, the behavior of forward interest rates in financial markets, and, second, the pattern of external imbalances.After discussing the possible causes for these two features, Giethner turns to the implications for policy:

These features are interesting, in part, because they seem somewhat anomalous, or inconsistent with what the past has led us to expect. They seem likely to be related to each other and both are a feature of the changes underway in global financial integration. Understanding the forces behind these phenomena or anomalies is important to thinking through what they mean for policy.

What might this mean for the conduct of monetary policy? To the extent that these forces act to put downward pressure on interest rates and upward pressure on other asset prices, they would contribute to more expansionary financial conditions than would otherwise be the case. And, if all else were equal, which of course is unlikely ever to be the case, monetary policy in the affected countries would have to adjust in response; policy would have to act to offset these effects in order to achieve the same impact on the future path of demand and inflation. To do otherwise would run the risk that monetary policy would be too accommodative, pulling resources from the future in a way that would alter the trajectory for the growth of the capital stock, perhaps amplifying the imbalances, and compromising the price stability.I suggest reading the entire speech.

...

Let me conclude by observing that a constellation of factors has aligned to produce the current combination of low world interest rates, low risk premia and large global imbalances. Most of these factors are outside the control of U.S. monetary policy, and we do not fully understand their implications for our economy and for policy. The process of global economic integration makes it ever more important that we work to improve our understanding of how this complex of global monetary arrangements affects our objectives.

FED: Q4 Mortgage Debt Continues Rapid Growth

by Calculated Risk on 3/09/2006 02:02:00 PM

The FED Flow of Funds report was released today. It shows that household mortgage debt increased at a record pace in 2005.

On a dollar basis, household mortgage debt increased by a near record $290.6 Billion in the 4th quarter. The last 8 quarters (billions increase in household mortgages, Includes loans made under home equity lines of credit):

q1 2004: $190.4

q2 2004: $211.1

q3 2004: $277.1

q4 2004: $232.9

q1 2005: $184.5

q2 2005: $277.9

q3 2005: $314.1

q4 2005: $290.6

From Rex Nutting of CBS MarketWatch: U.S. household debt up most in 20 years

U.S. households took on debt at the fastest pace in 20 years in 2005, fueled by a housing boom that boosted their net worth to a record $52.1 trillion, the Federal Reserve said Thursday.And for the fourth quarter:

The Fed's quarterly flow of funds report shows the explosion of debt in the U.S. economy continued in 2005, with net savings in the economy falling below 1% of gross domestic product for the first time on record.

Led by a surge in mortgage borrowing, U.S. households' debt increased 11.7% to record $11.5 trillion in 2005, the fastest growth since 1985, the Fed said.

In the fourth quarter, total debt in the economy grew at an annual rate of 9.5%, down from 9.6% in the third quarter.

Household debt increased at an 11% pace, down from 12.4% in the third quarter. Mortgage debt increased 13.2%, down from 14.9% in the third quarter. Credit card debt fell 0.7% in the fourth quarter.

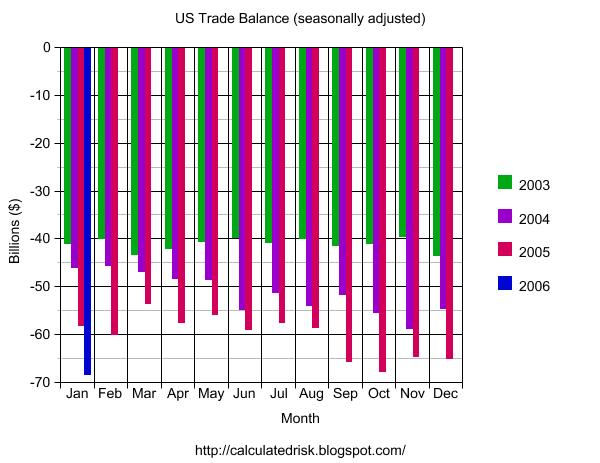

January US Trade Deficit: $68.5 Billion

by Calculated Risk on 3/09/2006 12:01:00 AM

UPDATE: Brad Setser's comments are interesting: Mike Mandel, Ricardo Hausmann and Federico Sturzenegger better be right (January trade data)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis reports that the U.S. trade deficit for January was $68.5 Billion.

Click on graph for larger image.

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that total January exports of $114.4 billion and imports of $182.9 billion resulted in a goods and services deficit of $68.5 billion, $3.4 billion more than the $65.1 billion in December, revised.More to come.

January exports were $2.8 billion more than December exports of $111.6 billion. January imports were $6.2 billion more than December imports of $176.6 billion.

Wednesday, March 08, 2006

Slowing housing won't sink spending: Poole

by Calculated Risk on 3/08/2006 02:59:00 PM

From Reuters: Slowing housing won't sink spending: Poole

The U.S. housing sector may already be cooling but it should maintain its lofty level and not undermine the economic expansion, St. Louis Federal Reserve Bank President William Poole said on Wednesday.Those are the big questions: Will housing activity "stabilize" or keep falling? And what will be the impact on jobs and the US economy?

"My hunch ... is that housing activity will stabilize and remain at a high level this year," Poole told the St. Louis Regional Chamber and Growth Association over breakfast.

Poole, who is not a voting member of the FOMC this year, said rising inventories of unsold U.S. houses signaled a slowdown may already be underway.I disagree with Poole's comments. I think the substantial mortgage equity withdrawal (MEW) in recent years contributed significantly to GDP growth, and declining MEW will be a significant drag for the next few years.

Some economists have forecast a downturn in the housing sector will sap consumer spending, which has been driving U.S. growth since a shallow recession in 2001.

They argue that homeowners have extracted equity from now more valuable homes to support spending despite, weak income growth in recent years. But Poole dismissed this concern.

"The marginal contribution to the pace of consumer spending stemming from the wealth effect -- that is, from households extracting a portion of their home equity to spend on goods and services -- is not likely to be a significant concern."

"The reason is that other economy-wide developments, especially income and employment growth, typically exert a much greater influence on the consumer's pocketbook and spending habits than does the state of the housing industry,' he said.

MBA: Mortgage Application Volume Holds Steady

by Calculated Risk on 3/08/2006 10:00:00 AM

The Mortgage Bankers Association (MBA) reports that mortgage application volume was steady for the week ending March 3rd.

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 575.6 – an increase of 0.7 percent on a seasonally adjusted basis from 571.5 one week earlier. On an unadjusted basis, the Index increased 12.9 percent compared with the previous week, but was down 17.8 percent compared with the same week one year earlier.Mortgage rates increased:

The seasonally-adjusted Purchase Index decreased by 0.4 percent to 399.0 from 400.8 the previous week, whereas the Refinance Index increased by 2.6 percent to 1614.4 from 1573.5 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.31 percent from 6.18 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs increased to 5.69 percent from 5.64 percent ...

| Total | -17.8% |

| Purchase | -11.8% |

| Refi | -25.8% |

| Fixed-Rate | -14.6% |

| ARM | -25.0% |

Purchase activity is still fairly high though off from the peaks of 2005. Mortgage rates are increasing again, and will be increase again this week with the Ten Year note yield rising to 4.7%.

Tuesday, March 07, 2006

Krugman's Intro to Keynes's General Theory

by Calculated Risk on 3/07/2006 09:33:00 PM

Dr. DeLong excerpts Krugman's Intro to Keynes's General Theory

"... Keynes was no socialist - he came to save capitalism, not to bury it. And there’s a sense in which The General Theory was... a conservative book.... Keynes wrote during a time of mass unemployment, of waste and suffering on an incredible scale. A reasonable man might well have concluded that capitalism had failed, and that only... the nationalization of the means of production - could restore economic sanity.... Keynes argued that these failures had surprisingly narrow, technical causes... because Keynes saw the causes of mass unemployment as narrow and technical, he argued that the problem’s solution could also be narrow and technical: the system needed a new alternator, but there was no need to replace the whole car. In particular, “no obvious case is made out for a system of State Socialism which would embrace most of the economic life of the community.”... Keynes argued that much less intrusive government policies could ensure adequate effective demand, allowing the market economy to go on as before.There is much more at Dr. DeLong's blog.

Still, there is a sense in which free-market fundamentalists are right to hate Keynes. If your doctrine says that free markets, left to their own devices, produce the best of all possible worlds, and that government intervention in the economy always makes things worse, Keynes is your enemy. And he is an especially dangerous enemy because his ideas have been vindicated so thoroughly by experience.

Stripped down, the conclusions of The General Theory might be expressed as four bullet points:

1) Economies can and often do suffer from an overall lack of demand, which leads to involuntary unemployment

2) The economy’s automatic tendency to correct shortfalls in demand, if it exists at all, operates slowly and painfully

3) Government policies to increase demand, by contrast, can reduce unemployment quickly

4) Sometimes increasing the money supply won’t be enough to persuade the private sector to spend more, and government spending must step into the breach

To a modern practitioner of economic policy, none of this - except, possibly, the last point - sounds startling or even especially controversial. But these ideas weren’t just radical when Keynes proposed them; they were very nearly unthinkable. And the great achievement of The General Theory was precisely to make them thinkable....

I've read Keynes' General Theory of Employment, Interest and Money twice. It is a tough read, but well worth the effort.