RSS Feed

RSS Feed by Calculated Risk on 4/17/2006 01:50:00 AM

Monday, April 17, 2006

Caroline Baum: Banks Have No Exposure to Mortgages?

Carolina Baum writes: Banks Have No Exposure to Mortgages? Think Again.

Every time the subject of banks making risky home loans to bad credit risks -- no money down, no questions asked -- the usual retort is that banks sell the mortgages. They aren't at risk. It doesn't matter if the loan stops performing because they don't own it.However the data doesn't tell which loans the banks have kept. Most banks claim they have kept the better quality loans (low LTV).

That's not exactly true. According to the Federal Reserve's Flow of Funds report for the fourth quarter of 2005, mortgages accounted for 32 percent of commercial banks' financial assets. Throw in agency- and mortgage-backed securities, and the exposure to outright and securitized mortgage loans is 44 percent.

A few statistics:

-- 43 percent of first-time home buyers made no down payment last year, according to a study by First American Corp.

-- 22 percent of the borrowers with initial interest payments of 2.5 percent or less have negative equity in their homes (the principal balance is greater than the size of the initial loan); 40 percent have less than 40 percent equity.

-- About one-quarter of the jobs created since the 2001 recession have been in construction, real estate and mortgage finance.

Sunday, April 16, 2006

$70 Oil and Gasoline

by Calculated Risk on 4/16/2006 11:57:00 PM

My post on Angry Bear: $70 Oil.

The spot price for wholesale unleaded gasoline just hit $2.12 per gallon, up almost 15 cents in the last week. The gasoline balance in charts from the DOE's This Week In Petroleum.

Domestic gasoline production is still below 2005 levels for the same period. Falling production is a typical pattern for this time of year as refineries shift blends. Also, according to the DOE, there has been "unusually high refinery maintenance in the U.S. ... this spring".

Luckily gasoline imports are still higher than last year. Of course this adds to the trade deficit.

Meanwhile the demand for gasoline keeps rising.

And the end result is falling stocks. However stocks are still in the normal range for this time of year, and domestic production should increase over the next few weeks. Still a 15 cent rise in the wholesale price should lead to higher prices at the pump in the next couple of weeks. Gasoline is already close to $3.00 per gallon for regular unleaded in my town.

Friday, April 14, 2006

House Prices and Sales Volumes: California and Arizona

by Calculated Risk on 4/14/2006 11:14:00 AM

Here are three articles on house prices and sales volumes:

From the San Diego Union: San Diego housing market continues cooling trend

... the San Diego region's housing market continued its slow cooling trend in March, which marked the 11th month in a row of single-digit price gains.From the LA Times: Housing Prices in L.A. Aren't Letting Up

The end of the first quarter also marked the 21st consecutive month in which sales volumes were down on a year-over-year basis, DataQuick Information Systems reported Thursday.

...

Last month's overall sales count was 4,146, a decline of 17 percent from March 2005. That was the lowest count for March since March 1998, when 4,016 homes sold.

The pace of resale condo sales fell by nearly 30 percent to 841 units, compared to the same month last year. That was a gain over February's resale condo tally of 657 units, however.

The overall median price for all homes sold was $504,000, a 5.7 increase over March 2005 and a slight rise over February's median of $502,000. The county hit a record overall median price of $518,000 in November 2005.

In March, the median hit $506,000, up 15% from a year earlier and 3% above the prior month, according to DataQuick Information Systems, a La Jolla-based research firm that analyzes property transactions.From the Arizona Republic: Median resale housing prices still dropping

Los Angeles County thus joined Orange, Ventura and San Diego counties in crossing the half-million-dollar mark, keeping Southern California's place among the nation's priciest housing markets. Orange and Ventura counties' medians sailed through the $600,000 level in the middle of last year, and San Diego's broke through the $500,000 point last fall.

...

Sales volumes are slowing while more homes are coming on the market. In March, 9,755 homes changed hands in L.A. County, a 10.3% decline from a year earlier, and the fifth straight month of falling sales.

...

Today's combination of prices rising more slowly, fewer sales and growing supply are typical of the first phase of a slowdown, UCLA economist Christopher Thornberg says.

"Prices are still going up, because they always go up even when the market starts to cool," he says. "It will take six to nine months for a cooling market to start to see lower prices. It happens time after time."

Median resale housing prices kept falling through most of the Southeast Valley in March, mainly because there are so many more homes on the market. But it's still too early to say if this will continue for the rest of the year.

The main exception was Ahwatukee Foothills, where prices jumped 6 percent from February to March, to $364,250. But that is still below its December median of $386,250. Median home prices from February to March fell 5 percent in Gilbert to $322,500, and almost 4 percent in Tempe to $288,400.

Prices in Mesa, meanwhile, fell less than 1 percent to $243,500, and 1.6 percent in Chandler to $295,000.

Thursday, April 13, 2006

Dr. Duy: Fed Policy in Transition

by Calculated Risk on 4/13/2006 10:47:00 PM

Dr. Tim Duy presents another Fed Watch: Policy in Transition. Excerpt:

"... recent data reveals that the economy enjoys enough momentum to justify another rate hike in May. That is something of a given at this point; the real question is the June meeting. I continue to feel that the Fed would like to take a pass at that meeting on the expectation of slowing economic growth, but make it clear that the odds of tightening beyond that remain about 50%. The question is whether the data will continue to support such a move, especially since policymakers would likely risk somewhat higher interest rates now to avoid even more aggressive hikes later. Particularly important is the relative impact of possible higher commodity prices versus expectations of slowing demand growth.Interesting speculation! And just a reminder, every Monday, Dr. Dave Altig presents the market based probablities on Fed Funds rates.

Another possible path comes to mind. As the play on housing becomes less stimulative, will market participants find yet another asset play to maintain household wealth? ..."

Kudos to Real Estate Broker Gary Watts

by Calculated Risk on 4/13/2006 08:15:00 PM

One year ago, Gary Watts predicted:

Watts expressed his enthusiasm this way: The recent $100 increase in monthly payments - or $1,200 a year - is nothing compared to what he predicts is Orange County home-price appreciation potential: as much as $70,000 a year.At that time (March 2005), the median Orange County home was selling for $555K according to DataQuick.

"There's too much emphasis on interest rates in the marketplace," Watts said. "Who wouldn't trade $1,200 for $70,000?"

DataQuick announced today that the median Orange County house is selling for $625K.

That is an increase of $70K in one year.

Watts prediction for 2006:

"Fifteen percent is pretty much in the bag for Orange County in 2006," [Gary Watts] says. "It's impossible for prices to go down this year."

FED's Kohn: "great uncertainties" Due to Housing Market

by Calculated Risk on 4/13/2006 02:51:00 PM

At the Bankers and Business Leaders Luncheon in Kansas City, Federal Reserve Governor Donald L. Kohn spoke on the economic outlook today. Overall Kohn was very positive on the economy, but expressed some concern about the housing market:

"If the past is any guide, the effect of rising interest rates is likely to be felt most visibly in housing markets. The rate for a thirty-year, fixed-rate mortgage is up 70 basis points from its level in the middle of last year, and one-year adjustable-rate mortgages have risen more than 100 basis points over the same period. In addition, house prices have increased considerably relative to rents, incomes, and returns on alternative assets. Already there have been signs that housing demand has begun to moderate. Sales of both new and existing homes are down substantially from their levels last summer, and information on mortgage applications and pending home sales point to further softening in the next few months. With demand slowing, house prices also seem likely to decelerate. Indeed, we are beginning to see hints of moderation in some of the data on housing prices.

As a consequence, spending for new housing construction, after contributing nearly 1/2 percentage point to overall GDP growth last year, may not increase much this year. Moreover, the slowdown in house price increases could well hold back growth in consumption spending on a wide variety of goods and services. The rapid run-up in prices over the past few years and hence in household wealth, perhaps combined with the increasing ease of tapping that wealth, probably has been a major reason that households have been saving so little of their current flow of income. As house-price appreciation slows, the personal saving rate likely should begin a gradual ascent.

To be candid, however, the behavior of the housing market and the response of spending are among the great uncertainties about the economic outlook. I have sketched a benign scenario of gradual adjustment that lines up very nicely with the Federal Reserve's assessment that overall growth should slow to a sustainable pace. But our ability to predict asset prices is very limited, especially when the trajectory of those prices is shifting, as that of house prices appears to be doing right now. Moreover, we have particular difficulty in assessing how consumers will respond to changes in their perceptions of future capital gains and actual home prices. The housing market and its effects on spending will be among the areas that Tom and I and our colleagues on the FOMC will be monitoring most closely as we try to discern the emerging pattern of economic activity and inflation."

Wells Fargo: Housing Market "noticeably deteriorated"

by Calculated Risk on 4/13/2006 02:17:00 PM

From the Contra Costa Times: State's housing market retreats. The Contra Costa Times excerpts from a new Wells Fargo report on the California economy.

Click on graph for larger image.

Wells Fargo provides this graphic of unsold inventory in California by county. The caption reads:

California housing inventories can no longer be considered lean. Orange County and San Diego appear most at risk for near-term home price deceleration.From the Times article:

The housing market in California has fallen into a visible slump, and the downturn could erode economic expansion in fast-growing regions such as the East Bay, economists warned Wednesday.

Existing home sales have skidded, houses now languish on the market for longer periods, and the rate of home building has slowed, according to the report issued by Wells Fargo Bank.

...the Wells Fargo economic study warned of a chill for real estate.

"California housing market conditions have noticeably deteriorated since September," Scott Anderson, Wells Fargo senior economist, wrote in his report.

...

"The California housing market may have skipped a beat, but the patient is not dead yet," Anderson stated in his study. "The decline so far appears manageable for the industry as well as for the California economy."

Still, some of the recent trends in housing portray a sector in retreat from the white-hot levels of the last years:

• Existing home sales statewide "plunged" in November, with an 11.2 percent decline; in December, with a 17.6 percent drop; and in January, with a 5.9 percent setback, Wells Fargo reported, citing data released by the California Association of Realtors.

• Unsold inventories of detached houses rose to 6months in January, far above the 3.2 months that houses remained unsold in January 2005.

• Statewide housing permits have drooped 11 percent below last year's pace.

• Median prices have been "nearly flat" in the last six months, although they remain 13.8 percent above the levels of a year ago.

Wednesday, April 12, 2006

Housing: Quote of the Day

by Calculated Risk on 4/12/2006 07:42:00 PM

Barry Ritholtz (The Big Picture) provides this quote:

"Home sales are in the process of reversing all the gains of the past two years and reverting to 2003 levels."

- Robert Mellman, economist, J.P. Morgan

MBA: Mortgage Application Volume Drops

by Calculated Risk on 4/12/2006 09:35:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Drops in Latest Survey

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 579.4, a decrease of 5.5 percent on a seasonally adjusted basis from 612.8 one week earlier. On an unadjusted basis, the Index decreased 5.1 percent compared with the previous week and was down 14.7 percent compared with the same week one year earlier.Mortgage rates increased slightly:

The seasonally-adjusted Purchase Index decreased by 4.7 percent to 417.7 from 438.2 the previous week whereas the Refinance Index decreased by 6.6 percent to 1532.4 from 1640.8 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.50 percent from 6.49 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs increased to 5.97 percent from 5.96 percent ...

| Total | -14.7% |

| Purchase | -11.9% |

| Refi | -19.3% |

| Fixed-Rate | -5.2% |

| ARM | -31.8% |

Purchase activity is off 11.9% from last year. This provides further evidence that housing is slowing.

Tuesday, April 11, 2006

Toll Bros CEO: Speculators Impacting Supply

by Calculated Risk on 4/11/2006 06:44:00 PM

Dow Jones reports: Toll Bros CEO: Housing Comparisons Difficult Over Last Year

Toll Brothers Inc. Chief Executive Robert Toll said comparisons in the housing market continue to be difficult over last year ...How Speculation impacts supply:

...

As demand declined, Toll said speculators left the market.

"What's more you get the speculator putting their product back on the market - so you've got a little excess supply," Toll said.

A recent report by the National Association of Realtors (NAR) reported that 39.9% of all homes nationwide bought in 2005 were purchased as second homes. NAR reported 12.2% were purchased as vacation homes and 27.7% for investments. This is clear evidence of speculation.

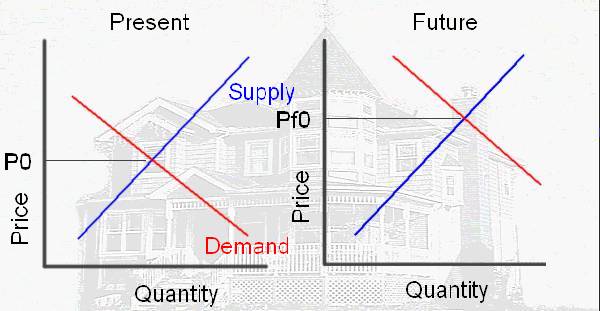

The following supply demand diagrams illustrate this type of speculation.

Click on diagram for larger image.

The above diagram shows the motive for the speculator. If he buys today, at price P0, he believes he can sell in the future at price Pf0 (price future zero), because of higher future demand. The speculation would return: Profit = Pf0-P0-storage costs (the storage costs are mortgage, property tax, maintenance, and other expenses minus any rents).

In this model, speculation is viewed as storage; it removes the asset from the supply. The following diagram shows the impact on price due to the speculation:

Since speculation removes the asset from the supply, the Present supply curve shifts to the left (light blue) and the price increases from P0 to P1. In the second diagram, when the speculator sells, the supply increases (shifts to the right). The future price will fall from PF0 to PF1. As long as (PF1 – storage costs) is greater than P1 the speculator makes a profit.

However, if the price does not rise, the speculator must either hold onto the asset or sell for a loss. If the speculator chooses to sell, this will add to the supply and put additional downward pressure on the price.

This is the type of speculation that Robert Toll is describing.

For more on speculation, especially leverage (using nontraditional mortgages), see my post on Angry Bear: Speculation is the Key. (Some of this post is a duplicate of that post).