RSS Feed

RSS Feed by Calculated Risk on 4/24/2006 10:49:00 AM

Monday, April 24, 2006

Foreclosures Increasing

From Foreclosures.com: Mortgage Defaults on the Rise in West and Southwest

... reported today that foreclosure activity in the first quarter of 2006 increased significantly from the fourth quarter of 2005 in several western and southwestern housing markets.As DataQuick recently noted: "Foreclosure activity is edging up from its bottom, but is still low."

"The biggest increases were in major urban centers around the West," said ForeclosureS.com president Alexis McGee. "For example, Los Angeles County recorded 6,314 pre-foreclosure filings and foreclosures through March, up from 4,911 in Q4 of 2005, while in San Diego the numbers jumped from 1,565 in Q4 of 2005 to 2,241 in Q1 of 2006."

She went on to say that such increases were coincident with cooling markets in previously overheated areas, and with the steady rise in interest rates.

...

She added that rampant speculation in some markets, along with a slowdown in price appreciation would lead to an increase in delinquencies and foreclosures.

"In Las Vegas, this appears to be already happening. Foreclosure activity jumped to 3,246 in Q1 of 2006 from 1,480 in Q4 of 2005. Speculators who came late to the party are being washed out of the market."

She pointed to widespread concern over the number of interest only and high negative amortization loans that had been issued by lenders in recent years as homebuyers sought to qualify for ever more expensive homes during the coastal markets' price boom of the last half decade.

"In San Diego for example," said Ms. McGee, "more than half of home purchases in 2004 and 2005 were financed with these exotic mortgage products. When these loans reset to true market rates the payment shock can be severe and put many households in financial distress."

She referred to a recent study by Dr. Christopher Cagan of First American Real Estate Solutions. Cagan stated that an option ARM with payments of $800 per month could jump to $3000 per month when reset to market rates. "That's a recipe for financial disaster," said Ms. McGee.

Sunday, April 23, 2006

Housing: Fleck and Watts

by Calculated Risk on 4/23/2006 03:15:00 PM

This is the Night and Day of housing.

Fleck (aka Bill Fleckenstein) writes for MSN Money: The housing bubble has popped

And Orange County Real Estate broker Gary Watts provides his view: Housing's #1 fan. Last week, I acknowledged Watt's on-target 2005 prediction, but I think he is wrong about 2006. From Watts:

I am sticking to my 15% gains for resale housing in 2006.From Fleck:

...

I believe that a lot of sellers who were planning on listing their homes during this summer, "jumped-the-gun", thinking that they should get their homes on the market during the spring, when there are an usually large build-up of buyers. If this is true, we will not see the usual increase of our summer listing inventory. If in fact this happens, we will have an "Inverted Year". Usually we have a lot of buyers and few listings but this year, I am betting that the listings will decrease by summer (rather than increase) and more buyers will be in the market, especially with the Fed announcement that the interest-rate increases are finished. This will create more real estate sales activity in the latter half of the year rather than the usual torrid pace of the spring.

Reports of falling sales and investors stuck with properties they can't sell are just the beginning. Property owners should worry; so should their lenders.

...

To me, it's not debatable that the real-estate bust is starting to gather steam. The top was approximately when Time Magazine published its June 12, 2005, cover story: "Home $weet Home: Why We're Going Gaga Over Real Estate".

...

After having leveled off for a while, the real-estate market is now starting to slide. We're seeing signs of sales slowing and inventory accumulating, which are all quite classic ...

It is indeed the financial institutions that are most at risk in the real-estate market (which is not to say that consumers and speculators won't get hurt). The lenders will bear the brunt of the pain, because in many cases, they loaned the entire purchase prices of many homes. As I have said often, the housing bubble has been more a lending bubble. It will be the impairment of the financial institutions that will stop the flow of credit to the real-estate market. In turn, that will accelerate the collapse in house prices somewhere along the way.

Saturday, April 22, 2006

WaPo: Housing Investors in Retreat

by Calculated Risk on 4/22/2006 01:23:00 AM

Kirstin Downey writes in the Washington Post: After Pushing Up Prices, Investors Are Left Holding Too Many Homes

Investors who sought quick profits buying and selling real estate in the Washington region are in full retreat, dampening demand for homes, most notably for condos.

What is becoming apparent ... is how big a part speculators played in the region's real estate boom of the past few years. ... condominiums, ... townhouses and single-family houses, were snapped up by investors using no-money-down financing and non-traditional loans. They helped send prices soaring at unprecedented rates. And now many are trying to sell, or rent at a loss. Some may eventually dump properties at low prices to get rid of them. That could weigh down values for everyone.

Sales of new condos fell 43 percent in the first quarter of the year, compared with the first quarter of 2005, according to one report, and there are almost four times as many existing condos for sale than last year.

"We think the softness of the market is largely due to the pulling out of investors," said Gopal Ahluwalia, staff vice president for research at the National Association of Home Builders. "They have not only pulled back, they are canceling purchases."

Click on photo for larger image.

Photo Credit: Bubble Meter. From the WaPo article:

... the local Internet blog Bubble Meter focused last month on what it called "the bubblicious bench."See WaPo for a different picture of the bench. An interesting article.

Friday, April 21, 2006

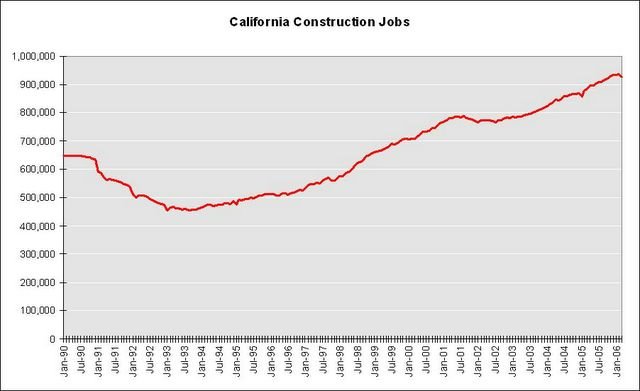

California Construction Jobs

by Calculated Risk on 4/21/2006 06:58:00 PM

The previous post provided excerpts from an LA Times article indicating the number of construction jobs may be decreasing in California.

Click on graph for larger image.

This graph show the number of construction jobs in California since 1990. The housing slump of the early '90s is very clear. Following the business investment driven recession in 2001, construction employment was fairly stable for a couple of years and then started increasing again.

If the small drop in March construction employment is the beginning of a prolonged housing slump, I'd expect employment to fall by a couple hundred thousand jobs over the next few years - similar to the early '90s slump.

LA Times: Construction Decline Means Loss of Jobs

by Calculated Risk on 4/21/2006 05:56:00 PM

The LA Times reports: Construction Decline Means Loss of Jobs

California employment fell in March for the first time since last spring, the state reported today, a drop due almost entirely to a decline in the construction sector as the housing boom comes to a close.From the California Labor Market Information Division:

And the first ripples of the housing slowdown are beginning to be felt in the larger economy.

Over the last four years, soaring house prices generated widespread benefits. Flush homeowners tapped into their newfound equity to pay for new cars, remodeling jobs and lavish vacations, all of which spread the wealth around.

Now, fewer homes are selling, which means builders aren't working overtime to make more of them. That means they need fewer workers — 9,400 fewer in March.

That's one explanation for the overall net drop of 10,800 payroll jobs in March. Another is more modest: it rained a lot in March. This might have worked to keep construction employment down, said state finance chief Howard Roth.

Sectors with increased employment, in order of job gain, were:

Leisure and hospitality (6,500);

Information (3,300);

Financial activities (1,500); and

Natural resources and mining (100).

Sectors with decreased employment included:

Construction (9,400);

Trade, transportation and utilities (4,100);

Professional and business services (3,100);

Government (2,200); other services (2,100);

Manufacturing (900); and

Educational and health services (400).

UCLA on Housing

by Calculated Risk on 4/21/2006 11:48:00 AM

Several economists from the UCLA Anderson Forecast (One of the top rated forecasters) will present at a San Diego conference on May 3rd. Here are some previews:

Christopher Thornberg, a senior economist at Anderson Forecast, said the forecast will be focusing on San Diego because its housing market is the first to follow a nationwide trend of depreciation and a cooling of the real estate bubble.

"A bubble is a function of a period of time where there is expectation in the marketplace and, as a result, people cash in and it feeds up the price," Thornberg said.

He said forecasters are worried about how the housing market will affect the economy.

"We see depreciation starting to flow and overall sales starting to decline, and when real estate markets cool, construction jobs are lost, and real estate and mortgage brokers lose their jobs," he said.

...

Edward Leamer, the director of Anderson Forecast, said the term real estate bubble refers to the extremely high and unsustainable prices for certain assets.

"When the market is hot you get a lot of sales. When the market is cold, the result is that there is a lot of withholding and people don't sell. We're at the initial early warning signs," Leamer said.

He said the housing bubble is 20 to 30 percent off its absolute peak, and with another three to four months of sales volume drops, it will be absolutely clear that the housing bubble has peaked.

"Sales volumes will drop substantially. The popping will be more in terms of sales volumes than with real estate prices," Leamer said.

Thursday, April 20, 2006

$3 Gasoline

by Calculated Risk on 4/20/2006 04:52:00 PM

$3 Gasoline is coming? In California, its already here.

With spot oil prices close to $74 per barrel, $3.00 gasoline might look cheap.

Photo taken April 20, 2006.

Rising Rents and Inflation

by Calculated Risk on 4/20/2006 11:22:00 AM

As the housing market slows, rents are starting to rise. The OC Register reports: No slowdown in O.C. rents

Apartment rents spiked 7 percent in the first quarter to $1,441 a month, compared to the year-ago quarter, said apartment tracker RealFacts in a report expected today.

...

Landlords say they are making up for the years after the '01 dot.com bust when a slowing economy flattened rates.

Rental growth slowed to under 5 percent from late 2001 to early 2005 ...

Click on graph for larger image.

Vacancy rates are declining, but are still above normal for recent years according to the Census Bureau. In regions with higher than normal vacancy rates, vacancies will probably keep rents from rising too quickly. However another concern is that a slowing housing market will lead to higher CPI due to rising Owners' Equivalent Rent. Dr. Altig touched on this yesterday.

"Mike [Bryan] notes that owners equivalent rent accelerated in March, something many folks have been concerned about for some time."

Here is a graph of the monthly changes for Owners' Equivalent Rent (OER). OER is the largest single component of CPI and many people have argued that OER was understated as house prices rose, and that OER would start rising as housing slowed - leading to higher reported inflation.

For those interested in how OER is calculated, here is a description from the BLS: Consumer Price Indexes for Rent and Rental Equivalence

A higher reported CPI might lead to higher rates and further impact the housing market.

UPDATE: Here is a writeup from Asha Bangalore and Paul Kasriel at Northern Trust: The FOMC Finds Itself in a Tight Spot. Excerpt:

"We need to watch the owner’s equivalent rent and rent of primary residence components of shelter costs which are showing an upward trend. Owner’s equivalent rent rose 0.4% in March, after a 0.3% increase in February and a 0.2% gain in January. Adjustments for utilities play a role in the computation of this component in addition to rental prices. The value of landlord provided utilities is subtracted from rent to obtain the “pure rent” measure of owner’s equivalent rent. In situations of rising natural gas prices a larger amount is subtracted to estimate pure rent vs. situations when natural gas prices are falling. The recent decline in natural gas prices could explain to some degree the upward trend of owner’s equivalent rent. In addition, the upward trend of the rent component of shelter costs also contributed to higher owner’s equivalent rent. Higher rents reflect demand pressures on rental property as rising mortgage rates could have priced out otherwise eligible potential home owners. The rent index moved up 0.4% in March after a 0.3% gain in February and a 0.1% increase in January."

Wednesday, April 19, 2006

MBA Purchase Index

by Calculated Risk on 4/19/2006 11:13:00 PM

Thanks to Anon in the comments of the previous post, here is a longer term graph for the MBA Purchase Index.

Click on graph for larger image.

Note: This slide is from the MBA Economic Presentation on Feb 22, 2006.

The Purchase Index YTD average is 420.0, compared to the 2005 YTD of 444.3. That is a decline of just over 5%. However, over the last 6 to 7 weeks, the MBA Purchase Index has averaged about 11% less than the comparable period one year ago.

This is about the decline that David Berson, Fannie Mae Economist, is projecting in his April Forecast for the rest of the year:

Home sales are projected to fall by nearly 10 percent in 2006 in reaction to investor pullbacks and lower affordability."A home sales decline of 10% would probably not have a serious impact on the overall economy in 2006. I think a sales decline of 20% or more would have significant economic consequences - but we haven't seen that yet in the MBA numbers.

Since Feb 22, the Purchase Index has been around 400. Here is the data not included on the chart:

| Date | Purchase Index | 4-Week Average |

| Feb 24, 2006 | 400.8 | 406.6 |

| Mar 3, 2006 | 399.0 | 400.1 |

| Mar 10, 2006 | 403.0 | 402.9 |

| Mar 17, 2006 | 393.6 | 399.1 |

| Mar 24, 2006 | 404.1 | 399.9 |

| Mar 31, 2006 | 438.2 | 409.7 |

| Apr 7, 2006 | 417.7 | 413.4 |

| Apr 14, 2006 | 407.4 | 416.9 |

UPDATE: DoctorWho points to this chart from Fannie Mae:

UPDATE: DoctorWho points to this chart from Fannie Mae:The first chart is mislabeled by the MBA - it starts in 2000. The second chart provides the MBA index since 1990 and shows how the Purchase Index tracks home sales.

MBA: Mortgage Application Volume Down Slightly

by Calculated Risk on 4/19/2006 10:06:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Drops Slightly

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 569.6, a decrease of 1.7 percent on a seasonally adjusted basis from 579.4 one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week and was down 14.9 percent compared with the same week one year earlier.Mortgage rates increased slightly:

The seasonally-adjusted Purchase Index decreased by 2.5 percent to 407.4 from 417.7 the previous week whereas the Refinance Index decreased by 0.4 percent to 1526.1 from 1532.4 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.56 percent from 6.50 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs increased to 6.00 percent from 5.97 percent ...

| Total | -14.9% |

| Purchase | -12.7% |

| Refi | -18.4% |

| Fixed-Rate | -6.2% |

| ARM | -30.5% |

Purchase activity is off 12.7% from last year. This provides further evidence that housing is slowing.