RSS Feed

RSS Feed by Calculated Risk on 4/26/2006 11:50:00 AM

Wednesday, April 26, 2006

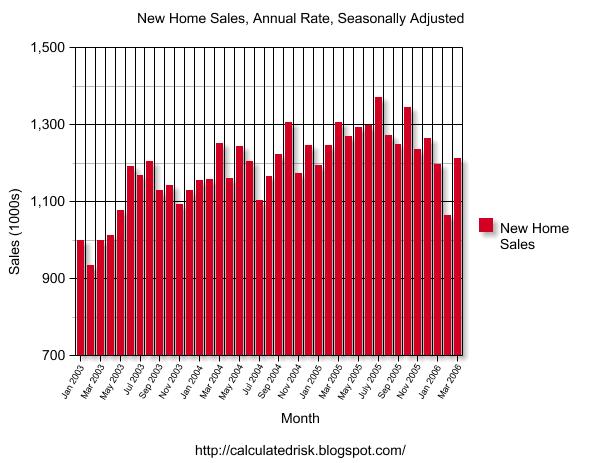

New Home Sales YTD

Is housing slowing? Looking at New Home Sales, the answer is unequivocally yes.

Click on graph for larger image.

New Home Sales for 2006 are below both 2004 and 2005. In February I cautioned "One month does not make a trend, but New Home Sales have fallen in six of the last seven months."

That same caution applies to the March numbers. New Home Sales have now fallen six of the last eight months - a definite down trend. But 2006 is still the third best year so far.

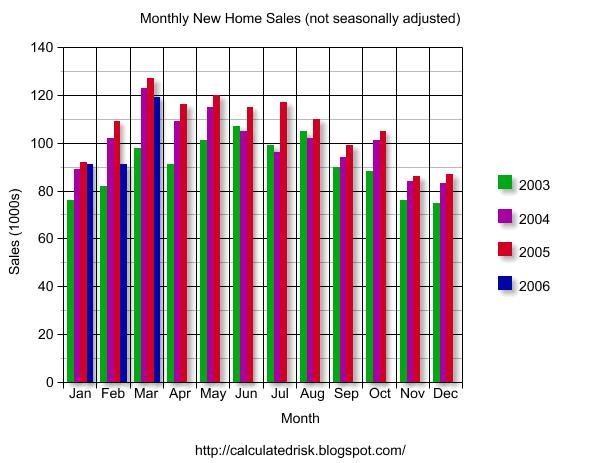

This graph (from the previous post) shows the reported sales (NSA) by month for the last four year. For each month, sales for 2006 have been below 2005.

The reason I follow housing so closely is I expect a slowing housing market to impact the economy.

However, as I wrote last month, "I'd be very concerned if New Home Sales fall below about 1.05 million units annual rate for several months." That hasn't happened for even one month yet.

March New Home Sales: 1.213 Million

by Calculated Risk on 4/26/2006 10:01:00 AM

According to the Census Bureau report, New Home Sales in March were at a seasonally adjusted annual rate of 1.213 million. February's sales were revised down slightly to 1.066 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

The Not Seasonally Adjusted monthly rate was 119,000 New Homes sold. There were 127,000 New Homes sold in March 2005.

On a year over year basis, March 2006 sales were 7.2% lower than March 2005.

The median and average sales prices declined.

The median sales price of new houses sold in March 2006 was $224,200; the average sales price was $279,100.

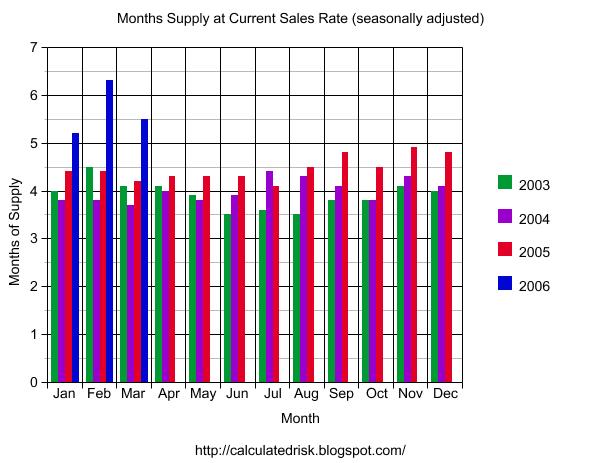

The seasonally adjusted estimate of new houses for sale at the end of March was 555,000. This represents a supply of 5.5 months at the current sales rate.

The 555,000 units of inventory is another all time record for new houses for sale. On a months of supply basis, inventory is significantly above the level of recent years.

Although sales bounced back in March from the February lows, this report shows that the housing market continues to slow down.

MBA: Mortgage Application Volume Down

by Calculated Risk on 4/26/2006 09:44:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Down

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 548.6, a decrease of 3.7 percent on a seasonally adjusted basis from 569.6 one week earlier. On an unadjusted basis, the Index decreased 3.2 percent compared with the previous week and was down 22.4 percent compared with the same week one year earlier. There were no holiday adjustments made for the Easter holiday.Mortgage rates were steady:

The seasonally-adjusted Purchase Index decreased by 4.4 percent to 389.4 from 407.4 the previous week whereas the Refinance Index decreased by 2.4 percent to 1489.4 from 1526.1 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.53 percent from 6.56 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 5.96 percent from 6.00 percent ...

| Total | -22.4% |

| Purchase | -19.1% |

| Refi | -27.4% |

| Fixed-Rate | -14.7% |

| ARM | -36.9% |

Purchase activity is off 22.4% from last year. This is a significant decline from last year and provides further evidence that housing is slowing.

Tuesday, April 25, 2006

Bush Blunders on Gasoline

by Calculated Risk on 4/25/2006 01:27:00 PM

The AP reports: Bush Eases Environmental Rules on Gasoline

President Bush on Tuesday ordered a temporary suspension of environmental rules for gasoline, making it easier for refiners to meet demand and possibly dampen prices at the pump. He also halted for the summer the purchase of crude oil for the government's emergency reserve.Halting the purchase of crude oil for the SPR is reasonable, but the suspension of environmental rules is not. Last year I supported the temporary suspension of environmental rules as a response to the impact of Hurricanes Katrina and Rita. Does the Bush Administration believe the recent increase in gasoline prices is temporary? Or will the suspension of environmental rules become permanent?

NOTE: It makes sense to reduce the number of different blends used around the country to avoid spot shortages, but not to return to the air quality standards of 30+ years ago.

Existing Home Sales

by Calculated Risk on 4/25/2006 10:03:00 AM

UPDATE: The National Association of Realtors (NAR) released their data for Existing Home Sales in March. NAR reported:

Sales of existing homes edged up in March following a strong rebound in February, according to the National Association of Realtors®.Existing Home Sales are a trailing indicator. The sales are reported at close of escrow, so March sales reflects agreements reached in January and February.

Total existing-home sales – including single-family, townhomes, condominiums and co-ops – rose 0.3 percent to a seasonally adjusted annual rate1 of 6.92 million units in March from a pace of 6.90 million in February, but were 0.7 percent below a 6.97 million-unit level in March 2005.

David Lereah, NAR’s chief economist, said sales are leveling out. “It’s a good sign to see home sales holding close to the level of a strong rebound in the month before,” he said. “This is additional evidence that we’re experiencing a soft landing. We may see some minor slowing in home sales as interest rates rise, but the market clearly is stabilizing.” Lereah expects 2006 to be the third strongest year on record for home sales.”

Also note that mortgage applications fell about 10% in February and March (compared to January). This probably indicates that existing home sales will fall in the coming months on a seasonally adjusted (SA) basis.

Click on graph for larger image.

Existing Home inventories rose to 3.19 million units in March. This is the start of the listing season, and I expect inventories to continue to rise.

If sales fall about 10% (as indicated by the MBA purchase index) and inventories continues to rise at the current pace, the months of supply could be over 6 months by Summer. Usually 6 to 8 months of inventory starts causing pricing problem - and over 8 months a significant problem.

New Home sales (released tomorrow) is usually a better indicator of the housing market.

Monday, April 24, 2006

Builders Fret Over Immigrant Debate

by Calculated Risk on 4/24/2006 03:46:00 PM

From BuilderOnline: Builders Fret Over Immigrant Debate: Construction Would Halt Under Stricter Laws, the Industry Warns

In the debate over how to fix the nation's immigration laws, few sectors have more at stake than the construction industry, one of the country's economic bright spots.There is a new home being built right next door to me. The work crews all speak Spanish, although I have no idea if they are legal or illegal immigrants. But it makes me wonder if there are far more people employed in construction than are reported by the Bureau of Labor Statistics.

One of every four workers in construction is an immigrant, according to government statistics.

And as orders for new housing have soared over the last decade, the industry's future has become increasingly intertwined with that of the immigrant workforce.

On any given day, 117,600 mostly immigrant workers around the country either work as day laborers or are looking for such work, according to a recent survey.If the immigrant workforce is underreported, then as the housing market slows, some of the lost jobs might not show up in the BLS data. Just something to keep in mind as we track construction employment in the US and California.

"The immigrant workforce is still keeping the housing market afloat to some extent," said Jerry Howard, chief executive of the National Association of Homebuilders.

UBS: Housing Demand Falling "More Quickly than Expected"

by Calculated Risk on 4/24/2006 02:55:00 PM

From MarketWatch: UBS tempers view on home builders

"The long-anticipated housing slowdown appears to be finally upon us," wrote analyst Margaret Whelan in a research note, citing new-home sales down 21% from their July high, while new-mortgage applications are off 23% from their peak in June.

Yet she noted that markets vary by geography, reflected in the disparity in home-order growth being reported by the building companies.

Whelan's long-standing expectation was a "soft-landing" scenario, reminiscent of the corrections in 1994 and 1995, and also between 1998 and 2000, where new-home sales dipped 20% over a 20-month period.

"Of late, however, the more rapid rate of decline in demand -- down 21% in eight months -- has led us to rethink our thesis for the near term," she said. "Given tough comparisons and a proliferation in for sale listings in some of the hotter markets, demand has fallen more quickly than we expected."

Foreclosures Increasing

by Calculated Risk on 4/24/2006 10:49:00 AM

From Foreclosures.com: Mortgage Defaults on the Rise in West and Southwest

... reported today that foreclosure activity in the first quarter of 2006 increased significantly from the fourth quarter of 2005 in several western and southwestern housing markets.As DataQuick recently noted: "Foreclosure activity is edging up from its bottom, but is still low."

"The biggest increases were in major urban centers around the West," said ForeclosureS.com president Alexis McGee. "For example, Los Angeles County recorded 6,314 pre-foreclosure filings and foreclosures through March, up from 4,911 in Q4 of 2005, while in San Diego the numbers jumped from 1,565 in Q4 of 2005 to 2,241 in Q1 of 2006."

She went on to say that such increases were coincident with cooling markets in previously overheated areas, and with the steady rise in interest rates.

...

She added that rampant speculation in some markets, along with a slowdown in price appreciation would lead to an increase in delinquencies and foreclosures.

"In Las Vegas, this appears to be already happening. Foreclosure activity jumped to 3,246 in Q1 of 2006 from 1,480 in Q4 of 2005. Speculators who came late to the party are being washed out of the market."

She pointed to widespread concern over the number of interest only and high negative amortization loans that had been issued by lenders in recent years as homebuyers sought to qualify for ever more expensive homes during the coastal markets' price boom of the last half decade.

"In San Diego for example," said Ms. McGee, "more than half of home purchases in 2004 and 2005 were financed with these exotic mortgage products. When these loans reset to true market rates the payment shock can be severe and put many households in financial distress."

She referred to a recent study by Dr. Christopher Cagan of First American Real Estate Solutions. Cagan stated that an option ARM with payments of $800 per month could jump to $3000 per month when reset to market rates. "That's a recipe for financial disaster," said Ms. McGee.

Sunday, April 23, 2006

Housing: Fleck and Watts

by Calculated Risk on 4/23/2006 03:15:00 PM

This is the Night and Day of housing.

Fleck (aka Bill Fleckenstein) writes for MSN Money: The housing bubble has popped

And Orange County Real Estate broker Gary Watts provides his view: Housing's #1 fan. Last week, I acknowledged Watt's on-target 2005 prediction, but I think he is wrong about 2006. From Watts:

I am sticking to my 15% gains for resale housing in 2006.From Fleck:

...

I believe that a lot of sellers who were planning on listing their homes during this summer, "jumped-the-gun", thinking that they should get their homes on the market during the spring, when there are an usually large build-up of buyers. If this is true, we will not see the usual increase of our summer listing inventory. If in fact this happens, we will have an "Inverted Year". Usually we have a lot of buyers and few listings but this year, I am betting that the listings will decrease by summer (rather than increase) and more buyers will be in the market, especially with the Fed announcement that the interest-rate increases are finished. This will create more real estate sales activity in the latter half of the year rather than the usual torrid pace of the spring.

Reports of falling sales and investors stuck with properties they can't sell are just the beginning. Property owners should worry; so should their lenders.

...

To me, it's not debatable that the real-estate bust is starting to gather steam. The top was approximately when Time Magazine published its June 12, 2005, cover story: "Home $weet Home: Why We're Going Gaga Over Real Estate".

...

After having leveled off for a while, the real-estate market is now starting to slide. We're seeing signs of sales slowing and inventory accumulating, which are all quite classic ...

It is indeed the financial institutions that are most at risk in the real-estate market (which is not to say that consumers and speculators won't get hurt). The lenders will bear the brunt of the pain, because in many cases, they loaned the entire purchase prices of many homes. As I have said often, the housing bubble has been more a lending bubble. It will be the impairment of the financial institutions that will stop the flow of credit to the real-estate market. In turn, that will accelerate the collapse in house prices somewhere along the way.

Saturday, April 22, 2006

WaPo: Housing Investors in Retreat

by Calculated Risk on 4/22/2006 01:23:00 AM

Kirstin Downey writes in the Washington Post: After Pushing Up Prices, Investors Are Left Holding Too Many Homes

Investors who sought quick profits buying and selling real estate in the Washington region are in full retreat, dampening demand for homes, most notably for condos.

What is becoming apparent ... is how big a part speculators played in the region's real estate boom of the past few years. ... condominiums, ... townhouses and single-family houses, were snapped up by investors using no-money-down financing and non-traditional loans. They helped send prices soaring at unprecedented rates. And now many are trying to sell, or rent at a loss. Some may eventually dump properties at low prices to get rid of them. That could weigh down values for everyone.

Sales of new condos fell 43 percent in the first quarter of the year, compared with the first quarter of 2005, according to one report, and there are almost four times as many existing condos for sale than last year.

"We think the softness of the market is largely due to the pulling out of investors," said Gopal Ahluwalia, staff vice president for research at the National Association of Home Builders. "They have not only pulled back, they are canceling purchases."

Click on photo for larger image.

Photo Credit: Bubble Meter. From the WaPo article:

... the local Internet blog Bubble Meter focused last month on what it called "the bubblicious bench."See WaPo for a different picture of the bench. An interesting article.