RSS Feed

RSS Feed by Calculated Risk on 5/14/2006 05:53:00 PM

Sunday, May 14, 2006

Dr. Duy thinks FED Will Pause

On Economist's View, Dr. Duy writes: FED Watch: To Pause or Not to Pause

"... my interpretation of policy at this point is that the Fed intends to pause at the next meeting while awaiting data that calls into question their expectation of slowing demand later this year. In this light, they will discount nominal signals such as prices and focus on real indicators. Currently, real data on housing and consumer spending are consistent with their null hypothesis."If Duy is correct, ignore CPI and PPI this week, and focus on jobs, consumer spending and housing indicators to predict the actions of the FED in June.

Saturday, May 13, 2006

Foreclosure Stories

by Calculated Risk on 5/13/2006 12:29:00 AM

From the Rocky Mountain News: Playing mortgage roulette

Thousands of Denver homeowners gambled on adjustable rate mortgage loans three years ago. Now those bets are coming up short. These homeowners are facing the hard truth that their ARM mortgage payments are going up several hundred dollars more each month as their rates adjust skyward.Foreclosures In Columbus Are Rising

The higher payments are expected to cost many homeowners in the metro area tens of millions of dollars in extra mortgage payments and drive up the already near-record number of foreclosures.

...

It's a national problem, with an estimated $2 trillion in home loans expected to adjust upward in 2006 and 2007, according to Economy.com, a research firm based in West Chester, Pa.

And the Denver area may be particularly hard hit, because homeowners in Colorado on average have little equity in their homes.

In Colorado, 28.5 percent of homeowners have 5 percent or less equity in their homes, and 47 percent have 15 percent or less equity, according to a report released earlier this year by Christopher L. Cagan, director of research and analytics at First American Real Estate Solutions in Santa Ana, Calif.

Only Tennessee homeowners, on average, have less equity in their homes, according to the report.

This lack of equity is one on the driving forces behind the rising Denver-area foreclosure rate, according to many experts.

This year is on track to eclipse 2005 as the second worst year ever for foreclosures. Last year, more than 14,000 Denver-area homeowners defaulted on mortgages.

Increasingly, people who locked in three-year ARMs with rates in the 4 percent range are finding loan rates rising by 50 percent or more.

"Alot of people actually financed homes they could not afford,"says economist Dr. Mike Daniels.Home foreclosures soar, with Georgia leading the way

And now some economist say the local housing bubble could burst. Experts say forclosures in Columbus are up 25 percent from last year. The culprit -- rising mortgage rates. Something a lot of homeowners didn't budget for.

"I don't think people really read the fine print about what was going to happen to their payment when the interest rates went up,"says Daniels.

New Hampshire foreclosures up; mortgage rates drop

In areas that have seen substantial appreciation, foreclosures are rising, but are still very low. In areas like Denver, foreclosures are already near record levels. Speculation, using exotic mortgages, was nationwide and the negative impact of foreclosures will probably also be national in scope.

Friday, May 12, 2006

UCLA's Thornberg: "Was that a 'Pop' I Heard?"

by Calculated Risk on 5/12/2006 08:10:00 PM

Writing in the East Bay Quarterly, Dr. Thornberg on California housing:

"... there were some legitimate reasons for the increases in prices. The late nineties saw a sharp rise in rental rates around the state, caused by a growing gap between production and demand. The late nineties saw the removal of tax liability on the sale of a home within a certain amount. Then there was the large drop in mortgage rates between 2001 and 2003. But since 2003 there has been little reason to believe the price increases we have seen are legitimate. Mortgage rates are rising slowly, rents are just now starting to recover and with the state permitting over 200,000 units over the last two years those housing shortages seem to be a thing of the past.

A bubble is when the market price of an asset becomes misaligned with what the fundamentals say the asset should be worth. Bubbles form because of buyers who concentrate on trends, not fundamentals. Property prices may have risen for legitimate reasons in the past, but this past performance is being taken as a sign of things to come, even though the drivers of the market point in a different direction. But the force of people rushing into the market to collect what they see as ‘free money’ may be enough to drive up prices all on their own. This self-fulfilling prophesy cannot last forever though. Eventually the harsh reality will settle in, and the markets will come to a halt. It is just a matter of time. The irrationality of the market makes it tough to predict the when, only the eventual direction is known for sure.

The best leading indicator of a cooling real estate bubble is unit sales. The frenzy that characterizes the rush to get some of that free money is best characterized by a run up in units being bought and sold. Unit sales of existing homes in the state have fallen from 140,000 to 110,000 (seasonally adjusted). In the East Bay monthly sales have fallen to about 1900 units, still high but the downtrend continues. New permits for residential structures have also fallen to below 200,000 units for the state, although they remain solid in the East Bay at slightly over 10,000 new units annually. Inventory levels are on the rise in all the major markets according to data from the California Association of Realtors. Make no mistake, all the numbers still reflect a hot market, and are considerably above where they were as recently as 3 years ago. But these markets are very trend sensitive. The slowing of the market feeds on itself, not unlike the acceleration did. When the market was hot, it caused people to rush in to get a piece of the action, causing it to get hotter. Now as it cools, it will cause more people to think twice before buying, causing it to cool more. Going by past trends this slow decline will continue for the first half of this year, and then the bottom will truly begin to drop out.

As for prices, they are still rising. Much has been made of this, and discussions about how unusual it is are common in the press. The real estate community claims it is indicative of a ‘soft-landing’ scenario. Let me be perfectly clear, there is absolutely nothing unusual about the current pattern of slowing in the market. Prices always lag sales activity on the order of six months to a year. With the markets starting to slow as of late 2005 we would expect price appreciation to slow and come to a halt somewhere towards the end of 2006. This is exactly what we are starting to see. From the 25% pace, appreciation has fallen below 10% as of March of this year. Expect it to continue downward.

So is this the time to sell your house and move in with your parents? Only if you happen to be a masochist, and even then it might end up being too painful. Housing bubbles do not pop on the price side, unless there is a substantial loss of employment in the local economy—the kind of employment losses typically associated with a wider recession. And even under those circumstances the price declines tend to be slow. If you need a good example to go by, the breaking of the late seventies bubble would be a good start. While the US economy was dramatically hurt by the deep recession in 1983 and the shallow one in 1981, only in one year—1982, did California actually see a decline in its workforce. As a result prices stayed relatively stable, falling in value only slightly.

Given the current momentum in the general economy, the forecast for real estate is general cooling. Appreciation will slow to a mere 6% (nominal) by the end of this year and will be flat in 2007. Yet the ‘soft landing’ scenario being predicted by the industry is clearly overly optimistic. We predict that sales of existing homes at the state level will fall from 530,000 units sold in 2005 to 390,000 in 2007 and even lower in 2008. New units being built will drop below 150,000 units by 2008. The impact on the real estate and mortgage industries will be substantial.

What risk does the State have? In 2005 brokerage commission fees nationally tallied in at something close to $100 billion. California’s share of this is probably at least 15%, or $15 billion or more. If the average broker pays 7.5% state income tax on this, this suggests that the drop in sales of homes will cause a $1 billion hit to the state in proprietors income alone. Throw in taxes paid by mortgage brokers and residential developers and you can see the revenue problems that will start to accumulate in the latter part of this year. The spillover to the rest of the economy will be noticeable. State employment growth will slow to 1%, and taxable sales growth will slow to 4%. With taxable sales slowing along with income, the state will start feeling the pinch. Do not expect the dramatic collapse we saw in 2001, but then again we have less room to spare.

Of course the industry that has the greatest degree of risk is construction. Is seems doubtful that non-residential construction will be able to pick up the slack in the wake of the slowdown in residential units. We expect residential permits in the state to fall by over a third in the next few years. The decline will be larger in the places that have been building at an incredibly high pace, namely Sacramento, Contra Costa and of course the Inland Empire. Expect new permits to fall by close to 40% in these areas. There will also be a distinct shift in the type of construction, away from pricey higher end units towards entry level units. Local governments interested in promoting the development of affordable housing will find it much easier to get builders to buy into various programs when demand is slack.

The value of non-residential permits have been growing over the past two years, but only due to the increasing cost of construction. In real terms the amount being built has been flat since bottoming out in 2003. Commercial space still has a high vacancy rate, and demand for new space will remain tepid there for a number of years. Retail and industrial space are tight, but these are being driven in part by the high degree of consumer spending on imports. Weaker spending growth will cool demand for these sectors as well. Construction employment will lose 200,000 jobs statewide over the next three years, with an additional unknown number of jobs lost in the informal sector. In the East Bay this will likely translate into the loss of 17,000 construction jobs in three years.

Is there a possibility of a worse outcome? Certainly. Other shocks to the economy, or a rapid closing of the current account deficit could cause a major recession. This would worsen the outlook substantially. But there is no evidence of this secondary possibility at this point in time. So we see the housing crunch as a force that will slow growth, not stop it. Look for weak growth starting beginning the end of this year or early next year and lasting for up to two years. What is clear is that the downside risks are larger than the upside."

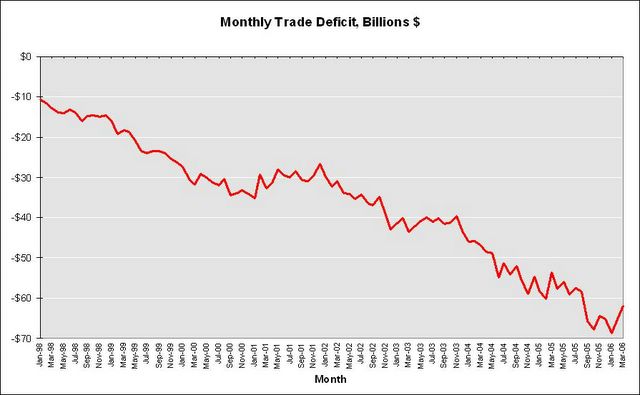

March Trade Deficit: $62 Billion

by Calculated Risk on 5/12/2006 10:56:00 AM

From the AP: Trade Deficit Declines for 2nd Month

The Commerce Department reported Friday that the gap between what the country sells abroad and what it imports narrowed to $62 billion in March, the smallest deficit in seven months. It was a 5.5 percent improvement from February's $65.6 billion deficit which in turn had fallen from the all-time high of $68.6 billion set in January.

Click on graph for larger image.

This graph shows the long term downward trend. Its too soon to argue a trend change, but this month's report definitely surprised me - mostly because import traffic was very strong at the West Coast ports. I will need to look through the numbers this weekend.

For some excellent analysis, see Brad Setser: Not quite as good as they look

Last December I suggested the trade deficit might stabilize, but that prediction was based on a slowing US economy. And the US economy hasn't slowed yet.

Thursday, May 11, 2006

Shiller: Real Estate could lead World into Recession

by Calculated Risk on 5/11/2006 04:07:00 PM

From the GlobeandMail.com: Shiller sees U.S. rally cutting out, Feels housing slowdown could be trigger

Stock markets are still expensive, and investors could be in for an unpleasant surprise once corporate profits begin to weaken, says the Yale University economist who predicted the crash of 2000-2002.

...

Mr. Shiller said the Standard & Poor's 500-stock index is still valued at about 27 times earnings -- far below the bubble-era peak of 46 but still well above the long-term average of about 15. Those numbers are based not on last year's earnings but on a 10-year average of profits.

"I think we could have a number of disappointing years," the economist said in an interview yesterday with The Globe and Mail. "We see earnings growing rapidly, but I feel skeptical about [the sustainability of] that."

...

The trigger for a profit slowdown, he suggests, could be a fall in consumer confidence and U.S. housing prices, the signs of which are beginning to appear in places such as San Francisco, Boston and Miami. Mr. Shiller updated Irrational Exuberance last year and devoted a large chunk of it to his view of speculative bubbles in real estate.

"It looks like we're at the peak" in U.S. housing, he said. "But I can't claim victory yet.

"The equity bust of 2000 produced a mild recession, and was rather short-lived. It's very hard to predict . . . [but] if the real estate market does tank, it will cause a worldwide recession." Falling real estate values "will probably be spread over many countries."

Wednesday, May 10, 2006

Fannie CEO Frets about ARMs

by Calculated Risk on 5/10/2006 05:08:00 PM

From Reuters: Fannie CEO frets about adjustable mortgages

Fannie Mae's chief executive said on Wednesday the U.S. housing market will face significant resetting of adjustable rate mortgages over the next two years and he worries about this sparking foreclosures in some locations.

...

"If jobs are pretty stable, if home prices have come up underneath the mortgages to support them and if there's not any incidence of appraisal fraud, it could be just fine," [Daniel Mudd, president and chief executive officer] said. "If in certain geographies, some of those factors are different -- there's some appraisal fraud, or there's an economic downturn or home prices have declined -- it could be a very different scenario.

"In that case, what you'd worry about, really on a neighborhood-by-neighborhood basis, is you have a foreclosure here and you have a foreclosure there and soon you've got four foreclosures on the market and you've got plywood on the windows and that could have a very deleterious effect," on the market, Mudd said.

REAL Fed Funds Rate

by Calculated Risk on 5/10/2006 03:24:00 PM

UPDATE: Professor Thoma parses the FOMC statement: The FOMC Raises Target Rate to 5%

Using the Dallas Fed's trimmed-mean PCE inflation rate (6 month average, annualized) and the effective nominal Fed Funds rate, the Real Fed Funds Rate is now around 2.5% (assuming current inflation at the same level as March).

Click on graph for larger image.

This graphs shows the REAL Fed Funds rate for the last 20 years. The median is 2.9%; still higher than the current rate. Of course inflation could dip with all the rate hikes already in the pipeline and the REAL rate would increase even if the FED pauses.

But right now inflation, using the trimmed-mean PCE method, is still too high. The FED is probably comfortable with measured inflation in the 1% to 2% range.

The wildcard remains the housing market. If housing slows too quickly (see previous post with 20% drop in the MBA Purchase Index from last year) then the economy might slow quicker than expected and the FED will have overshot.

If inflation remains at this level, or continues to increase, then the FED will have to continue hiking rates.

The June meeting should be interesting.

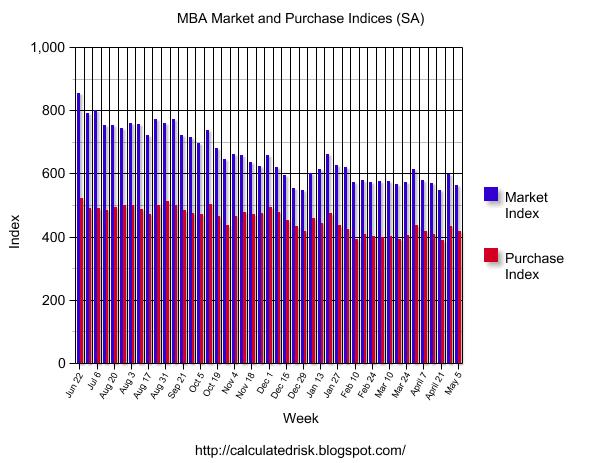

MBA: Mortgage Application Volume Down

by Calculated Risk on 5/10/2006 10:01:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Down

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 562.1, a decrease of 5.8 percent on a seasonally adjusted basis from 596.8 one week earlier. On an unadjusted basis, the Index decreased 5.2 percent compared with the previous week and was down 27.1 percent compared with the same week one year earlier.Mortgage rates were mixed:

The seasonally-adjusted Purchase Index decreased by 3.9 percent to 416.5 from 433.3 the previous week whereas the Refinance Index decreased by 8.8 percent to 1427.4 from 1565.6 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.61 percent from 6.57 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 6.04 percent from 6.08 percent ...

| Total | -27.1% |

| Purchase | -20.7% |

| Refi | -36.9% |

| Fixed-Rate | -19.4% |

| ARM | -41.0% |

Purchase activity is off 20.7% from the comparable week last year.

Tuesday, May 09, 2006

California Real Estate Agent Boom Continues

by Calculated Risk on 5/09/2006 10:06:00 PM

Housing may be slowing, but ...

Click on graph for larger image.

This graph shows the number of licensed Brokers and salespeople in California for each March.

The California Department of Real Estate reports the total number of agents in California is now 490,861, up 0.9% from last month, and up 10% from last March. The number of licensed salespeople has risen 80% since March 2000. The number of Brokers has increased almost 26%.

... the pace of new licensees has not slowed.

The GOP sends me an Email

by Calculated Risk on 5/09/2006 08:31:00 PM

I've made an effort to limit the number of political posts on this blog. This will be an exception ...

As an introduction, I'm a lifelong Republican and former youth delegate to the RNC (when I was in college). The GOP sent me an email today and I've posted excerpts on Angry Bear: The GOP Talking Point.

I'm ready for a change.

Now back to economics ...