RSS Feed

RSS Feed by Calculated Risk on 6/09/2006 10:55:00 AM

Friday, June 09, 2006

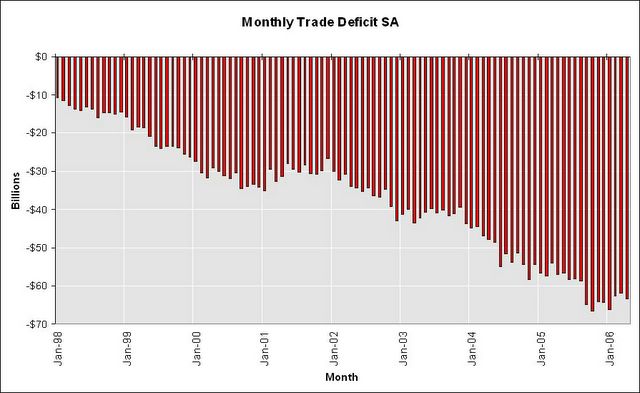

April Trade Deficit: $63.4 Billion

UPDATE: On Econbrowser, See Dr. Menzie Chinn's April 2006 Trade Balance Figures

The Census Bureau reported today that the US trade deficit increased to $63.4 billion in April, compared to expectations of $65.0 Billion.

Click on graph for larger image.

Looking at a multi-year graph, its hard to say if there has been a trend change (is the deficit stabilizing at these levels?) or if the trend is still for increasing trade gaps.

My prediction for 2006 was for the deficit to stabilize at the levels seen in the 4th quarter - mostly because I thought the US economy would slow in 2006. Its still too early to tell.

See Dr. Setser's: Not quite as bad as I expected

Thursday, June 08, 2006

Household Valuation Change: FED vs. OFHEO

by Calculated Risk on 6/08/2006 10:53:00 PM

Last year I compared the change in the FED's estimate of the total value of household real estate with the OFHEO House Price Index (HPI).

The FED's estimate of the value of household real estate is in the Flow of Funds report: B.100 Balance Sheet of Households and Nonprofit Organizations. The FED includes any new stock put into place and improvements to existing stock, so we need to subtract the value of new private single family construction and improvements for the same time period.

OFHEO's House Price Index showed an increase of 2.03% for Q1 2006.

The FED's method showed an increase of 1.85%. Once again, about the same.

FED: 2006 Q1 Mortgage Debt Continues Rapid Growth

by Calculated Risk on 6/08/2006 01:46:00 PM

The FED Flow of Funds report was released today. It shows that household mortgage debt increased significantly in Q1 2006.

On a dollar basis, household mortgage debt increased by $260.7 Billion in the 1st quarter. The last 9 quarters (billions increase in household mortgages, Includes loans made under home equity lines of credit):

q1 2004: $190.4

q2 2004: $211.1

q3 2004: $277.1

q4 2004: $232.9

q1 2005: $189.9

q2 2005: $280.2

q3 2005: $314.8

q4 2005: $293.5

q1 2006: $260.7

From Reuters on debt increase: US household wealth rose in first quarter

'... the Fed said borrowing outside the financial sector soared at an annual rate of 11 percent in the first quarter, faster than the fourth quarter's 9.4 percent pace.

It was the fastest rate of growth in nonfinancial debt since an 11.9 percent rate in the fourth quarter of 1986, the Fed said.

Growth in nonfinancial debt was propelled by an annualized 12.9 percent rise in federal debt, up from a 7.8 percent increase in borrowing in the previous quarter. It was the highest rate of growth in federal debt since the first quarter of 2005.

Household borrowing gained at an 11.6 percent annual pace, up from 11.1 percent in the fourth quarter.

Business debt grew by a 10.4 percent annual rate, up from 8.3 percent at the end of 2005. Borrowing at the state and local government level slowed to a rise of 5.8 percent from 8.6 percent the previous quarter.'

Wednesday, June 07, 2006

MBA: Mortgage Refinance Applications Decline

by Calculated Risk on 6/07/2006 09:59:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Refinance Applications Decline

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 534.4, a decrease of 1.4 percent on a seasonally adjusted basis from 541.9 one week earlier. On an unadjusted basis, the Index decreased 11.7 percent compared with the previous week and was down 28.0 percent compared with the same week one year earlier.Mortgage rates decreased slightly:

The seasonally-adjusted Purchase Index increased slightly to 395.6 from 395.5 the previous week whereas the Refinance Index decreased by 3.8 percent to 1356.0 from 1409.0 one week earlier...

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.60 percent from 6.66 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 6.05 percent from 6.09 percent ...

| Total | -28.0% |

| Purchase | -16.9% |

| Refi | -42.6% |

| Fixed-Rate | -25.6% |

| ARM | -33.1% |

More evidence of a weak housing market in comparison to 2005.

Tuesday, June 06, 2006

NAR: Housing Market 'Vulnerable'

by Calculated Risk on 6/06/2006 10:50:00 AM

Form the National Association of Realtors: Home Sales Settling Down and Appreciation Slowing

The housing boom has ended but sales at historically healthy levels will continue, and price appreciation will return to normal patterns across much of the country, according to the National Association of Realtors®.

David Lereah, NAR’s chief economist, said home sales are settling into a slower pace. “In recent years we were occasionally challenged to find appropriate superlatives to describe surprisingly high home sales,” he said. “Now the housing market has cooled, but 2006 is still expected to be the third strongest on record. In this case, experiencing a slowing from a hot market is a good thing because we need a solid housing sector to provide an underlying base to the economy, and slower appreciation will help to preserve long-term affordability. But this is a time for the Fed to pause on rate hikes because we have some interest-sensitive housing markets that have become vulnerable.”

Existing-home sales are projected to drop 6.8 percent to 6.60 million this year from the record 7.08 million in 2005. New-home sales are forecast to fall 13.4 percent to 1.11 million from a record 1.28 million in 2005. Housing starts are likely to decline 6.2 percent to 1.94 million in 2006 compared with 2.07 million last year.

NAR President Thomas M. Stevens from Vienna, Va., said rising interest rates have slowed home sales in many high cost markets, while job growth has boosted sales in some moderately priced areas. “Broadly speaking, rising inventories have taken the pressure off of unsustainable home price growth,” said Stevens, senior vice president of NRT Inc. “For most of the nation, this means future home price gains will be much closer to the normal returns we expect from housing.”

The 30-year fixed-rate mortgage should average 6.9 percent during the second half of the year, and the unemployment rate is expected to average 4.8 percent in 2006.

The national median existing-home price for all housing types is forecast to rise 5.3 percent this year to $231,300. With more construction in 2006 taking place in lower cost housing markets, the median new-home price is projected to increase 0.8 percent to $242,900.

“Historically, home prices rise 1.5 to 2 percentage points faster than the rate of inflation, so the rise we anticipate in existing home prices this year is actually a little above the high end of historic norms,” Lereah said. “The double-digit home price gains we saw in 2005 underscore what a superlative year it was.”

Inflation, as measured by the Consumer Price Index, is seen at 3.1 percent in 2006, compared with 3.4 percent last year. Growth in the U.S. gross domestic product is likely to be 3.4 percent this year. Inflation-adjusted disposable personal income should grow 3.1 percent this year.

Monday, June 05, 2006

Bernanke: Unemployment Claims Rising

by Calculated Risk on 6/05/2006 04:25:00 PM

From Bernanke's remarks today: Comments on the Outlook for the U.S. Economy and Monetary Policy

"Gains in payroll employment in recent months have been smaller than their average of the past couple of years, and initial claims for unemployment insurance have edged up. These developments are consistent with the softening in the pace of overall economic activity that seems to be under way."(emphasis added)

Click on graph for larger image.

The vertical white line is the start of the previous recession. Initial claims spiked after 9/11 and Hurricane Katrina, but in general the four week average of initial claims changes slowly.

As Bernanke noted, initial claims have been rising. A couple of weeks ago, I suggested this might be an indicator of slowing job market.

This is something to watch before the next Fed meeting.

Bernanke: Economy Slowing, Inflation Too High

by Calculated Risk on 6/05/2006 02:47:00 PM

From MarketWatch: Bernanke notes slowdown but stresses inflation fight

Although the anticipated slowdown in growth is underway, financial markets should not question the inflation-fighting credentials of the Federal Reserve, Fed chief Ben Bernanke said Monday. "There is a strong consensus" among FOMC members to keep inflation low, Bernanke told an international banking forum here. Recent core inflation readings "have been higher in recent months" and "has reached a level that, if sustained, would be at or above the upper end of the range that many economists, including myself, would consider consistent with price stability and the promotion of maximum long-run growth," Bernanke said. These core readings "are unwelcome developments," he said."Therefore, the FOMC will be vigilant to ensure that the recent pattern of elevated monthly core inflation readings is not sustained," Bernanke said. Bernanke said the slow down in the U.S. economy is no longer simply a forecast. "Real domestic product grew rapidly in the first quarter of this year, but the anticipated moderation of economic growth seems now to be under way," Greenspan said.I enjoyed the Greenspan error in the last sentence! This should impact the Fed Funds expectations again.

Expectations of a FED Pause Rise

by Calculated Risk on 6/05/2006 10:49:00 AM

From the Cleveland FED: Fed Funds Rate Predictions

Click on graph for larger image.

After the jobs report on Friday, market expectations are split almost evenly between a pause and one more 25 bps hike.

These are the same graphs that Dr. Altig used to present Monday (See Dr. Altig: Hawk Killer). Now the Cleveland Fed is updating these graphs daily.

Saturday, June 03, 2006

UCLA's Leamer: Housing a "Sick Sector"

by Calculated Risk on 6/03/2006 08:54:00 AM

From Lisa Girion at the LA Times: Weak Job Growth Raises Concerns

UCLA Anderson Forecast Director Edward Leamer said all the speculation about what the central bank and its new chairman, Ben S. Bernanke, should do about rates was folly because of a real estate slowdown that was well underway.A few more comments on the economy from the article:

"I don't think the Fed, at this point, has much control," Leamer said.

"We have a sick sector, the housing sector, and there's not a whole lot of medicine the Fed can provide."

Leamer's group sees declining home sales contributing to a broad economic slowdown that bottoms out at 2% growth and stays there for at least a couple of years.

"It's been a drunken party for several years," he said. "Now, we have to deal with the hangover."

"The slowdown is in place," wrote John Silvia, an economist at Wachovia Corp. "How much and how rapid remains an issue."

"There is now a growing body of evidence — especially among leading indicators — that a meaningful economic slowdown is underway and this will finally cause the Fed to hold" its benchmark short-term rate at 5%, said Bernard Baumohl, executive director of Economic Outlook Group.

"The economy is slowing fast," said Ian Shepherdson, chief U.S. economist at High Frequency Economics Ltd.

Friday, June 02, 2006

Standard Pacific Corp. Warns

by Calculated Risk on 6/02/2006 07:38:00 PM

Yawn ... another homebuilder warns: Standard Pacific Corp.

Net new home orders for the first two months of the 2006 second quarter were down 41% from the year earlier period, driven in large part by an increase in the Company's cancellation rate and continued softening of demand in many of the Company's larger markets. Orders were off in Southern California, Northern California, Florida and Arizona, up in Texas and Colorado and off slightly in the Carolinas. The Company's gross orders for the first two months of the 2006 second quarter were off 22% versus the year ago period.

In light of the decreased order levels for the first two months of the 2006 second quarter, the Company expects to lower its earnings and delivery guidance for the full year and will provide the updated guidance in conjunction with its regularly scheduled earnings release at the end of July.