RSS Feed

RSS Feed by Calculated Risk on 7/20/2006 01:32:00 AM

Thursday, July 20, 2006

Thornberg: Housing a "Classic Bubble"

UCLA Economist Christopher Thornberg is quoted in the San Bernardino Sun: Region's home sales looking like 'classic bubble'

"The soft-landing people are full of nonsense," said Christopher Thornberg, senior economist at UCLA. "This is a classic bubble. And unit sales are falling faster than in past bubbles."I think Thornberg is optimistic.

"We are in the middle of this decline. If we are lucky, prices will go flat. But we are not going to have prices fall like the stock market. You won't see declines of 10 percent or 15 percent per year. What will happen is that prices will flatten out," he said, adding that there might not be housing appreciation until 2011.

Next year will be critical from the standpoint of how the consumer will react to not having "a house cash machine" that can be tapped for spending thanks to rapidly appreciating value.

"A major pullback in consumer spending could get ugly very quickly," he said.

Click on graph for larger image.

This graph shows the price of Los Angeles housing based on the OFHEO housing index. For the real price, the nominal price is adjusted by CPI, less Shelter, from the BLS.

Although I agree prices will probably not fall 10%+ per year, I think the bust will last longer than 5 years and prices will fall steadily in real terms. In the previous California housing bust, prices declined for 6 1/2 years and the median house lost almost 34% in real terms.

Here is a chart of the year to year price declines in Los Angeles according OFHEO.

| Year of Housing Bust | Nominal Annual Price Decline | Cumulative Nominal Price Decline | Real Annual Price Decline | Cumulative Real Price Decline |

| 1 | -1.9% | -1.9% | -5.1% | -5.1% |

| 2 | -1.0% | -2.9% | -3.8% | -8.7% |

| 3 | -5.5% | -8.2% | -7.9% | -15.9% |

| 4 | -7.3% | -14.9% | -9.8% | -24.2% |

| 5 | -6.1% | -20.1% | -8.2% | -30.4% |

| 6 | +0.2% | -19.9% | -2.6% | -32.3% |

| 6.5 | -1.2% | -20.9% | -2.4% | -33.9% |

The worst annual declines occurred in the 3rd, 4th and 5th years of the housing bust.

Wednesday, July 19, 2006

MarketWatch: Bernanke overstates wage growth

by Calculated Risk on 7/19/2006 10:31:00 PM

Rex Nutting writes at MarketWatch: Bernanke overstates wage growth

Fed Chairman Ben Bernanke told senators Wednesday that he sees "some evidence" that wages are finally beginning to catch up with productivity growth ... "It's been slow coming. I want to be clear about that," Bernanke said of wage growth.And on real compensation, Nutting correctly notes:

But the figures Bernanke used in his testimony were not accurate. At several points in his testimony, Bernanke overstated the growth of wages over the past few years.

...

To his credit, Bernanke told Sen. Elizabeth Dole, R-N.C., that the evidence for wages catching up "is not very overwhelming." He noted that "the average hourly earnings number is up about a percentage point this last year versus the previous year."

But even that underwhelming figure is wrong.

According to the Bureau of Labor Statistics, average hourly earnings are up about 3.9% in the past year. Once adjusted for the 4.3% rise in inflation, however, real average hourly earnings are down 0.5% in the past year. The wage figures cover about 80% of U.S. workers.

If you look at nonfarm business compensation per hour, you have real increases about 2.5% over the past few years," Bernanke said. "And if you look at real average hourly earnings, it's much closer to zero."Kudos to Nutting.

The first part of that is true, according to BLS statistics. Real compensation has risen 2.5% cumulatively in the past two years.

The second part of Bernanke's statement is misleading but also technically true: Real average hourly earnings are down 1.6% in the past two years, which is "much closer to zero" than 2.5%.

While real compensation has risen 2.5% in the past two years, productivity is up a cumulative 5.5% over that period.

By that measure, compensation is not catching up with productivity; it is still falling behind.

Bernanke and Disposable Personal Income

by Calculated Risk on 7/19/2006 03:46:00 PM

Professor Hamilton covers some of Chairman Bernanke's positive comments today: Bernanke's latest testimony

This sentence, from Dr. Bernanke's statement leapt off the page (as least for me):

"... favorable fundamentals, including relatively low unemployment and rising disposable incomes, should provide support for consumer spending."Rising disposable incomes?

Click on graph for larger image.

SOURCE: BEA Personal Income and Its Disposition, Monthly

One of my concerns has been that real disposable personal income has been fairly flat for the last 6 months. Consumers have increased their consumption, as measured by real PCE, by borrowing, not from any increase in real DPI.

Perhaps Chairman Bernanke believes that nominal disposable incomes will continue to rise at the about the current pace, even as inflation subsides, thereby increasing real disposable incomes. In that case, rising DPI "should provide support for consumer spending". Maybe.

DataQuick: Bay Area home sales continue to drop

by Calculated Risk on 7/19/2006 02:40:00 PM

DataQuick reports: Bay Area home sales continue to drop, prices reach new peak

Home sales in the Bay Area continued to slow last month as prices reached new highs. Prices increased at their slowest pace in more than three years ...

| Median Home Price | June-04 | June-05 | June-06 | Pct.Chg |

| Alameda | $489K | $581K | $593K | 2.1% |

| Contra Costa | $458K | $558K | $592K | 6.1% |

| Marin | $690K | $815K | $829K | 1.7% |

| Napa | $501K | $608K | $638K | 4.9% |

| San Francisco | $653K | $760K | $778K | 2.4% |

| San Mateo | $646K | $752K | $759K | 0.9% |

| Santa Clara | $549K | $645K | $684K | 6.0% |

| Solano | $358K | $449K | $482K | 7.3% |

| Sonoma | $449K | $557K | $587K | 5.4% |

| TOTAL Bay Area | $516K | $610K | $644K | 5.6% |

I added the June 2004 median prices to give a two year perspective on prices.

"The market is definitely slowing but can only be considered "slow" when compared to the hot market of 2004 and 2005. In reality, today's market is pretty normal and balanced, right between the grim times of 1993 to 1995 and the frenzies of 1999 and 2004-2005. The Bay Area's market is reaching the end of a real estate cycle, it looks like prices could flatten out sometime this fall. What happens after that is anyone's guess," said Marshall Prentice, DataQuick president.

| Homes Sold | June-04 | June-05 | June-06 | Pct.Chg |

| Alameda | 2,922 | 2,730 | 1,991 | -27.1% |

| Contra Costa | 2,772 | 2,640 | 1,900 | -28.0% |

| Marin | 544 | 454 | 435 | -4.2% |

| Napa | 233 | 209 | 189 | -9.6% |

| San Francisco | 847 | 723 | 652 | -9.8% |

| San Mateo | 1,122 | 917 | 765 | -16.6% |

| Santa Clara | 3,543 | 3,220 | 2,562 | -20.4% |

| Solano | 1,055 | 1,147 | 732 | -36.2% |

| Sonoma | 1,066 | 974 | 666 | -31.6% |

| TOTAL Bay Area | 14,104 | 13,014 | 9,892 | -24.0% |

Sales have been falling for two years in the Bay Area. Since DataQuick's President says what happens next is "anyone's guess" - I'll guess we will see falling prices later this year.

MBA: Mortgage Application Volume Declines

by Calculated Risk on 7/19/2006 10:42:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Declines

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 540.8, a decrease of 4.6 percent on a seasonally adjusted basis from 566.8 one week earlier. On an unadjusted basis, the Index increased 36.4 percent compared with the previous week but was down 31.3 percent compared with the same week one year earlier.Mortgage rates decreased:

The seasonally-adjusted Purchase Index decreased by 6.2 percent to 398.5 from 425.0 the previous week and the Refinance Index decreased by 1.6 percent to 1377.6 from 1400.5 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.73 percent from 6.81 percent...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 6.28 percent from 6.41 percent ...

| Total | -31.3% |

| Purchase | -17.8% |

| Refi | -47.4% |

| Fixed-Rate | -31.8% |

| ARM | -30.0% |

Purchase activity is off 17.8% compared to the same week last year. The MBA purchase index has been fairly flat for several months. I expect another drop in the seasonally adjusted purchase activity in the coming months.

Tuesday, July 18, 2006

Fed Funds Rate Predictions

by Calculated Risk on 7/18/2006 09:06:00 PM

Update: Check out Dr. Tim Duy's Fed Watch: Living on a Knife Edge

The Cleveland FED presents the Fed Funds Rate probabilities based on options on federal funds futures. For the next two meetings (August and September), the current probabilities are interesting:

Click on graph for larger image (new window).

For the August meeting, the highest probability is 5.50%; another 25 bps hike.

For the September meeting, the highest probability is 5.25%.

This implies either a pause at both meetings, or a rate increase in August followed by a rate decrease in September.

I think this is the first time in this cycle that we've seen the highest probability FED Funds rate be lower for the further out meeting.

DataQuick: SoCal Appreciation / Sales Weaken

by Calculated Risk on 7/18/2006 02:44:00 PM

DataQuick reports: Southland home prices set record, appreciation/sales weaken

Southern California home prices climbed to a new peak last month but at the slowest pace in more than six years. Prices edged higher even as June sales fell to a seven- year low, the result of higher borrowing costs, more inventory and less urgency among buyers.

| Median Home Price | June-04 | June-05 | June-06 | Pct.Chg |

| Los Angeles | $414K | $475K | $517K | 8.8% |

| Orange County | $540K | $603K | $646K | 7.1% |

| San Diego | $464K | $493K | 488K | -1.0% |

| Riverside | $319K | $393K | $422K | 7.4% |

| San Bernardino | $246K | $322K | $367K | 14.0% |

| Ventura | $500K | $584K | $627K | 7.4% |

| TOTAL SoCal | $406K | $465K | $493K | 6.0% |

I added the June 2004 median prices to give a two year perspective on prices.

DataQuick addessed the apparently price puzzle with rising inventories and falling sales:

"Many view this as a great conundrum: Prices continue to rise, even set records, as sales continue to slow. It happened for two years in San Diego before prices last month finally fell slightly below year-ago levels. We view this as the normal winding down of a real estate cycle, where declining demand gradually erodes price growth until it halts or reverses. We expect more markets to see prices flatten or decline a bit in the second half of this year," said Marshall Prentice, DataQuick president.

| Homes Sold | June-04 | June-05 | June-06 | Pct.Chg |

| Los Angeles | 11,673 | 12,001 | 10,248 | -14.6% |

| Orange County | 4,749 | 4,898 | 3,608 | -26.3% |

| San Diego | 6,208 | 5,663 | 4,301 | -24.1% |

| Riverside | 6,343 | 6,485 | 5.927 | -8.6% |

| San Bernardino | 4,292 | 4,700 | 3.998 | -14.9% |

| Ventura | 1,466 | 1,707 | 1,155 | -32.3% |

| TOTAL SoCal | 34,731 | 35,454 | 29,237 | -17.5% |

Notice that San Diego had declining sales in 2005 compared to 2004. As LA Times writer David Streitfeld noted about the San Diego housing market:

San Diego had the wildest run-up among major California cities, with prices tripling since the mid-1990s. ... The market also began to fade first in San Diego. ...It does appear that San Diego is leading the way, and I think that means declining prices soon in all of SoCal.

Whatever happens [in San Diego], optimists and pessimists agree, will happen later in the rest of the state.

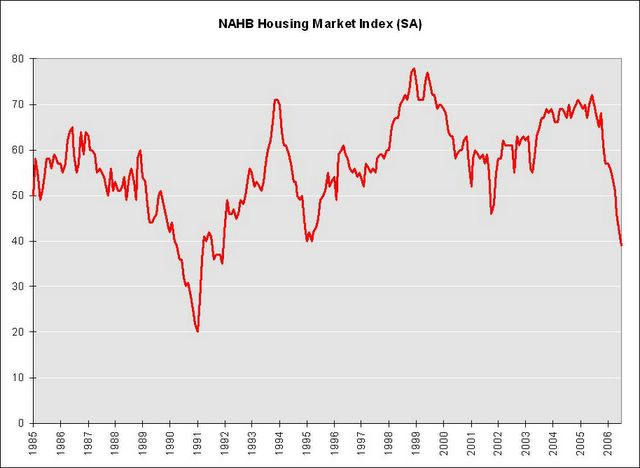

NAHB: Builder Confidence Slips Again In July

by Calculated Risk on 7/18/2006 01:23:00 PM

The National Association of Home Builders reports: Builder Confidence Slips Again In July

Click on graph for larger image.

Increased concerns about interest rates and housing affordability caused builder confidence in the market for new single-family homes to slip three more notches to 39, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI) for July, reported today.

“The HMI is down from its most recent cyclical high of 72 in June of last year, and reflects growing builder uncertainly on the heels of reduced sales and increased cancellations related to eroding affordability as well as an ongoing withdrawal of investors/speculators from the marketplace,” said NAHB Chief Economist David Seiders.

“But just as concerning to many builders is the potential for more monetary tightening by the Federal Reserve that could drive interest rates, and thereby homeownership costs, even higher. Ironically, the Fed’s inflation-fighting moves have helped firm up the rental market and raise the ‘owners’ equivalent rent’ components of the core inflation measures that the Fed is seeking to contain,” Seiders added.

...

All three component indexes fell in July. The largest decline was in the index gauging sales expectations for the next six months, which fell five points to 46. The index gauging current sales of new single-family homes fell four points to 43 and the index gauging traffic of prospective buyers fell two points to 27.

Builders in the West region, who have been the most optimistic in the HMI for some time, recorded the biggest dip in confidence this time around, with a nine-point decline to 51. Builders in the Northeast posted a five-point decline to 36, and builders in the Midwest posted a four-point decline to 21. The HMI for the large South region edged up two points to 50, although this measure still is down considerably from a cyclical high of 77 in June of last year.

“In terms of historical comparison, the HMI’s movement is essentially in line with readings from the 1994-95 period when the Federal Reserve tightened monetary policy and a fairly orderly cooling-down process occurred in the nation’s housing markets,” Seiders observed. “That is what our forecasts anticipate happening in the current period, provided the downside risks of rising interest rates and a bail-out by investors/speculators do not become too pronounced.

With respect to interest rates, we expect the Federal Reserve to maintain the current 5.25 percent target for the federal funds rate for some time, and we’re projecting only modest increases in long-term interest rates from current levels.”

Here is a chart of the various components of the index.

The Housing Market Index cotinues to fall and is now at the lowest level since 1991.

Monday, July 17, 2006

Housing: Skies Not Sunny in San Diego

by Calculated Risk on 7/17/2006 03:26:00 AM

David Streitfeld writes in the LA Times: For San Diego Real Estate, the Skies Are Not So Sunny. Excerpts:

San Diego had the wildest run-up among major California cities, with prices tripling since the mid-1990s. ... The market also began to fade first in San Diego. ...Streitfeld relates some positive comments from a local real estate broker and then notes:

Whatever happens here, optimists and pessimists agree, will happen later in the rest of the state.

That's about the only thing everyone agrees on. The size of the coming hangover is a particularly contentious matter.

Most analysts and people in the real estate industry insist it will be mild. The housing bears say the bulls are either misguided, uninformed or shills.

... the fliers taped to the window outside the office door tell a different story. "Huge Price Reduction," one says. Another says both "Reduced" and "$15,000 Credit."I believe this is just the beginning.

In some cases, the prices are dropping faster than the fliers can be reprinted.

A two-bedroom town home has its price of $324,900 crossed out with a marking pen, replaced by $309,900. Another house, a four-bedroom in suburban La Mesa, has a printed price of $575,000.

Below that is handwritten $549,000.

Scribbled below that is a new minimum: $499,000.

Sunday, July 16, 2006

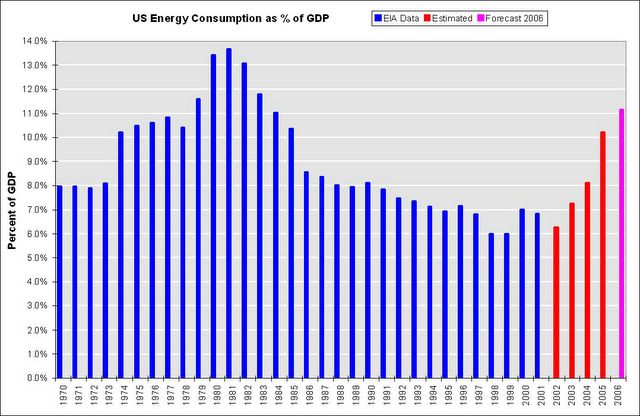

Energy Consumption as Percent of GDP

by Calculated Risk on 7/16/2006 08:31:00 PM

From this Christian Science Monitor article: Oil spike: a surmountable challenge?

... back in 1981, energy was a much larger part of the US economy, representing 14 percent of the gross domestic product, Wyss says. Because energy was so crucial back then, the Federal Reserve pushed interest rates sharply higher to curtail inflation.I've heard this statement before on CNBC several times. Is energy consumption really only 7% of GDP?

Today, energy represents 7 percent of GDP. "The Fed will not have to jerk interest rates up," says Wyss. "We are in better shape."

First, I checked with the EIA: Table 1.5 Energy Consumption, Expenditures. Sure enough, for the last 2 years reported, energy consumption was 7% and 6.8% of GDP. Of course those were for the years 2000 and 2001, respectively.

Energy prices have increased significantly faster than GDP over the last 5 years. Sure enough, it appears Mr. Wyss is using old numbers.

Click on graph for larger image.

Using a combination of EIA numbers for energy sources, and BLS numbers for price changes, and holding consumption steady (very conservative), this graph shows that US Energy Consumption is around 11.2% of GDP right now. (UPDATE NOTE: I'll try to do a more comprehensive calculation later this week - with links and my calculations. this was a rough estimate)

As an aside, ignore Mr. Wyss' comments on the FED. The FED looks primarily at core inflation rates (like Core CPI and PCE). Alhtough the FED is concerned about higher energy prices feeding through to core inflation rates, they aren't really focused directly on energy prices.

On energy issues, see Dr. Hamilton's: Can the economy shrug off $80 oil?