RSS Feed

RSS Feed by Calculated Risk on 8/30/2006 08:24:00 PM

Wednesday, August 30, 2006

Retailer Watch

I've been looking for signs of a retail slowdown. Here is some more news today:

From MarketWatch: Ethan Allen sales slow in August

Ethan Allen Interiors Inc.'s chairman and chief executive Farooq Kathwari ... said sales have further slowed in August. In a statement, Kathwari said lower consumer confidence and the company's initiative to reduce lead time in filling customer orders has impacted the company's first quarter results. ...On July 27, the Danbury, Conn.-based maker and retailer of home furnishings and accessories said written business in past months had slowed from prior-year levels.From Reuters: Costco cuts forecast as discretionary spending slows

Costco ... warned of lower-than-expected quarterly profit because of disappointing margins, as customers cut back on purchases of big-ticket discretionary items such as furnitureOf course, there is this from the AP: Analysts See Solid August Retail Sales

...

The warning from the largest U.S. warehouse club operator took analysts by surprise because Costco's sales growth has been among the strongest in the retail sector in recent quarters.

...

"This could be an early sign that the higher-income consumer is finally starting to feel a bit of a pinch," said Anthony Chukumba, an analyst with Morningstar.

...

Lower-priced chains such as Wal-Mart Stores Inc. have been feeling ... pressure for more than a year because their lower-income customers are most sensitive to rising energy costs.

There are indications that the economic pain is moving up the income scale. Chukumba noted that housewares retailer Williams-Sonoma Inc. ... cut its profit forecast last week.

Back-to-school shoppers are expected to lift August same-store sales for a handful of retailers, though high energy prices and interest rates will have likely tempered overall retail sales.Overall the retail news isn't bad, and these warnings are not large misses. On Thursday, after the market closes, we will find out how the caffeine addicts (Starbucks) are holding up!

This year, August retail sales are also expected to benefit from tax-free holidays declared in 13 states aimed at helping back-to-school shoppers.

Dow Jones: Subprime mortgages see early defaults

by Calculated Risk on 8/30/2006 04:49:00 PM

Via the Contra Costa Times: Subprime mortgages see early defaults

More subprime borrowers are defaulting in the early months of their home loans ... in recent months, an increasing number of lenders catering to borrowers with weak credit have reported a sharp rise in delinquencies that had occurred as soon as six months after origination.So far no real surprise, but ...

Nationwide, about 3 1/2 subprime loans out of every 10,000 originated between January and June had a delinquency on their first monthly payment ... only one out of every 10,000 subprime loans granted last year had experienced missed payment in their first month. ...

"If those borrowers are finding themselves in trouble very early on, it may give lenders an indication that the underwriting criteria or quality control are not sufficiently tight," says Damien Weldon, director of collateral risk analytics at LoanPerformance. ...

Those early defaults have forced lenders such as NetBank Inc., Fremont General Corp. and H&R Block Inc. to buy back loans already sold to whole-loan acquirers, particularly Wall Street investment banks that pool and package those loans into asset-backed securities and then sell them to large investors such as insurance companies and hedge funds. The buybacks, in turn, have led lenders to incur losses and set aside more money in their reserve funds for potential loan repurchases in the future.These buybacks are interesting. I wonder how many loans these subprime lenders might be forced to buy back?

... H&R Block told investors ... "an increase in early payment delinquencies" and the resulting "higher level of repurchase requests from loan buyers" led it to increase its loan reserves. ...

MBA: Mortgage Applications Decline

by Calculated Risk on 8/30/2006 12:18:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Applications Decline

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 556.5, a decrease of 0.9 percent on a seasonally adjusted basis from 561.5 one week earlier. On an unadjusted basis, the Index decreased 2.3 percent compared with the previous week and was down 22.4 percent compared with the same week one year earlier.Mortgage rates increased slightly, after declining for the last several weeks:

The seasonally-adjusted Purchase Index decreased by 1.6 percent to 375.9 from 382.2 the previous week and the Refinance Index increased slightly to 1609.2 from 1608.5 one week earlier. The Purchase Index is at its lowest level since November 2003. emphasis added

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.39 percent from 6.38 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs increased to 5.97 percent from 5.91 percent ...

| Total | -22.4% |

| Purchase | -19.2% |

| Refi | -26.4% |

| Fixed-Rate | -21.3% |

| ARM | -25.2% |

Purchase activity continues to fall and is at 2003 levels. August 2006 purchase activity is off 21.7% compared to August 2005. Year-to-date purchase activity is off 12.9% compared to 2005 and appears to be getting worse.

Interest rates on a 30 year mortgage have fallen from a peak of 6.86%, just two months ago, to 6.38% last week. This has helped boost refinance activity in recent weeks.

The refinance share of mortgage activity increased to 41.5 percent of total applications from 40.6 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 26.8 percent of total applications from 26.4 percent the previous week.It is possible that refinance activity will decline when the new Nontraditional Mortgage Guidance is released in the next couple of months.

Tuesday, August 29, 2006

Study: Housing Market Getting Worse

by Calculated Risk on 8/29/2006 04:17:00 PM

From the Dow Jones Newswire: August Home Data Weak

Sales and home prices fell at a faster clip than expected and inventories climbed further in August as the housing market continued to deteriorate, according to a Banc of America Real Estate Agent survey.

Nontraditional Mortgage Guidance: 60 Days

by Calculated Risk on 8/29/2006 11:57:00 AM

Matthew Swibel writes in Fortune on August 23rd: Dodging A Bullet

"A band of five government regulating agencies led by the Comptroller of the Currency, appear likely in the next 60 days or so to pour cold water on the hot--and lucrative--nontraditional mortgage loan market adored by banks and mortgage brokers. These include the popular, but deadly interest only and pay-option adjustable rate, in which borrowers decide each month how much to repay."Swibel told me that the OCC is "growing frustrated by delays caused by other agencies" and is pushing hard for the release of the guidance.

UPDATE: This paper was released today by the OCC. OCC Working Paper 2006-1, "Foreclosures of Subprime Mortgages in Chicago: Analyzing the Role of Predatory Lending Practices," by Morgan Rose.

This paper suggests passage of the Nontraditional Mortgage Guidance as a possible regulatory action to address rapidly rising foreclosures due to subprime lending:

"A ... candidate for action would be encouraging subprime lenders to review and tighten their lending practices to ensure that their borrowers, especially those seeking refinances, are not taking on more debt than they can handle given their other financial obligations, and that all information relevant to a potential borrower’s ability to repay a loan is considered before extending a loan. This approach is consistent with the recently proposed Interagency Guidance on Nontraditional Mortgage Products, which encourages prudent loan terms and underwriting standards rather than restricting particular loan features. ... this approach has the major benefits of addressing the key role that this paper’s findings indicate low- or no-documentation plays, and being less likely to cause unintended and undesired distortions in the subprime lending market."

Monday, August 28, 2006

America's Long-Term Fiscal Health

by Calculated Risk on 8/28/2006 03:17:00 PM

Over on Angry Bear, I disagree with former Senators Kerrey and Rudman: Just Say No.

Professor Samwick, a new and welcome addition to Angry Bear, agrees with me: First Things First

"... the appropriate target for the General Fund deficit is for it to average to zero over a business cycle. A corollary to that is that the General Fund should be in surplus during the non-recessionary parts of that business cycle. (A slightly weaker target that I would also accept is that the Debt/GDP ratio not trend upward over time.) This Administration seems to have no problem submitting budgets that don't conform to this target. Certainly the Congress doesn't aspire to a higher standard.

So as much as I would like to see the looming financial crises with entitlement programs averted, CR's requirement of the current leadership in the White House and the Capitol is a reasonable one to impose as a precondition for agreeing to a bipartisan effort to address what will be the most immediate budget issues in a decade or two."

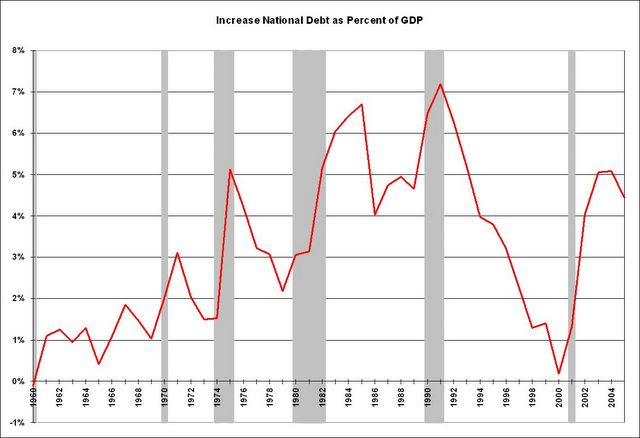

Click on graph for larger image.

Click on graph for larger image.This graph shows the increase in the National Debt as a percentage of GDP since 1960. Recessions are shaded.

Note: Since the graph is based on annual numbers, recessions are approximate. Also, the graph uses the annual increase in the National Debt as a surrogate for the General Fund deficit.

Sometimes there were fiscal policy changes at the same time as the recession (like in '61, '81 and '01), but the cyclical increases in the deficit, related to recessions, are very clear.

If the U.S. economy slides into recession next year, the cyclical increase in the deficit, based on previous down cycles, will probably be on the order of 2% of GDP. Another 2% on top of the current 4% to 4.5% Bush structural deficit is close to 6.5% of GDP. And a 6.5% of GDP annual increase in the National Debt, for a $13.5 Trillion economy, is almost $900 Billion per year!

That is why resolving the Bush structural deficit is so important. If the Bush Administration is serious about improving America's long-term fiscal outlook, let them prove it by taking steps to reduce the structural deficit first, before addressing entitlements.

Bloomberg: Business Spending May Languish

by Calculated Risk on 8/28/2006 02:12:00 AM

Last month I asked: Will Business Investment Rescue the Economy? I was not sanguine.

Here are some further thoughts on business investment from this Bloomberg article: Business Spending May Languish, Raising Risk of U.S. Recession

Forecasts of a moderate slowdown for the U.S. economy this year assume that businesses will accelerate their spending on equipment, helping compensate for any weakening in consumer demand. ...Schwab sent me a recent forecast titled "Recession Watch". The piece made many of the same arguments, without the flair, of Nouriel Roubini.

"Most of the people forecasting a soft landing are counting on a boost from capital expenditures," says Liz Ann Sonders, chief investment strategist at Charles Schwab & Co. in New York. "I would be careful about that." She puts the odds of a recession at more than 50-50, "and it could happen relatively quickly."

"It makes little sense for businesses to accelerate their capital-spending plans at a time when final consumer demand, the largest source of demand, is decelerating," says Jan Hatzius, chief U.S. economist with Goldman Sachs in New York. "We have long been skeptical about the `handoff' concept."The article presents some optimitic views on business spending, and then returns to the theme:

New skeptics are being made too. Donald Straszheim, vice chairman of Roth Capital Partners LLC in Newport Beach, California, says he's reconsidered the prediction he made in December of a business spending binge.

"A business decision-maker would have to be blind not to see what's going on and be rethinking whether they ought to be a little more cautious over the next 24 months," says Straszheim.

Only 21 percent of the firms in the Federal Reserve Bank of Philadelphia's August survey said they expect to increase capital spending over the next six months, the lowest percentage since January 2003. ...And Paul Kasriel of Northern Trust asks the obvious question:

"Capital spending among small businesses is pretty flat," says William Dunkelberg, chief economist at NFIB. "There's nothing really exciting happening there, either in terms of buildings or software and equipment."

"If companies weren't on a spending boom earlier in the cycle, when consumer demand was soaring and their balance sheets were running over with cash, why would they suddenly go on a spending boom now?"This makes sense, and historically residential investment leads nonresidential investment - either up or down. And residential investment is clearly falling. So a business investment boom is possible, but I wouldn't bet on it.

Saturday, August 26, 2006

Residential Construction Layoffs

by Calculated Risk on 8/26/2006 09:42:00 PM

Today I heard, through a company insider, about significant layoffs at one of the major (top ten) homebuilders. I can't confirm the information, so I won't mention the company, but I have been expecting layoffs in the residential construction field to accelerate in the second half of 2006. Click on graph for larger image.

Click on graph for larger image.

Note the scale doesn't start from zero: this is to better show the change in employment.

Currently there are 3.323 million people employed in residential construction in the U.S. according to the BLS. In July, the BLS reported that residential construction employment decreased by 9,000 jobs, and is now down about 37,000 jobs, a decrease of just over 1% from the peak in February.

If the current bust is similar to previous Residential Investment busts, reported residential construction employment might decrease by 800K to 1.3 Million over several years. That means residential construction employment might start falling by 30K per month or more, perhaps as soon as the August report.

This Press Enterprise article has some details on construction layoffs in California's Inland Empire: Construction hitting a wall

Inland home builders accustomed to years of unfettered growth are reassessing their expansion plans, slowing construction, discarding options to buy new land and trying to unload lots they already own.The hope is that these laid off workers will find other work.

...

Major public home builders have quietly begun to dismiss employees. Among the first to downsize in the Inland Empire was KB Home, which this year laid off 39 employees in the region, or about 10 percent of its staff.

"Virtually all the big builders are cutting back head count ... All are cutting costs and the easiest thing to cut unfortunately are people," said Stephen East, an analyst based in St. Louis specializing in public home builders for Susquehanna Financial Group LLP.

The cuts include field superintendents, office clerical workers and upper-level managers in land acquisition and entitlement, said Lee Terry, president of Lee Terry & Associates, an executive search firm for the home-building industry based in San Mateo.

...

Shea Homes recently let go five employees after lower sales projections led to elimination of a planned design center and the outsourcing of some other operations, said Bob Yoder, president of the Inland division of Shea Homes.

...

[Doug McAllister, Western Door's chief executive] said his company has dismissed less-experienced carpenters, and he plans to lay off about 20 percent of his 250 office, production and warehouse workers. He said to retain his best carpenters, he will reassign some to remodeling.

...

RSI Professional Builder Services in Chino ... [a] cabinet manufacturer ... let go 20 people, or about 10 percent of the company's work force, said Eric Vanderheyden, president and general manager.

"We are just scaling back our expectations," he said.

Unemployment in the Inland region is the lowest it has been in several decades, so those who lose jobs in real estate are likely to be rehired, said Inland economist John Husing.I believe Dr. Husing has it backwards; the Inland economy is strong because of residential construction. Therefore I suspect these workers will have a difficult time finding other jobs. And many jobs in housing related industries have non-transferable skills, require low levels of education, and are relatively well paying. So even if these laid off workers find new employment, they may have to take significant pay cuts.

For instance, construction workers no longer needed to build houses could build commercial buildings and public projects or become warehouse workers and truck drivers, he said.

"Anytime something happens like this there is a little pain. But we are better able to handle it than at any time in the 42 years since I have been studying the economy," Husing said.

The August employment report will be released next Friday, and might show the first significant impact of the housing bust on employment.

UPDATE: From Nouriel Roubini: Eight Market Spins About Housing by Perma-Bull Spin-Doctors...And the Reality of the Coming Ugliest Housing Bust Ever ...

And from The Observer: Paul Ashworth, chief US economist at Capital Economics suggests "The downturn in the US housing market will force businesses to slash 73,000 jobs a month in the new year". See The Observer: US housing slump fuels crash fears

Enough Gloom; A Touch of Grace

by Calculated Risk on 8/26/2006 04:38:00 PM

This is a short break from the economics posts.

I found this fan tribute to ... well ... long term readers can guess who.

Enjoy and have a great day!

Friday, August 25, 2006

Lower Growth Forecasts

by Calculated Risk on 8/25/2006 04:36:00 PM

A couple of related stories ...

Just a few months ago most analysts were still very positive on the U.S. economy through '07. Now economists are starting to revise down their growth estimates. As an example, from Globe and Mail: Higher odds of a hard landing

The end of the U.S. housing boom will trim consumer spending, slow economic growth and set the stage for a recession in corporate profits, according to a forecast from economists at National Bank Financial.And from the AP: Housing and fuel strain shoppers

"In light of the swift buildup of the inventory of unsold homes, it is only a matter of time before prices decline at the national level," Clément Gignac and Stéfane Marion wrote in a note.

"In our opinion, a deterioration of household net worth, at a time when the sum of the household energy bill and financial obligations has risen to a record share of disposable income, will force consumers to rebuild their savings rate."

The economists cut their U.S. 2007 economic growth target to 1.9 per cent from a 2.4 per cent projection in July-August, and lowered their expectations for personal consumption growth to 1.4 per cent from 2.3 per cent. They also raised the odds of a U.S. hard landing to 40 per cent from 25 per cent.

"This development will set the stage for a recession in U.S. profits," Mr. Gignac and Mr. Marion said.

Retailers and economists say many Americans are waiting to buy big-ticket items and cutting back on frills. Homeowners are shelving plans to remodel kitchens. Families are dining out less and tightening their budgets.The article mentions the sluggish sales at Lowe's, Wal-Mart and at several casual dininrestaurantsts. The AP article concludes with this frightening story:

"People are taking funds from one area and committing them to another, gasoline and utilities in particular," said Gregory Miller, chief economist at Sun Trust Bank Inc. He predicts growth in consumer spending will fall from a rate of 2.5 percent to around 1.5 percent during the second half of this year, bringing down overall economic growth at the same rate.

At the same time, homeowners are seeing a key source of their wealth lose value as housing prices fall in some parts of the country.

Psychologically, this creates the opposite of the "wealth effect" that kept upbeat consumers spending as stock prices rose in the late 1990s and real estate boomed after the recession in 2001, said Robert Weagley, chair of the personal financial planning department at the University of Missouri.

... After two strong years of sales, business has slowed dramatically this summer [says] David Richardson, the 50-year-old co-owner of Rothschild's Antiques and Home Furnishings in St. Louis.Many people will be surprised at how quickly market psychology can change. I'm reminded of something Stephen Robinett once wrote:

"Look around," Richardson said, gesturing to an empty store. "I'm scared. I don't know what's the right thing to do. Do you stand by the tried and true, or do you move on?"

"Speculative bubbles go on longer and end quicker than most people expect."