RSS Feed

RSS Feed by Calculated Risk on 11/06/2006 04:53:00 PM

Monday, November 06, 2006

UBS: Home Prices to Decline 10% in 2007

From MarketWatch: UBS sees home prices down 10% in 2007

Home prices will fall 10% on average in 2007 and it will likely take three years to clear out the huge inventory of empty unsold homes currently in the market, according to a UBS report released Monday.

Fed's Moskow on Housing

by Calculated Risk on 11/06/2006 04:30:00 PM

Chicago Fed President Michael H. Moskow spoke today on the U.S Economic Outlook. Moskow focused on the housing market:

Residential investment has fallen 7-1/2 percent year-to-date, and in the third quarter it shaved 1.1 percentage points off of GDP growth. Additionally, home prices have been rising more slowly and by some measures have even declined. These developments raise important questions for the economy as a whole: Will there be further declines in housing markets? And will the current and any further declines in housing lead to more general economic weakness?

Here, it's important to remember the positive longer-run fundamentals underpinning housing demand. Since the mid-1990s, the housing capital stock—which reflects the number of homes in the U.S. as well as their size and quality—has been growing about 3 percent per year on average.

This demand for housing has been supported by the step-up in productivity growth, which improved the long-run income prospects for Americans. Furthermore, financial innovations lowered borrowing costs and greatly increased access to credit. As a result, the homeownership rate in the U.S. has increased from 64 percent in the mid-1990s to 69 percent in 2005, with improvements across nearly all demographic and income groups. And many people have put their money into bigger and better homes. Between 1995 and 2005, the size of a typical new home increased nearly 20 percent, and many homeowners invested in home improvements and renovations.

Nonetheless, with underlying housing demand growing 3 percent per year, the large gains in residential investment—which averaged 8-1/2 percent per year between 2001 and 2005—clearly could not continue indefinitely. Moreover, housing demand may slow to less than 3 percent, as demographics point to slower growth in household formation. As a result, we at the Chicago Fed expect some further weakness in residential construction.

By themselves, the declines in residential investment could contribute to some volatile numbers for overall GDP growth, as we saw in the third quarter. But their direct impact on the economy is limited by the relative size of residential investment. Home construction is on average only about 5 percent of GDP—that's about the same as people spend on recreation items such as books, golf clubs, and tickets to theater and opera.

Click on graph for larger image.

Click on graph for larger image.Moskow is correct that residential investment is on average around 5% of GDP (actually the median was 4.5% during the last 35 years). However, residential investment (RI) has recently fallen to 5.7% of GDP from the peak of 6.3% in the second half of 2005. So if RI falls back to the median level of the last 35 years (4.5% of GDP), the decline in RI has just started.

In order to generate more general economic weakness, the housing slowdown would have to spill over into other sectors of the economy. One avenue for this to occur is through home prices. We all know that home prices have soared during the past five years. The factors that caused fundamental increases in the demand for housing should be reflected to some degree in higher home prices. But there is still a risk that prices have also been boosted by factors unrelated to demand fundamentals. If that is the case, prices in some regions could unwind and reduce residential construction. And the negative wealth effects from softening house prices could reduce consumption more than anticipated.

Currently, we do not see the slowing in housing markets spilling over into a more prolonged period of weakness in the U.S. economy overall. On balance, the 95 percent of the economy outside of housing remains on good footing. emphasis added

Roubini on CNBC and more

by Calculated Risk on 11/06/2006 11:54:00 AM

From Roubini: Desperate Realtors... Desperate Retailers... Desperate Housewives...

"It is a lousy time to buy as prices are falling - at an annualized rate of 10% for new homes - and they will be falling another 20 to 30% in the next two-three years as the glut of housing and the bust in the housing market unravels: which fool would buy a home now when a 20% down-payment and the entire equity in such down-payment will be altogether wiped out by a fall in home prices in the next few years? Anyone buying today at the still stratospheric prices will destroy his/her home equity in short order."Reuters reports the opposite view: Greenspan: more housing weakness ahead, worst over

The U.S. housing market will weaken further, but the sharpest decline is over as inventories of unsold homes decrease, Former Federal Reserve Chairman Alan Greenspan said on Monday.And Morgan Stanley's Stephen Jen (whom Brad Setser calls the "anti-Roubini") writes: The Risk of a Recession Within 12 months is Now Only 13%

"This is not the bottom, but the worst is behind us," Greenspan said at a conference organized by financial services firm Charles Schwab.

...

A decline in U.S. home sales and construction has contributed to an overall slowing of economic growth to 1.6 percent in third quarter. But Greenspan said housing activity is likely no longer to be a drag on overall economic growth as unsold inventories clear out and stabilize against sales levels.

The former central banker said he is "reasonably confident" the United States will not slide into recession because businesses appear to be strong, as evinced by strong corporate profit margins and healthy levels of capital investment.

"Overall, we remain comfortable with the view that the bond markets over-reacted to the slowdown in the housing markets, and that the structural US bears may have gotten ahead of themselves in predicting a recession in the US."

Click on graph for larger image.

Click on graph for larger image. Right now it seems like many people are bearish, mostly because the relatively few bears are very noisy and ubiquitous lately. Even though the bear camp is growing, the overwhelming consensus is still for a soft landing (Greenspan, Jen, etc.). The consensus view is GDP will rebound in Q4 and be slightly below trend in 2007. This graph from the FDIC shows the Blue Chip Forecast consensus.

This comment from Setser is an excellent observation:

"The dispersion in credible views about the likely course of the US economy is unusually large."And mostly the difference in views comes down to the impact of the housing bust on the general economy. I think how people view the housing bust, depends on how they viewed the housing boom. Those that felt there was excessive speculation in the housing market (the definition of a bubble) believe that the housing bust has just started. Those that felt the boom was mostly based on fundamentals, with a little "froth", think the bust is almost over.

Obviously I believe there was excessive speculation, so I think the bust has a long way to go.

Monopoly: Housing Bust Edition

by Calculated Risk on 11/06/2006 12:04:00 AM

Click on image for larger version.

Click on image for larger version.

Image from Aaron Erimez. (Hat tip: Satellite Sky)

Enjoy!

Sunday, November 05, 2006

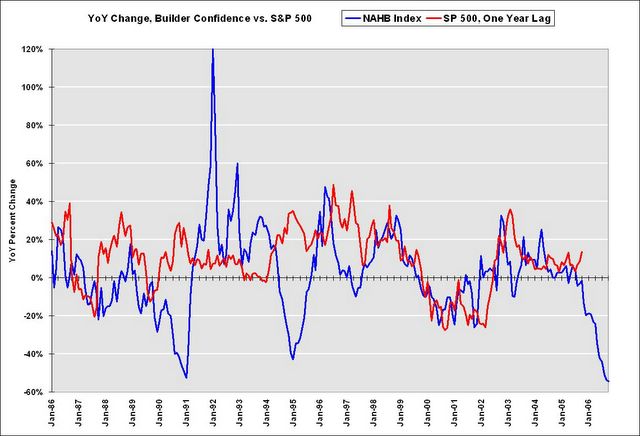

Schwab Chart: Builder Confidence vs. S&P 500

by Calculated Risk on 11/05/2006 01:57:00 PM

Several people have sent me the chart in this CNNMoney article: Can the Economy Survive the Housing Bust?

It turns out that the mood of builders is a terrific stock market bellwether: The correlation between current builder confidence and future stock market returns over the past ten years is downright unnerving.This is an example of a forced correlation. By picking a certain time period, and adjusting the scales, the correlation looks very strong.

Not only did the NAHB index presage the start of the post-1994 bull market in stocks, but its decline starting in 1999 foreshadowed the equity market collapse that came the following year. Builder confidence rebounded in November 2001 - a year ahead of the stock market upswing that began in October 2002.

Why is Sonders worried now? Just look at the chart. Over the past year, the NAHB housing index plummeted 54 percent. Were stocks to follow suit, the S&P - 1400 in late October - would be trading below 700 this time next year.

Click on graph for larger image.

Click on graph for larger image.But here is a comparison over a longer period - since 1985 when the NAHB Builder confidence index was introduced. In the long run, Builder confidence moves between about 20 and 70, whereas the S&P 500 trends higher. So the comparison breaks down over a longer period.

To compare these two series, it would be better to compare the YoY change.

This graphs shows that the YoY changes have tracked closely (with a one year lag for the S&P 500) for the last 10 years, but in earlier years there was very little correlation between stocks and builder confidence.

Once again, I don't like the way the chart was presented, and I don't think there is a long term correlation between the two series.

Saturday, November 04, 2006

NY Times: Incorrect chart on MEW

by Calculated Risk on 11/04/2006 06:29:00 PM

The following chart is from the NY Times article: Mortgage Lesson No. 1: Home Is Not a Piggy Bank Click on image for full chart.

Click on image for full chart.

From the article:

"In the first six months of this year, even with interest rates rising, more than $511 billion was extracted from homes through cash-out refinancing and home equity loans, and that was more than the amount taken out for all of 2005, a record year for mortgage equity extraction."This is not correct. From the Federal Reserve Flow of Funds report, mortgage debt (including home equity loans) increased a total of $436.4 Billion in the first 6 months of 2006. Total household mortgage debt was $9,324.5 Billion on June 30, 2006 as compared to $8,888.1 Billion on Dec 31, 2005. (See line 32 in linked Fed report). Line 32 includes "loans made under home equity lines of credit and home equity loans secured by junior liens."

And that is total mortgage debt. To calculate MEW, household investment in housing has to be subtracted from the increase in total mortgage debt. This includes investment in new homes, home improvements, and various taxes and fees.

The following table is a comparison between the NY Times numbers and my estimates of MEW:

| MEW Comparison: NY Times vs. CR (billions) | ||

| Year | NY Times | CR estimate |

| 2001 | $210 | $156 |

| 2002 | $260 | $331 |

| 2003 | $410 | $453 |

| 2004 | $458 | $504 |

| 2005 | $483 | $540 |

| 2006 (first half) | $511 | $156 |

In general the estimates are fairly close. However the NY Times estimate for 2006 appears to be incorrect.

Friday, November 03, 2006

Unemployment Rate vs. Recessions

by Calculated Risk on 11/03/2006 10:42:00 PM

In the comments to the previous post, ac suggests we "would expect to see the unemployment rate drop to a new low just prior to a recession". This is historically correct. Click on graph for larger image.

Click on graph for larger image.

Historically the unemployment rate has no predictive value. It does not rise right before a recession - in fact it is common for the unemployment rate to set a new low right before a recession starts. Of course, just because the unemployment rate has hit a new low, doesn't mean a recession is imminent either!

The bottom line is the unemployment rate has no predictive value. It is simply a coincident indicator.

Treasury: Mortgage Loan Fraud Continues to Rise

by Calculated Risk on 11/03/2006 06:47:00 PM

From the U.S. Department of Treasury's Financial Crimes Enforcement Network (FinCEN): Assessment Reveals Suspected Mortgage Loan Fraud Continues to Rise

Click on graph for larger image.

An assessment released today by the Financial Crimes Enforcement Network (FinCEN) reveals that suspected mortgage loan fraud in the United States continues to rise, and has risen 35 percent in the past year. FinCEN conducted the assessment, which was based on an analysis of Suspicious Activity Reports (SARs) regarding suspected mortgage loan fraud, to identify trends and patterns that may be useful to law enforcement, regulatory authorities, and financial institutions offering mortgage loan products.Here is the FinCEN report.

FinCEN began its assessment after noticing a significant increase in the filing of SARs concerning mortgage loan fraud.

WSJ: The New Word in Home Sales: 'Canceled'

by Calculated Risk on 11/03/2006 03:44:00 PM

From the WSJ: The New Word in Home Sales: 'Canceled' (update: for those without WSJ AZCentral has the story too).

A little over a year ago, buyers couldn't wait to sign contracts to purchase homes. Now, many can't wait to get out of them.A few stats:

With real-estate prices falling around the country and even pro-industry trade groups predicting further declines over the next year, buyers are backing away from deals in droves. At a semiannual housing forecast conference last week in Washington, D.C., economists reported that contract-cancellation rates for big builders were running around 40 percent - about twice as high as last year's levels. Anecdotally, real-estate professionals say they are seeing a similar dynamic in existing-home sales.

Some of the cancellations are by people who signed new-home contracts at one price months ago, haven't yet closed, and are now stunned to see the builder drastically cutting prices on identical properties. Some are by speculators caught short by other investments they can't unload. And some are by people trapped in a chain reaction: They can't sell their old home - or the buyer has canceled the contract - so they are being forced to cancel the deal on a new house they are buying somewhere else.

New-home builders are taking a big hit from record numbers of contract cancellations, or "kickouts." Fort Worth, Texas-based D.R. Horton Inc., the nation's biggest developer, says its cancellation rate is currently 40 percent, compared with 29 percent a year ago. Meritage Homes Corp., in Scottsdale, Ariz., is reporting a 37 percent kickout rate, compared with 21 percent a year ago. And Standard Pacific Corp. says that 50 percent of its contracts fell through in the third quarter of this year, compared with 18 percent for the same period last year.And on existing homes:

Cancellations by buyers of existing homes are up as well. Although no formal measures exist, historically they have been in the 2 percent range...

Sean Shallis, senior real-estate strategist for the Shallis Team of Re/Max Villa Realtors in Jersey City, N.J., says that roughly 22 percent of his sales have fallen apart before closing this year because the buyers backed out, up from 10 percent last year.

...

Kickouts were high nationwide in the late 80s, and in California and New England in the early 90s, spurred by massive job losses. But until now there's never been a period where cancellations have spiked in the absence of a recession...

FDIC: Economic Conditions and Emerging Risks in Banking

by Calculated Risk on 11/03/2006 02:02:00 PM

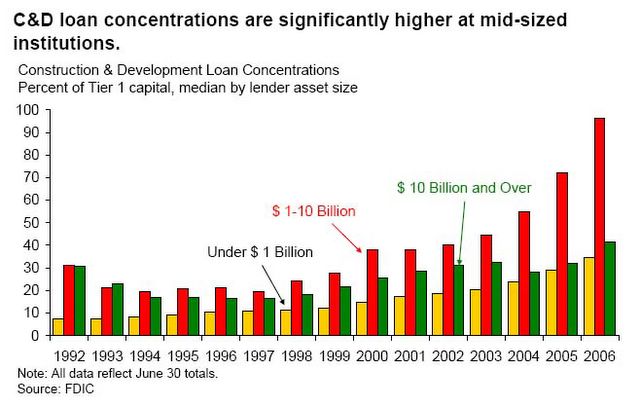

The FDIC Semiannual Report: Economic Conditions and Emerging Risks in Banking has been released. The report identifies several risks: declining Net Interest Margins because of the inverted yield curve, the housing market in general and sub-prime lending specifically, looser lending standards and concentration risk - especially for mid-sized institutions - in commercial real estate (CRE) and construction & development (C&D).

Before noting the negative comments, the FDIC outlook is the same as the consensus: a soft landing.Click on graph for larger image.

GDP is expected to grow at a rate below its long-run average over the next year due to the combination of a slowing housing market, continued high energy prices, slowing production in the auto industry, and lagged effects of previous interest rate increases. However, the corporate sector continues to perform well. Corporate profits currently make up more than 12 percent of GDP—the highest proportion since the 1960s—and grew more than 20 percent in the twelve months to June 30, 2006. Corporate balance sheets are also strong and reflect a debt-to-net-worth ratio for the second quarter of just over 40 percent, the lowest point since the mid-1980s.The FDIC expressed concern about households:

Household liabilities, on the other hand, reached an all-time high of more than 19 percent of assets by the end of the second quarter 2006, as the personal saving rate has fallen into negative territory for five consecutive quarters. Housing-related debt service costs are at all-time highs, and use of home equity loans has slowed sharply as the effects of recent interest rate increases set in.The second graph shows declining Net Interest Margins (NIMs) due to the inverted yield curve:

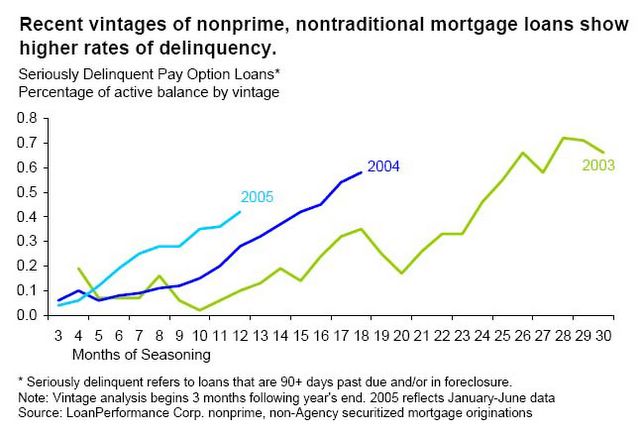

... the Treasury yield curve, which exhibited a small positive slope at the time of our last report, is currently more inverted than at any point since 2001. The inverted yield curve is pressuring lending institutions, which tend to have liabilities priced according to short-term interest rates and assets priced according to long-term interest rates. As a result, NIMs have fallen, particularly at large institutions, whose liabilities are more elastic than smaller banks’ due to their smaller percentage of core deposits. Four of six Regional Risk Committees cited interest rate risk as a potential concern due to the flat-to-inverted yield curve and narrowing margins.After reviewing the "softening housing market", the FDIC expressed concern about nontraditional mortages:

It is very likely that both delinquency and foreclosure rates will rise if the housing slowdown deepens. The first fault lines likely to appear in mortgage credit performance would be among highly leveraged, variable rate borrowers who have stretched their financial resources to purchase a home during the recent housing boom. Five of six Regional Risk Committees reported some level of concern about future performance of prime residential loans due to slowing home price appreciation.

There are emerging signs of potential credit distress among holders of subprime adjustable-rate mortgages (ARMs). Nationwide, foreclosures started on subprime ARMs made up 2.0 percent of loans in the second quarter, up from 1.3 percent in mid-2004. Subprime ARMs are experiencing stress in states as diverse as California, which has had rapid home price gains and solid economic performance, and Michigan, where house prices have been stagnant and the economy is weaker. This suggests that national factors, like interest rate increases, are important factors behind subprime mortgage credit stress, in addition to local economic or housing market conditions.

Certain household-sector developments that have emerged during the recent housing boom could potentially amplify the adverse effects of a housing slowdown. These developments include: (1) a negative personal saving rate and unprecedented levels of home equity liquidation, (2) a greater degree of homeowner leverage, and (3) much broader use of so-called alternative mortgage products, including interest-only and payment option mortgages. With household finances already under pressure from high financial obligation ratios, these developments may place homeowners in a more tenuous position than has been the case prior to previous periods of housing weakness.And another area of concern is the concentration of loans for CRE and C&D:

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loan

concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.

In Memoriam: Doris "Tanta" Dungey

| Privacy Policy |

| Copyright © 2007 - 2025 CR4RE LLC |

| Excerpts NOT allowed on x.com |