RSS Feed

RSS Feed by Calculated Risk on 12/18/2006 04:00:00 PM

Monday, December 18, 2006

NAHB: Builder Confidence Declines in December

by Calculated Risk on 12/18/2006 01:12:00 PM

From NAHB: Builder Confidence Holding Steady in December

At 32 for the present month, the overall HMI is down a single point from November but remains above the recent low of 30 in September.

Click on graph for larger image.

Click on graph for larger image.The only component index to register a decline in December was the one measuring traffic of prospective buyers which, after a three-point jump last month, returned to its October level of 23. The component gauging current single-family home sales remained even at 33, up slightly from its recent low, while the component gauging sales expectations for the next six months rose three points to 48 – its third consecutive monthly gain.

Regionally, the HMI posted the biggest gain this time around in the Midwest, which has shown the greatest weakness in this measure for many months. That region posted a 7-point gain to 22 on the confidence scale, while the Northeast was unchanged at 37, the South dropped a point to 39 and the West declined four points to 31.

Sunday, December 17, 2006

What year is it?

by Calculated Risk on 12/17/2006 11:59:00 PM

Dr. Christine Chmura, president and chief economist at Chmura Economics & Analytics, says the economic pessimists aren't looking at the complete picture. She writes in the Richmond Times-Dispatch: Consumer debt high, but there's more to the story.

"...the Fed reports that household debt service payment (interest and principal) of homeowner mortgages relative to disposable personal income was 11.6 percent in the second quarter of 2007, the highest ratio on record since the data were first calculated in 1980.But Chmura says:

Combining mortgage debt, consumer debt and other financial obligations -- auto leases, rental payments, homeowners insurance, property-tax payments gives the broadest view of debt for households.

Once again the Fed reports that this debt-service ratio for households is the highest on record: 14.4 percent of disposable personal income.

Couple this information about consumer debt with a significant slowdown in home-price acceleration, and pessimists point toward a soon-to-occur recession."

"[The pessimists] haven't looked at the complete picture.Never mind that Chmura mixes flows with stocks, more importantly she could have written this piece in mid-1990 - just as the early '90s recession started.

A full balance sheet reflects assets as well as liabilities. As of the third quarter of 2006, household assets were at a record $67.058 trillion. Rising values in real estate and equities contributed to the increase.

More important, net worth hit a record $54.063 trillion during the same quarter.

So ... when the bills roll in over the next month, just remind yourself that the consumer engine that fueled an expansion still has the ability to support more spending and keep the economy robust."

Chmura notes that the mortgage portion of the homeowners financial obligation ratio (FOR) was a record 11.6% in Q2 2006. In Q2 1990, the ratio was a then record 10.9%. The Q2 2006 debt service ratio (DSR) was a record 14.4%; in Q2 1990 it was a near record 11.96%. And in Q2 1990, pessimists were also concerned about "a significant slowdown in home-price acceleration".

But if someone just looked at the household balance sheet in Q2 1990, everything looked great (Fed: Flow of Funds). Assets were a record $23.7 Trillion and net worth hit a record $20.1 Trillion in Q2 1990.

And then the recession started ...

Saturday, December 16, 2006

Silent Night

by Calculated Risk on 12/16/2006 12:04:00 AM

A short clip from the CSI: New York episode "Silent Night" that aired this week. You know who played a skating star (a stretch!) whose best friend is murdered. This is the ending sequence of the episode:

Friday, December 15, 2006

WSJ: The old rules don't apply

by Calculated Risk on 12/15/2006 06:39:00 PM

The WSJ suggests:

"... the U.S. central bank and much of Wall Street are now betting that the old rules don't apply, and that a recession next year, while possible, is unlikely."And the WSJ quotes Dr. Leamer:

"This time will be different," Ed Leamer, who heads the forecasting center at the University of California at Los Angeles's Anderson School of Management, predicts in a report. "This time the problems in housing will stay in housing." It's a prediction, he admits, that "keeps us up at night."Will this time be different? Will the problems in housing stay in housing? Or will the problems spread to the general economy?

A Citigroup research note on retailers this morning starts with:

"We have a neutral outlook on the ... retailers in our coverage universe ..."And concludes in BOLD:

"We are keeping a close watch on the housing market as we progress through 2H06."Obviously asking: Will the problems in housing stay in housing?

Current data, like the better than expected November retail numbers (although Q4 is still on track to have the weakest nominal retail growth since the 2001 recession), indicate the housing bust might not be significantly impacting retail sales yet. Other data, such as from trucking company YRC Worldwide, are not as comforting:

"... the economy has slowed significantly in the fourth quarter, resulting in lower volumes than we anticipated across all of our asset-based business units," stated Bill Zollars, Chairman, President and CEO of YRC Worldwide.... Fourth quarter tonnage is projected to be lower than 2005 by a mid-single digit percentage for each business unit.And more:

[Jordan Alliger, an analyst at Deutsche Bank] cited perceived risks to the economy in 2007, which could further weaken the unusually sluggish demand truckers have witnessed in the second half of this year.But the key isn't what is happening right now; the key is what happens early next year. (Note: I know I've been repeating this timing for some time - but it is almost here!).

...

"Should the peak season volume malaise extend deeper into 2007 and call into question the so-called 'soft-landing' economic scenario, we could yet prove far too conservative with our newly revised down forecasts," the analyst wrote.

Justin Yagerman, an analyst at Wachovia Capital Markets, said the soft freight demand raises concern about the health of the economy.

"Conversations with carriers have shown no indication of improving economic forces as freight demands remain muted," Yagerman said in a research note on Wednesday.

Residential construction layoffs will be significant soon (probably starting this month or in January). Home equity extraction has been falling rapidly. Nonresidential construction might have peaked. Foreclosures are rising and will probably be at, or near, record levels in 2007 (at least in California). And issues with mortgage credit quality are finally coming to light.

We will find out soon if the "problems in housing will stay in housing". Right now I'm not sanguine. And I can understand why Dr. Leamer has trouble sleeping.

DataQuick: California Sales Lowest Since 1998

by Calculated Risk on 12/15/2006 02:59:00 PM

DataQuick reports: California November Home Sales Click on graph for larger image.

Click on graph for larger image.

A total of 39,200 new and resale houses and condos were sold statewide last month. That's down 8.3 percent from 42,750 for October and down 23.5 percent from a 51,250 for November 2005.Although some areas are already seeing YoY nominal price declines (Bay Area, San Diego, Ventura), the median YoY price in California increased slightly.

Last month's sales made for the slowest November since 1998 when 37,928 homes were sold.

The median price paid for a home last month was $469,000. That was up 0.4 percent from October's $467,000, and up 2.4 percent from $458,000 for November a year ago.

Tanta: Let Slip the Dogs of Hell

by Calculated Risk on 12/15/2006 10:26:00 AM

I still haven’t gotten over the fact that there’s a “capital management” group out there having named itself “Cerberus”. Those of you who were not asleep in Miss Buttkicker’s Intro to Western Civ will recognize Cerberus; the rest of you may have picked up the mythological fix from its reprise as “Fluffy” in the first Harry Potter novel. Wherever you get your culture, Cerberus is the three-headed dog who guards the gates of Hell. It takes three heads to do that, of course, because it’s never clear, in theology or finance, whether the idea is to keep the righteous from falling into the pit or the demons from escaping out of it (the third head is busy meeting with the regulators). Cerberus is relevant not just because it supplies me with today’s metaphor, but because it was the Biggest Dog of three (including Citigroup and Aozora, a Japanese bank) who in April bought a 51% stake in GMAC’s mega-mortgage operation, GM having, of course, once been renowned as one of the Big Three Automakers until it became one of the Big Three Financing Outfits With A Sideline In Cars. I tried to find a link for you to Aozora Bank’s announcement of the purchase, but the only press release I could find for that day involved the loss of customer data. They must have been so busy letting GMAC into the underworld that the dog head keeping the deposit tickets from getting out got distracted.

The third Big Dog with a new stake in GMAC is Citigroup, who sent out a cute “Industry Note” on 12/13/06 on the subject of the coming consolidation in the mortgage biz. It so happens that I was doing some heavy drugs on the 13th, but apparently I wasn’t the only one (I, on the other hand, am getting over it). The thing I really like about the Citi note is that everything comes in threes:

Meanwhile, the [mortgage] industry is facing several ‘hot–button’ issues, including:I hate to make you wait, so here’s the punchline:

• increased regulatory scrutiny of exotic mortgages and option adjustable rate mortgages (option ARMs),

• resetting rates on hybrids,

• deteriorating credit on subprime and Alt A mortgages.

Key questions for investors relate to how these issues influence volume, margins and credit going forward:

• Will the recent declines in originations continue, especially given higher long-term rates and relatively lower purchase mortgages?

• Will margins continue to contract, as competition for shrinking volumes is intense, and several players make apparently desperate efforts to keep activity in-line with recently beefed-up capacity?

• Will credit become more of an issue as ARM rates reset higher and consumers feel the pressure of higher credit card payments and energy costs?

We think the answers to these questions are, for the most part, “No.” . . .OK, so there was slightly more detail to that answer. As in, there are three reasons why Citi thinks the mortgage origination side will “rationalize” in 2007:

1. First, we expect a continued market share shift away from the industry’s weaker players, toward those with dominant scale and diverse and flexible production channels (i.e., retail, wholesale, and correspondent).Now, I’m just a Little Mortgage Weenie, not a Big Finance Dog, but bear with me while I ask some stupid questions. Like: how do the Big Dogs maintain “diverse and flexible production channels” (i.e., little mortgage banker Puppies to sell you correspondent business and little broker Puppies to sell you wholesale business) when “market share currently held by top-tier players” expands to two-thirds (meaning less diverse off-load strategies for the Little Puppies in the “production channels,” putting them at further pipeline/counterparty risk unless they become Bigger Puppies, which makes them competitors instead of “channels,”), while at the same time watching some of the Little Puppies (in whom the Big Dogs have a major equity stake) crawl under the porch to die? I know Citi doesn’t seem to have noticed that the “increased regulatory scrutiny” is not just of “products” but of “wholesale operational/management controls,” but I did. Anyway,

2. Second, we look for further industry consolidation, likely driven by the pressures of market forces (lower volumes and margins) on second- and third-tier players. The market share currently held by top-tier players (47% held by the top five originators) should expand toward two-thirds and beyond over the foreseeable future.

3. Third, we think the ultimate failure and/or closure of certain weaker market participants is a distinct possibility - given the changing economics of mortgage production and securitization sales during the current post-refinancing cycle. While the timing of such potentially market-disruptive failures/closures is difficult to predict, we believe the most likely casualties will be those players that lack the necessary scale efficiencies and flexibility to adjust to an increasingly competitive environment.

In fact, several mortgage industry deals have recently emerged, as a few Wall Street firms have shown their increased interest. Notable transactions include Morgan Stanley’s agreement to acquire Saxon (for $706 million), Merrill Lynch’s agreement to buy NCC’s First Franklin (for $1.3 billion), and Bear Stearns’ agreement to buy the mortgage unit of ECC Capital Corp (for $26 million). In addition, a few large monoline mortgage players have either announced plans to sell or are pursuing strategic options, including ACC Capital Holdings’ search for a possible buyer for Ameriquest, H&R Block’s announced exploration of strategic options for its Option One mortgage unit, and ABN AMRO’s recently disclosed decision to put its mortgage business on the block. Finally, the recent unceremonious closure of Ownit Mortgage, which was apparently unable to find a prospective merger partner, seems likely to be the first of potentially many large mortgage operations that may be shuttered due to the industry’s current excess capacity.Ownit’s “unceremonious” problem was it couldn’t find a merger partner? According to Marketwatch, “Ownit was formed in 2003 when Merrill Lynch, Interthinx, Mindbox, C-BASS, Litton Loan Services and other ‘key industry vendors’ formed a strategic alliance with [Bill] Dallas to buy a wholesale mortgage company called Oakmont Mortgage.” Bill Dallas used to run Little Subprime Dog First Franklin until it found a home with a Medium Respectable Bank Dog National City, who just offered to unload it on Big Wall Street Dog Merrill Lynch, who is rumored to be a 20% stakeholder in Ownit (Dead Puppy). As far as I can tell, the “unceremonious closure” of Ownit came about when Merrill, and possibly some other bankers, shut off Ownit’s warehouse line of credit without prior notice, preventing them from funding any more worthless loans. Well, you could call that an “excess capacity” problem. You could say they just needed a “merger partner.” You could smoke dope with all three of your heads.

(Sidetrack: Citi notes that PHH is a possible Medium Dog merger/acquisition target. I am old enough to have spent years trying to teach myself to stop calling PHH PHH after it became Cendant. I have only just barely gotten used to calling it PHH again after Cendant’s exciting descent into the Underworld. Now this old dog has to learn a new trick? I have no idea why I would bother; I’m beginning to doubt that any of these dogs will come when called anyway.)

I bring all this up not just to stick it to Citicorp, but because we’ve all been asking the question lately of who will be the bagholder when the exotic/subprime mortgage problem finds a home. We have noted in our discussions that credit risk can move in two directions: the wholesaler takes it off the originator and the bond investor takes it off the wholesaler/issuer with the helpful assistance of protection sellers in the hedge fund credit-swap market, but when the “DETOUR” signs pop up, the bond investor can work really hard on forcing it back to the wholesaler/issuer, who can try to put it back to the originator, who gets to try to recover something in a foreclosure sale. If the originator has any financial strength left to buy loans back with, that is; see the sad stories of Ownit, Option One, Fremont, New Century, etc. The “disintermediation” of the mortgage origination side keeps the Big Dogs “flexible,” meaning able to withstand cyclical downturns in the business, but the burning desire on the Street for “vertical integration” seems to mean an endless appetite for erasing that flexibility by buying up the originators of junk, so that they will have paid what one assumes is real money for the privilege of buying back their own loans right at the time they get the “flexibility” of not buying any more of them from the “intermediaries.” If you thought the only thing that would stop the circle jerk of risk was putting some credit and pricing discipline into the game, I guess you’re just a weenie like me. Anyone who can make sense of this is free to set me straight. And if the answer has “sorting socks” in it, don’t bother. I’ve tried that.

There’s some more interesting stuff in the Citi note that I’ll try to share with you later. Let me just leave you with this last bit:

Over the near-to intermediate-term (next 12-18 months), we believe mortgage industry rationalization will be driven by cyclical market forces – including lower originations, weaker margins, and deteriorating credit. We also expect recent secular shifts to influence consolidation next year, including new stricter regulatory oversight of “nontraditional” products, expanding advantages of diversification and economies of scale, and increased demand by Wall Street firms for the “raw materials” (manufacturing and servicing) necessary to vertically integrate the mortgage business.Am I too old to understand what the term “secular” means these days, or do I just not have enough heads? Or maybe this is all about theology, not finance, and “secular” just means whatever is in Hell next year. Thank Heaven someone’s guarding the gates thereof: a hedge fund.

Thursday, December 14, 2006

Has Nonresidential Construction Peaked?

by Calculated Risk on 12/14/2006 09:10:00 PM

Most of my focus has been on residential construction and the impending residential construction layoffs. Now is probably the time to start looking for declines in nonresidential construction.

Historically nonresidential investment (including nonresidential construction) has trailed residential investment by about 3 to 5 quarters. Since residential construction spending peaked in December 2005, and residential construction employment peaked in February 2006, it is about time for nonresidential construction to peak - if spending and employment follow the common historical patterns (note: there have been a few exceptions). Click on graph for larger image.

Click on graph for larger image.

The first graph shows seasonally adjusted private employment for both residential and nonresidential construction. Note that the graph does not start at zero to better show the changes in employment. Source: BLS.

Residential construction employment is clearly trending down, and is probably about to fall "off the cliff". But look at nonresidential construction employment: it is too early to say for sure, but it appears employment might have peaked. Construction spending shows a similar pattern. Private residential construction spending peaked in December 2005, and it appears all other construction spending (public and private nonresidential) might have peaked in August. Source: Census Bureau.

Construction spending shows a similar pattern. Private residential construction spending peaked in December 2005, and it appears all other construction spending (public and private nonresidential) might have peaked in August. Source: Census Bureau.

It is early, and these small changes might be normal monthly noise, but since the historical pattern suggests nonresidential construction will probably start declining soon, this might be the first evidence that nonresidential construction has peaked.

DataQuick: Bay Area home prices decline, sales at five-year low

by Calculated Risk on 12/14/2006 01:22:00 PM

DataQuick reports: Bay Area home prices decline, sales at five-year low

Bay Area home prices dipped below year-ago levels in November for the second time in three months as sales held steady at a five-year low, a real estate information service reported.Update: chart added.

The median price paid for a home in the nine-county Bay Area was $616,000 in November. That was 0.3 percent higher than $614,000 in October but down 1.4 percent from $625,000 in November last year, according to DataQuick Information Systems.

Last month's year-over-year decline was the steepest since prices fell 2.1 percent in February 2002.

| Bay Area California Median Home Prices | ||||

| Area | Nov '04 | Nov '05 | Nov '06 | Pct Change |

| Alameda | $500K | $587K | $581K | -1.0% |

| Contra Costa | $474K | $589K | $562K | -4.6% |

| Marin | $739K | $809K | $841K | 4.0% |

| Napa | $535K | $605K | $596K | -1.5% |

| San Francisco | $697K | $749K | $754K | 0.7% |

| San Mateo | $664K | $733K | $726K | -1.0% |

| Santa Clara | $560K | $653K | $665K | 1.8% |

| Solano | $400K | $490K | $446K | -9.0% |

| Sonoma | $472K | $574K | $530K | -7.7% |

| Bay Area | $533K | $625K | $616K | -1.4% |

I added the November 2004 median prices to give a two year perspective on prices.

A total of 7,204 new and resale houses and condos sold in the Bay Area last month. That was down 9.7 percent from 7,979 sales in October, and down 25.9 percent from 9,717 in November last year. A decline from October to November is normal for the season.

Last month's sales count was the lowest for any November since 2001, when 6,644 homes sold. Since 1988, November sales have ranged from 5,579 in 1994 to 10,897 in 2004.

| Bay Area California Homes Sold | ||||

| Area | Nov '04 | Nov '05 | Nov '06 | Pct Change |

| Alameda | 2,251 | 2,009 | 1,441 | -28.3% |

| Contra Costa | 2,179 | 1,961 | 1,406 | -28.3% |

| Marin | 413 | 361 | 268 | -25.8% |

| Napa | 221 | 183 | 125 | -31.7% |

| San Francisco | 616 | 594 | 441 | -25.8% |

| San Mateo | 920 | 756 | 581 | -23.1% |

| Santa Clara | 2,624 | 2,394 | 1,846 | -22.9% |

| Solano | 918 | 774 | 565 | -27.0% |

| Sonoma | 755 | 685 | 531 | -22.5% |

| Bay Area | 10,897 | 9,717 | 7,204 | -25.9% |

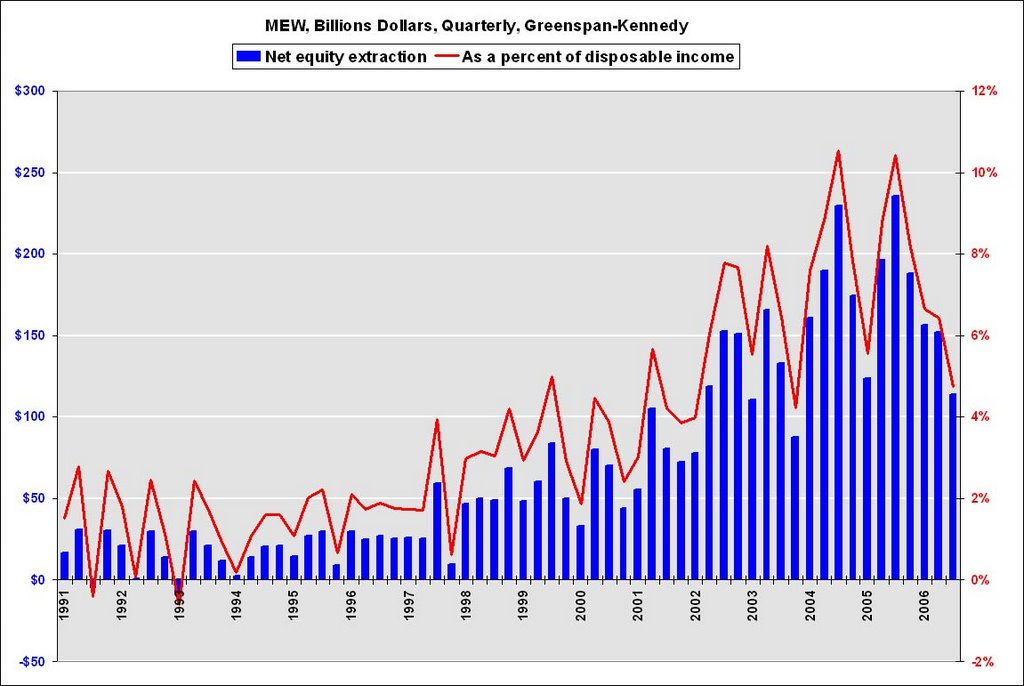

Greenspan-Kennedy MEW Graph

by Calculated Risk on 12/14/2006 12:20:00 PM

Click on graph for larger image.

Click on graph for larger image.

Here is a graph of the Greenspan-Kennedy MEW results, both in billions of dollars quarterly (not annual rate), and as a percent of personal disposable income.

In Memoriam: Doris "Tanta" Dungey

| Privacy Policy |

| Copyright © 2007 - 2025 CR4RE LLC |

| Excerpts NOT allowed on x.com |