RSS Feed

RSS Feed by Calculated Risk on 12/27/2006 12:07:00 PM

Wednesday, December 27, 2006

More on November New Home Sales

Please see the previous post: November New Home Sales Click on graph for larger image.

Click on graph for larger image.

One of the most reliable economic leading indicators is New Home Sales.

New Home sales were falling prior to every recession of the last 35 years, with the exception of the business investment led recession of 2001. This should raise concerns about a possible consumer led recession in the months ahead.

Some more optimistic observers will argue that sales have fallen back to a sustainable level after the excesses of 2004 and 2005. Others will argue that sales have to fall more in coming years, to make up for the excesses of recent years. That is one of the reasons 2007 will be such an interesting year.

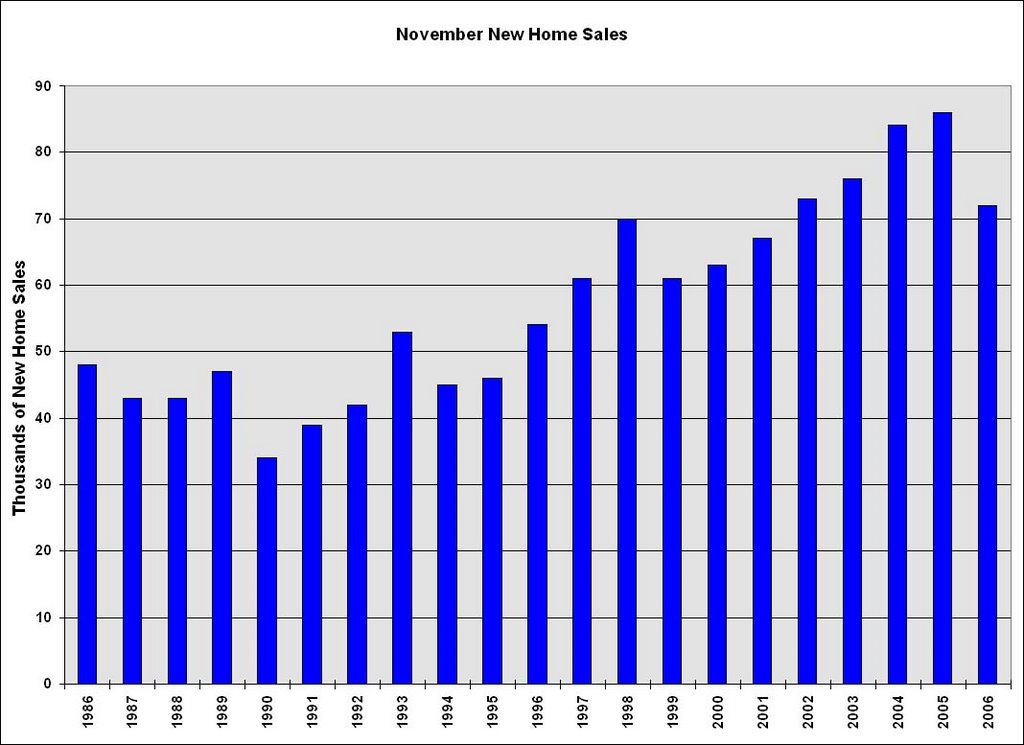

The second graph shows November New Home sales for the last 20 years. The recent sharp drop in sales is similar to the decrease at the start of the 1990s housing bust.

Also note that November sales have fallen below the 2002 levels.

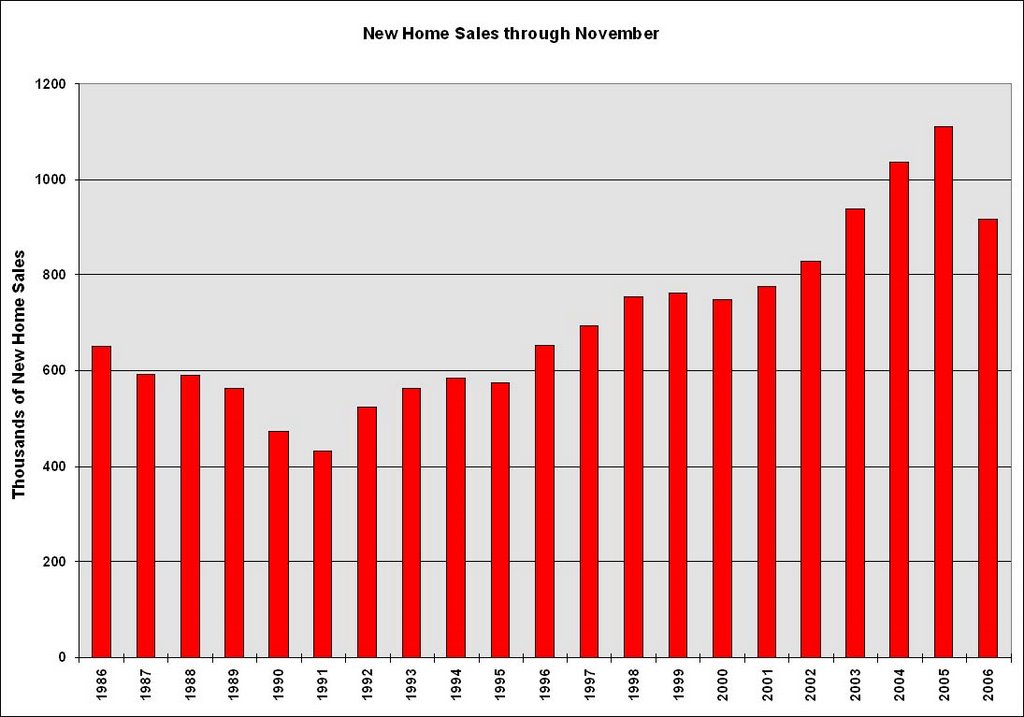

The third graph shows YTD New Home sales through November. It now appears that 2006 will finish as the 4th best year behind 2003.

Sales for the most recent months have fallen to the 2002 level. Fannie Mae is currently estimating that sales for 2007 and 2008 will be at the 2002 level (about 975K units). I think sales will fall further, perhaps to the level of the 1998 through 2001 period, or about 900K units in 2007.

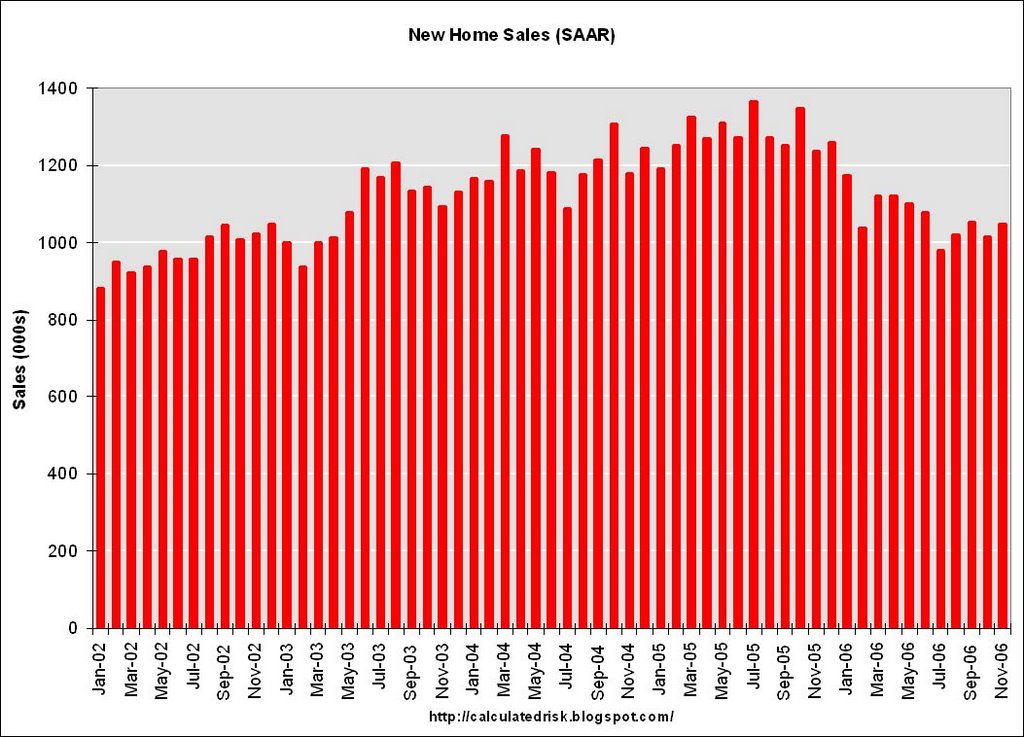

November New Home Sales: 1.047 Million SAAR

by Calculated Risk on 12/27/2006 10:24:00 AM

According to the Census Bureau report, New Home Sales in November were at a seasonally adjusted annual rate of 1.047 million. Sales for October were revised up to 1.013 million, from 1.004 million. Numbers for August and September were also revised up slightly too.

Click on Graph for larger image.

Sales of new one-family houses in November 2006 were at a seasonally adjusted annual rate of 1,047,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 3.4 percent above the revised October rate of 1,013,000, but is 15.3 percent below the November 2005 estimate of 1,236,000.

The Not Seasonally Adjusted monthly rate was 72,000 New Homes sold. There were 86,000 New Homes sold in November 2005.

On a year over year NSA basis, November 2006 sales were 16.3% lower than November 2005. Also, November '06 sales were below November 2004 (84,000) and November 2003 (76,000) sales.

This is the lowest November since 2001 when 67,000 new homes were sold.

The median and average sales prices were mixed. Caution should be used when analyzing monthly price changes since prices are heavily revised.

The median sales price of new houses sold in November 2006 was $251,700; the average sales price was $294,900.

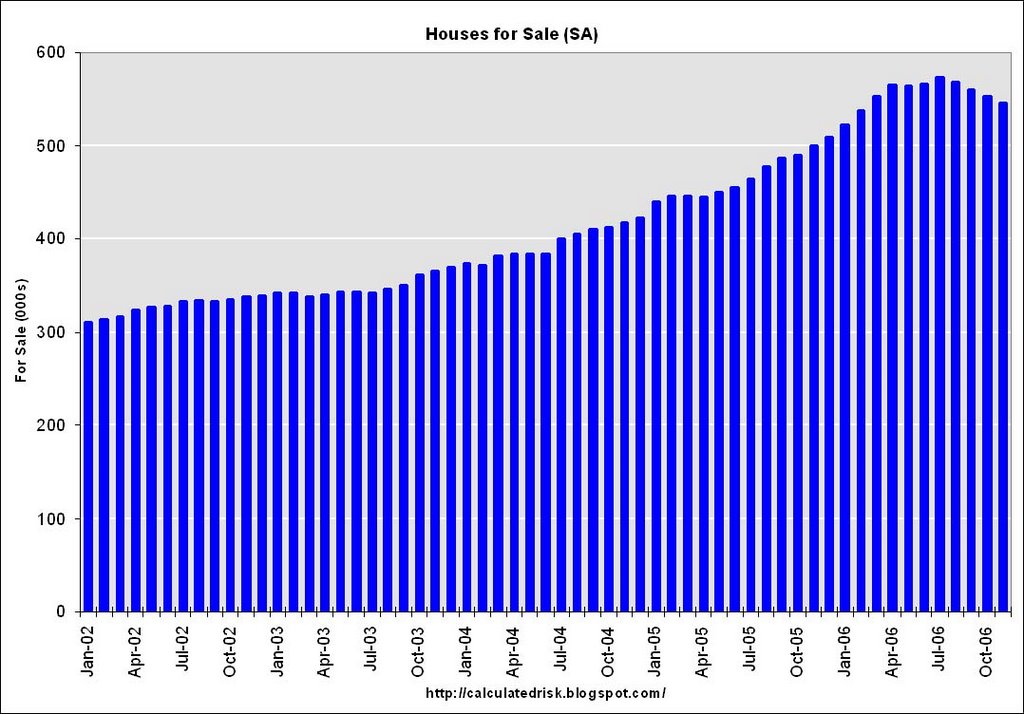

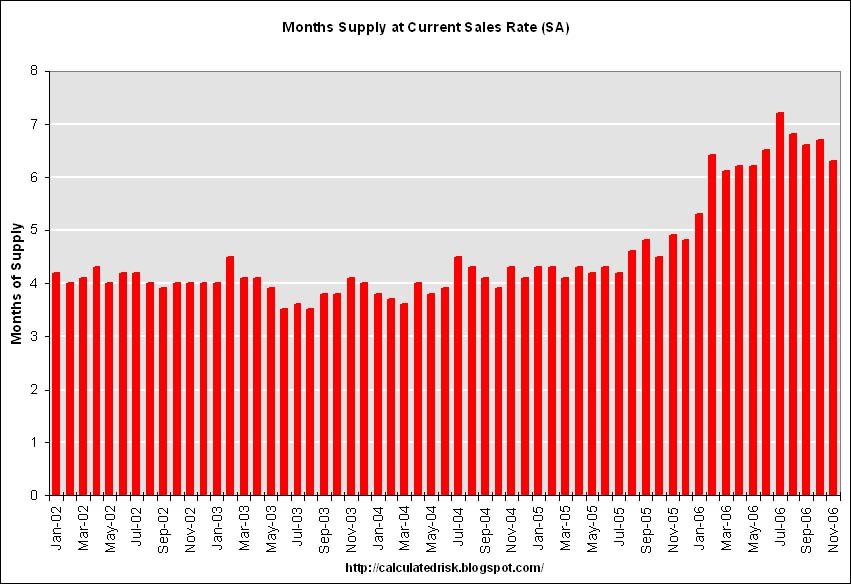

The seasonally adjusted estimate of new houses for sale at the end of November was 545,000.

The 545,000 units of inventory is slightly below the levels of the last six months. Inventory numbers from the Census Bureau do not include cancellations - and cancellations are at record levels. Actual New Home inventories are much higher - some estimate about 20% higher. This represents a supply of 6.3 months at the current sales rate.

This represents a supply of 6.3 months at the current sales rate.

On a months of supply basis, inventory is above the level of recent years.

More later today on New Home Sales.

Immigrant Worker: "There's no work here anymore."

by Calculated Risk on 12/27/2006 01:26:00 AM

From the WaPo: Immigrants' Jobs Vanish With Housing Slowdown

The gold rush came in drywall, laminate flooring and granite countertops ...The housing starts data suggests that 400K to 600K BLS reported jobs will be lost in residential construction over the next six months. But many more jobs will be lost by illegal immigrants working in construction. And the loss of these jobs matter too:

Then sometime last year ... the rush began to go bust, little by little, month by month. The contractors stopped hiring. The phone stopped ringing. Washington, it seemed, had all the houses it could hold.

... On Jan. 20, he is taking his family back to El Salvador, with plans to open an auto repair shop with the money he has saved. "There's no work here anymore,"

...

"A slowdown in the construction industry hits illegals much harder than the rest of the general population," [said Steven A. Camarota, research director of the Center for Immigration Studies.]

The effects of the slowdown are also rippling through Hispanic-owned businesses. "A lot of my customers have gone to Florida, to the Carolinas," said Carlos Castro, owner of the Todos Supermarket chain and chairman of the Hispanic Business Council in Prince William County.

Sales are down slightly at Castro's stores, but he said some of his suppliers are experiencing 30 to 40 percent decreases in local orders, with smaller, less-established businesses taking the biggest hit.

MBA: Mortgage Applications Decrease

by Calculated Risk on 12/27/2006 12:20:00 AM

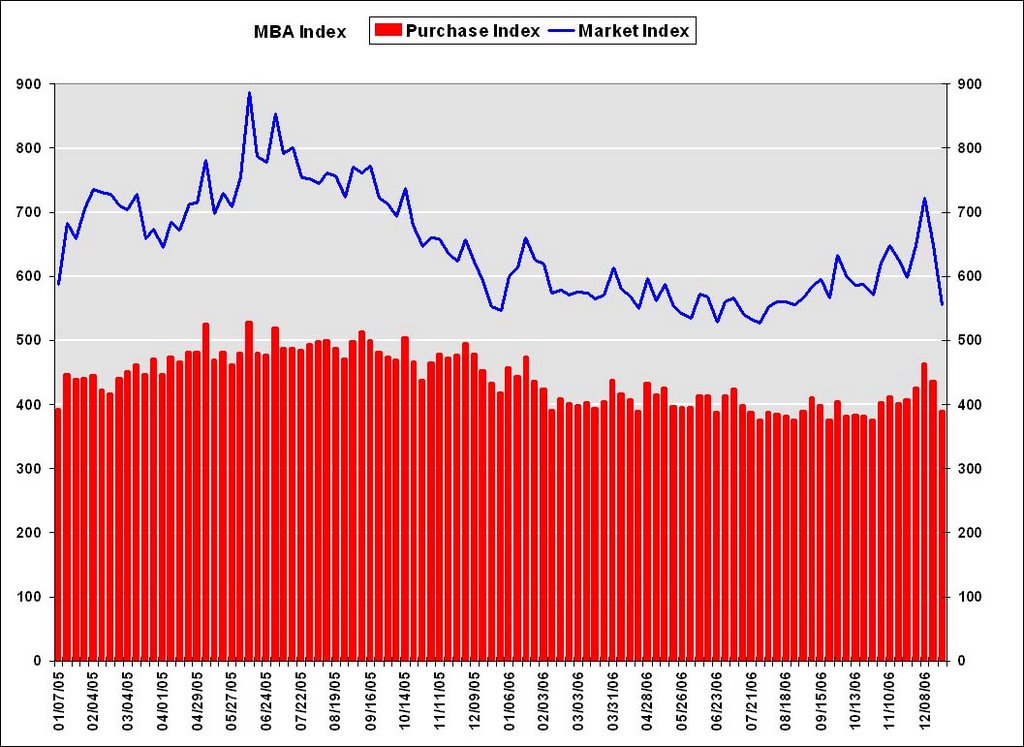

The Mortgage Bankers Association (MBA) reports: Mortgage Applications Decrease in Week before Christmas Click on graph for larger image.

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 555.8, a decrease of 14.2 percent on a seasonally adjusted basis from 647.6 one week earlier. On an unadjusted basis, the Index decreased 15 percent compared with the previous week and was up 16.6 percent compared with the same week one year earlier.Mortgage rates increased:

The Refinance Index decreased by 18.5 percent to 1604.6 from 1968.8 the previous week and the seasonally adjusted Purchase Index decreased by 10.6 percent to 390.2 from 436.5 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.12 from 6.10 percent ...

The average contract interest rate for one-year ARMs increased to 5.87 percent from 5.82 ...

The second graph shows the Purchase Index and the 4 and 12 week moving averages since January 2002. The four week moving average is down 1 percent to 429.3 from 433.4 for the Purchase Index.

The second graph shows the Purchase Index and the 4 and 12 week moving averages since January 2002. The four week moving average is down 1 percent to 429.3 from 433.4 for the Purchase Index.The refinance share of mortgage activity decreased to 48.8 percent of total applications from 50.8 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 23.1 from 23.6 percent of total applications from the previous week. The ARM share is at its lowest level since October 2003.

Tuesday, December 26, 2006

2007 Economic Growth: The Consensus View

by Calculated Risk on 12/26/2006 11:19:00 AM

From the USA Today: Growth or recession in 2007?

In a poll of 21 prominent economists conducted by the Securities Industry and Financial Markets Association (SIFMA), the respondents expected economic growth of a median 2.5% in 2007, down from 3.3% in 2006.So the consensus view for 2007 is just below trend growth. See the USA today article for quotes from various forecasters.

But the difference of opinion is big. In the survey by SIFMA, the estimates for gross domestic product growth ranged from 1.6% to 2.9%.

Monday, December 25, 2006

The "anti-Goldilocks economy"

by Calculated Risk on 12/25/2006 11:58:00 PM

From the NY Times: An Economy of Extremes

Economists have long waxed lyrical about a “Goldilocks economy”— one that is not too hot, not too cold.Too hot and too cold - definitely not "just right". The NY Times presents several differing views on the impact of the housing bust on the general economy. However ...

...

The “just right” economy is not often achieved, of course, but lately this bedtime story has taken a particularly tricky turn: it is both too hot and too cold.

...

Lombard Street Research, a British economic forecasting firm, recently dubbed the American economy the “anti-Goldilocks economy.”

There is one crucial weakness to all the forecasts ... Part way through the bust of perhaps the strongest housing boom on record ... Nobody has ever seen how a situation like this unwinds ...there are enough uncertainties to warrant talk of a recession.Even Fannie Mae is upping the probabilities of a recession:

...

“If housing is as unhelpful on the way down as it was helpful on the way up, we will get a recession,” Mr. [Allen Sinai, president and chief global economist at Decision Economics] said.

“We’ve increased the probability of a recession in our forecast to 35 percent,” said David W. Berson, chief economist of Fannie Mae.

Sunday, December 24, 2006

Happy Holidays!

by Calculated Risk on 12/24/2006 12:22:00 AM

Out through the fields and the woodsLove greatly. Enjoy the season!

And over the walls I have wended;

I have climbed the hills of view

And looked at the world, and descended;

I have come by the highway home,

And lo, it is ended.

The leaves are all dead on the ground,

Save those that the oak is keeping

To ravel them one by one

And let them go scraping and creeping

Out over the crusted snow,

When others are sleeping.

And the dead leaves lie huddled and still,

No longer blown hither and thither;

The last lone aster is gone;

The flowers of the witch-hazel wither;

The heart is still aching to seek,

But the feet question ‘Whither?’

Ah, when to the heart of man

Was it ever less than a treason

To go with the drift of things,

To yield with a grace to reason,

And bow and accept the end

Of a love or a season?

Reluctance by Robert Frost From A Boy's Will, 1913.

Saturday, December 23, 2006

O.C. Register: Lender on Orange County Housing

by Calculated Risk on 12/23/2006 06:11:00 PM

From Lansner on Real Estate in the OC Register: Lender Norris eyeballs O.C. housing '07

We'll start with lender/investor Bruce Norris of The Norris Group. He's followed Southern California real estate for seemingly ever. He deftly called the beginning of the turn-of-the-century housing rally but now he has turned bearish. Let's see what he's thinking ...Excerpts:

Us: What's your outlook for the local housing market for 2007?

Bruce: Orange County prices down 5 percent.

...

Us: What might be the housing surprise we'll be talking about a year from now?

Bruce: The greatest year-over-price year decline since the Great Depression, nationally.

Friday, December 22, 2006

Year End Predictions

by Calculated Risk on 12/22/2006 06:07:00 PM

Last year I tried to predict the top economic stories of 2006. I intentionally went "out on a limb", and I definitely missed a few. I'll be doing it again this year. Recession or no recession? I guess I'll have to make a call next week!

But first, a quick review - here are some stories that I thought would not be big in '06:

Energy Prices: I expect oil prices to stabilize or decline next year. WTI spot prices closed at $59.96 today.

I missed this one big time. WTI spot prices are $62+ today - that doesn't seem too far off, but I completely missed the huge price increase in the middle of '06.

Bush Economic proposals: I think the Bush Administration will be shackled by scandals and Iraq, so I don't expect any major new proposals. I hope I'm wrong about Iraq.

Got that one right. I wish I was wrong about Iraq.

Trade Deficit / Current Account Deficit: I could be wildly wrong here too, but I think the trade deficit will stabilize or even decline slightly next year. Note: I clarified this one - I expected the deficit to stabilize at the Q4 level - clearly the deficit was going to increase in '06.

Looks pretty good. The trade deficit appears to have stabilized at about the level of Q4 2005. However, the current account deficit is still climbing.

The Budget Deficit: Although I expect the General Fund deficit to grow to around $600 Billion in 2006, I don't think it will become a huge story until '07 or '08.

This was more of a story than I expected, mainly because the General Fund deficit declined to $434 Billion from $470 Billion in fiscal 2005. I still think the huge story will be in the coming years.

And here are the stories I thought would be big in '06:

5) The End of the Greenspan Era I think Dr. Bernanke will face a significant challenge in '06, perhaps by one the following top stories - perhaps by something completely unexpected. Stephen Roach recently wrote:

"Alan Greenspan faced a stock-market crash two months after he took over in August 1987. Paul Volcker had to cope with a rout in the bond market three months after he became chairman in August 1979. G. William Miller was challenged immediately by a dollar crisis in the spring of 1978. For Arthur Burns, it was the inflation bogie in the early 1970s."Missed that one: Bernanke had a crisis free year.

4) Housing Slowdown In my opinion, the Housing Bubble was the top economic story of 2005, but I expect the slowdown to be a form of Chinese water torture. Sales for both existing and new homes will probably fall next year from the records set in 2005. And median prices will probably increase slightly, with declines in the more "heated markets".

Pretty close.

3) Pension Blowup / Major Bankruptcy Of course I am thinking GM, but maybe it will be another major corporation.

Another complete whiff.

2) Slowing Economy If the US and the World economies slide into recession, this will be the top story next year. I still think it is too early to call, but I do think economic growth will slow substantially next year.

Slow? Yes. Slow substantially? We will need to see the Q4 GDP numbers - right now I think Q4 GDP will be around 2%.

1) Interest Rates ... like many observers, I expect the Fed to start lowering rates later next year as the economy slows. But here is the surprise, I think long rates will start to rise when the Fed starts cutting the Fed Funds rate.

I clearly missed the timing of the rate cut, but this prediction was that long rates would rise as the Fed cut rates. We will have to wait to see if that happens.

Here is how the AP ranked the top 2006 stories.

Fed: Mortgage Obligation Ratio at Record Levels in Q3

by Calculated Risk on 12/22/2006 02:45:00 PM

The Federal Reserve released the "Household Debt Service and Financial Obligations Ratios" for Q3 2006 today.

DEFINITIONS: The household debt service ratio (DSR) is an estimate of the ratio of debt payments to disposable personal income. Debt payments consist of the estimated required payments on outstanding mortgage and consumer debt.The owner FOR (Financial Obligation Ratio) was 18.16% in Q3 '06, off slightly from the revised 18.17% for Q2 '06 (Q2 was originally reported at 18.06%)

The financial obligations ratio (FOR) adds automobile lease payments, rental payments on tenant-occupied property, homeowners' insurance, and property tax payments to the debt service ratio.

The mortgage portion of the FOR set a new record at 11.68%, up slightly from 11.65% in Q2 '06. (Q2 was originally 11.60%)

The household DSR (Debt Service ratio) was off slightly at 14.49%, from 14.51% in Q2 '06. (Q2 was originally 14.40%)

Note: All of the estimates for Q2 were revised upwards, otherwise these would have been new records across the board.

Click on graph for larger image.

Click on graph for larger image.With relatively low mortgage rates, one might expect the mortgage portion of the FOR to be lower than previous periods, not at record high levels.

Note that the previous housing bubble peaked with the mortgage portion of the FOR at 10.38%.