RSS Feed

RSS Feed by Calculated Risk on 12/07/2007 08:30:00 AM

Friday, December 07, 2007

November Employment Report

From MarketWatch: Payrolls up 94,000; jobless rate stays at 4.7% on household survey gains

The economy added 94,000 nonfarm payroll jobs last month, according to a survey of business establishments, the Labor Department said in a mixed report released Friday.

...

Goods-producing industries cut 33,000 jobs in November, including 24,000 in construction and 11,000 in manufacturing.

Services-producing industries added 127,000 jobs. Financial services cut 20,000 jobs.

Thursday, December 06, 2007

From AAA to Worthless in Less than a Year

by Calculated Risk on 12/06/2007 11:19:00 PM

Note: If you are looking for a discussion of the Mortgage Freeze plan, see Tanta's The Plan: My Initial Reaction

First, here is a great graphical explanation of a CDO from Felix Salmon at Portfolio.com: What's a C.D.O.?

Now back to the Adams Square Funding liquidation. Thanks to jck for sending me the prospectus for the deal. Here are the notes:

U.S.$48,000,000 CLASS A SENIOR FLOATING RATE NOTES DUE DECEMBER 2051And here were the initial ratings:

U.S.$51,000,000 CLASS B-1 SENIOR FLOATING RATE NOTES DUE DECEMBER 2051

U.S.$10,000,000 CLASS B-2 SENIOR FLOATING RATE NOTES DUE DECEMBER 2051

U.S.$15,250,000 CLASS C FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$16,000,000 CLASS D FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$5,000,000 CLASS E FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$20,000,000 SUBORDINATED NOTES DUE DECEMBER 2051

Adams Square Funding I, Ltd. (the “Issuer”) will issue the Notes referenced above on or about December 15, 2006 ...

It is a condition of the issuance of the Notes on the Closing Date that (a) the Class A Notes be rated “Aaa” by Moody’s Investors Service, Inc. (“Moody’s”) and “AAA” by Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. (“S&P”), respectively, (b) the Class B-1 Notes be rated at least “Aa2” and “AA” by Moody’s and S&P, respectively, (c) the Class B-2 Notes be rated at least “Aa3” and “AA-” by Moody’s and S&P, respectively, (d) the Class C Notes be rated at least “A2” and “A” by Moody’s and S&P, respectively, (e) the Class D Notes be rated at least “Baa2” and “BBB” by Moody’s and S&P, respectively, and (f) the Class E Notes be rated at least “Ba1” and “BB+” by Moody’s and S&P, respectively. The Subordinated Notes will not be rated.All of the above notes are worthless, including the AAA rated (by S&P) Class A notes.

Even the $342 million in Super Senior notes were impaired. As S&P noted yesterday: "proceeds will not be sufficient to cover the funded portion of the super-senior swap in full and that no proceeds will be available for distribution to the class A, B, C, D, or E notes."

From AAA to worthless in less than a year.

Rabobank bails out SIV, "model is dead"

by Calculated Risk on 12/06/2007 10:23:00 PM

From the Financial Times: Rabobank bails out SIV

Rabobank on Thursday ... bail[ed] out a troubled structured investment vehicle ... The Dutch bank plans to take assets worth €5.2bn ($7.6bn) on to its balance sheet to prevent a fire sale of Tango Finance.Memo to Paulson and Citigroup: SIVs are dead.

The bank, which manages the SIV with Citigroup, has already sold almost half the vehicle’s assets because it could not find sufficient funding. ...

Eddie Villiers, responsible for European sales at Rabobank, said: "The current SIV business model is dead and so there is no prospect of its survival in its current form."

“Our decision has been made purely for liquidity reasons as the assets in the portfolio are of high quality, but there is no market for asset-backed commercial paper for SIVs. We have done this for reputational reasons as our exposure to the SIV is small,” Mr Villiers said.

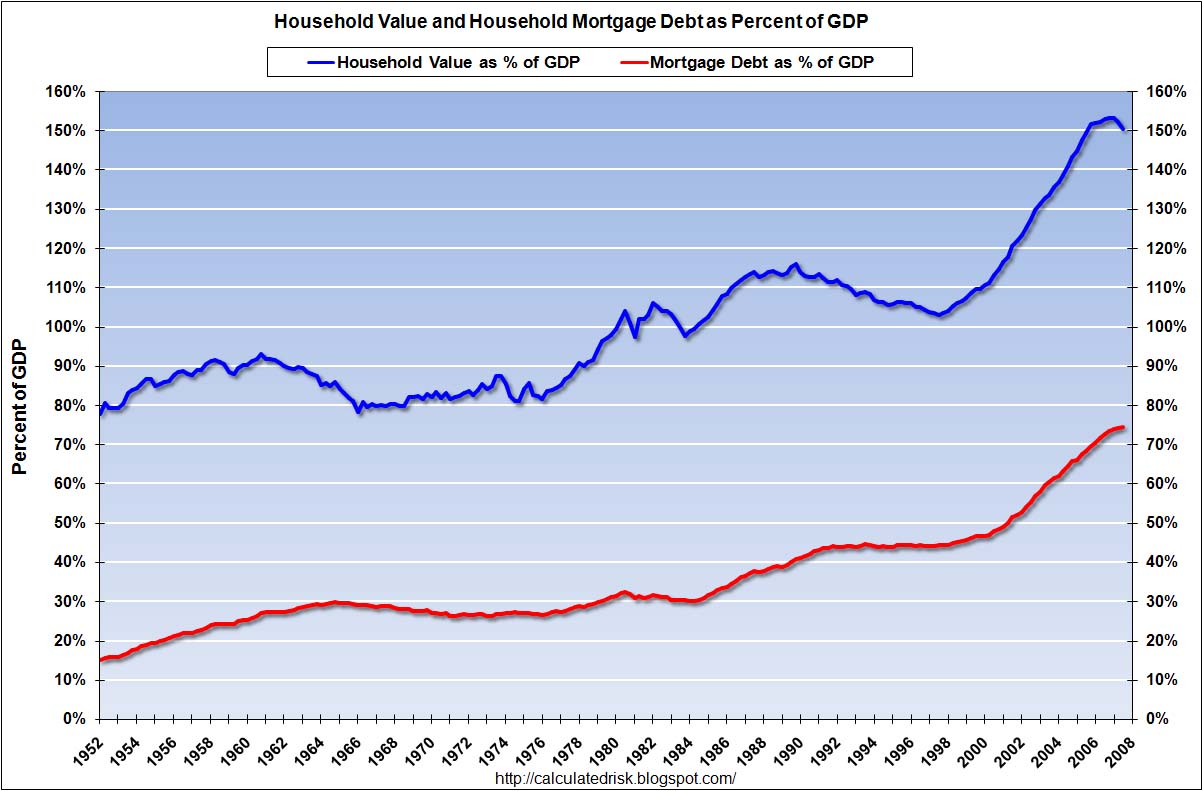

Fed: Existing Household Real Estate Assets Decline $67 Billion in Q3

by Calculated Risk on 12/06/2007 07:16:00 PM

Here is some more data from the Fed's Flow of Funds report.

The Fed report shows that household real estate assets increased from $20.94 Trillion in Q2 to $20.99 Trillion in Q3. However, when we subtract out new single family structure investment and residential improvement, the value of existing household real estate assets declined by $67 Billion.

The simple math: Increase in household assets: $20,991.18 Billion minus $20,937.62 Billion equals $53.56 Billion. Now subtract investment in new single family structures ($297.2 Billion Seasonally Adjusted Annual Rate) and improvements ($185.8 Billion SAAR). Note: to make it simple, divide the SAAR by 4.

Finally $53.56B minus $297.2B/4 minus $185.8B/4 equals a decline in existing assets of $67.2B. This was a quarterly price decline of about 0.3%, about the same as the OFHEO House Price index decline.

As mentioned earlier, household equity declined by $128 Billion in Q3.

Household debt increased by $182.1 Billion in Q3 (down from $213.6B in Q2, and up slightly from $181.48B in Q1 2007). The mortgage equity withdrawal numbers will probably still be fairly strong in Q3.

Household percent equity was at an all time low of 50.4%.

This graph shows homeowner percent equity since 1954. Even though prices have risen dramatically in recent years, the percent homeowner equity has fallen significantly (because of mortgage equity extraction 'MEW'). With prices now falling - and expected to continue to fall - the percent homeowner equity will probably decline rapidly in the coming quarters.

Also note that this percent equity includes all homeowners. Based on the methodology in this post, aggregate percent equity for households with a mortgage has fallen to 33% from 36% at the end of 2006.

If Goldman Sachs and Moody's are correct and house prices fall 15% nationally (30% in some areas), the value of existing household real estate assets will fall by $3 Trillion over the next few years.

You Can't Make Stuff Like This Up

by Anonymous on 12/06/2007 06:55:00 PM

From CNN:

WASHINGTON (CNN) — Harried homeowners seeking mortgage relief from a new Bush administration hotline Thursday had to contend with a bit of temporary misdirection from the president himself.

As he announced his plan to ease the mortgage crisis for consumers, President Bush accidentally gave out the wrong phone number for the new “Hope Now Hotline” set up by his administration.

Anyone who dialed 1-800-995-HOPE did not reach the mortgage hotline but instead contacted the Freedom Christian Academy — a Texas-based group that provides Christian education home schooling material.

The White House press office quickly put out a correction moments after the President’s remarks. After dialing the correct number, 1-888-995-HOPE, CNN was connected to a “counselor” within three minutes.

The Plan: My Initial Reaction

by Anonymous on 12/06/2007 04:20:00 PM

A lot of people are very worked up over the idea that the New Hope Plan is, in essence, the government mandating a kind of reneging on private contracts (the PSAs or Pooling and Servicing Agreements that govern how securitized loans are handled). I personally think you can all stand down on that one. From what I have seen about the plan to date, it is clear to me that it is in fact structured with the overarching goal of making sure that it stays on the allowable side of the existing contracts. I proceed from the assumption that nobody could write such a convoluted and counter-intuitive plan if that wasn’t the goal. So everyone who is thinking, “Gee, we’re violating contracts and we still don’t get much out of it!” is thinking the wrong thing, in my view. It’s more like “Gee, we don’t get much out of it when we don’t violate contracts.”

American Banker has a summary of The Plan details up here (it’s free this week if you register, and the registration process is painless). The basic outline is that loans are put into three segments:

1. Borrower appears (from fairly superficial analysis of the data, not any deep digging) to be eligible for a refinance. These borrowers are to be encouraged to refinance.

2. Borrower appears able to make payment at current rate, but appears (again, from fairly superficial analysis) to be unlikely to be able to refinance (generally because LTV is too high with FICO too low). These borrowers are eligible for the “fast-tracked” mod (the rate freeze) if they meet some FICO and payment increase tests.

3. Borrower appears unable to make payment even at current rate; these borrowers are presumed to be unable to refinance. They are not eligible for the “fast track” rate freeze mod; they may be eligible for some kind of work out, but it would have to be handled the old-fashioned fully-analyzed case-by-case way.

There’s some detail about the FICO and payment tests used in segment 2.

I’m guessing that structuring of things will strike folks as weird. To me, it says that a rule of thumb is being created that puts borrowers in three categories:

1. Not in default and default not imminent

2. Not in default and default reasonably foreseeable

3. In default or default imminent

As it happens, the PSAs for these deals will nearly universally contain language that says loans can only be modified if they are in default, or default is imminent, or default is reasonably foreseeable. Therefore, what The Plan does is simply provide a kind of standard definition of those categories for the vintages of loans in question. That’s why the Group 1 borrowers—those who could be eligible for a refinance—are never eligible for these “fast track” mods. It is hard to say that default (in the current pool) is reasonably foreseeable for a loan that has a refinance opportunity. No, it doesn’t make any difference that the refinanced loan might be highly likely to default at some fairly soon point in some new pool. This isn’t about solving the borrower’s problems permanently in the best possible way (a mod might be a better permanent solution than a refi for the borrower). It’s about solving the problem while staying inside the security rules.

And the rules in question are really important ones, not just idiosyncratic servicing rules that could probably be waived in a crisis by the trustee with the consent of the rating agencies.

First, REMICs (go here if you have no idea what a REMIC is). REMIC election involves the tax treatment of principal and interest payments and is much too complex to summarize here. The basic issue is that it creates a trust that owns the underlying pool of loans. The trust issues two classes of securities, regular interests and a residual interest. Interest income is taxable (as ordinary income) to the holders of regular interests. Gain/loss for tax purposes is also taken by the residual holder. The trust itself is not taxed; it’s just a pass-through entity. That prevents a “double taxation” from arising, in which the trust would have to pay taxes on interest income and then the regular class holders would also pay taxes.

One of the qualifying requirements of REMIC status is that the underlying pool of loans is “fixed.” REMICs do not acquire new loans after their pools are established; they do not account for any loans on a “held for sale” basis and they do not sell any loans. (Putbacks for breach are an exception, and always transact at par, not at market value.) If at any time the trust starts taking actions that can be interpreted as “actively managing” the underlying pool, the REMIC status is in jeopardy (the trust might have to start paying taxes, which would make the whole deal uneconomical).

So while the legislation and IRS rules authorizing and dealing with REMICs are not really about defining default servicing practices, they have affected default servicing practices (loss mitigation) because they have defined a kind of transaction that might look like active management of the pool but really isn’t: modifications (or other workouts) for defaulted or about-to-default loans. In essence, the REMIC law creates an exception for these loss-mit practices, so that servicers can use them without endangering the REMIC status of the trust. This is how what might seem like unrelated issues—how to best service a mortgage loan, how trust entities are or are not taxed by the IRS—get related.

The issue is further complicated by the off-balance-sheet nature of these trusts. (They don’t have to be off-balance sheet, but most of them are.) To be accounted for off the issuer’s balance sheet, the trust must be “qualifying” under the SFAS 140 rules. The “Q status” is similar to the REMIC status: the pool must be “static” or fixed or not actively managed or, in the charming industry parlance, “brain dead.” If it is determined that a pool is being actively managed, it “loses its Q” and gets forced onto the issuer’s balance sheet. SFAS 140, like the tax code, isn’t designed to be about good mortgage servicing practices, but it, like the tax code, has to include some definitions of acceptable “managing” of individual loans that are exceptions to the “brain dead pool” rule.

There was a bit of a dust-up earlier this year over the SFAS 140 issue. In a nutshell, while the REMIC law says that modifications are OK when the loan is in default or default is reasonably foreseeable, there was some concern that SFAS 140 only allows modifications if the loan is in default. That would mean that if you modified a loan that was current today, but that you had reason to believe would default next month (say, at reset) if you didn’t do anything about it, you’d be OK with your REMIC status but not OK with your Q status. The waters were calmed when the SEC published an official opinion that “reasonably foreseeable default” was an acceptable basis for modifying a loan under SFAS 140 as well as IRS 860D.

The takeaway point: a great deal of more-or-less informed commentary and blather you will find on whether securitizations “allow” modifications is based not on a question of what verbiage is or is not in the PSA, but rather on an interpretation of what is or is not required for REMIC tax treatment or off-balance sheet accounting. All the PSAs say, somewhere, that servicers will not do things that would jeopardize REMIC status or Q election. The whole point of the letter opinion released by the SEC this summer was to create a kind of regulatory “safe harbor” here: it said that if servicers use the “reasonably foreseeable default” standard that they are already allowed to use for REMIC-status purposes, they are OK with Q-status.

This “safe harbor” for Q-status did not and does not “override” any explicit contractual limitations on modifications that might be in any given PSA. In other words, if the PSA says explicitly that mods are allowed only for loans in default, but not for loans that are current (but likely to default), then that’s the standard. If a servicer went ahead and modified a current loan (under the “reasonably foreseeable” standard), then the servicer could be in breach of the PSA contract, even though the servicer is OK on the REMIC status and Q status. This raises the interesting question of whether there are actually any PSAs that so explicitly forbid this kind of modification, and if so, how many; that’s our next subject. But I know of no informed, sane observer who is claiming that the SEC letter, for instance, was a form of government abrogating of existing contracts. It was simply a case of a regulator ruling that if the PSA allows a certain class of modifications (implicitly or explicitly), the servicer’s exercise of the option to pursue those mods would not create an accounting nightmare. You may, if you like, interpret that as a regulator removing an obstacle to the enforcement of contracts as written.

So what do the PSAs say?

This is a hard question to answer definitively, because the PSAs for mortgage-related securitizations have not been forced to be uniform on this (or about 100 other) subjects. It is possible that some verbiage related to loss mit and modifications differs between contracts because someone somewhere really thought it was important; it is possible that some of it differs just because different law firms with different styles were used to draft the PSAs; it is possible that some of this is a matter of a lapse of attention somewhere. I think it never pays to underestimate the extent to which the industry does certain things because they did it that way back when they did their first securitization, and at no time since then has it ever become an issue, and nobody makes bonuses by making issues out of things that aren’t issues. Certain people have reacted to proposals for “safe harbor” legislation involving mortgage modifications by assuming, not necessarily wisely, that the contractual provisions in question are always and everywhere something that the parties to the contract have a real interest in defending or enforcing. The possibility that both servicers and investors are going back, reading these things, slapping themselves on the heads and saying, “Damn, why’d we put that in there?” is very real. Unfortunately, “investors” are so diverse and numerous and diffused that you just don’t get two parties sitting down and amicably agreeing to amend these PSAs to clear up a little problem.

So we get back to the apparently empirical question of what these PSAs actually do say. I have read many of them, but I sure haven’t read all of them. I am therefore willing to take the American Securitization Forum’s word for it here:

These agreements typically employ a general servicing practice standard. Typical provisions require the related servicer to follow accepted servicing practices and procedures as it would employ “in its good faith business judgment” and which are “normal and usual in its general mortgage servicing activities” and/or certain procedures that such servicer would employ for loans held for its own account.The ASF goes on to propose model contract language that it encourages the industry to adopt. This would go a long way to preventing this kind of chaos in the future. But even with existing documents, you will note that it appears that very few have explicit restrictions on modifications (aside from the “golden rule” standard of generally accepted servicing practices, with the expectation that the servicer will treat the pooled loans in the same way it would treat its own portfolio of loans). Those that do have explicit restrictions have mechanisms for those restrictions to be amended, in most cases by less than 100% concurrence of all investors.

Most subprime transactions authorize the servicer to modify loans that are either in default, or for which default is either imminent or reasonably foreseeable. Generally, permitted modifications include changing the interest rate on a prospective basis, forgiving principal, capitalizing arrearages, and extending the maturity date. The “reasonably foreseeable” default standard derives from and is permitted by the restrictions imposed by the REMIC sections of the Internal Revenue Code of 1986 (the “REMIC Code”) on modifying loans included in a securitization for which a REMIC election is made. Most market participants interpret the two standards of future default – imminent and reasonably foreseeable – to be substantially the same.

The modification provisions that govern loans that are in default or reasonably foreseeable default typically also require that the modifications be in the best interests of the securityholders or not materially adverse to the interests of the securityholders, and that the modifications not result in a violation of the REMIC status of the securitization trust.

In addition to the authority to modify the loan terms, most subprime pooling and servicing agreements and servicing agreements permit other loss mitigation techniques, including forbearance, repayment plans for arrearages and other deferments which do not reduce the total amount owing but extend the time for payment. In addition, these agreements typically permit loss mitigation through non-foreclosure alternatives to terminating a loan, such as short sales and short payoffs.

Beyond the general provisions described above, numerous variations exist with respect to loan modification provisions. Some agreement provisions are very broad and do not have any limitations or specific types of modifications mentioned. Other provisions specify certain types of permitted modifications and/or impose certain limitations or qualifications on the ability to modify loans. For example, some agreement provisions limit the frequency with which any given loan may be modified. In some cases, there is a minimum interest rate below which a loan's rate cannot be modified. Other agreement provisions may limit the total number of loans that may be modified to a specified percentage (typically, 5% where this provision is used) of the initial pool aggregate balance. For agreements that have this provision: i) in most cases the 5% cap can be waived if consent of the NIM insurer (or other credit enhancer) is obtained, ii) in a few cases the 5% cap can be waived with the consent of the rating agencies, and iii) in all other cases, in order to waive the 5% cap, consent of the rating agencies and/or investors would be required. It appears that these types of restrictions appear only in a minority of transactions. It does not appear that any securitization requires investor consent to a loan modification that is otherwise authorized under the operative documents.

So is all this uproar over contractual provisions just a tempest in a teapot? Well, some of it is. The issue around “safe harbor” and enforcement of contracts heated up once we moved from the proposition of doing mods the old-fashioned “case by case” way, and into this new idea of the “freeze” or a kind of across-the-board approach to modifications. It is that, specifically, that appears to some people to be a violation of contract provisions; therefore, to give servicers “safe harbor” for using the “freeze” approach would, it seems to many people, be a case of the government invalidating contracts.

Whether this is really a serious issue or not depends on how the “freeze” thing works out in detail. It seems likely to me that Sheila Bair’s original proposal for the “across the board” freeze of all ARM rates would, in fact, have run into this very serious problem. It’s not that in that case the number of modifications would exceed the set caps in the contracts; it would clearly do so for those contracts with caps, but as we’ve seen those caps can be waived or amended in most cases. The problem with the Bair proposal is that it doesn’t measure each modification against the standard of benefit to or neutral effect on the trust, and that loans that are probably not in any reasonably foreseeable danger of default would get included. That would cause the REMIC and Q status problems to come back into play.

The Hope Now proposal is intended to be an improvement on the Bair proposal by limiting the “freeze” precisely to the “in reasonably foreseeable danger of default” category. That solves the REMIC and Q-related problems. The difficulty that remains is whether, in any given case, the default that is in foreseeable danger of happening would cost more to the security than the modification. That is where the rubber meets the road.

That’s the rationale for excluding loans that could qualify for a refinance. The presumption is always that the trust would lose less by a refinance (since it would get paid off at par) than a mod, and so you can’t say that modifying one of these loans shows a net benefit to the trust. The rationale for defining the modification-eligible group, number 2, as “not refinanceable” is that that creates a presumption that a mod would be a net benefit or neutral to the trust (since the only other option, given that we believe default is reasonably foreseeable, is foreclosure).

So it’s not that we’re necessarily replacing the old-fashioned case-by-case mods with the fast-track “freeze” mods. We’re creating a way of segmenting the borrower class so that one class of borrowers can be presumed to meet all the requirements in the PSAs for modifications. If the borrower isn’t in that group (2), then a modification could still be done, but it doesn’t have the presumption of meeting the rules, you still have to determine whether a mod is less loss to the trust than not modifying (and therefore letting the loan default and foreclosing), you have to examine the borrower’s circumstances (to make sure that they are no longer in reasonably foreseeable danger of default after the mod), get a new appraisal or AVM or broker price opinion on the property (to estimate losses in event of foreclosure), and run the comparative numbers.

At the end of it, then, it gets a lot easier to figure out the rationale of some of the details of the Group 2 process (FICOs here or there, income verified or not, etc.). None of that is about figuring out whether the borrower "needs" or "deserves" to be helped. It is about figuring out whether the borrower has any realistic option of refinancing, given current contraints in the mortgage market and the HPA outlook. That, in turn, is crucial because to modify a loan that could have refinanced opens up the servicer to liability for contract violations (and potentially loss of REMIC tax status and Q-status, too).

There isn't, as far as I can see, any "safe harbor" provision in all of this. That tells me, at this point, that the authors of this plan believe it is liability-proof (that it basically meets the requirements of the existing PSAs, with the caveat that it isn't a legally binding mandate on all servicers and securities, so a deal with a very restrictive PSA that this isn't compatible with can just opt out).

Is it all kind of anemic after all the build-up? Yep. Does it mean contracts are now invalidated in the U.S.? Not as far as I can see; in fact, I'd say the contracts were the part of this that got the most thorough protection. In my reading of this, giving a deal to a borrower almost seems incidental.

MBA Mortgage Delinquency Graph

by Calculated Risk on 12/06/2007 02:21:00 PM

While we patiently wait for Tanta's analysis of the Freeze, here is a graph of the MBA mortgage delinquency rate since 1979 (hat tip Bill). Click on graph for larger image.

Click on graph for larger image.

This is the overall delinquency rate, and it is at the highest rates since 1986. As noted earlier this morning, delinquencies are getting worse in every category - including prime fixed rate mortgages - and getting worse at a faster rate in every category.

It seems like a long time ago, but it was in July of this year that Bernanke presented a report to Congress arguing that the subprime problems would stay in subprime, and that the problems were contained to variable rate subprime loans (see this post). Bernanke couldn't have been more wrong.

About Mod Re-Defaults

by Anonymous on 12/06/2007 01:39:00 PM

While we're all eagerly crowding around the teevee waiting for the Great Loan Modification Speech (can it get any nerdier than that? Can it? Sheesh) I want to comment on this little statistic, that is getting thrown around a lot:

Modified loans frequently re-default. Joshua Rosner at Graham-Fisher & Co. says 40% to 60% of subprime and Alt-A borrowers who have their loans modified end up defaulting anyway within the next two years. Fitch Ratings puts the recidivism rate at a slightly lower 35% to 40% for good modification programs.Let us bear in mind that such statistics have to be based on loans that were modified no more recently than 2005 (newer mods would not have a 24-month post-modification history). It is quite possible, indeed it is likely, that modifications done in 2005 and earlier (when there were many more refi opportunities and most borrowers could sell their homes for at least the loan amount) were done for borrowers with problems like job loss or illness that either simply recurred or that created other (non-mortgage) debt problems down the road.

This is not to argue that modifications done now for loans originated in 2005 and after would perform better. Or worse. Or the same. It is to say that we are probably in uncharted territory and that "past history" was a lousy guide when we made the loans and might be a lousy guide when we have to work them out.

Furthermore, 40-60% is a very big range. In the absence of other information, I would certainly guess that most if not all of that variation is due to servicer quality, not borrower quality. If that is true, then performance of modified loans can be improved by something that is well within the control of the industry.

Now you can go back to waiting around the teevee . . .

Fed: Homeowner Percent Equity Falls to Record Low

by Calculated Risk on 12/06/2007 12:14:00 PM

The Fed released the Q3 Flow of Funds report today.

Homeowner equity declined by $128 Billion in Q3 as appreciation slowed (why didn't assets decline?) and equity withdrawal was still strong.

Homeowner percent equity fell to a record low of 50.4% (this includes the almost 1/3 of homeowners with no mortgage). I'll have more this afternoon.

The Big Freeze: Details Soon

by Calculated Risk on 12/06/2007 12:11:00 PM

Mr. Bush speaks at 1:40PM ET. Mr. Paulson at 1:45PM. Tanta at 2:00PM.

OK, I'm just kidding about Tanta, but I'm looking forward to her comments.