RSS Feed

RSS Feed by Calculated Risk on 9/03/2010 11:23:00 AM

Friday, September 03, 2010

ISM Non-Manufacturing Index declines in August

Earlier employment posts:

The August ISM Non-manufacturing index was at 51.5%, down from 54.3% in July - and below expectations of 53.0%. The employment index showed contraction in August at 48.2%. Note: Above 50 indicates expansion, below 50 contraction.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

The overall ISM index, and the employment index, are both at the lowest level since January.

From the Institute for Supply Management: August 2010 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in August for the eighth consecutive month, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.

The report was issued today by Anthony Nieves, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee; and senior vice president — supply management for Hilton Worldwide. "The NMI (Non-Manufacturing Index) registered 51.5 percent in August, 2.8 percentage points lower than the 54.3 percent registered in July, indicating continued growth in the non-manufacturing sector but at a slower rate. The Non-Manufacturing Business Activity Index decreased 3 percentage points to 54.4 percent, reflecting growth for the ninth consecutive month, but at a slower rate than in July. The New Orders Index decreased 4.3 percentage points to 52.4 percent, and the Employment Index decreased 2.7 percentage points to 48.2 percent, reflecting contraction after one month of growth.

emphasis added

Employment-Population Ratio, Part Time Workers, Unemployed over 26 Weeks

by Calculated Risk on 9/03/2010 09:50:00 AM

Here are a few more graphs based on the employment report ...

Percent Job Losses During Recessions, aligned at Bottom Click on graph for larger image.

Click on graph for larger image.

This graph shows the job losses from the start of the employment recession, in percentage terms - this time aligned at the bottom of the recession (Both the 1991 and 2001 recessions were flat at the bottom, so the choice was a little arbitrary).

The dotted line shows the impact of Census hiring. In August, there were only 82,000 temporary 2010 Census workers still on the payroll. The number of Census workers will continue to decline - and the remaining gap between the solid and dashed red lines will be gone soon.

Employment-Population Ratio

The Employment-Population ratio increased to 58.5% in August from 58.4% in July.  This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.

This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.

Note: the graph doesn't start at zero to better show the change.

The Labor Force Participation Rate increased to 64.7% from 64.6% in July. This is the percentage of the working age population in the labor force. This increase was mostly because of the an increase in the teen participation rate (related to the very weak teen participation rate during the summer). The participation rate is well below the 66% to 67% rate that was normal over the last 20 years.

As the employment picture improves, people will return to the labor force, and that will put upward pressure on the unemployment rate.

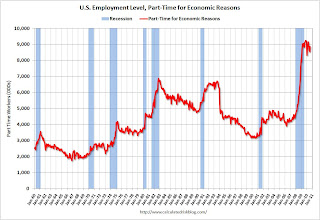

Part Time for Economic Reasons  From the BLS report:

From the BLS report:

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) increased by 331,000 over the month to 8.9 million. These individuals were working part time because their hours had been cut back or because they were unable to find a full-time job.The number of workers only able to find part time jobs (or have had their hours cut for economic reasons) was at 8.9 million in August. This increase was bad news.

The all time record of 9.24 million was set in October 2009.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 16.7% in August from 16.5% in July.

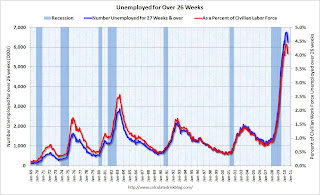

Unemployed over 26 Weeks

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.According to the BLS, there are 6.249 million workers who have been unemployed for more than 26 weeks and still want a job. This is 4.1% of the civilian workforce. It appears the number of long term unemployed has peaked ... hopefully not because people are giving up.

Summary

The underlying details of the employment report were mixed. The positives: the upward revisions to the June and July reports, a slight increase in hours worked for manufacturing employees (flat for all employees), an increase in hourly wages, and the decrease in the long term unemployed. Other positives include the slight increase in the employment-population ratio and the participation rate.

The negatives include the hiring of only 60,000 ex-Census, the increase in the unemployment rate (including U-6), and the increase in part time workers for economic reasons.

Overall this was a weak report and is consistent with a sluggish recovery.

Earlier employment post today:

August Employment Report: 60K Jobs ex-Census, 9.6% Unemployment Rate

by Calculated Risk on 9/03/2010 08:30:00 AM

From the BLS:

Nonfarm payroll employment changed little (-54,000) in August, and the unemployment rate was about unchanged at 9.6 percent, the U.S. Bureau of Labor Statistics reported today. Government employment fell, as 114,000 temporary workers hired for the decennial census completed their work. Private-sector payroll employment continued to trend up modestly (+67,000).Census 2010 hiring decreased 114,000 in August. Non-farm payroll employment increased 60,000 in July ex-Census.

Both June and July payroll employment were revised up. "June was revised from -221,000 to -175,000, and the change for July was revised from -131,000 to -54,000."

Click on graph for larger image.

Click on graph for larger image.This graph shows the unemployment rate vs. recessions.

Nonfarm payrolls decreased by 54 thousand in August. The economy has gained 229 thousand jobs over the last year, and lost 7.6 million jobs since the recession started in December 2007.

The second graph shows the job losses from the start of the employment recession, in percentage terms (as opposed to the number of jobs lost).

The second graph shows the job losses from the start of the employment recession, in percentage terms (as opposed to the number of jobs lost).The dotted line is ex-Census hiring. The two lines have almost joined since the decennial Census hiring is almost over.

For the current employment recession, employment peaked in December 2007, and this recession is by far the worst recession since WWII in percentage terms, and 2nd worst in terms of the unemployment rate (only early '80s recession with a peak of 10.8 percent was worse).

This is another weak report, however the upwards revisions to June and July were a positive. The participation rate increased slightly - and that is good news - but the unemployment rate also increased. I'll have much more soon ...

Update: For more, see: Employment-Population Ratio, Part Time Workers, Unemployed over 26 Weeks

Thursday, September 02, 2010

Krugman: On Inflation and Interest Rates

by Calculated Risk on 9/02/2010 11:46:00 PM

From Paul Krugman in the NY Times: The Real Story

... When Mr. Obama first proposed $800 billion in fiscal stimulus, there were two groups of critics. Both argued that unemployment would stay high — but for very different reasons.The second half slowdown arrived right on schedule (maybe a month early). And there is no question who was correct on inflation and interest rates.

One group — the group that got almost all the attention — declared that the stimulus was much too large, and would lead ... to skyrocketing interest rates and soaring inflation.

The other group, which included yours truly, warned that the plan was much too small given the economic forecasts then available. ... Critics in the second camp were particularly worried about what would happen this year, since the stimulus would have its maximum effect on growth in late 2009 then gradually fade out. Last year, many of us were already warning that the economy might stall in the second half of 2010.

But now what? Unemployment is still too high ...

Employment Report Preview

by Calculated Risk on 9/02/2010 08:30:00 PM

1) The consensus is for a headline payroll number of minus 90,000 and for the unemployment rate to increase to 9.6% in August from 9.5% in July.

Goldman Sachs is forecasting a minus 125,000 headline payroll number, with no change in private employment and minus 115,000 decline in decennial Census employment. That gives a negative 10,000 ex-Census.

2) My estimate is the decennial Census workforce was reduced by 116,000 in August. This suggests a consensus headline payroll number of +26,000 ex-Census (see point 4). I'll take the under on payroll employment ex-Census.

3) The unemployment rate is dependent on both job creation and the participation rate (both numbers from the household survey - payroll employment is from the establishment survey).

Usually the participation rate - the percent of the civilian population in the labor force - falls when the job market is weak. And a decline in the participation rate puts downward pressure on the unemployment rate (and the opposite is true when the participation rate increases). For technical reasons, there is a possibility that the participation rate increased in August - even with weak job creation - putting upward pressure on the unemployment rate.

4) And here is an easy prediction: there will be some confusion about which payroll number to report!

Here is an excerpt from a employment report preview story from CNBC:

Investors are likely to focus on the private payrolls number, analysts said, given that overall payrolls data is expected to have been influenced by the loss of government census hiring, among other factors.What "other factors"? The reason everyone has switched to the private payroll number is because of the hiring and layoffs associated with the decennial Census. But this misses any local and state government layoffs (kind of a big story right now).

Reporting that is consistent with non-decennial Census employment reports is to lead with the headline payroll number ex-Census. What has confused some people (I think) is that the Census hiring and layoffs is Not Seasonally Adjusted (NSA), and the headline number is SA. Usually it is not appropriate to mix NSA and SA numbers, but this is a rare exception.

I checked with the BLS, and I even submitted it as a question when the BLS had their first live chat back in March:

9:34 Michele Walker (BLS-CES) -Oh well ... this will be the last big change in decennial Census employment.

Submitted via email from Bill: Hi. The headline payroll number is seasonally adjusted, and the hiring for the 2010 Census is NSA. How would you suggest adjusting for the 2010 Census hiring to determine the underlying trend (not counting the snow storms!)?

Thanks for your question Bill.

There is an adjustment made for the 2010 Census. Before seasonally adjusting the estimates, BLS makes a special modification so that the Census workers do not influence the calculation of the seasonal factors. Specifically, BLS subtracts the Census workers from the not-seasonally adjusted estimates before running seasonal adjustment using X-12. After the estimates have been seasonally adjusted, BLS adds the Census workers to the seasonally adjusted totals. Therefore, to determine the underlying trend of the total nonfarm (TNF) employment estimates (minus the Census workers), simply subtract the Census employment from the seasonally adjusted TNF estimate.

Realtors, Builders oppose another Housing Tax Credit

by Calculated Risk on 9/02/2010 05:09:00 PM

A couple of quotes from Kathleen Pender at the San Francisco Chronicle: Little support for new home-buyer tax credit

"We are not advocating another one. We think it's important for the market to have time to recover on its own," says Walter Molony, spokesman for the National Association of Realtors.And HUD Secretary Shaun Donovan said yesterday, via Reuters: No talk of new homebuyer tax credit

...

"From a political standpoint, with Congress not wanting to increase the debt, it would be too expensive," [Bernard Markstein, senior economist with the National Association of Home Builders] says. "In terms of advisable, we are bordering on where tax credits become ineffective."

"It is not high on anyone's list that we have heard. We have not heard Congress talking about renewing it," Housing and Urban Development Secretary Shaun Donovan said in response to a reporter's question about a possible tax credit renewal.

Hotel Occupancy Rate: Just below 2008 Levels

by Calculated Risk on 9/02/2010 02:30:00 PM

Hotel occupancy is one of several industry specific indicators I follow ...

From HotelNewsNow.com: STR: Chain scales report weekly increases

Overall, the industry’s occupancy increased 10.6% to 60.1%, ADR rose 2.4% to US$96.50, and revenue per available room increased 13.2% to US$57.98.The following graph shows the four week moving average for the occupancy rate by week for 2008, 2009 and 2010 (and a median for 2000 through 2007).

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notes: the scale doesn't start at zero to better show the change. The graph shows the 4-week average, not the weekly occupancy rate.

On a 4-week basis, occupancy is up 7.9% compared to last year (the worst year since the Great Depression) and 3.9% below the median for 2000 through 2007.

The occupancy rate is just below the levels of 2008 - but 2008 was a tough year for the hotel industry!

Data Source: Smith Travel Research, Courtesy of HotelNewsNow.com

Greece: Default Probabilities before and after policy response

by Calculated Risk on 9/02/2010 12:18:00 PM

Here is a graph from the Council of Foreign Relations blog: Greek Debt Crisis – Apocalypse Later Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph from Paul Swartz at the CFR shows the default probabilities on three different dates:

On April 30th, no European plan was yet in place to address the ballooning Greek debt, and default was considered a real possibility in the short term. On May 11th, just after the European Stabilization Mechanism (ESM) was announced, markets sharply cut their view on the odds of default across all time horizons. ... On September 1st, the market’s view of the probability of default within two years was lower than before the ESM was announced, but higher over longer time frames.So initially the policy response lowered the default probabilities across all time frames (from red to light blue), but now - after further analysis - the default probabilities have increased for longer time frames (green).

Pending Home Sales increase in July

by Calculated Risk on 9/02/2010 10:00:00 AM

From the NAR: Pending Home Sales Rise

The Pending Home Sales Index ... rose 5.2 percent to 79.4 based on contracts signed in July from a downwardly revised 75.5 in June, but remains 19.1 percent below July 2009 when it was 98.1. The data reflects contracts and not closings, which normally occur with a lag time of one or two months.This suggests a small increase in existing home sales in September (reported when transactions close), but this also suggests double digit months of supply for some time.

Lawrence Yun, NAR chief economist, cautioned that there would be a long recovery process. “Home sales will remain soft in the months ahead ..."

Weekly initial unemployment claims decline slightly

by Calculated Risk on 9/02/2010 08:30:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending Aug. 28, the advance figure for seasonally adjusted initial claims was 472,000, a decrease of 6,000 from the previous week's revised figure of 478,000. The 4-week moving average was 485,500, a decrease of 2,500 from the previous week's revised average of 488,000.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the 4-week moving average of weekly claims since January 2000.

The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased this week by 2,500 to 485,500.

Claims for last week were revised up from 473,000 to 478,000. So the level this week is about the same as initially reported last week.

The current level of the 4-week average suggests a weak job market.