RSS Feed

RSS Feed by Calculated Risk on 9/09/2010 12:23:00 PM

Thursday, September 09, 2010

Government Employment since 1976

Menzie Chinn at Econbrowser posted a graph of total government employment over the last decade: The "Ever-Expanding" Government Sector, Illustrated

In response to the comments to his post, here are a couple of additional graphs: Click on graph for larger image.

Click on graph for larger image.

This graph shows federal, state, and local government employment as a percent of the civilian noninstitutional population since 1976 (all data from the BLS).

Federal government employment has decreased over the last 35 years (mostly in the 1990s), state government employment has been flat, and local government employment has increased.

Note the small spikes very 10 years. That is the impact of the decennial census. The second graph shows government employment excluding education as a percent of the civilian noninstitutional.

The second graph shows government employment excluding education as a percent of the civilian noninstitutional.

The percent of federal and state government employment (ex-education) have all declined. Local government employment has been steady - so overall government employment (ex-education) as a percent of the civilian population is down over the last 35 years.

Trade Deficit declines in July

by Calculated Risk on 9/09/2010 09:11:00 AM

The Census Bureau reports:

[T]otal July exports of $153.3 billion and imports of $196.1 billion resulted in a goods and services deficit of $42.8 billion, down from $49.8 billion in June, revised.

Click on graph for larger image.

Click on graph for larger image.The first graph shows the monthly U.S. exports and imports in dollars through June 2010.

Although imports declined in July, imports have been increasing much faster than exports.

The second graph shows the U.S. trade deficit, with and without petroleum, through July.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.The decrease in the deficit in July was across the board, although the oil deficit only declined slightly. And the trade gap with China declined slightly to $25.92 billion from $26.15 billion in June - essentially unchanged.

This is the 2nd largest monthly trade deficit since the 2008 collapse in trade.

Weekly Initial Unemployment Claims decline

by Calculated Risk on 9/09/2010 08:30:00 AM

UPDATE: BofA noted this morning that 9 states reported delays in filing jobless claims because of labor day weekend ... so the actual was probably higher (ht Brian)

The DOL reports on weekly unemployment insurance claims:

In the week ending Sept. 4, the advance figure for seasonally adjusted initial claims was 451,000, a decrease of 27,000 from the previous week's revised figure of 478,000. The 4-week moving average was 477,750, a decrease of 9,250 from the previous week's revised average of 487,000.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the 4-week moving average of weekly claims since January 2000.

The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased this week by 9,250 to 477,750.

Claims for last week were revised up from 472,000 to 478,000.

This is the lowest level for weekly claims since early July, but it is still very high - and the current level of the 4-week average suggests a weak job market.

Wednesday, September 08, 2010

The Frugal are Losers Too

by Calculated Risk on 9/08/2010 08:34:00 PM

From Graham Bowley at the NY Times: Debtors Feast at the Expense of the Frugal

For example, anyone keeping $500,000 in a 12-month certificate of deposit earning a rate of 1.5 percent annually — one of the best savings rates available nationally these days — would earn $7,500 a year, hardly enough to live on. Just three years ago, that same investment would have generated $26,250.Obviously retired people, living on bond yields, are taking a hit as bonds mature. And this is pushing some conservative investors into riskier assets too.

... Anyone investing $500,000 in 10-year Treasuries at current yields would earn $13,500 a year.

The BEA has been reporting that Personal interest income has been falling since Sept 2008, and I expect interest income will fall further as bonds and CDs mature.

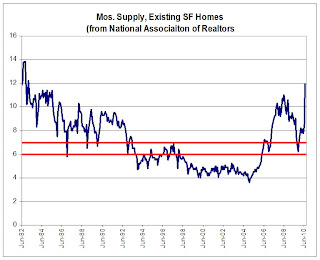

Lawler: Again on Existing Home Months’ Supply: What’s “Normal?”

by Calculated Risk on 9/08/2010 04:49:00 PM

CR Note: This is from economist Tom Lawler.

It has become “common practice” when talking about the “months’ supply” of existing homes for sale for folks to say that the “normal” months’ supply, or the months’ supply that means it is neither a “buyers” or a “sellers” market, is around 6 to 7 months. Yet here is the history of months’ supply for existing SF homes from the National Association of Realtors. Click on graph for larger image in new window.

Click on graph for larger image in new window.

As one can see, this “metric” actually has not been in the six-to-seven month range very often. From mid-1982 through 1992, the months’ supply measure was above seven months in all but a handful of months, while from 1998 to the spring of 2006 it was always below six months.

The measure, of course, is quite volatile, and sorta weird in that the inventory number (the numerator) is not seasonally adjusted while the sales data (the denominator) is seasonally adjusted. The measure also can be extremely volatile as sales tend to be impacted more by “special factors” (weather, tax credits, etc.) than listings.

But the measure is only one of many measures that may be “indicative” of “excess” supply, and it probably isn’t even close to the best measure. However, it is the most timely, so folks watch it closely – but sometimes place WAY to much meaning in month-to-month swings.

CR Note: The above was from economist Tom Lawler.

From CR: I'm one of the people who has called 6 to 7 months a "normal" months-of-supply. As the graph above shows, it is hard to define a normal based on the last 30 years.

I've heard the 6 to 7 months metric for years - and it fits the data I have. Perhaps the idea that 6 to 7 months is "normal" comes from new home inventory. This graph shows new home inventory back to 1963 (unfortunately Tom Lawler's graph only goes back to 1982).

This graph shows new home inventory back to 1963 (unfortunately Tom Lawler's graph only goes back to 1982).

For new homes, it does look like around 6 months supply is normal. I suspect if the existing home graph went back to the '60s, something like 6 months would be normal.

Lawler's caution is something to keep in mind. But double digit months-of-supply is clearly very high.

Consumer Credit Declines in July

by Calculated Risk on 9/08/2010 03:09:00 PM

The Federal Reserve reports:

In July, total consumer credit decreased at an annual rate of 1-3/4 percent. Revolving credit decreased at an annual rate of 6-1/4

percent, and nonrevolving credit increased at an annual rate of 1/2 percent.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the increase in consumer credit since 1978. The amounts are nominal (not inflation adjusted).

Revolving credit (credit card debt) is off 15.2% from the peak. Non-revolving debt (auto, furniture, and other loans) is off 1.1% from the peak. Note: Consumer credit does not include real estate debt.

Fed's Beige Book: Continued growth, but "widespread signs of a deceleration"

by Calculated Risk on 9/08/2010 02:00:00 PM

Note: This is based on information collected on or before August 30, 2010.

From the Federal Reserve: Beige book

Reports from the twelve Federal Reserve Districts suggested continued growth in national economic activity during the reporting period of mid-July through the end of August, but with widespread signs of a deceleration compared with preceding periods.And on real estate:

...

Manufacturing activity expanded further on balance, although the pace of growth appeared to be slower than earlier in the year. Most Districts reported further gains in production activity and sales across a broad spectrum of manufacturing industries. However, New York, Richmond, Atlanta, and Chicago noted that the overall pace of growth slowed, while Philadelphia, Cleveland, and Kansas City reported that demand softened compared with the previous reporting period.

Activity in residential real estate markets declined further. Most District reports highlighted evidence of very low or declining home sales, which many attributed to a sustained lull following the expiration of the homebuyer tax credit at the end of June. Some Districts, such as New York and Dallas, noted that the expiration of the tax credit created especially weak conditions for lower-priced homes, while others, including Philadelphia and Kansas City, identified the high end of the market as the primary weak spot. Residential construction activity declined in most areas in response to weak demand.Pretty weak, but still growing in August.

...

Demand for commercial, industrial, and retail space generally remained depressed. Vacancy rates stayed at elevated levels in general and rose further in a few Districts, placing substantial downward pressure on rents.

BLS: Job Openings increases in July, Low Labor Turnover

by Calculated Risk on 9/08/2010 10:00:00 AM

Note: The temporary decennial Census hiring and layoffs has distorted this series over the last few months. The total separations has increased, but that includes the temporary Census workers that were let go.

From the BLS: Job Openings and Labor Turnover Summary

There were 3.0 million job openings on the last business day of July 2010, the U.S. Bureau of Labor Statistics reported today. The job openings rate increased over the month to 2.3 percent. The hires rate (3.3 percent) and the separations rate (3.4 percent) were unchanged....Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. The CES (Current Employment Statistics, payroll survey) is for positions, the CPS (Current Population Survey, commonly called the household survey) is for people.

The following graph shows job openings (purple), hires (blue), Total separations (include layoffs, discharges and quits) (red) and Layoff, Discharges and other (yellow) from the JOLTS.

Unfortunately this is a new series and only started in December 2000.

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notice that hires (blue) and separations (red) are pretty close each month. In July, about 4.4 million people lost (or left) their jobs, and 4.23 million were hired (this is the labor turnover in the economy) for a loss of 168,000 jobs in July (this includes Census jobs lost).

The employment report (revised) showed a loss of only 54,000 jobs in July, and usually these numbers are pretty close, so this is a little puzzling. I expect some revisions to one or both reports.

When the hires (blue line) is above total separations, the economy is adding net jobs, when the blue line is below total separations (as in July), the economy is losing net jobs.

It appears job openings are still trending up, however labor turnover is still fairly low.

MBA: Mortgage Purchase Activity increases slightly

by Calculated Risk on 9/08/2010 07:32:00 AM

The MBA reports: Mortgage Purchase Applications Up, Refinance Applications Fall Slightly in Latest MBA Weekly Survey

The Refinance Index decreased 3.1 percent from the previous week. The seasonally adjusted Purchase Index increased 6.3 percent from one week earlier.

...

“Purchase applications increased last week, reaching the highest level since the end of May. However, purchase activity remains well below levels seen prior to the expiration of the homebuyer tax credit, and is almost 40 percent below the level recorded one year ago,” said Michael Fratantoni, MBA’s Vice President of Research and Economics. “On the other hand, refinance volume dropped last week for the first time in six weeks, but the level of applications to refinance remains close to recent highs, as historically low mortgage rates continue to draw borrowers into the market.”

...

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.50 percent from 4.43 percent, with points decreasing to 0.96 from 1.34 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

As the MBA's Fratantoni noted, "purchase activity remains well below levels seen prior to the expiration of the homebuyer tax credit" and this suggests existing home sales in August, September and even October, will only be slightly higher than in July.

Tuesday, September 07, 2010

Mortgage Rates and Home Prices

by Calculated Risk on 9/07/2010 10:21:00 PM

David Leonhardt writes at the NY Times Economix: Mortgage Rates and Home Prices

Interest rates are historically low right now. They will surely rise at some point. All else equal, higher rates should push home prices down.Nope.

...

[see graph]

...

It’s not easy to see much of a relationship.

...

My best guess for why the two don’t correlate more closely is the role that psychology plays in housing markets. Prices just don’t move as quickly as economic theory suggests they should.

I've tried to explain this several times in several different ways. Price is what you pay for something. Interest rates are related to how the item is financed. Some people pay cash for a house. Would they pay more because interest rates are low? Nope.

Imagine just one buyer gets a special interest rate. Would that lucky buyer be willing to pay more than all other buyers for the same property? Nope.

It is true that low rates make buying more attractive as compared to renting. And that can increase the demand for buying - and more demand might mean slightly higher prices. But if rates are low, a rational buyer will expect mortgages rates to rise when they sell the property, and under the theory that mortgage rates impact price, the price will then fall in the future. That makes the property less attractive, and the buyer in the low interest rate environment will not want to overpay for the house.

So the buyer needs to consider both current interest rates and future interest rates, and by the time they are done doing all the calculations, you get the graph that Leonhardt shows. And that is exactly what I'd expect - there is little relationship between house prices and mortgage rates. That doesn't surprise me at all.

Note: When I wrote about this in 2005, I used a car example. Would people pay more for a car if interests rates are low?