RSS Feed

RSS Feed by Calculated Risk on 9/20/2010 11:31:00 AM

Monday, September 20, 2010

NBER: Recession ended in June 2009

From NBER: NBER Business Cycle Dating Committee Announces Trough Date

The Business Cycle Dating Committee of the National Bureau of Economic Research ... determined that a trough in business activity occurred in the U.S. economy in June 2009. The trough marks the end of the recession that began in December 2007 and the beginning of an expansion. The recession lasted 18 months, which makes it the longest of any recession since World War II.This is somewhat subjective - and I thought they'd wait longer because the committee usually waits until some of the key indicators have returned to pre-recession levels. This time no indicator has reached the pre-recession level, and some are still very low (like personal income less transfer payments).

In determining that a trough occurred in June 2009, the committee did not conclude that economic conditions since that month have been favorable or that the economy has returned to operating at normal capacity. Rather, the committee determined only that the recession ended and a recovery began in that month. A recession is a period of falling economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. The trough marks the end of the declining phase and the start of the rising phase of the business cycle. Economic activity is typically below normal in the early stages of an expansion, and it sometimes remains so well into the expansion.

The committee decided that any future downturn of the economy would be a new recession and not a continuation of the recession that began in December 2007. The basis for this decision was the length and strength of the recovery to date.

NAHB Builder Confidence stuck at low level in September

by Calculated Risk on 9/20/2010 10:00:00 AM

The National Association of Home Builders (NAHB) reports the housing market index (HMI) was at 13 in September. This is the same low level as in August and below expectations. The record low was 8 set in January 2009, and 13 is very low ...

Note: any number under 50 indicates that more builders view sales conditions as poor than good. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph compares the NAHB HMI (left scale) with single family housing starts (right scale). This includes the September release for the HMI and the July data for starts (August starts will be released tomorrow).

This shows that the HMI and single family starts mostly move in the same direction - although there is plenty of noise month-to-month.

Press release from the NAHB: Builder Confidence Unchanged in September

Builder confidence in the market for newly built, single-family homes held unchanged in September from the previous month's low level of 13, according to the latest National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today.

"In general, builders haven't seen any reason for improved optimism in market conditions over the past month," noted NAHB Chairman Bob Jones, a home builder from Bloomfield Hills, Mich. "If anything, consumer uncertainty has increased, and builders feel their hands are tied until potential home buyers feel more secure about the job market and economy."

"The stall in the nation's housing market continues," agreed NAHB Chief Economist David Crowe. "Builders report that the two leading obstacles to new-home sales right now are consumer reluctance in the face of the poor job market and the large number of foreclosed properties for sale."

Over 50 and Unemployed: Will they ever work again?

by Calculated Risk on 9/20/2010 08:33:00 AM

From Mokoto Rich at the NY Times: For the Unemployed Over 50, Fears of Never Working Again (ht Ann)

Of the 14.9 million unemployed, more than 2.2 million are 55 or older. Nearly half of them have been unemployed six months or longer, according to the Labor Department. The unemployment rate in the group — 7.3 percent — is at a record, more than double what it was at the beginning of the latest recession.It is hard for people in their 50s to change careers, or rebuild their savings after a long period of unemployment. And, as in the story, they may end up taking Social Security early - just to get by - and that means they will receive a significantly lower monthly payout than if they waited until 66. A very tough situation.

After other recent downturns, older people who lost jobs fretted about how long it would take to return to the work force and worried that they might never recover their former incomes. But today, because it will take years to absorb the giant pool of unemployed at the economy’s recent pace, many of these older people may simply age out of the labor force before their luck changes.

Sunday, September 19, 2010

FT: Junk bond prices hit pre-crisis levels

by Calculated Risk on 9/19/2010 08:47:00 PM

From the Financial Times: Junk bond prices hit pre-crisis levels

Strong investor demand for junk bonds has pushed the average price on such corporate debt to its highest level since June 2007, when companies could borrow with ease at the height of the credit boom.And from the WSJ: Bond Markets Get Riskier

except with permission

Bond markets are growing riskier as investors seeking steady returns bid up prices and ignore some early warning signs similar to those that flashed during the credit bubble.This seems like investors chasing yield - and that is making it easy to sell junk bonds. Oh well ...

Last week, prices on high-yield, or junk, bonds, hit their highest level since 2007, nearly double their lows of the credit crisis. Nine months into the year, companies have sold $172 billion in junk bonds, already an annual record, according to data provider Dealogic.

Weekly Schedule for September 19th

by Calculated Risk on 9/19/2010 02:45:00 PM

Note: The previous post is a summary of last week with graphs.

Four key housing reports will be released this week: the September homebuilder confidence survey (Monday), August housing starts (Tuesday), August existing home sales (Thursday), and August new home sales (Friday). Also the FOMC meets on Tuesday.

Making Home Affordable Program (HAMP) for August and the “Housing Scorecard”

Moody's/REAL Commercial Property Price Index (CPPI) for July.

10 AM: The September NAHB homebuilder survey. This index collapsed following the expiration of the home buyer tax credit. The consensus is for a slight increase to 14 from 13 in August (still very depressed).

8:30 AM: Housing Starts for August. Housing starts also collapsed following the expiration of the home buyer tax credit. The consensus is for a slight increase to 550K (SAAR) in August from 546K in July.

10:00 AM: the BLS will release the Regional and State Employment and Unemployment report for August.

2:15 PM: The FOMC statement will be released. I don't expect any significant changes to the statement compared to the statement following the August meeting.

Early: The AIA's Architecture Billings Index for August will be released (a leading indicator for commercial real estate). This has been showing ongoing contraction, and usually this leads investment in non-residential structures (hotels, malls, office) by 9 to 12 months.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index declined sharply following the expiration of the tax credit, and the index has only recovered slightly over the last couple months - suggesting reported home sales through at least October will be very weak.

10:00 AM: 10:00 FHFA House Price Index for July. This is based on GSE repeat sales and is no longer as closely followed as Case-Shiller (or CoreLogic).

8:30 AM: The initial weekly unemployment claims report will be released. Consensus is for about the same as last week (450 thousand).

10:00 AM: Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for an increase to 4.1 million (SAAR) in August from 3.83 million in July. Housing economist Tom Lawler is projecting 4.1 million SAAR. In addition to sales, the level of inventory and months-of-supply will be very important (since months-of-supply impacts prices).

10:00 AM: Conference Board's index of leading indicators for August. The consensus is for a 0.1% increase in this index.

1:00 PM ET: Former Fed Chairman Paul A. Volcker gives the Keynote address at the Chicago Fed and IMF Thirteenth Annual International Banking Conference

8:30 AM: Durable Goods Orders for August from the Census Bureau. The consensus is for a 1.0% decline in durable good orders.

10:00 AM: New Home Sales for August from the Census Bureau. The consensus is for a slight increase in sales to 290K (SAAR) in August from 276K in July.

1:00 PM: Richmond Fed President Jeffrey Lacker speaks on the economic outlook at the 2010 Kentucky Economic Association Annual Conference

4:30 PM: Fed Chairman Ben Bernanke speaks at the Conference Co-sponsored by the Center for Economic Policy Studies and the Bendheim Center for Finance, Princeton University, Princeton, N.J: "Implications of the Financial Crisis for Economics"

After 4:00 PM: The FDIC will probably have another busy Friday afternoon ...

Summary for week ending Sept 18th

by Calculated Risk on 9/19/2010 10:30:00 AM

A summary of last week - mostly in graphs:

From the Fed: Industrial production and Capacity Utilization

Industrial production rose 0.2 percent in August after a downwardly revised increase of 0.6 percent in July [revised down from 1.0 percent]. ... The capacity utilization rate for total industry rose to 74.7 percent, a rate 4.7 percentage points above the rate from a year earlier and 5.9 percentage points below its average from 1972 to 2009.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows Capacity Utilization. This series is up 9.6% from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 74.7% is still far below normal - and well below the the pre-recession levels of 81.2% in November 2007. (Note: this is actual a decrease before the revision to July)

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.This is the highest level for industrial production since Oct 2008, but production is still 7.2% below the pre-recession levels at the end of 2007.

The increase in August was about consensus, however the sharp downward revision to July puts this below consensus.

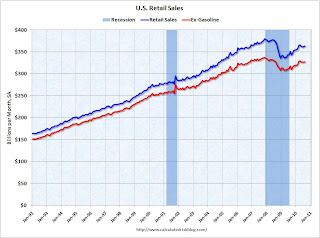

On a monthly basis, retail sales increased 0.4% from July to August (seasonally adjusted, after revisions), and sales were up 3.6% from August 2009. Retail sales increased 0.6% ex-autos.

On a monthly basis, retail sales increased 0.4% from July to August (seasonally adjusted, after revisions), and sales were up 3.6% from August 2009. Retail sales increased 0.6% ex-autos. This graph shows retail sales since 1992. This is monthly retail sales, seasonally adjusted (total and ex-gasoline).

Retail sales are up 8.4% from the bottom, but still off 4.3% from the pre-recession peak.

Retail sales are still below the April level - and have mostly moved sideways for six months.

From CoreLogic: CoreLogic Home Price Index Remained Flat in July

This graph shows the national CoreLogic HPI data since 1976. January 2000 = 100.

This graph shows the national CoreLogic HPI data since 1976. January 2000 = 100.The index is flat over the last year, and off 28% from the peak.

The index is 6.1% above the low set in March 2009, and I expect to see a new post-bubble low for this index later this year or early in 2011.

Press Release: August PCI Decline Signals Struggling Economy, but no Double-Dip

Press Release: August PCI Decline Signals Struggling Economy, but no Double-DipThis graph shows the index since January 1999.

This is a new index, and doesn't have much of a track record in real time, although the data appears to suggest that the recovery has slowed - even stalled - over the last 4 months.

The Cleveland Fed has released the median CPI:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.1% (0.6% annualized rate) in August. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.2% annualized rate) during the month.

...

Over the last 12 months, the median CPI rose 0.5%, the trimmed-mean CPI rose 0.9%, the CPI rose 1.1%, and the CPI less food and energy rose 0.9%.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows three measure of inflation, Core CPI, Median CPI (from the Cleveland Fed), and 16% trimmed CPI (also from Cleveland Fed).

They all show that inflation has been falling, and that measured inflation is up less than 1% year-over-year. Core CPI was flat, and median CPI and the 16% trimmed mean CPI were up 0.1% in August.

Best wishes to all.

Hubbard and Mayer recycle Morgan Stanley's housing proposal

by Calculated Risk on 9/19/2010 07:25:00 AM

Let me start with an excerpt from Chirs Mayer and Todd Sinai's piece in Sept 2005: Bubble Trouble? Not Likely

Chicken Littles have squawked that the sky -- or the ceiling -- is about to fall on the housing market. ... Yet basic economic logic suggests that this apparent evidence of a bubble is anything but. Even in the highest-price cities, housing is, at most, slightly more expensive than average.And from Glenn Hubbard on Face the Nation in August, 2005

I don't think we're likely to see a large nominal price collapse, that is largely falling house prices, but I think we'll see much slower rates of growth in house prices after 2005.Since I was one of those "Chicken Littles", I'm curious how those views on housing worked out?

And now Glenn Hubbard and Chris Mayer recycle the poorly conceived Morgan Stanley proposal: How Underwater Mortgages Can Float the Economy

[W]e propose a new program through which the federal government would direct the public and quasi-public entities that guarantee mortgages — Fannie Mae, Freddie Mac, Ginnie Mae, the Department of Veterans Affairs loan-guarantee program and the Federal Housing Administration — to make it far easier and quicker for homeowners to refinance.At least they mention the existing refinance programs already in place (that was an improvement on MS)!

This program would be simple: the agencies would direct loan servicers — the middlemen who monitor and report loan payments — to send a short application to all eligible borrowers promising to allow them to refinance with minimal paperwork. Servicers would receive a fixed fee for each mortgage they refinanced, which would be rolled into the mortgage to eliminate costs to taxpayers.

But the rest of Tom Lawler's criticism still holds: “Slam-Dunk” Stimulus? MS = Missing Something!!!!

Saturday, September 18, 2010

FOMC Statement Preview

by Calculated Risk on 9/18/2010 09:44:00 PM

I thought there were three things to look for in the August 10th FOMC statement:

1) How the statement would discuss the economic slowdown.

The FOMC statement was more pessimistic in August than in June.

Information received since the Federal Open Market Committee met in June indicates that the pace of recovery in output and employment has slowed in recent months. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising; however, investment in nonresidential structures continues to be weak and employers remain reluctant to add to payrolls. Housing starts remain at a depressed level. Bank lending has continued to contract. Nonetheless, the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, although the pace of economic recovery is likely to be more modest in the near term than had been anticipated.In the period since the August FOMC meeting, the economic data has remained weak, but the data hasn't indicated a further slowdown (at least not yet). So I expect the tone of the first paragraph to be about the same.

2) How the FOMC would express more concern about deflation. The FOMC didn't make a significant change:

Measures of underlying inflation have trended lower in recent quarters and, with substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to be subdued for some time.Actually inflation expectations have been trending down, and the FOMC might remove the "stable" expectations phrase this week (although this seems to be a key point of contention on the FOMC).

3) And the BIG one for the August meeting was how the FOMC would change their reinvestment strategy. They decided to keep the Federal Reserve's holdings of securities stable by investing the principal payments from maturing MBS in longer-term Treasury securities.

So what will change in the September FOMC statement? Probably very little. The first paragraph will be reworked a little, but the tone will probably remain the same. And the key sentence "exceptionally low levels of the federal funds rate for an extended period" will mostl likely stay the same.

And it seems too soon for further easing based on Fed Chairman Ben Bernanke comments in his speech at Jackson Hole. Bernanke suggested that additional easing would probably require “significant weakening of the outlook” or a meaningful decline in inflation expectations (or further disinflation). The first hasn't happened yet ... although they might express more concern about disinflation this week.

Q2 Flow of Funds: Household Net Worth off $12.3 Trillion from Peak

by Calculated Risk on 9/18/2010 05:10:00 PM

The Federal Reserve released the Q2 2010 Flow of Funds report yesterday: Flow of Funds.

According to the Fed, household net worth is now off $12.3 Trillion from the peak in 2007, but up $4.7 trillion from the trough in Q1 2009.  Click on graph for larger image in new window.

Click on graph for larger image in new window.

This is the Households and Nonprofit net worth as a percent of GDP.

This includes real estate and financial assets (stocks, bonds, pension reserves, deposits, etc) net of liabilities (mostly mortgages). Note that this does NOT include public debt obligations.

Note that this ratio was relatively stable for almost 50 years, and then we saw the stock market and housing bubbles. This graph shows homeowner percent equity since 1952.

This graph shows homeowner percent equity since 1952.

Household percent equity (as measured by the Fed) collapsed when house prices collapsed in 2007 and 2008.

In Q2 2010, household percent equity (of household real estate) was up to 40.7% from the all time low of 36.1% in Q1 2009. The increase was due to both an increase in the value of household real estate and a $49 billion decline in mortgage debt.

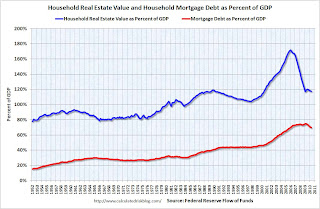

Note: something less than one-third of households have no mortgage debt. So the approximately 50+ million households with mortgages have far less than 40.7% equity. The third graph shows household real estate assets and mortgage debt as a percent of GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

Mortgage debt declined by $49 billion in Q2. Mortgage debt has now declined by $463 billion from the peak. According to an analysis by the WSJ, most of the decline in debt has been because of defaults, see: Defaults Account for Most of Pared Down Debt

As house prices decline further, I expect the percent equity to decline and household net worth to fall.

Unofficial Problem Bank List increases to 854 institutions

by Calculated Risk on 9/18/2010 11:20:00 AM

Note: this is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for September 17, 2010.

Changes and comments from surferdude808:

The FDIC got back to work closing banks in earnest this Friday after taking about a month hiatus. Also, as anticipated the OCC released its actions for July/August. Activities by the FDIC and OCC contributed to many changes in the Unofficial Problem Bank List this week as the six failures were removed and there were 11 additions.Once again - a special thanks to surferdude808 for all his hard work maintaining this list.

After these changes, the Unofficial Problem Bank List stands at 854 institutions with assets of $416 billion, up from 849 institutions with assets of $415.3 billion last week.

The failures include The Peoples Bank ($447 million), Maritime Savings Bank ($350 million), First Commerce Community Bank ($248 million Ticker: FCGA), Bank of Ellijay ($169 million), ISN Bank ($82 million), and Bramble Savings Bank ($48 million).

Most notable among the 11 additions are Nextier Bank, National Association, Evans City, PA ($558 million); American National Bank of Minnesota, Baxter, MN ($322 million); State Bank Financial, La Crosse, WI ($308 million); and National Bank of New York City, New York City, NY ($253 million).