RSS Feed

RSS Feed by Calculated Risk on 10/31/2016 01:41:00 PM

Monday, October 31, 2016

Q3 2016 GDP Details on Residential and Commercial Real Estate

The BEA has released the underlying details for the Q3 advance GDP report this morning.

The BEA reported that investment in non-residential structures increased at a 5.4% annual pace in Q3. This is a turnaround from recent quarters when non-residential investment declined due to less investment in petroleum exploration. Investment in petroleum and natural gas exploration still declined in Q3, from a $47.1 billion annual rate in Q2 to a $42.2 billion annual rate in Q3 - and is down from $149 billion in Q3 2014 (down by more than two-thirds).

Excluding petroleum, non-residential investment in structures increased at a 10% annual rate in Q3.

Click on graph for larger image.

Click on graph for larger image.

The first graph shows investment in offices, malls and lodging as a percent of GDP. Office, mall and lodging investment has increased a little recently, but from a very low level.

Investment in offices increased in Q3, and is up 28% year-over-year -increasing from a very low level - and is now above the lows for previous recessions (as percent of GDP).

Investment in multimerchandise shopping structures (malls) peaked in 2007 and was up year-over-year. The vacancy rate for malls is still very high, so investment will probably stay low for some time.

Lodging investment increased further in Q3, and with the hotel occupancy rate near record levels, it is likely that hotel investment will increase further in the near future. Lodging investment is up 23% year-over-year.

My guess is office and hotel investment growth will start to slow (office vacancies are still high, although hotel occupancy is near record levels). But investment growth has been very strong this year.

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

Home improvement was the top category for five consecutive years following the housing bust ... but now investment in single family structures has been back on top for three years and will probably stay there for a long time.

However - even though investment in single family structures has increased from the bottom - single family investment is still very low, and still below the bottom for previous recessions as a percent of GDP. I expect further increases over the next few years.

Investment in single family structures was $237 billion (SAAR) (about 1.3% of GDP), and was down in Q3 compared to Q2, but is down slightly year-over-year.

Investment in home improvement was at a $223 billion Seasonally Adjusted Annual Rate (SAAR) in Q2 (about 1.1% of GDP), and is up 9% year-over-year.

Dallas Fed: Regional Manufacturing Activity Increases in October

by Calculated Risk on 10/31/2016 10:50:00 AM

From the Dallas Fed: Texas Manufacturing Activity Increases Again, but at a Slower Pace

Texas factory activity increased again in October, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, posted a fourth consecutive positive reading but moved down to 6.7. This suggests output grew but at a slower pace this month. ...This was the last of the regional Fed surveys for October.

...

The general business activity index has been negative for nearly two years, although it continued to push closer to positive territory in October, coming in at -1.5.

...

Labor market measures indicated flat employment levels and slightly shorter workweek length. The employment index came in at 0.2, suggesting little change in headcounts in October. The hours worked index edged down to -1.8. ...

emphasis added

Here is a graph comparing the regional Fed surveys and the ISM manufacturing index:

Click on graph for larger image.

Click on graph for larger image.The New York and Philly Fed surveys are averaged together (yellow, through October), and five Fed surveys are averaged (blue, through October) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through September (right axis).

It seems likely the ISM manufacturing index will show expansion again in October, and the consensus is for a reading of 51.6.

Black Knight: House Price Index up 0.3% in August, Up 5.3% year-over-year

by Calculated Risk on 10/31/2016 09:30:00 AM

Note: I follow several house price indexes (Case-Shiller, CoreLogic, Black Knight, Zillow, FHFA, FNC and more). Note: Black Knight uses the current month closings only (not a three month average like Case-Shiller or a weighted average like CoreLogic), excludes short sales and REOs, and is not seasonally adjusted.

From Black Knight: Black Knight Home Price Index Report: August 2016 Transactions U.S. Home Prices Up 0.3 Percent for the Month; Up 5.3 Percent Year-Over-Year

• August’s 5.3 percent annual home price appreciation (HPA) continues a trend of very stable growth, with seven of the last eight months seeing the same rate of annual HPAThe year-over-year increase in this index has been about the same for the last year.

• At $266K, the U.S. is now within just 0.7 percent of a new national peak and up over 33 percent from the market’s bottom

• Nine states saw negative monthly price movement, led by South Carolina, North Dakota, Virginia, Connecticut and Missouri, all down 0.3 percent from July

• Home prices in nine of the nation’s 20 largest states and nine of the 40 largest metros hit new peaks

Note that house prices are close to the bubble peak in nominal terms, but not in real terms (adjusted for inflation).

Personal Income increased 0.3% in September, Spending increased 0.5%

by Calculated Risk on 10/31/2016 08:36:00 AM

The BEA released the Personal Income and Outlays report for September:

Personal income increased $46.7 billion (0.3 percent) in September according to estimates released today by the Bureau of Economic Analysis ... Personal consumption expenditures (PCE) increased $61.0 billion (0.5 percent).On inflation: The PCE price index increased 1.2 percent year-over-year due to the sharp decline in oil prices (This was up from 1.0% year-over-year in August). The core PCE price index (excluding food and energy) increased 1.7 percent year-over-year in September (the same as in August).

...

Real PCE increased 0.3 percent. The PCE price index increased 0.2 percent. Excluding food and energy, the PCE price index increased 0.1 percent.

Sunday, October 30, 2016

Sunday Night Futures: Gasoline Prices up Slightly Year-over-year

by Calculated Risk on 10/30/2016 06:24:00 PM

Weekend:

• Schedule for Week of Oct 30, 2016

• "How do I protect myself if Trump is elected?"

Monday:

• At 8:30 AM ET, Personal Income and Outlays for September. The consensus is for a 0.4% increase in personal income, and for a 0.5% increase in personal spending. And for the Core PCE price index to increase 0.1%.

• At 9:45 AM, the Chicago Purchasing Managers Index for October. The consensus is for a reading of 54.3, up from 54.2 in September.

• At 10:30 AM, the Dallas Fed Survey of Manufacturing Activity for October. This is the last of the regional Fed surveys for October.

From CNBC: Pre-Market Data and Bloomberg futures: S&P futures and DOW futures are down slightly (fair value).

Oil prices were down over the last week with WTI futures at $48.70 per barrel and Brent at $49.71 per barrel. A year ago, WTI was at $47, and Brent was at $48 - so oil prices are UP slightly year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.20 per gallon - a year ago prices were $2.18 per gallon - so gasoline prices are up slightly year-over-year.

"How do I protect myself if Trump is elected?"

by Calculated Risk on 10/30/2016 12:01:00 PM

Quite a few readers have asked me this question. My usual answer is that I expect Ms. Clinton to be elected President, and that the expansion will continue.

I've spoken to several key analysts and economists, and for their forecasts, all are assuming Ms. Clinton will be the next President (my forecasts also assume a Clinton presidency). So if Trump is elected, expect some market volatility as forecasts are changed. As Merrill Lynch recently noted:

"As our strategists have noted, the initial reaction to a potential Trump victory would likely be a risk-off event in the markets, which we think could end up delaying the Fed from hiking in December."That is just a guess at the short term reaction. The general rule is don't invest based on your political views.

However policy does matter for investing and the economy. As an example, it was obvious to invest in oil when George W. Bush became President. And insurance companies like United Healthcare and Aetna seemed like good bets with a President Obama.

Another example of policy is the deregulation of banks (and the anti-regulation attitude of the Bush administration) as part of the housing bubble story.

But what about with Mr. Trump? He has said he'd "build a wall" along the border with Mexico, renegotiate all trade deals, cut taxes on high income earners, repeal Obamacare and more. But it is unclear what he'd actually do as President. As an example, no one really thinks a wall will be built along the entire border (maybe sections of a wall - and Mexico wouldn't pay for it).

Repealing the ACA - without a replacement - would lead to many millions of Americans without health insurance. And those with preexisting conditions would be uninsurable. This seems politically unlikely (without a replacement policy), but if it happens, sell those health insurance companies.

Right now it is hard to guess what policy would look like with Mr. Trump (Trump doesn't seem to understand policy issues - like his ignorant comments on the VAT while talking about trade with Mexico). One key concern with Trump is the potential for a trade war - and that could happen almost without warning.

Long time readers remember when I used to write about the impact of policy (both good and bad), but there hasn't been much policy to discuss for the last few years. If Trump is elected, I'd expect a GOP sweep, and then I'll be writing frequently about policy again. Since Trump is at war with the data (he rejects data that doesn't fit his views), I don't expect evidence based policy proposals - and that almost always means bad results.

Until we see the actual policy proposals, it is hard to predict the impact. I will not predict a recession just because Trump is elected, but I do think the economy would perform better under Clinton than Trump.

Also, the words of a President matter. Mr Trump has been reckless and irresponsible with his comments, and that would probably continue. One absurd comment could send the markets into a tailspin (and that could happen at any time). That should make investors more cautious (as an example, I'm recommending that my home builder friends ease back on their spec building if Trump is elected).

In conclusion: I expect Ms. Clinton to be elected and I'm currently taking no action to protect myself against the risks of a Trump presidency. The risks are real, but I think the odds of Trump winning are very low. If the unimaginable happens, I'll be writing about when to head to the bunker.

Saturday, October 29, 2016

October 2016: Unofficial Problem Bank list declines to 173 Institutions

by Calculated Risk on 10/29/2016 02:45:00 PM

This is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for October 2016.

Changes and comments from surferdude808:

Update on the Unofficial Problem Bank List for October 2016. During the month, the list fell from 177 institutions to 173 after five removals and one addition. Assets dropped by $562 million to an aggregate $54.9 billion. A year ago, the list held 264 institutions with assets of $79.2 billion.

Actions have been terminated against Horry County State Bank, Loris, SC ($383 million Ticker: HCFB) and Heritage Community Bank, Greeneville, TN ($89 million). Finding merger partners were Landmark Community Bank, National Association, Isanti, MN ($80 million); Citizens State Bank, Kingsland, GA ($56 million); and Home Savings Bank, Jefferson City, MO ($24 million). Added this month was The First National Bank of Lacon, Lacon, IL ($70 million).

In a change, the OCC released an update on its enforcement action activity today, the last Friday of the month. Historically, the OCC has issued its update on the first Friday following the 15th of the month. While the FDIC provides a release on the last Friday of the month as well; however, it only includes action changes for the preceding month, so their information has a longer lag time. Conversely, the Federal Reserve releases individual action changes as they occur instead of waiting to accumulate them in a monthly release.

Schedule for Week of Oct 30, 2016

by Calculated Risk on 10/29/2016 08:12:00 AM

The key report this week is the October employment report on Friday.

Other key indicators include the October ISM manufacturing and non-manufacturing indexes, October auto sales, and the September trade deficit.

The FOMC meets on Tuesday and Wednesday, and no change to policy is expected.

8:30 AM ET: Personal Income and Outlays for September. The consensus is for a 0.4% increase in personal income, and for a 0.5% increase in personal spending. And for the Core PCE price index to increase 0.1%.

9:45 AM: Chicago Purchasing Managers Index for October. The consensus is for a reading of 54.3, up from 54.2 in September.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for October. This is the last of the regional Fed surveys for October.

10:00 AM: ISM Manufacturing Index for October. The consensus is for the ISM to be at 51.6, up from 51.5 in September.

10:00 AM: ISM Manufacturing Index for October. The consensus is for the ISM to be at 51.6, up from 51.5 in September.Here is a long term graph of the ISM manufacturing index.

The ISM manufacturing index indicated expansion at 51.5% in September. The employment index was at 49.7%, and the new orders index was at 55.1%.

10:00 AM: Construction Spending for September. The consensus is for a 0.6% increase in construction spending.

All day: Light vehicle sales for October. The consensus is for light vehicle sales to decrease to 17.6 million SAAR in October, from 17.7 million in September (Seasonally Adjusted Annual Rate).

All day: Light vehicle sales for October. The consensus is for light vehicle sales to decrease to 17.6 million SAAR in October, from 17.7 million in September (Seasonally Adjusted Annual Rate).This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the September sales rate.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for October. This report is for private payrolls only (no government). The consensus is for 170,000 payroll jobs added in October, up from 154,000 added in September.

2:00 PM: FOMC Meeting Announcement. No change to policy is expected at this meeting.

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 255 thousand initial claims, down from 258 thousand the previous week.

10:00 AM: Manufacturers' Shipments, Inventories and Orders (Factory Orders) for September. The consensus is a 0.2% increase in orders.

10:00 AM: the ISM non-Manufacturing Index for October. The consensus is for index to decrease to 56.1 from 57.1 in August.

8:30 AM: Employment Report for October. The consensus is for an increase of 178,000 non-farm payroll jobs added in October, up from the 156,000 non-farm payroll jobs added in September.

The consensus is for the unemployment rate to decline to 4.9%.

This graph shows the year-over-year change in total non-farm employment since 1968.

This graph shows the year-over-year change in total non-farm employment since 1968.In September, the year-over-year change was 2.45 million jobs.

A key will be the change in wages.

8:30 AM: Trade Balance report for September from the Census Bureau.

8:30 AM: Trade Balance report for September from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through July. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is for the U.S. trade deficit to be at $38.9 billion in September from $40.7 billion in August.

Friday, October 28, 2016

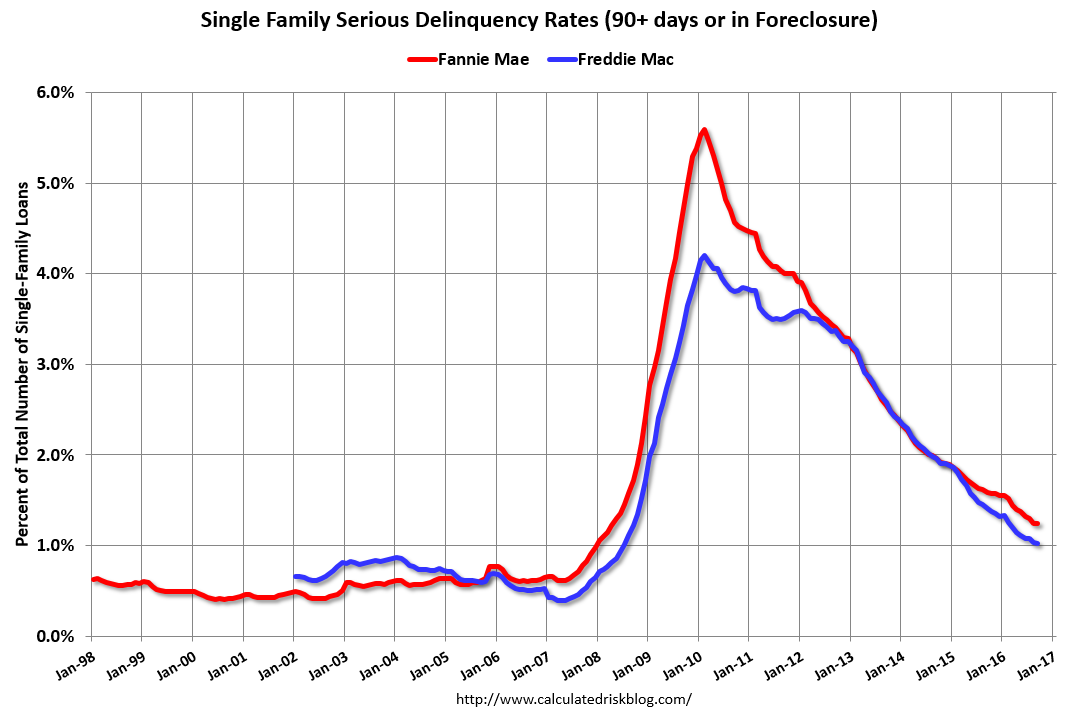

Fannie Mae: Mortgage Serious Delinquency rate unchanged in September

by Calculated Risk on 10/28/2016 05:04:00 PM

Fannie Mae reported today that the Single-Family Serious Delinquency rate was at 1.24% in September, unchanged from 1.24% in August. The serious delinquency rate is down from 1.59% in September 2015.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59%.

Click on graph for larger image

Click on graph for larger image

Although the rate is generally declining, the "normal" serious delinquency rate is under 1%.

The Fannie Mae serious delinquency rate has fallen 0.35 percentage points over the last year, and at that rate of improvement, the serious delinquency rate will not be below 1% for about 8 more months.

Note: Freddie Mac reported yesterday.

Q3 GDP: Investment

by Calculated Risk on 10/28/2016 02:05:00 PM

The graph below shows the contribution to GDP from residential investment, equipment and software, and nonresidential structures (3 quarter trailing average). This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

In the graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. So the usual pattern - both into and out of recessions is - red, green, blue.

The dashed gray line is the contribution from the change in private inventories.

Click on graph for larger image.

Click on graph for larger image.

Residential investment (RI) decreased at a 6.2% annual rate in Q3. Equipment investment decreased at a 2.7% annual rate, and investment in non-residential structures increased at a 5.4% annual rate.

On a 3 quarter trailing average basis, RI (red) is unchanged, equipment (green) is slightly negative, and nonresidential structures (blue) is slightly positive.

I'll post more on the components of non-residential investment once the supplemental data is released.

I expect investment to pick up going forward, and for the economy to grow at a steady pace.

The second graph shows residential investment as a percent of GDP.

Residential Investment as a percent of GDP has generally been increasing, but is only just above the bottom of the previous recessions - and I expect RI to continue to increase for the next few years.

I'll break down Residential Investment into components after the GDP details are released.

Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

The third graph shows non-residential investment in structures, equipment and "intellectual property products". Investment in equipment - as a percent of GDP - has declined a little recently.. Investment in nonresidential structures - as a percent of GDP - had been moving down due to less investment in energy and power, and is now moving sideways.

The third graph shows non-residential investment in structures, equipment and "intellectual property products". Investment in equipment - as a percent of GDP - has declined a little recently.. Investment in nonresidential structures - as a percent of GDP - had been moving down due to less investment in energy and power, and is now moving sideways.

Still no worries - residential investment will pickup (still very low), and non-residential will also pickup.