RSS Feed

RSS Feed by Calculated Risk on 5/14/2018 03:16:00 PM

Monday, May 14, 2018

LA area Port Traffic Increases YoY in April

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12 month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12 month basis, inbound traffic was up 0.2% compared to the rolling 12 months ending in March. Outbound traffic was up 1.0% compared to the rolling 12 months ending in March.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

In general imports have been increasing, and exports are mostly moving sideways recently.

Payroll Employment and Seasonal Factors

by Calculated Risk on 5/14/2018 11:26:00 AM

This might be a good time to review the seasonal pattern for employment.

Even in the best of years there are a significant number of jobs lost in the months of January and July. In 1994, when the economy added almost 3.9 million jobs, there were 2.25 million lost in January 1994 (not seasonally adjusted, NSA), and almost 1 million payroll jobs lost in July of that year.

This year, in January 2018, 3.1 million total jobs were lost (NSA). And in April 2018 (last month), almost 1 million jobs were added (NSA). On a seasonally adjusted basis, the BLS reported 176 thousand jobs (SA) added in January, and 164 thousand added in April.

A clear example of the a seasonal pattern is that teachers leave the workforce every year in July. And then those teachers return to the payrolls in September and early October. Since this happens every year, the BLS applies a seasonal adjustment before reporting the headline number.

For the private sector, there are always a large number of jobs lost in January (retailers and others cutting jobs) and in September (summer hires let go).

Click on graph for larger image.

Click on graph for larger image.

This graph shows the seasonal pattern since 2002 for both total nonfarm jobs and private sector only payroll jobs. Notice the large spike down every January.

Also notice the spike down in July (red) that is related to teachers leaving the labor force.

The key point is this is a series that NEEDS a seasonal adjustment. There is significant, but predictable, seasonal variation in employment.

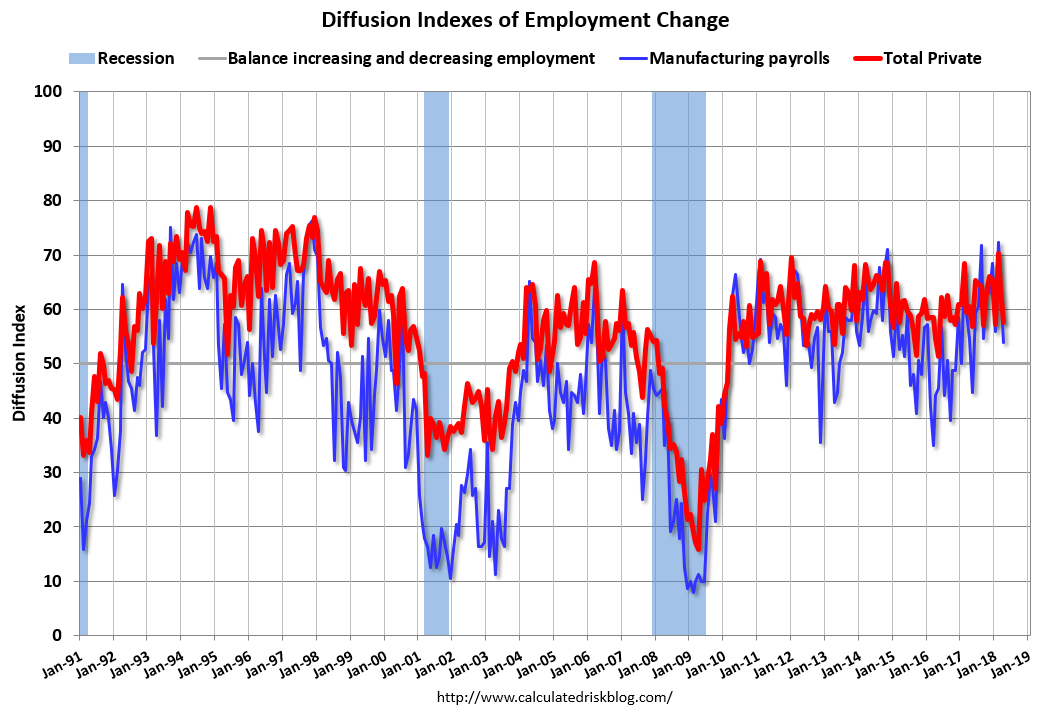

Employment: April Diffusion Indexes

by Calculated Risk on 5/14/2018 09:03:00 AM

I haven't posted this in a few months.

The BLS diffusion index for total private employment was at 57.6 in April, down from 64.1 in March.

For manufacturing, the diffusion index was at 53.9, down from 64.5 in March.

Think of this as a measure of how widespread job gains are across industries. The further from 50 (above or below), the more widespread the job losses or gains reported by the BLS. Above 60 is very good. From the BLS:

Figures are the percent of industries with employment increasing plus one-half of the industries with unchanged employment, where 50 percent indicates an equal balance between industries with increasing and decreasing employment.

Overall both total private and manufacturing job growth was less widespread in April compared to the previous two months.

Overall both total private and manufacturing job growth was less widespread in April compared to the previous two months.

Sunday, May 13, 2018

Sunday Night Futures

by Calculated Risk on 5/13/2018 07:16:00 PM

Weekend:

• Schedule for Week of May 13, 2018

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures: S&P 500 are up 7, and DOW futures are up 71 (fair value).

Oil prices were up over the last week with WTI futures at $70.65 per barrel and Brent at $77.07 per barrel. A year ago, WTI was at $46, and Brent was at $47 - so oil prices are up about 50%+ year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.87 per gallon. A year ago prices were at $2.32 per gallon - so gasoline prices are up 55 cents per gallon year-over-year.

Goldman: "Environment for investors is less pleasant than last year"

by Calculated Risk on 5/13/2018 08:01:00 AM

A brief excerpts from a research note by Goldman Sachs chief economist Jan Hatzius:

"The environment for investors is less pleasant than last year. Although growth is strong, corporate earnings have been on a tear, and both inflation and interest rates remain historically low, all of these tailwinds are abating at the margin. Perhaps more fundamentally, if financial conditions need to tighten to limit the overshoot of full employment, this is likely to mean a downward price adjustment for a weighted average of government bonds, corporate credit, and equities. Effectively, the overall size of the pie is set to shrink, and in that environment it will get harder to generate good risk-adjusted returns for all but the savviest investors."

emphasis added

Saturday, May 12, 2018

Schedule for Week of May 13, 2018

by Calculated Risk on 5/12/2018 08:11:00 AM

The key economic reports this week are April Housing Starts and Retail Sales.

For manufacturing, April industrial production, and the May New York, and Philly Fed manufacturing surveys, will be released this week.

No major economic releases scheduled.

8:30 AM ET: Retail sales for April will be released. The consensus is for a 0.3% increase in retail sales.

8:30 AM ET: Retail sales for April will be released. The consensus is for a 0.3% increase in retail sales.This graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993. Retail and Food service sales, ex-gasoline, increased by 4.2% on a YoY basis.

8:30 AM ET: The New York Fed Empire State manufacturing survey for May. The consensus is for a reading of 15.5, down from 15.8.

10:00 AM: The May NAHB homebuilder survey. The consensus is for a reading of 70, up from 69 in April. Any number above 50 indicates that more builders view sales conditions as good than poor.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Housing Starts for April.

8:30 AM: Housing Starts for April. This graph shows single and total housing starts since 1968.

The consensus is for 1.325 million SAAR, up from 1.319 million SAAR in March.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for April.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for April.This graph shows industrial production since 1967.

The consensus is for a 0.6% increase in Industrial Production, and for Capacity Utilization to decrease to 78.4%.

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 217 thousand initial claims, up from 211 thousand the previous week.

8:30 AM: the Philly Fed manufacturing survey for May. The consensus is for a reading of 22.0, down from 23.2.

11:00 AM: The New York Fed will release their Q1 2018 Household Debt and Credit Report

10:00 AM: State Employment and Unemployment (Monthly) for April 2018

Friday, May 11, 2018

Oil Rigs: "Rig additions keep rolling along"

by Calculated Risk on 5/11/2018 06:32:00 PM

A few comments from Steven Kopits of Princeton Energy Advisors LLC on May 11, 2018:

• Total US oil rigs were up, +10 to 844

• Horizontal oil rigs, however, were only up +2 at 745

...

• Oil rig additions came in the neglected ‘directional’ category, but only represented the recovery off rigs taken off line last week

• With the Brent spread over $6 / barrel, the end of the Iran deal, and a general sense of bullishness around oil markets, expect rig count additions to accelerate

Click on graph for larger image.

Click on graph for larger image.CR note: This graph shows the US horizontal rig count by basin.

Graph and comments Courtesy of Steven Kopits of Princeton Energy Advisors LLC.

The Projected Improvement in Life Expectancy

by Calculated Risk on 5/11/2018 04:07:00 PM

Here is something different, but it is important when looking at demographics ...

The following data is from the CDC United States Life Tables, 2014 by Elizabeth Arias.

In 2014, the overall expectation of life at birth was 78.9 years, a 0.1-year increase from 2013. Between 2013 and 2014, life expectancy at birth increased by 0.1 year for both males (76.4 to 76.5) and females (81.2 to 81.3) and for the black (75.5 to 75.6) and white (79.0 to 79.1) populations. Life expectancy at birth increased by 0.2 years for the Hispanic (81.9 to 82.1) and non-Hispanic black (75.1 to 75.3) populations. Life expectancy at birth remained unchanged for the non-Hispanic white population (78.8).Instead of look at life expectancy, here is a graph of survivors out of 100,000 born alive, by age for three groups: those born in 1900-1902, born in 1949-1951 (baby boomers), and born in 2014.

...

[The following] summarizes the number of survivors out of 100,000 persons born alive by age, race, Hispanic origin, and sex for 2014. ... In 2014, 99.4% of all infants born in the United States survived the first year of life. In contrast, only 87.6% of infants born in 1900 survived the first year. Of the 2014 period life table cohort, 58.1% survived to age 80 and 2.1% survived to age 100. In 1900, 13.5% of the life table cohort survived to age 80 and only 0.03% survived to age 100

emphasis added

Click on graph for larger image.

Click on graph for larger image.There was a dramatic change between those born in 1900 (blue) and those born mid-century (orange). The risk of infant and early childhood deaths dropped sharply, and the risk of death in the prime working years also declined significantly.

The CDC is projecting further improvement for childhood and prime working age for those born in 2014, but they are also projecting that people will live longer.

The second graph uses the same data but looks at the number of people who die before a certain age, but after the previous age. As an example, for those born in 1900 (blue), 12,448 of the 100,000 born alive died before age 1, and another 5,748 died between age 1 and age 5.

The second graph uses the same data but looks at the number of people who die before a certain age, but after the previous age. As an example, for those born in 1900 (blue), 12,448 of the 100,000 born alive died before age 1, and another 5,748 died between age 1 and age 5.The peak age for deaths didn't change much for those born in 1900 and 1950 (between 76 and 80, but many more people born in 1950 will make it).

Now the CDC is projection the peak age for deaths - for those born in 2014 - will increase to 86 to 90! Using these stats - for those born this year (in 2018) - more than two-thirds will make it to the next century.

Also the number of deaths for those younger than 20 will be very small (down to mostly accidents, guns, and drugs). Self-driving cars might reduce the accident components of young deaths.

An amazing statistic: for those born in 1900, about 13 out of 100,000 made it to 100. For those born in 1950, 199 are projected to make to 100 - a significant increase. Now the CDC is projecting that 2,111 out of 100,000 born in 2014 will make it to 100. Stunning!

Some people look at this data and worry about supporting all these old people. To me, this is all great news - the vast majority of people can look forward to a long life - with fewer people dying in childhood or during their prime working years.

Early Q2 GDP Forecasts

by Calculated Risk on 5/11/2018 11:19:00 AM

From Merrill Lynch:

Downward revisions to inventories this week leaves 1Q GDP tracking a tenth lower to 2.2% for 1Q GDP. We are tracking 3.2% for 2Q. [May 11 estimate].And from the Altanta Fed: GDPNow

emphasis added

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2018 is 4.0 percent on May 9, unchanged from May 3. [May 9 estimate]From the NY Fed Nowcasting Report

The New York Fed Staff Nowcast stands at 3.0% for 2018:Q2. [May 11 estimate]CR Note: These early estimates suggest real annualized GDP in the 3% to 4% in Q2.

Merrill: "Retail spending stalls again"

by Calculated Risk on 5/11/2018 09:25:00 AM

A few excerpts from a Merrill Lynch research note: Retail spending stalls again

According to BAC aggregated credit and debit card data, retail sales ex-autos declined 0.1% mom seasonally adjusted in April. This suggests that the better momentum in consumer spending seen in March failed to carry over to start the second quarter. We saw two headwinds for the consumer in April: weather and higher gasoline prices.CR Note: Retail sales for April are scheduled to be released on Tuesday, May 15th. The consensus is retail sales increased 0.3% in April.

We find evidence that unseasonably cold weather conditions likely played a role in holding back consumer activity. Specifically, the Midwest and the Northeast experienced below average temperatures ...

Higher gasoline prices also likely dampened overall consumer spending. According to the Energy Information Administration, retail gasoline prices jumped 6.4% mom in April as crude oil prices rose on negative supply shock and solid global demand. This led to a surge in spend at gasoline stations and a shift away from other categories. ...

...

Bottom line: Retail spending softened in April. The weather impact should prove temporary but rising gasoline prices is likely to persist, eating away some of the positive impact from higher after-tax wages seen post tax reform.