RSS Feed

RSS Feed by Calculated Risk on 8/07/2019 10:42:00 AM

Wednesday, August 07, 2019

Las Vegas Real Estate in July: Sales down 2% YoY, Inventory up 71% YoY

This is a key former distressed market to follow since Las Vegas saw the largest price decline, following the housing bubble, of any of the Case-Shiller composite 20 cities.

The Greater Las Vegas Association of Realtors reported Local home prices still higher than one year ago, but not by much, GLVAR housing statistics for July 2019

Local home prices continue to be higher than they were a year ago, but not by much. So says a report released Wednesday by the Greater Las Vegas Association of REALTORS® (GLVAR).1) Overall sales were down 1.8% year-over-year to 3,883 in July 2019 from 3,955 in July 2018.

...

The total number of existing local homes, condos and townhomes sold during July was 3,883. Compared to one year ago, July sales were down 0.8% for homes and down 5.9% for condos and townhomes.

...

By the end of July, GLVAR reported 7,808 single-family homes listed for sale without any sort of offer. That’s up 63.1% from one year ago. For condos and townhomes, the 1,864 properties listed without offers in July represented a 112.3% jump from one year ago.

While the local housing supply is up from one year ago, Carpenter said it’s still below what would normally be considered a balanced market. At the current sales pace, she said Southern Nevada still has less than a three-month supply of homes available for sale.

...

The number of so-called distressed sales remains near historically low levels. GLVAR reported that short sales and foreclosures combined accounted for just 2.0% of all existing local property sales in July. That compares to 2.9% of all sales one year ago and 6.4% two years ago.

emphasis added

2) Active inventory (single-family and condos) is up sharply from a year ago, from a total of 5,665 in July 2018 to 9,752 in July 2019. Note: Total inventory was up 71% year-over-year. This is a significant increase in inventory, although months-of-supply is still somewhat low.

3) Low level of distressed sales.

MBA: Mortgage Applications Increased in Latest Weekly Survey

by Calculated Risk on 8/07/2019 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 5.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 2, 2019.

... The Refinance Index increased 12 percent from the previous week and was 116 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 7 percent higher than the same week one year ago.

...

“The Federal Reserve cut rates as expected last week, but the bigger influence on the financial markets was the beginning of a trade war with China. The result was a sharp drop in mortgage rates, which will likely draw many refinance borrowers into the market in the coming weeks,” said Mike Fratantoni, MBA Senior Vice President and Chief Economist. “The 30-year fixed rate mortgage fell to its lowest level since November 2016, and the drop resulted in an almost 12 percent increase in refinance application volume, bringing the index to a reading over 2,000 – its highest over the same time period. We fully expect that refinance volume will jump even higher this week given the further drop in rates.”

Added Fratantoni, “Lower mortgage rates did not pull more homebuyers into the market, as purchase volume slipped a bit last week, but still remains around 7 percent ahead of last year’s pace.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($484,350 or less) decreased to 4.01 percent from 4.08 percent, with points increasing to 0.37 from 0.34 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

Mortgage rates have declined from close to 5% late last year to around 3.6% this week (expect a further drop in rates in the MBA survey next week).

We should see a further increase in refinance activity next week.

The second graph shows the MBA mortgage purchase index

The second graph shows the MBA mortgage purchase indexAccording to the MBA, purchase activity is up 7% year-over-year.

Tuesday, August 06, 2019

Summer Teen Employment

by Calculated Risk on 8/06/2019 01:13:00 PM

Here is a look at the change in teen employment over time.

The graph below shows the participation rate and employment-population ratio for those 16 to 19 years old.

The graph is Not Seasonally Adjusted (NSA), to show the seasonal hiring of teenagers during the summer.

A few observations:

1) Although teen employment has recovered some since the great recession, overall teen employment had been trending down. This is probably because more people are staying in school (a long term positive for the economy).

Click on graph for larger image.

Click on graph for larger image.

2) A smaller percentage of teenagers are seeking summer employment. The seasonal spikes are smaller than in previous decades. So a smaller percentage of teenagers are joining the labor force during the summer as compared to previous years. This could be because of fewer employment opportunities, or because teenagers are pursuing other activities during the summer.

3) The decline in teenager participation is one of the reasons the overall participation rate has declined (of course, the retiring baby boomers is the main reason the overall participation rate has declined over the last 20 years).

BLS: Job Openings "Little Changed" at 7.3 Million in June

by Calculated Risk on 8/06/2019 10:06:00 AM

Notes: In June there were 7.348 million job openings, and, according to the June Employment report, there were 5.975 million unemployed. So, for the sixteenth consecutive month, there were more job openings than people unemployed. Also note that the number of job openings has exceeded the number of hires since January 2015 (over 4 years).

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings was little changed at 7.3 million on the last business day of June, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.7 million and 5.5 million, respectively. ...The following graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

The number of quits was little changed in June at 3.4 million. The quits rate was 2.3 percent. The quits level was little changed for total private and decreased for government (-19,000).

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for June, the most recent employment report was for July.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

Jobs openings decreased in June to 7.348 million from 7.384 million in May.

The number of job openings (yellow) are down 1% year-over-year.

Quits are up 2% year-over-year. These are voluntary separations. (see light blue columns at bottom of graph for trend for "quits").

Job openings remain at a high level, and quits are still increasing year-over-year. This was a solid report.

CoreLogic: House Prices up 3.4% Year-over-year in June

by Calculated Risk on 8/06/2019 09:19:00 AM

Notes: This CoreLogic House Price Index report is for June. The recent Case-Shiller index release was for May. The CoreLogic HPI is a three month weighted average and is not seasonally adjusted (NSA).

From CoreLogic: U.S. Home Price Insights Through June 2019 with Forecasts from July 2019

Home prices nationwide, including distressed sales, increased year over year by 3.4% in June 2019 compared with June 2018 and increased month over month by 0.4% in June 2019 compared with May 2019 (revisions with public records data are standard, and to ensure accuracy, CoreLogic incorporates the newly released public data to provide updated results).CR Note: The CoreLogic YoY increase had been in the 5% to 7% range for several years, before slowing last year.

The CoreLogic HPI Forecast indicates that home prices will increase by 5.2% on a year-over-year basis from June 2019 to June 2020. On a month-over-month basis, home prices are expected to increase by 0.5% from June 2019 to July 2019.

“Tepid home sales have caused home prices to rise at the slowest pace for the first half of a year since 2011. Price growth continues to be faster for lower-priced homes, as first-time buyers and investors are both actively seeking entry-level homes. With incomes up and current mortgage rates about 0.8 percentage points below what they were one year ago, home sales should have a better sales pace in the second half of 2019 than a year earlier, leading to a quickening in price growth over the next year.”, Dr. Frank Nothaft, Chief Economist for CoreLogic

emphasis added

The year-over-year comparison has been positive for more than seven years since turning positive year-over-year in February 2012.

Monday, August 05, 2019

Tuesday: Job Openings

by Calculated Risk on 8/05/2019 09:39:00 PM

Tuesday:

• At 10:00 AM ET: Job Openings and Labor Turnover Survey for June from the BLS. Jobs openings decreased in May to 7.323 million from 7.372 million in April.

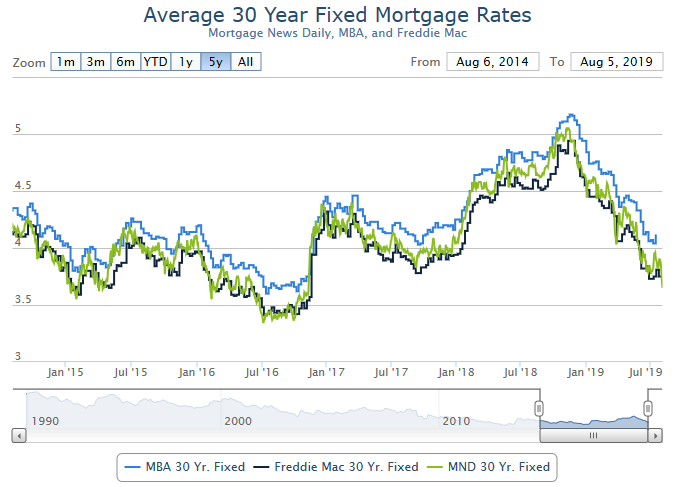

Mortgage Rates Fall Sharply, 3.5% 30 Year Fixed

by Calculated Risk on 8/05/2019 05:13:00 PM

From Matthew Graham at MortgageNewsDaily: Just When You Thought Rates Wouldn't Go Any Lower

Mortgage rates were already in great shape on Friday after having fallen to the lowest levels since November 2016. Rather than draw inspiration from the week's big ticket events (Fed announcement and jobs report), the biggest source of inspiration was a flare-up in trade tensions following Trump's announcement of new tariffs on Chinese imports. Trade war drama flared over the weekend as China's central bank set the country's currency at the weakest levels in more than a decade.

…

Mortgage-backed securities (MBS)--the bonds that directly influence mortgage rates--have a hard time keeping up when financial markets are this volatile. Mortgage lenders also tend to proceed cautiously when dropping rates to multi-year lows in the midst of a these sorts of big market swings. That means mortgage rates haven't dropped nearly as quickly as Treasury yields, but they're nonetheless at the lowest levels since November 2016 today. [30YR FIXED - 3.5% - 3.75% (wider range than normal due to volatility)]

Click on graph for larger image.

Click on graph for larger image.This graph from Mortgage News Daily shows mortgage rates since 2014.

This graph is interactive, and you could view mortgage rates back to the mid-1980s - click here for graph.

Update: Framing Lumber Prices Down 20% Year-over-year

by Calculated Risk on 8/05/2019 02:34:00 PM

Here is another monthly update on framing lumber prices. Lumber prices declined from the record highs in early 2018, and are now down 15% to 25% year-over-year.

This graph shows two measures of lumber prices: 1) Framing Lumber from Random Lengths through Aug 2, 2019 (via NAHB), and 2) CME framing futures.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

Right now Random Lengths prices are down 25% from a year ago, and CME futures are down 15% year-over-year.

There is a seasonal pattern for lumber prices, and usually prices will increase in the Spring, and peak around May, and then bottom around October or November - although there is quite a bit of seasonal variability.

The trade war is a factor with reports that lumber exports to China have declined by 40% since last September.

CalculatedRisk Speaks! "2020 Economic Forecast featuring the UCI Paul Merage School of Business"

by Calculated Risk on 8/05/2019 11:45:00 AM

On October 23rd, I will be one of three speakers at the "2020 Economic Forecast featuring the UCI Paul Merage School of Business" in Newport Beach, California, sponsored by the Newport Beach Chamber of Commerce.

UCI Finance Professor Christopher Schwarz and I will be discussing the 2020 economic outlook, and Dr. Richard Afable will be discussing "The Future of the Healthcare System".

This is a lunch time event (from 11:15 am to 1:30 pm) at the Balboa Bay Resort.

Click here for more information and tickets. Tickets are $65 for members, and $75 for non-members and includes lunch. (I'm speaking for free).

Best to all.

ISM Non-Manufacturing Index decreased to 53.7% in July

by Calculated Risk on 8/05/2019 10:07:00 AM

The July ISM Non-manufacturing index was at 53.7%, down from 55.1% in June. The employment index increased to 56.2%, from 55.0%. Note: Above 50 indicates expansion, below 50 contraction.

From the Institute for Supply Management: July 2019 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in July for the 114th consecutive month, say the nation’s purchasing and supply executives in the latest Non-Manufacturing ISM® Report On Business®.

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management® (ISM®) Non-Manufacturing Business Survey Committee: “The NMI® registered 53.7 percent, which is 1.4 percentage points lower than the June reading of 55.1 percent. This represents continued growth in the non-manufacturing sector, at a slower rate. This is the index’s lowest reading since August 2016, when it registered 51.8 percent. The Non-Manufacturing Business Activity Index decreased to 53.1 percent, 5.1 percentage points lower than the June reading of 58.2 percent, reflecting growth for the 120th consecutive month. The New Orders Index registered 54.1 percent; 1.7 percentage points lower than the reading of 55.8 percent in June. The Employment Index increased 1.2 percentage points in July to 56.2 percent from the June reading of 55 percent. The Prices Index decreased 2.4 percentage points from the June reading of 58.9 percent to 56.5 percent, indicating that prices increased in July for the 26th consecutive month. According to the NMI®, 13 non-manufacturing industries reported growth. The non-manufacturing sector’s rate of growth continued to cool off. Respondents indicated ongoing concerns related to tariffs and employment resources. Comments remained mixed about business conditions and the overall economy.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This suggests slower expansion in July than in June.