RSS Feed

RSS Feed by Calculated Risk on 3/16/2021 09:00:00 PM

Tuesday, March 16, 2021

Wednesday: Housing Starts, FOMC Announcement, Forecasts, and Press Conference

See my FOMC Preview

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, Housing Starts for February. The consensus is for 1.570 million SAAR, down from 1.580 million SAAR.

• At 2:00 PM, FOMC Meeting Announcement. No change to policy is expected at this meeting.

• At 2:00 PM, FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

• At 2:30 PM, Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

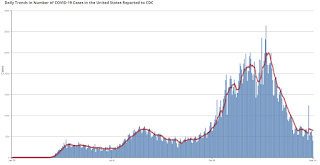

March 16 COVID-19 Test Results and Vaccinations

by Calculated Risk on 3/16/2021 04:17:00 PM

From Bloomberg on vaccinations as of Mar 16th:

"So far, 111 million doses have been given. In the last week, an average of 2.44 million doses per day were administered."Here is the CDC COVID Data Tracker. This site has data on vaccinations, cases and more.

And check out COVID Act Now to see how each state is doing. (updated link to new site)

There have been almost 21,000 US deaths reported in March due to COVID.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 54,239, well above the low following the summer surge of 35,000.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 34,636 well above the post-summer surge low of 23,000.

Phoenix Real Estate in February: Sales Up 5% YoY, Active Inventory Down 61% YoY

by Calculated Risk on 3/16/2021 02:07:00 PM

The Arizona Regional Multiple Listing Service (ARMLS) reports ("Stats Report"):

1) Overall sales were at 7,659 in February, up 5.2% from 7,279 in February 2020.

2) Active inventory was at 4,144, down 60.9% from 10,590 in February 2020.

3) Months of supply decreased to 1.14 in February from 2.14 in February 2020. This is very low.

Sales are reported at the close of escrow, so these sales were mostly signed in December and January.

CAR on California February Housing: Sales up 10% YoY, Active Listings down 53% YoY

by Calculated Risk on 3/16/2021 11:34:00 AM

California home sales moderated in February as mortgage rates spiked in recent weeks, while tight housing supply continued to constrain demand, especially in more affordable markets, the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) said today.CR Note: Existing home sales are reported when the transaction closes, so this was mostly for contracts signed in December and January.

Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 462,720 in February, according to information collected by C.A.R. from more than 90 local REALTOR® associations and MLSs statewide. The statewide annualized sales figure represents what would be the total number of homes sold during 2021 if sales maintained the February pace throughout the year. It is adjusted to account for seasonal factors that typically influence home sales.

February home sales decreased 4.5 percent from 484,760 in January and were up 9.7 percent from a year ago, when 421,670 homes were sold on an annualized basis. While still solid, the nearly 10 percent sales increase was the smallest gain in the past seven months.

...

“The housing market has been cruising at a robust pace since the second half of 2020 but has encountered some speedbumps recently as rates began to rise,” said C.A.R. President Dave Walsh, vice president and manager of the Compass San Jose office. “While higher rates may slow growth in home sales temporarily, the major roadblock in the long run is a shortage of homes for sale. With inventory dropping more than a half from a year ago, the market will soften in the second half of 2021 if we don’t see enough homes come on the market to meet demand.”

...

The Unsold Inventory Index (UII) inched up from 1.9 months in January to 2.0 months in February but dropped sharply from a year ago, when there was 3.6 months of housing inventory. The index indicates the number of months it would take to sell the supply of homes on the market at the current rate of sales.

Active listings fell 52.5 percent in February from last year and continued to drop more than 40 percent on a year-over-year basis for the eighth consecutive month. On a month-to-month basis, for-sale properties inched up slightly by 0.4 percent in February and should climb further in the coming months as the market prepares for the spring homebuying season and the pandemic situation continues to improve.

emphasis added

NAHB: Builder Confidence Decreased to 82 in March

by Calculated Risk on 3/16/2021 10:06:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 82, down from 84 in February. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Higher Material Costs, Interest Rates Lower Builder Sentiment

Despite high buyer traffic and strong demand, builder sentiment fell in March as rising lumber and other material prices pushed builder confidence lower. The latest National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) shows that builder confidence in the market for newly built single-family homes fell two points to 82 in March.

Though builders continue to see strong buyer traffic, recent increases for material costs and delivery times, particularly for softwood lumber, have depressed builder sentiment this month. Supply shortages and high demand have caused lumber prices to jump about 200 percent since last April.

Builder confidence peaked at a level of 90 last November and has trended lower as supply-side and demand-side factors have trimmed housing affordability. While single-family home building should grow this year, the elevated price of lumber is adding approximately $24,000 to the price of a new home. And mortgage interest rates, while historically low, have increased about 30 basis points over the last month. Nonetheless, the lack of resale inventory means new construction is the only option for some prospective home buyers.

...

The HMI index gauging current sales conditions fell three points to 87 while the component measuring sales expectations in the next six months increased three points to 83. The gauge charting traffic of prospective buyers held firm at 72.

Looking at the three-month moving averages for regional HMI scores, the Northeast rose two points to 80, the Midwest fell one point to 80, the South dropped two points to 82 and the West posted a three-point loss to 90.

Click on graph for larger image.

Click on graph for larger image.This graph show the NAHB index since Jan 1985.

This was slightly below the consensus forecast, but still a very strong reading.

Housing and homebuilding have been one of the best performing sectors during the pandemic.

Industrial Production Decreased 2.2 Percent in February

by Calculated Risk on 3/16/2021 09:22:00 AM

From the Fed: Industrial Production and Capacity Utilization

In February, total industrial production decreased 2.2 percent. Manufacturing output and mining production fell 3.1 percent and 5.4 percent, respectively; the output of utilities increased 7.4 percent.

The severe winter weather in the south central region of the country in mid-February accounted for the bulk of the declines in output for the month. Most notably, some petroleum refineries, petrochemical facilities, and plastic resin plants suffered damage from the deep freeze and were offline for the rest of the month. Excluding the effects of the winter weather would have resulted in an index for manufacturing that fell about 1/2 percent and in an index for mining that rose about 1/2 percent. Both indexes would have remained below their pre-pandemic (February 2020) levels.

At 104.7 percent of its 2012 average, total industrial production in February was 4.2 percent lower than its year-earlier level. Capacity utilization for the industrial sector decreased 1.7 percentage points in February to 73.8 percent, a rate that is 5.8 percentage points below its long-run (1972–2020) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April, but still below the level in February 2020.

Capacity utilization at 73.8% is 5.8% below the average from 1972 to 2020.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production decreased in February to 104.7. This is 4.2% below the February 2020 level.

The change in industrial production was below consensus expectations.

Retail Sales Decreased 3.0% in February

by Calculated Risk on 3/16/2021 08:39:00 AM

On a monthly basis, retail sales decreased 3.0 percent from January to February (seasonally adjusted), and sales were up 6.3 percent from February 2020.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for February 2021, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $561.7 billion, a decrease of 3.0 percent from the previous month, and 6.3 percent above February 2020.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were down 3.5% in February.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 7.0% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 7.0% on a YoY basis.Sales in February were well below expectations, however sales in January were revised up.

Monday, March 15, 2021

Tuesday: Retail Sales, Industrial Production, Homebuilder Survey

by Calculated Risk on 3/15/2021 09:12:00 PM

From Matthew Graham at Mortgage News Daily: MBS RECAP: Fighting Good Fight, Waiting on Fed Day

Coming off a fairly rough Friday at the end of last week, it's mildly reassuring to begin the new week with no additional damage. ... The takeaway is simple: it's a rising rate environment until proven otherwise. If one event has the power to change the trading tone in bonds this week, it's Wednesday's Fed Announcement [30 year fixed 3.33%]Tuesday:

emphasis added

• At 8:30 AM ET, Retail sales for February is scheduled to be released. The consensus is for a 0.5% decrease in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for February. The consensus is for a 0.6% increase in Industrial Production, and for Capacity Utilization to increase to 75.8%.

• At 10:00 AM, The March NAHB homebuilder survey. The consensus is for a reading of 83, down from 84. Any number above 50 indicates that more builders view sales conditions as good than poor.

March 15 COVID-19 Test Results and Vaccinations

by Calculated Risk on 3/15/2021 06:52:00 PM

From Bloomberg on vaccinations as of Mar 15th:

"So far, 109 million doses have been given. In the last week, an average of 2.43 million doses per day were administered."Here is the CDC COVID Data Tracker. This site has data on vaccinations, cases and more.

And check out COVID Act Now to see how each state is doing. (updated link to new site)

There have been over 20,000 US deaths reported in March due to COVID.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 64,867, well above the low following the summer surge of 35,000.

Note that last week, Missouri reported 81,000 previously unreported cases, and that caused the spike in total cases (and an increase in 7 day average).

Note that last week, Missouri reported 81,000 previously unreported cases, and that caused the spike in total cases (and an increase in 7 day average).

MBA Survey: "Share of Mortgage Loans in Forbearance Decreases to 5.14%"

by Calculated Risk on 3/15/2021 04:00:00 PM

Note: This is as of March 7th.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 5.14%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 6 basis points from 5.20% of servicers’ portfolio volume in the prior week to 5.14% as of March 7, 2021. According to MBA’s estimate, 2.6 million homeowners are in forbearance plans.

...

“One year after the onset of the pandemic, many homeowners are approaching 12 months in their forbearance plan. That is likely why call volume to servicers picked up in the prior week to the highest level since last April, and forbearance exits increased to their highest level since January. With new forbearance requests unchanged, the share of loans in forbearance decreased again,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “Homeowners with federally backed loans have access to up to 18 months of forbearance, but they need to contact their servicer to receive this additional relief.”

Fratantoni added, “The American Rescue Plan provides needed support for homeowners who are continuing to struggle during these challenging times, and stimulus payments are being delivered to households now. We anticipate that this support, along with the improving job market, will help many homeowners to get back on their feet.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April, then trended down - and has mostly moved slowly down recently.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) remained the same relative to the prior two weeks at 0.07%."