RSS Feed

RSS Feed by Calculated Risk on 4/30/2021 08:36:00 AM

Friday, April 30, 2021

Personal Income increased 21.1% in March, Spending increased 4.2%

The BEA released the Personal Income and Outlays report for March:

Personal income increased $4.21 trillion (21.1 percent) in March according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $4.18 trillion (23.6 percent) and personal consumption expenditures (PCE) increased $616.0 billion (4.2 percent).The March PCE price index increased 2.3 percent year-over-year and the March PCE price index, excluding food and energy, increased 1.8 percent year-over-year.

Real DPI increased 23.0 percent in March and Real PCE increased 3.6 percent; goods increased 7.3 percent and services increased 1.7 percent. The PCE price index increased 0.5 percent. Excluding food and energy, the PCE price index increased 0.4 percent .

emphasis added

The following graph shows real Personal Consumption Expenditures (PCE) through March 2021 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income was slightly above expectations (boosted by American Rescue Act), and the increase in PCE was at expectations.

Thursday, April 29, 2021

Friday: Personal Income and Outlays

by Calculated Risk on 4/29/2021 09:00:00 PM

Friday:

• At 8:30 AM ET, Personal Income and Outlays, March 2021. The consensus is for a 20.1% increase in personal income, and for a 4.2% increase in personal spending. And for the Core PCE price index to increase 0.3%.

• At 9:45 AM, Chicago Purchasing Managers Index for April.

• At 10:00 AM, University of Michigan's Consumer sentiment index (Final for April). The consensus is for a reading of 87.5.

Freddie Mac: Mortgage Serious Delinquency Rate decreased in March

by Calculated Risk on 4/29/2021 05:51:00 PM

Freddie Mac reported that the Single-Family serious delinquency rate in March was 2.34%, down from 2.52% in February. Freddie's rate is up from 0.60% in March 2020.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble, and peaked at 3.17% in August 2020 during the pandemic.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image

Click on graph for larger image

Mortgages in forbearance are being counted as delinquent in this monthly report, but they will not be reported to the credit bureaus.

This is very different from the increase in delinquencies following the housing bubble. Lending standards have been fairly solid over the last decade, and most of these homeowners have equity in their homes - and they will be able to restructure their loans once (if) they are employed.

Also - for multifamily - delinquencies were at 0.17%, up from 0.14% in February, and up more than double from 0.08% in March 2020.

April 29th COVID-19 Vaccinations, New Cases, Hospitalizations; Lowest 7-Day Average New Cases Since October 2020

by Calculated Risk on 4/29/2021 03:49:00 PM

Note: I'm looking forward to not posting this daily! I've been posting this data daily for over a year, and I'll stop once all three of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine, and

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000.

According to the CDC, 237.4 million doses have been administered. 38.4% of the population over 18 is fully vaccinated, and 54.9% of the population over 18 has had at least one dose (141.8 million people over 18 have had at least one dose).

And check out COVID Act Now to see how each state is doing.

Over 18,500 US deaths were reported so far in April due to COVID.

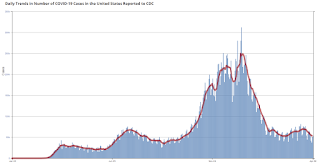

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

Note: The ups and downs during the Winter surge were related to reporting delays due to the Thanksgiving and Christmas holidays.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

Note: The ups and downs during the Winter surge were related to reporting delays due to the Thanksgiving and Christmas holidays.

This data is from the CDC.

The 7-day average is 52,528, down from 54,010 yesterday, and down from the recent peak of 69,881 on April 13, 2021. This is the lowest since October 12, 2020, but well above the post-summer surge low of 34,668.

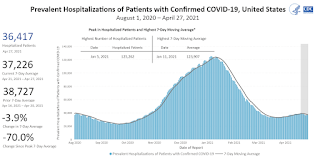

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 37,226, down from 37,606 reported yesterday, and well above the post-summer surge low of 23,000.

Hotels: Occupancy Rate Down 17% Compared to Same Week in 2019

by Calculated Risk on 4/29/2021 01:02:00 PM

Note: The year-over-year occupancy comparisons are easy, since occupancy declined sharply at the onset of the pandemic. However, occupancy is still down significantly from normal levels.

The occupancy rate is down 17% compared to the same week in 2019.

From CoStar: STR: US Weekly Hotel Occupancy Flat From Prior Week

U.S. weekly hotel occupancy remained flat from the previous week, according to STR‘s latest data through April 24.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

April 18-24, 2021:

• Occupancy: 57.3%

• Average daily rate (ADR): US$108.10

• Revenue per available room (RevPAR): US$61.93

Overall industry occupancy will likely remain plateaued until the summer leisure travel boom, but there has been noticeable uptick in weekday occupancy, which is indicative of increased business travel. ADR was up slightly from the previous week, and the Luxury, Midscale and Economy classes have each recovered more than 90% of their 2019 ADR levels.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2021, black is 2020, blue is the median, and dashed light blue is for 2009 (the worst year on record for hotels prior to 2020).

Occupancy is now slightly above the horrible 2009 levels.

Note: Y-axis doesn't start at zero to better show the seasonal change.

Note: Y-axis doesn't start at zero to better show the seasonal change.

A Few Comments on Q1 GDP

by Calculated Risk on 4/29/2021 11:36:00 AM

Earlier from the BEA: Gross Domestic Product, First Quarter 2021 (Advance Estimate)

Real gross domestic product (GDP) increased at an annual rate of 6.4 percent in the first quarter of 2021, according to the "advance" estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2020, real GDP increased 4.3 percent.On a Q1-over-Q1 basis, GDP was up 0.4%.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent decline in real GDP from the previous peak (currently the previous peak was in Q4 2019).

This graph is through Q1 2021, and real GDP is currently off 0.9% from the previous peak.

The advance Q1 GDP report, at 6.4% annualized, was slightly below expectations, largely due to a decline in private inventories.

Personal consumption expenditures (PCE) increased at a 10.7% annualized rate in Q1, due, in part, to the American Rescue Plan Act.

The second graph below shows the contribution to GDP from residential investment, equipment and software, and nonresidential structures (3 quarter trailing average). This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

In the graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. So the usual pattern - both into and out of recessions is - red, green, blue.

Of course - with the sudden economic stop due to COVID-19 - the usual pattern doesn't apply.

The dashed gray line is the contribution from the change in private inventories.

Residential investment (RI) increased at a 10.8% annual rate in Q1.

Equipment investment increased at a 16.7% annual rate, and investment in

non-residential structures decreased at a 4.8% annual rate (after getting crushed over the previous year)..

Residential investment (RI) increased at a 10.8% annual rate in Q1.

Equipment investment increased at a 16.7% annual rate, and investment in

non-residential structures decreased at a 4.8% annual rate (after getting crushed over the previous year)..The contribution to Q1 GDP from investment in private inventories was -2.64 percentage points (this will likely be a positive for Q2).

On a 3 quarter trailing average basis, RI (red) is up solidly, equipment (green) is also up solidly, and nonresidential structures (blue) is down.

On a 3 quarter trailing average basis, RI (red) is up solidly, equipment (green) is also up solidly, and nonresidential structures (blue) is down.

I'll post more on the components of non-residential investment once the

supplemental data is released.

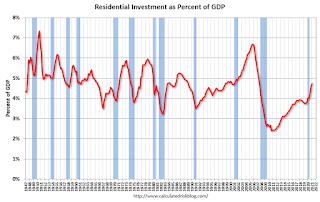

The second graph shows residential investment as a percent of GDP.

The second graph shows residential investment as a percent of GDP.

Residential Investment as a percent of GDP increased in Q1.

I'll break down Residential Investment into components after the GDP details are released.

Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

The third graph shows non-residential investment in

structures, equipment and "intellectual property products".

The third graph shows non-residential investment in

structures, equipment and "intellectual property products".

The second graph shows residential investment as a percent of GDP.

The second graph shows residential investment as a percent of GDP.Residential Investment as a percent of GDP increased in Q1.

I'll break down Residential Investment into components after the GDP details are released.

Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

The third graph shows non-residential investment in

structures, equipment and "intellectual property products".

The third graph shows non-residential investment in

structures, equipment and "intellectual property products".

Investment in non-residential structures declined in Q1 as a percent GDP, and will probably be weak for some time (hotel occupancy is still low, office and mall vacancy rates are high).

NAR: Pending Home Sales Increased 1.9% in March

by Calculated Risk on 4/29/2021 10:03:00 AM

From the NAR: Pending Home Sales Grow 1.9% in March

Pending home sales increased in March, snapping two consecutive months of declines, according to the National Association of Realtors®. All but one of the four major U.S. regions experienced month-over-month gains in March, while each area recorded year-over-year growth.This was below expectations for this index. Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in April and May.

The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, rose 1.9% to 111.3 in March. Year-over-year, contract signings jumped 23.3%, with the difference due in large part to the pandemic-induced lockdown in March 2020. An index of 100 is equal to the level of contract activity in 2001.

...

The Northeast PHSI rose 6.1% to 97.9 in March, a 16.7% increase from a year ago. In the Midwest, the index fell 3.7% to 98.6 last month, up 14.1% from March 2020.

Pending home sales transactions in the South jumped 2.9% to an index of 137.2 in March, up 27.9% from March 2020. The index in the West grew 2.9% in March to 94.5, up 29.8% from a year prior.

emphasis added

Weekly Initial Unemployment Claims at 553,000

by Calculated Risk on 4/29/2021 08:39:00 AM

The DOL reported:

In the week ending April 24, the advance figure for seasonally adjusted initial claims was 553,000, a decrease of 13,000 from the previous week's revised level. The previous week's level was revised up by 19,000 from 547,000 to 566,000. The 4-week moving average was 611,750, a decrease of 44,000 from the previous week's revised average. This is the lowest level for this average since March 14, 2020 when it was 225,500. The previous week's average was revised up by 4,750 from 651,000 to 655,750.This does not include the 121,749 initial claims for Pandemic Unemployment Assistance (PUA) that was down from 133,358 the previous week.

emphasis added

The following graph shows the 4-week moving average of weekly claims since 1971.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 651,000.

The previous week was revised up.

Regular state continued claims decreased to 3,813,109 (SA) from 3,886,198 (SA) the previous week.

Note: There are an additional 6,974,068 receiving Pandemic Unemployment Assistance (PUA) that decreased from 7,309,604 the previous week (there are questions about these numbers). This is a special program for business owners, self-employed, independent contractors or gig workers not receiving other unemployment insurance. And an additional 5,192,711 receiving Pandemic Emergency Unemployment Compensation (PEUC) down from 5,605,935.

Weekly claims were higher than the consensus forecast.

BEA: Real GDP increased at 6.4% Annualized Rate in Q1

by Calculated Risk on 4/29/2021 08:33:00 AM

From the BEA: Gross Domestic Product, First Quarter 2021 (Advance Estimate)

Real gross domestic product (GDP) increased at an annual rate of 6.4 percent in the first quarter of 2021, according to the "advance" estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2020, real GDP increased 4.3 percent. ...The advance Q1 GDP report, with 6.4% annualized growth, was slightly below expectations.

The increase in real GDP in the first quarter reflected increases in personal consumption expenditures (PCE), nonresidential fixed investment, federal government spending, residential fixed investment, and state and local government spending that were partly offset by decreases in private inventory investment and exports. Imports, which are a subtraction in the calculation of GDP, increased.

emphasis added

I'll have more later ...

Wednesday, April 28, 2021

Thursday: GDP, Unemployment Claims, Pending Home Sales

by Calculated Risk on 4/28/2021 09:00:00 PM

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for a decrease to 525 thousand from 547 thousand last week.

• Also at 8:30 AM, Gross Domestic Product, 1st quarter 2021 (Advance estimate). The consensus is that real GDP increased 6.5% annualized in Q1, up from 4.3% in Q4.

• At 10:00 AM, Pending Home Sales Index for March. The consensus is for a 6.0% increase in the index.