RSS Feed

RSS Feed by Calculated Risk on 7/30/2021 11:41:00 AM

Friday, July 30, 2021

Q2 2021 GDP Details on Residential and Commercial Real Estate

The BEA released the underlying details for the Q2 advance GDP report today.

The BEA reported that investment in non-residential structures decreased at a 7.0% annual pace in Q2. Note that weakness in non-residential structures started in 2019, before the pandemic.

Investment in petroleum and natural gas structures increased sharply in Q2 compared to Q1, and was up 46% year-over-year. However, investment in petroleum and natural gas structures is still down over 60% from the peak in 2014.

Click on graph for larger image.

Click on graph for larger image.

The first graph shows investment in offices, malls and lodging as a percent of GDP.

Investment in offices (blue) decreased in Q2, and was down 9.0% year-over-year.

Investment in multimerchandise shopping structures (malls) peaked in 2007 and was down about 19% year-over-year in Q2 - and at a record low as a percent of GDP. The vacancy rate for malls is still very high, so investment will probably stay low for some time.

Lodging investment increased slightly in Q2 compared to Q1, but lodging investment was down 19% year-over-year.

All three sectors - offices, malls, and hotels - are being hurt significantly by the pandemic.

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

Even though investment in single family structures has increased from the bottom, single family investment is just approaching normal levels as a percent of GDP.

Investment in single family structures was $405 billion (SAAR) (about 1.8% of GDP), and up 45% year-over-year.

Investment in multi-family structures increased in Q2.

Investment in home improvement was at a $331 billion Seasonally Adjusted Annual Rate (SAAR) in Q2 (about 1.5% of GDP). Home improvement spending has been strong during the pandemic.

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).Even though investment in single family structures has increased from the bottom, single family investment is just approaching normal levels as a percent of GDP.

Investment in single family structures was $405 billion (SAAR) (about 1.8% of GDP), and up 45% year-over-year.

Investment in multi-family structures increased in Q2.

Investment in home improvement was at a $331 billion Seasonally Adjusted Annual Rate (SAAR) in Q2 (about 1.5% of GDP). Home improvement spending has been strong during the pandemic.

Note that Brokers' commissions (black) increased sharply last year as existing home sales increased in the second half of 2020, but was down in Q2. Brokers' commissions were up 49% year-over-year in Q2.

Black Knight: Number of Homeowners in COVID-19-Related Forbearance Plans Increased Slightly

by Calculated Risk on 7/30/2021 10:07:00 AM

Note: Both Black Knight and the MBA (Mortgage Bankers Association) are putting out weekly estimates of mortgages in forbearance.

This data is as of July 27th.

From Andy Walden at Black Knight: Forbearances See Weekly Rise

After the last couple of weeks of volumes remaining flat, we did see some movement in the number of active forbearance plans this past week. According to our McDash Flash daily Forbearance Tracker data, the total number of active plans is up by 31,000 since last Tuesday.

Such upward movement late in the month has been relatively common in the recovery to date. Plan removals are clustered early in the month, which tends to lead to some degree of restart activity as the month progresses.

Despite this increase, there are still 163,000 (-7.9%) fewer plans than at the same time last month. As of July 27, 1.9 million borrowers remain in COVID-19 forbearance plans, making up 3.6% of all active mortgages and 2.0% of GSE, 6.3% of FHA/VA and 4.4% of Portfolio/PLS loans.

Click on graph for larger image.

Forbearances rose most significantly among loans held in bank portfolios or private label securities – which were up 35,000 for the week – with FHA/VA mortgages seeing a slight uptick in plans as well (+1,000). The 5,000-plan decline among GSE loans offset just a small share of the total weekly rise.

There are still some 179,000 plans are still scheduled to be reviewed for extension/removal in July, which provides some substantial opportunity for improvement next week.

While still low, new forbearance plan starts hit their highest weekly level since late March, with restart activity also remaining elevated. Roughly 2/3 of all starts over the past week were restarts. Removal volumes were the lowest since late May given the low volume of review activity at this time of month.

emphasis added

Personal Income increased 0.1% in June, Spending increased 1.0%

by Calculated Risk on 7/30/2021 08:37:00 AM

The BEA released the Personal Income and Outlays, June 2021 and Annual Update report:

Personal income increased $26.1 billion (0.1 percent) in June according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) decreased $2.6 billion (less than 0.1 percent) and personal consumption expenditures (PCE) increased $155.4 billion (1.0 percent).The June PCE price index increased 4.0 percent year-over-year and the June PCE price index, excluding food and energy, increased 3.5 percent year-over-year.

Real DPI decreased 0.5 percent in June and Real PCE increased 0.5 percent; goods decreased 0.2 percent and services increased 0.8 percent. The PCE price index increased 0.5 percent. Excluding food and energy, the PCE price index increased 0.4 percent.

emphasis added

The following graph shows real Personal Consumption Expenditures (PCE) through June 2021 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income and personal spending were above expectations, and the increase in PCE was slightly below expectations.

Thursday, July 29, 2021

Friday: Personal Income and Outlays

by Calculated Risk on 7/29/2021 09:00:00 PM

Friday:

• At 8:30 AM ET,: Personal Income and Outlays, June 2020. The consensus is for a 0.3% decrease in personal income, and for a 0.7% increase in personal spending. And for the Core PCE price index to increase 0.6%.

• At 9:45 AM, Chicago Purchasing Managers Index for July.

• At 10:00 AM, University of Michigan's Consumer sentiment index (Final for July). The consensus is for a reading of 80.8.

July 29th COVID-19, New Cases, Hospitalizations, Vaccinations

by Calculated Risk on 7/29/2021 03:49:00 PM

The 7-day average cases is the highest since April 18th.

The 7-day average hospitalizations is the highest since May 9th.

This data is from the CDC.

According to the CDC, on Vaccinations.

Total doses administered: 344,071,595, as of a week ago 339,763,765. Average doses last week: 0.62 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent over 18, One Dose | 69.4% | 69.3% | 68.6% | ≥70.0%1,2 |

| Fully Vaccinated✅ (millions) | 163.9 | 163.6 | 162.2 | ≥1601 |

| New Cases per Day3🚩 | 66,606 | 62,231 | 40,596 | ≤5,0002 |

| Hospitalized3🚩 | 31,148 | 29,541 | 21,464 | ≤3,0002 |

| Deaths per Day3🚩 | 296 | 296 | 222 | ≤502 |

| 1 America's Short Term Goals, 2my goals to stop daily posts, 37 day average for Cases, Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met (even if late). | ||||

KUDOS to the residents of the 20 states and D.C. that have achieved the 70% goal (percent over 18 with at least one dose): Vermont, Hawaii, Massachusetts and Connecticut are at 80%+, and Maine, New Mexico, New Jersey, Rhode Island, Pennsylvania, California, Maryland, Washington, New Hampshire, New York, Illinois, Virginia, Delaware, Minnesota, Oregon, Colorado and D.C. are all over 70%.

Next up are Florida at 68.2%, Utah at 67.7%, Wisconsin at 67.1%, Nebraska at 67.1%, South Dakota at 66.1%, Kansas at 66.0%, Iowa at 65.5%, and Nevada at 65.2%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

This data is from the CDC.

Las Vegas Visitor Authority for June: Convention Attendance N/A, Visitor Traffic Down 18% Compared to 2019

by Calculated Risk on 7/29/2021 02:44:00 PM

From the Las Vegas Visitor Authority: June 2021 Las Vegas Visitor Statistics

Marking the sixth consecutive month of MoM gains, June saw the destination host more than 2.9 million visitors, +3.2% MoM and down ‐17.6% vs. June 2019.

While convention and group data continue to be gathered, the return of several conventions including World of Concrete, Surfaces, Nightclub & Bar and the Int'l Esthetics, Cosmetics & Spa Conference helped support midweek business.

Hotel occupancy continued to improve, reaching 75.9% (up 5.0 pts MoM, down ‐15.8 pts vs. June 2019), as Weekend occupancy neared 90% (89.4%) and Midweek occupancy reached 70.9% (up 8.1 pts MoM, down ‐18.8 pts vs. June 2019.)

Click on graph for larger image.

Click on graph for larger image. The first graph shows visitor traffic for 2019 (blue), 2020 (orange) and 2021 (red).

Visitor traffic was down 17.6% compared to the same month in 2019.

There had been no convention traffic since March 2020, but there were a few conventions in June (data not available yet).

I'll add a graph of convention traffic once convention data is available.

Note: Conventions started again in June, but the data isn't available yet.

Hotels: Occupancy Rate Down 8% Compared to Same Week in 2019

by Calculated Risk on 7/29/2021 11:44:00 AM

Note: The year-over-year occupancy comparisons are easy, since occupancy declined sharply at the onset of the pandemic. So STR is comparing to the same week in 2019.

The occupancy rate is down 7.8% compared to the same week in 2019.

U.S. weekly hotel occupancy reached its highest level since October 2019, while room rates hit an all-time high, according to STR‘s latest data through July 24.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

July 18-24, 2021 (percentage change from comparable week in 2019*):

• Occupancy: 71.4% (-7.8%)

• Average daily rate (ADR): $141.75 (+4.0%)

• Revenue per available room (RevPAR): $101.24 (-4.2%)

Historically, the middle weeks of July are the country’s highest occupancy weeks each year, and 2021 has been no different even as demand slows week to week.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2021, black is 2020, blue is the median, dashed purple is 2019, and dashed light blue is for 2009 (the worst year on record for hotels prior to 2020).

Occupancy is well above the horrible 2009 levels and weekend occupancy (leisure) has been solid.

Note: Y-axis doesn't start at zero to better show the seasonal change.

Note: Y-axis doesn't start at zero to better show the seasonal change.

With solid leisure travel, the Summer months have had decent occupancy - but it is uncertain what will happen in the Fall with business travel.

NAR: Pending Home Sales Decreased 1.9% in June

by Calculated Risk on 7/29/2021 10:04:00 AM

From the NAR: Pending Home Sales Fall 1.9% in June

Pending home sales declined marginally in June after recording a notable gain in May, the National Association of Realtors® reported. Contract activity was split in the four major U.S. regions from both a year-over-year and month-over-month perspective. The Northeast recorded the only yearly gains in June.This was below expectations of a 0.5% increase for this index. Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in July and August.

The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, fell 1.9% to 112.8 in June. Year-over-year, signings also slipped 1.9%. An index of 100 is equal to the level of contract activity in 2001.

...

The Northeast PHSI increased 0.5% to 98.5 in June, an 8.7% rise from a year ago. In the Midwest, the index grew 0.6% to 108.3 last month, down 2.4% from June 2020.

Pending home sales transactions in the South fell 3.0% to an index of 132.4 in June, down 4.7% from June 2020. The index in the West decreased 3.8% in June to 98.1, down 2.6% from a year prior.

emphasis added

A Few Comments on Q2 GDP

by Calculated Risk on 7/29/2021 09:14:00 AM

Earlier from the BEA: Gross Domestic Product, Second Quarter 2021 (Advance Estimate) and Annual Update

Real gross domestic product (GDP) increased at an annual rate of 6.5 percent in the second quarter of 2021, according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 6.3 percent (revised).On a Q2-over-Q2 basis, GDP was up 16.7% (Q2 2020 was the depth of pandemic recession).

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent decline in real GDP from the previous peak (the previous peak was in Q4 2019).

This graph is through Q1 2022, and real GDP is now at a new peak; 0.8% above the previous peak.

The advance Q2 GDP report, at 6.5% annualized, was below expectations, due to several factors - a decline in private inventories, a decline in residential investment, a decline in government expenditures and a negative contribution from trade.

Personal consumption expenditures (PCE) increased at a 11.8% annualized rate in Q2, due, in part, to the American Rescue Plan Act.

The second graph below shows the contribution to GDP from residential investment, equipment and software, and nonresidential structures (3 quarter trailing average). This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

In the graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. So the usual pattern - both into and out of recessions is - red, green, blue.

Of course - with the sudden economic stop due to COVID-19 - the usual pattern doesn't apply.

The dashed gray line is the contribution from the change in private inventories.

Residential investment (RI) decreased at a 9.8% annual rate in Q2. Equipment investment increased at a 13.0% annual rate, and investment in non-residential structures decreased at a 7.0% annual rate (after getting crushed over the previous year)..

Residential investment (RI) decreased at a 9.8% annual rate in Q2. Equipment investment increased at a 13.0% annual rate, and investment in non-residential structures decreased at a 7.0% annual rate (after getting crushed over the previous year)..The contribution to Q2 GDP from investment in private inventories was -1.13 percentage points (this will likely be a positive in the second half of 2021).

On a 3 quarter trailing average basis, RI (red) is still up solidly, equipment (green) is up sharply, and nonresidential structures (blue) is still down.

On a 3 quarter trailing average basis, RI (red) is still up solidly, equipment (green) is up sharply, and nonresidential structures (blue) is still down.

I'll post more on the components of non-residential investment once the supplemental data is released.

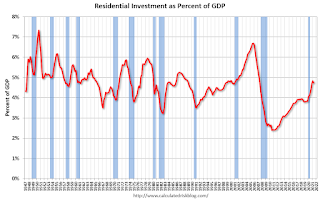

The third graph shows residential investment as a percent of GDP.

The third graph shows residential investment as a percent of GDP.

Residential Investment as a percent of GDP decreased in Q2, after increasing sharply for several quarters.

I'll break down Residential Investment into components after the GDP details are released.

Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

The fourth graph shows non-residential investment in

structures, equipment and "intellectual property products".

The fourth graph shows non-residential investment in

structures, equipment and "intellectual property products".

The third graph shows residential investment as a percent of GDP.

The third graph shows residential investment as a percent of GDP.Residential Investment as a percent of GDP decreased in Q2, after increasing sharply for several quarters.

I'll break down Residential Investment into components after the GDP details are released.

Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

The fourth graph shows non-residential investment in

structures, equipment and "intellectual property products".

The fourth graph shows non-residential investment in

structures, equipment and "intellectual property products".

Investment in non-residential structures declined in Q2 as a percent GDP, and will probably be weak for some time (hotel occupancy is still low, office and mall vacancy rates are high).

Weekly Initial Unemployment Claims decrease to 400,000

by Calculated Risk on 7/29/2021 08:38:00 AM

The DOL reported:

In the week ending July 24, the advance figure for seasonally adjusted initial claims was 400,000, a decrease of 24,000 from the previous week's revised level. The previous week's level was revised up by 5,000 from 419,000 to 424,000. The 4-week moving average was 394,500, an increase of 8,000 from the previous week's revised average. The previous week's average was revised up by 1,250 from 385,250 to 386,500.This does not include the 95,166 initial claims for Pandemic Unemployment Assistance (PUA) that was down from 109,868 the previous week.

emphasis added

The following graph shows the 4-week moving average of weekly claims since 1971.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 394,500.

The previous week was revised up.

Regular state continued claims increased to 3,269,000 (SA) from 3,262,000 (SA) the previous week.

Note: There are an additional 5,246,162 receiving Pandemic Unemployment Assistance (PUA) that increased from 5,133,938 the previous week (there are questions about these numbers). This is a special program for business owners, self-employed, independent contractors or gig workers not receiving other unemployment insurance. And an additional 4,233,883 receiving Pandemic Emergency Unemployment Compensation (PEUC) down from 4,134,716.

Weekly claims were at the consensus forecast.