RSS Feed

RSS Feed by Calculated Risk on 8/17/2021 05:02:00 PM

Tuesday, August 17, 2021

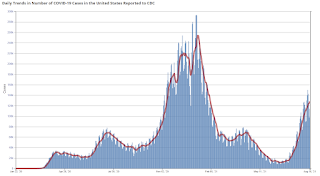

August 17th COVID-19: Wave Still Increasing

New data from Israel: A grim warning from Israel: Vaccination blunts, but does not defeat Delta (get vaccinated and mask up!)

Update: Great explainer here (not as bad as it seemed) Israeli data: How can efficacy vs. severe disease be strong when 60% of hospitalized are vaccinated?

The 7-day average deaths is the highest since May 14th.

According to the CDC, on Vaccinations.

Total doses administered: 357,894,995, as of a week ago 352,550,944. Average doses last week: 0.76 million per day.

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

The following 19 states have between 50% and 59.9% fully vaccinated: New Jersey at 59.9%, New Hampshire, Washington, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, Hawaii, California, Delaware, Pennsylvania, Wisconsin, and Nebraska, Florida and Iowa all at 50.6%.

Next up (total population, fully vaccinated according to CDC) are Illinois at 49.9%, Michigan at 49.6%, South Dakota at 48.0, Ohio at 47.4%, Kentucky at 46.9%, Arizona at 46.6%, Kansas at 46.6%, Alaska at 46.3%, Nevada at 46.0% and Utah at 45.8%.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

The 7-day average cases is the highest since February 5th.

The 7-day average hospitalizations is the highest since February 11th.

The 7-day average deaths is the highest since May 14th.

This data is from the CDC.

According to the CDC, on Vaccinations.

Total doses administered: 357,894,995, as of a week ago 352,550,944. Average doses last week: 0.76 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent fully Vaccinated | 50.9% | 50.8% | 50.3% | ≥70.0%1 |

| Fully Vaccinated (millions) | 168.9 | 168.7 | 166.9 | ≥2321 |

| New Cases per Day3🚩 | 128,347 | 125,036 | 112,259 | ≤5,0002 |

| Hospitalized3🚩 | 72,874 | 71,266 | 57,307 | ≤3,0002 |

| Deaths per Day3🚩 | 553 | 547 | 501 | ≤502 |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of the 6 states that have achieved 60% of total population fully vaccinated: Vermont at 67.1%, Massachusetts, Maine, Connecticut, Rhode Island and Maryland.

The following 19 states have between 50% and 59.9% fully vaccinated: New Jersey at 59.9%, New Hampshire, Washington, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, Hawaii, California, Delaware, Pennsylvania, Wisconsin, and Nebraska, Florida and Iowa all at 50.6%.

Next up (total population, fully vaccinated according to CDC) are Illinois at 49.9%, Michigan at 49.6%, South Dakota at 48.0, Ohio at 47.4%, Kentucky at 46.9%, Arizona at 46.6%, Kansas at 46.6%, Alaska at 46.3%, Nevada at 46.0% and Utah at 45.8%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

This data is from the CDC.

LA Area Port Traffic: Solid Imports, Weak Exports in July

by Calculated Risk on 8/17/2021 02:41:00 PM

Note: The expansion to the Panama Canal was completed in 2016 (As I noted a few years ago), and some of the traffic that used the ports of Los Angeles and Long Beach is probably going through the canal. This might be impacting TEUs on the West Coast.

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12 month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12 month basis, inbound traffic was up 0.2% in July compared to the rolling 12 months ending in June. Outbound traffic was down 2.2% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

2021 started off incredibly strong for imports.

Imports were up 2% YoY in July (recovered last year in July following the early months of the pandemic), and exports were down 24.0% YoY.

Imports were up 2% YoY in July (recovered last year in July following the early months of the pandemic), and exports were down 24.0% YoY.

NAHB: Builder Confidence Declined to 75 in August

by Calculated Risk on 8/17/2021 10:05:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 75, down from 80 in July. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Builder Confidence at 13-Month Low on Higher Material Costs, Home Prices

Builder sentiment in the market for newly-built single-family homes fell five points to 75 in August, according to the latest National Association of Home Builders/Wells Fargo Housing Market Index (HMI). The index is at its lowest point since July 2020.

Higher construction costs and supply shortages have led to significant price growth, which in turn has caused prospective buyers to experience sticker shock. The decline in the buyer traffic index to its lowest level since July 2020 is evidence that supply-side constraints have begun to hold consumers back.

...

The HMI index gauging current sales conditions fell five points to 81 and the component measuring traffic of prospective buyers also posted a five-point decline to 60. The gauge charting sales expectations in the next six months held steady at 81.

Looking at the three-month moving averages for regional HMI scores, the Northeast fell one point to 74, the Midwest dropped two points to 68, the South posted a three-point decline to 82 and the West registered a two-point drop to 85.

Click on graph for larger image.

Click on graph for larger image.This graph show the NAHB index since Jan 1985.

This was well below the consensus forecast, but still a solid reading.

Industrial Production Increased 0.9 Percent in July

by Calculated Risk on 8/17/2021 09:22:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production increased 0.9 percent in July after moving up 0.2 percent in June. In July, manufacturing output rose 1.4 percent. About half of the gain in factory output is attributable to a jump of 11.2 percent for motor vehicles and parts, as a number of vehicle manufacturers trimmed or canceled their typical July shutdowns. Despite the large increase last month, vehicle assemblies continued to be constrained by a persistent shortage of semiconductors; the production of motor vehicles and parts in July was about 3-1/2 percent below its recent peak in January 2021. The output of utilities decreased 2.1 percent in July, while the index for mining rose 1.2 percent.

At 101.1 percent of its 2017 average, total industrial production in July was 6.6 percent above its year-earlier level but 0.2 percent below its pre-pandemic (February 2020) level. Capacity utilization for the industrial sector rose 0.7 percentage point in July to 76.1 percent, a rate that is 3.5 percentage points below its long-run (1972–2020) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, but still below the level in February 2020.

Capacity utilization at 76.1% is 3.5% below the average from 1972 to 2020.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased in July to 101.1. This is 0.2% below the February 2020 level.

The change in industrial production was above consensus expectations, probably due to vehicle manufacturers not shutting down in July.

Retail Sales Decreased 1.1% in July

by Calculated Risk on 8/17/2021 08:39:00 AM

On a monthly basis, retail sales were decreased 1.1% from June to July (seasonally adjusted), and sales were up 15.8 percent from July 2020.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for July 2021, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $617.7 billion, a decrease of 1.1 percent from the previous month, but 15.8 percent above July 2020. ... The May 2021 to June 2021 percent change was revised from up 0.6 percent to up 0.7 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were down 1.4% in July.

The stimulus checks boosted retail sales significantly in March and April.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 14.2% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 14.2% on a YoY basis.

Sales in July were below expectations, however sales in May and June were revised up.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 14.2% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 14.2% on a YoY basis.Sales in July were below expectations, however sales in May and June were revised up.

Monday, August 16, 2021

Tuesday: Retail Sales, Industrial Production, Homebuilder Survey and More

by Calculated Risk on 8/16/2021 09:00:00 PM

From Matthew Graham at Mortgage News Daily: MBS RECAP: Drifty Day, Treasuries Hold Weekly Gains, MBS Underperform

MBS underperformed, ultimately returning to 'unchanged' levels in the 4pm hour even as Treasuries remined slightly stronger on the day. ... [30 year fixed 2.93%]Tuesday:

emphasis added

• At 8:30 AM ET, Retail sales for July is scheduled to be released. The consensus is for 0.2% decrease in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for July. The consensus is for a 0.5% increase in Industrial Production, and for Capacity Utilization to increase to 75.7%.

• At 10:00 AM, The August NAHB homebuilder survey. The consensus is for a reading of 80, unchanged from 80. Any number above 50 indicates that more builders view sales conditions as good than poor.

• At 12:00 PM, MBA Q2 National Delinquency Survey (expected)

• At 1:30 PM, Fed Chair Powell speaks: Conversation with the Chair: A Virtual Teacher Town Hall Meeting

August 16th COVID-19: Data reported on Monday is always low, and is revised up as data is received

by Calculated Risk on 8/16/2021 08:15:00 PM

This data is from the CDC.

According to the CDC, on Vaccinations.

Total doses administered: 357,292,057, as of a week ago 351,933,175. Average doses last week: 0.77 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent fully Vaccinated | 50.8% | 50.7% | 50.3% | ≥70.0%1 |

| Fully Vaccinated (millions) | 168.7 | 168.4 | 166.7 | ≥2321 |

| New Cases per Day3 | 108,470 | 115,299 | 110,656 | ≤5,0002 |

| Hospitalized3🚩 | 65,935 | 67,640 | 54,857 | ≤3,0002 |

| Deaths per Day3 | 495 | 523 | 495 | ≤502 |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of the 6 states that have achieved 60% of total population fully vaccinated: Vermont at 67.1%, Massachusetts, Maine, Connecticut, Rhode Island and Maryland.

The following 19 states have between 50% and 59.9% fully vaccinated: New Jersey at 59.8%, New Hampshire, Washington, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, Hawaii, California, Delaware, Pennsylvania, Wisconsin, Nebraska, Florida and Iowa at 50.4%.

Next up (total population, fully vaccinated according to CDC) are Illinois at 49.8%, Michigan at 49.6%, South Dakota at 47.9, Ohio at 47.4%, Kentucky at 46.8%, Arizona at 46.5%, Kansas at 46.5%, Alaska at 46.3%, Nevada at 46.0% and Utah at 45.8%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

This data is from the CDC.

MBA Survey: "Share of Mortgage Loans in Forbearance Decreases to 3.26%"

by Calculated Risk on 8/16/2021 04:00:00 PM

Note: This is as of August 8th.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 3.26%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 14 basis points from 3.40% of servicers’ portfolio volume in the prior week to 3.26% as of August 8, 2021. According to MBA’s estimate, 1.6 million homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 5 basis points to 1.69%. Ginnie Mae loans in forbearance decreased 23 basis points to 3.95%, while the forbearance share for portfolio loans and private-label securities (PLS) decreased 32 basis points to 7.05%. The percentage of loans in forbearance for independent mortgage bank (IMB) servicers decreased 17 basis points to 3.46%, and the percentage of loans in forbearance for depository servicers decreased 13 basis points to 3.36%.

“The largest decrease in a month in the share of loans in forbearance came from a jump in forbearance exits, as many homeowners are nearing the end of their forbearance terms. The forbearance share declined for all investor and servicer categories,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “New forbearance requests picked up slightly this week, particularly for Ginnie Mae loans, but overall trends remain positive. Incoming data continues to support our forecast of an improving job market in the months ahead.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April 2020, and has trended down since then.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) increased relative to the prior week: from 0.04% to 0.06%"

Boston Real Estate in July: Sales Up 14% YoY, Inventory Down 23% YoY

by Calculated Risk on 8/16/2021 03:10:00 PM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

For Boston (single family and condos):

Closed sales in July 2021 were 3,101, up 14.4% from 2,710 in July 2020.

Active Listings in July 2021 were 3,719, down 23.4% from 4,853 in July 2020.

Inventory in July was down 2.7% from last month.

Housing Inventory August 16th Update: Inventory Increased Week-over-week, Up 38% from Low in early April

by Calculated Risk on 8/16/2021 11:16:00 AM

Tracking existing home inventory will be very important this year.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of August 13th, inventory was at 422 thousand (7 day average), compared to 602 thousand for the same week a year ago. That is a decline of 29.8%.

A week ago, inventory was at 412 thousand, and was down 32.8% YoY.

Seasonally, inventory has bottomed. Inventory was about 37.7% above the record low in early April.

A couple of interesting points from 2019: In 2019, inventory bottomed at 814 thousand in February (so inventory is still very low compared to normal levels). And, in 2019, inventory peaked at 972 thousand in early August (an increase of about 19% from the low).

So inventory is less than half of what we'd normally expect, however inventory has increased (as a percentage) more than normal.

Key question: Usually inventory peaks in the Summer, and then declines into the Fall. Will inventory follow the normal seasonal pattern, or will inventory continue to increase over the coming months? This will be important to watch for house prices and housing activity.

Mike Simonsen discusses this data regularly on Youtube.

Altos Research has also seen a significant pickup in price decreases - back to the level of a year ago - but still well below a normal rate for August.