RSS Feed

RSS Feed by Calculated Risk on 1/06/2022 03:59:00 PM

Thursday, January 06, 2022

Goldman December Payrolls Preview

A few brief excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls rose 500k, above consensus of +444k. ... We estimate a one-tenth drop in the unemployment rate to 4.1%.CR Note: The consensus is for 400 thousand jobs added, and for the unemployment rate to decrease to 4.1%.

emphasis added

1st Look at Local Housing Markets in December

by Calculated Risk on 1/06/2022 01:13:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in December

A brief excerpt:

And a table of December sales. Sales were down 11.1% YoY, Not Seasonally Adjusted (NSA).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note that there was one fewer selling day in December ‘21 compared to December ‘20, so the Seasonally Adjusted (SA) number will show less of a YoY decline than the NSA numbers.

December Employment Preview

by Calculated Risk on 1/06/2022 10:53:00 AM

On Friday at 8:30 AM ET, the BLS will release the employment report for December. The consensus is for 400 thousand jobs added, and for the unemployment rate to decrease to 4.1%.

Click on graph for larger image.

Click on graph for larger image.• First, currently there are still about 3.9 million fewer jobs than in February 2020 (before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 20 months after the onset, is now significantly better than the worst of the "Great Recession".

• ADP Report: The ADP employment report showed a gain of 807,000 private sector jobs, well above the consensus estimate of 413,000 jobs added. The ADP report hasn't been very useful in predicting the BLS report, but this suggests the BLS report could be above expectations.

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index increased in December to 54.2%, up from 53.3% last month. This would suggest little change in manufacturing employment in December. ADP showed 74,000 manufacturing jobs added.

The ISM® Services employment index decreased in December to 54.9%, down from 56.5% last month. This would suggest a 200 thousand increase in service employment in December. Combined, the ISM indexes suggest employment below the consensus estimate.

• Unemployment Claims: The weekly claims report showed a decline in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 270,000 in November to 206,000 in December. This would usually suggest fewer layoffs in December than in November, although this might not be very useful right now. In general, weekly claims have been falling, and have been below expectations in December.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the November report.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the November report.This data is only available back to 1994, so there is only data for three recessions. In November, the number of permanent job losers decreased to 1.921 million from 2.126 million in October.

These jobs will likely be the hardest to recover, so it is a positive that the number of permanent job losers is declining fairly rapidly.

• Seasonal Retail Hiring: Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. But only a few temporary workers are hired in December. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

• Seasonal Retail Hiring: Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. But only a few temporary workers are hired in December. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

Retailers hired 332 thousand workers Not Seasonally Adjusted (NSA) net in November. This was somewhat lower than normal, and seasonally adjusted (SA) to a loss of 20 thousand jobs in November.

In 2020, retailers hired 140,300 employees (NSA) in December. That translated to a gain of 30,100 jobs SA. It is possible that retailers hired for some jobs early (in October), and retail (SA) will be slightly negative in the December report (always difficult to predict).

• Seasonal Retail Hiring: Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. But only a few temporary workers are hired in December. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

• Seasonal Retail Hiring: Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. But only a few temporary workers are hired in December. Here is a graph that shows the historical net retail jobs added for October, November and December by year.Retailers hired 332 thousand workers Not Seasonally Adjusted (NSA) net in November. This was somewhat lower than normal, and seasonally adjusted (SA) to a loss of 20 thousand jobs in November.

In 2020, retailers hired 140,300 employees (NSA) in December. That translated to a gain of 30,100 jobs SA. It is possible that retailers hired for some jobs early (in October), and retail (SA) will be slightly negative in the December report (always difficult to predict).

• Conclusion: There is significant optimism concerning the December employment report, and many analysts are expecting a strong report. Overall, the ADP report was strong and unemployment claims have been falling quickly.

As far as the pandemic, the number of daily cases during the reference week in December was around 120,000, up from around 80,000 in November. New cases per day started increasing rapidly after the reference week in December, so the current COVID wave probably had little impact on December hiring.

My sense is the report will be above consensus expectations.

ISM® Services Index Decreased to 62.0% in December

by Calculated Risk on 1/06/2022 10:03:00 AM

(Posted with permission). The December ISM® Services index was at 62.0%, down from 69.1% last month. The employment index decreased to 54.9%, from 56.5%. Note: Above 50 indicates expansion, below 50 in contraction.

From the Institute for Supply Management: Services PMI® at 62% December 2021 Services ISM® Report On Business®

Economic activity in the services sector grew in December for the 19th month in a row — with the Services PMI® exceeding 60 percent for the 10th consecutive month — say the nation’s purchasing and supply executives in the latest Services ISM® Report On Business®.This was below the consensus forecast, and the employment index decreased to 54.9%, from 56.5% the previous month.

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee: “In December, the Services PMI® registered 62 percent, 7.1 percentage points below November’s all-time high reading of 69.1 percent. The Business Activity Index registered 67.6 percent, a decrease of 7 percentage points compared to the reading of 74.6 percent in November, and the New Orders Index registered 61.5 percent, 8.2 percentage points lower than the all-time high reading of 69.7 percent reported in November.

emphasis added

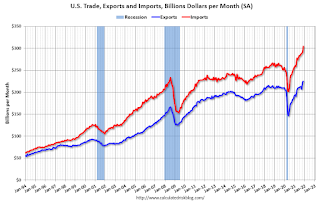

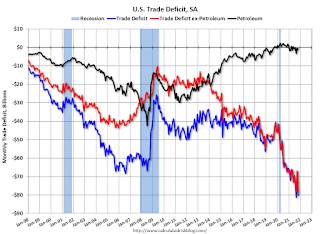

Trade Deficit Increased to $80.2 Billion in November

by Calculated Risk on 1/06/2022 08:44:00 AM

From the Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $80.2 billion in November, up $13.0 billion from $67.2 billion in October, revised.

November exports were $224.2 billion, $0.4 billion more than October exports. November imports were $304.4 billion, $13.4 billion more than October imports.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Both exports and imports increased in November.

Exports are up 21% compared to November 2020; imports are up 21% compared to November 2020.

Both imports and exports decreased sharply due to COVID-19, and have now bounced back (imports more than exports),

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Note that net, imports and exports of petroleum products are close to zero.

The trade deficit with China increased to $32.3 billion in November, from $30.6 billion in November 2020.

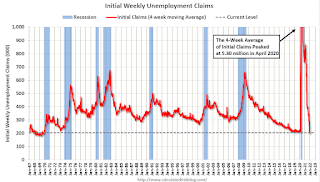

Weekly Initial Unemployment Claims Increase to 207,000

by Calculated Risk on 1/06/2022 08:34:00 AM

The DOL reported:

In the week ending January 1, the advance figure for seasonally adjusted initial claims was 207,000, an increase of 7,000 from the previous week's revised level. The previous week's level was revised up by 2,000 from 198,000 to 200,000. The 4-week moving average was 204,500, an increase of 4,750 from the previous week's revised average. The previous week's average was revised up by 500 from 199,250 to 199,750.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 204,500.

The previous week was revised up.

Weekly claims were close to the consensus forecast.

Wednesday, January 05, 2022

Thursday: Unemployment Claims, Trade Deficit, ISM Services

by Calculated Risk on 1/05/2022 09:00:00 PM

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. Initial claims were 198 thousand last week.

• At 8:30 AM, Trade Balance report for November from the Census Bureau. The consensus is the trade deficit to be $70.0 billion. The U.S. trade deficit was at $67.1 billion in October.

• At 10:00 AM, the ISM Services Index for December.

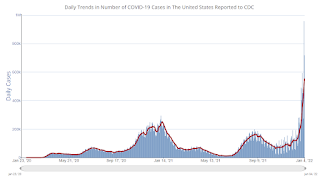

And on COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Week Ago | Goal | ||

| Percent fully Vaccinated | 62.3% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 206.8 | --- | ≥2321 | |

| New Cases per Day3🚩 | 554,328 | 281,842 | ≤5,0002 | |

| Hospitalized3🚩 | 85,423 | 64,152 | ≤3,0002 | |

| Deaths per Day3🚩 | 1,238 | 1,072 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of positive tests reported.

New cases are at record levels. It appears likely hospitalizations will exceed the previous 7-day average record of 124,031 a year ago.

Fortunately, deaths are still well below the previous 7-day average record of 3,421 in January 2021.

Apartment Vacancy Rate Declined in Q4

by Calculated Risk on 1/05/2022 02:42:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Apartment Vacancy Rate Declined in Q4

A brief excerpt:

Reis reported that the apartment vacancy rate was at 4.7% in Q4 2021, down from 4.8% in Q3, and down from a pandemic peak of 5.4% in Q1 2021.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Reis is just for large cities.

Reis also reported the asking rents were up 2.8% in Q4 compared to Q3, and up 11.9% year-over-year. Rents were down year-over-year through Q2 2021 (due to the pandemic) and picked up sharply in Q3. Even with the recent surge in rents, rents are only up 4.5% annualized over the last 2 years (since rents decreased early in the pandemic).

Reis: Office Vacancy Rates Decreased Slightly in Q4

by Calculated Risk on 1/05/2022 01:46:00 PM

Reis reported the office vacancy rate was at 18.1% in Q4 2021, down from 18.2% in Q3, and up from 17.8% in Q4 2020.

Q2 2021 saw the highest vacancy rate for offices since the early '90s at 18.5% (following the S&L crisis).

Click on graph for larger image.

Click on graph for larger image.

The first graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

Reis also reported that office effective rents were unchanged in Q4; rents are about the same rate as early 2019.

Click on graph for larger image.The first graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

The office vacancy rate was elevated prior to the pandemic and moved up during the pandemic.

Reis also reported that office effective rents were unchanged in Q4; rents are about the same rate as early 2019.

All vacancy data courtesy of Reis

Annual Vehicle Sales increase 3% in 2021; Sales Mix and Heavy Trucks

by Calculated Risk on 1/05/2022 11:23:00 AM

The BEA released their estimate of light vehicle sales for December today. The BEA estimates sales of 12.44 million SAAR in December 2021 (Seasonally Adjusted Annual Rate), down 3.3% from the November sales rate, and down 23.8% from December 2020.

Click on graph for larger image.

Click on graph for larger image.The first graph shows annual sales since 1976.

Light vehicle sales in 2021 were at 14.93 million, up 3.1% from 14.47 million in 2020.

Sales in 2021 were impacted significantly by supply chain disruptions, and sales were still down 12% from the 2019 level.

This suggests vehicle sales will increase in 2022 and boost GDP.

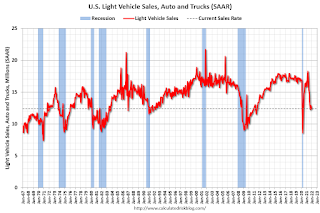

This graph shows monthly light vehicle sales since 1967 from the BEA. The dashed line is sales for the current month.

This graph shows monthly light vehicle sales since 1967 from the BEA. The dashed line is sales for the current month.

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic).

This graph shows monthly light vehicle sales since 1967 from the BEA. The dashed line is sales for the current month.The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic).

However, sales decreased earlier this year due to supply issues. It appears the "supply chain bottom" was in September, but sales in December were disappointing again.

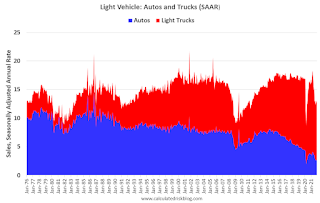

This third graph shows sales for passenger cars and trucks / SUVs through December 2021.

Over time the mix has changed more and more towards light trucks and SUVs (red).

Over time the mix has changed more and more towards light trucks and SUVs (red).The percent of light trucks and SUVs was at 79% in December 2021 - near the all-time high.

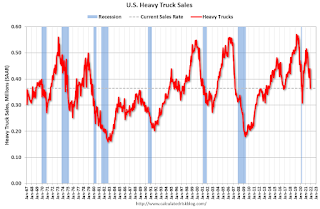

The fourth graph shows heavy truck sales since 1967 using data from the BEA. The dashed line is the December 2021 seasonally adjusted annual sales rate (SAAR).

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new all-time high of 563 thousand SAAR in September 2019.

Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Heavy truck sales declined sharply at the beginning of the pandemic, falling to a low of 308 thousand SAAR in May 2020.

Heavy truck sales declined sharply at the beginning of the pandemic, falling to a low of 308 thousand SAAR in May 2020. Heavy truck sales were at 364 thousand SAAR in December, down from 439 thousand SAAR in November, and down 19.5% from 452 thousand SAAR in December 2020. The decline is probably due to supply disruptions.