RSS Feed

RSS Feed by Calculated Risk on 2/14/2022 12:45:00 PM

Monday, February 14, 2022

A Few Comments on Inflation

With CPI inflation coming in at 7.5% year-over-year in January (YoY), and core CPI at 6.0% YoY - both the highest since 1982 - the FOMC is now expected to raise rates a number of times in 2022.

Last week, Goldman Sachs economists wrote:

“Following this morning’s strong CPI print, we are raising our Fed forecast to include seven consecutive 25bp rate hikes at each of the remaining FOMC meetings in 2022 (vs. five hikes in 2022 previously).”And Merrill Lynch economists noted:

emphasis added

"For the Fed, this report provides another wake-up call. Inflation is here and it continues to make its presence known everywhere. We remain comfortable with our hawkish call for the Fed to hike seven times this year ..."This is a significant outlook change from just a few months ago.

The FOMC will likely announce a rate hike at the March meeting, and perhaps even raise rates by 50bps (some analysts think the FOMC might announce an emergency hike before the FOMC meeting).

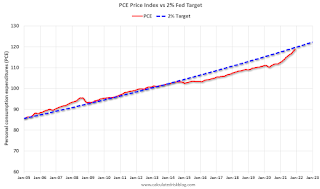

Click on graph for larger image.

Click on graph for larger image.This graph is from January 2005 (just an arbitrary date) through December 2022.

This shows that inflation had been below target for years. If we were doing price targeting (we aren't), then prices would just be getting back to the target.

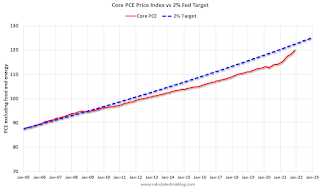

The second graph is for core PCE inflation shows the same pattern, but core PCE is even further below the trend line.

The question is not will some prices "stick", but rather will YoY inflation ease back towards the Fed's target? Or will inflation stay elevated?

The question is not will some prices "stick", but rather will YoY inflation ease back towards the Fed's target? Or will inflation stay elevated?My sense is once the pandemic slows significantly; inflation will ease back towards the Fed's target.

Of course, the pandemic is still contributing significantly to the surge in inflation (supply constraints, labor shortages, shift in buying patterns), and the FOMC cannot control the pandemic.

Housing Inventory February 14th Update: Inventory Down 2.5% Week-over-week; New Record Low

by Calculated Risk on 2/14/2022 10:02:00 AM

Tracking existing home inventory is very important in 2022.

Inventory usually declines in the winter, and this is a new record low for this series.

This inventory graph is courtesy of Altos Research.

As of February 11th, inventory was at 250 thousand (7-day average), compared to 344 thousand for the same week a year ago. That is a decline of 27.5%.

A week ago, inventory was at 256 thousand, and was down 27.9% YoY.

Inventory was down 5.9% from the previous week.

Compared to the same week in 2020, inventory is down 65.7% from 727 thousand.

Last year, seasonally, inventory bottomed in April 2021 - very late in the year - usually inventory bottoms by February. An early key in 2022 will be to watch if inventory bottoms earlier this year.

Mike Simonsen discusses this data regularly on Youtube.

Six High Frequency Indicators for the Economy

by Calculated Risk on 2/14/2022 08:57:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides.

There was a clear negative impact from the omicron variant of COVID that is starting to ease.

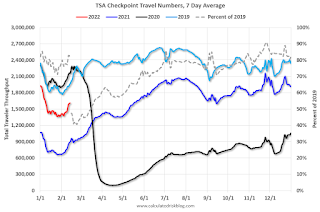

----- Airlines: Transportation Security Administration -----

The TSA is providing daily travel numbers.

This data is as of February 13th.

Click on graph for larger image.

Click on graph for larger image.

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 18.1% from the same day in 2019 (81.9% of 2019). (Dashed line)

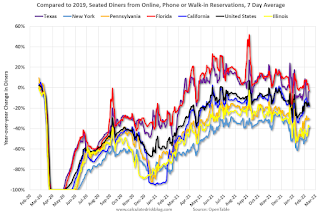

----- Restaurants: OpenTable -----

The second graph shows the 7-day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

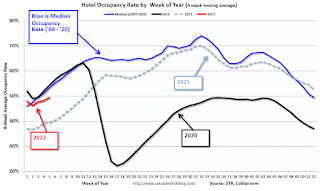

----- Hotel Occupancy: STR -----

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021.

This data is through February 5th. The occupancy rate was down 15.8% compared to the same week in 2019.

----- Transit: Apple Mobility -----

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

This data is through February 10th

This data is through February 10th

----- New York City Subway Usage -----

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider.

This data is through Friday, February 11th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

The TSA is providing daily travel numbers.

This data is as of February 13th.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 18.1% from the same day in 2019 (81.9% of 2019). (Dashed line)

Air travel had been off about 20% relative to 2019 for most of the second half of 2021 (with some ups and downs) - but picked up over the Thanksgiving and Christmas holidays (solid leisure travel) - and has declined in early 2022 (omicron / weak business travel).

The second graph shows the 7-day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

IMPORTANT: OpenTable notes: "we’ve updated the data including downloadable dataset from January 1, 2021, onward to compare seated diners from 2021 to 2019, as opposed to year over year." Thanks!

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:

This data is updated through February 12, 2022.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Dining was mostly moving sideways but declined during the winter wave of COVID and is now increasing. The 7-day average for the US is down 17% compared to 2019.

Thanks to OpenTable for providing this restaurant data:This data is updated through February 12, 2022.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Dining was mostly moving sideways but declined during the winter wave of COVID and is now increasing. The 7-day average for the US is down 17% compared to 2019.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through February 10th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $77 million last week, down about 41% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $77 million last week, down about 41% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021.

This data is through February 5th. The occupancy rate was down 15.8% compared to the same week in 2019.

The 4-week average of the occupancy rate is below the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase seasonally over the next few months. The key question is: How much business travel will return?

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

This data is through February 10th for the United States and several selected cities.

The graph is the running 7-day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7-day average for the US is at 105% of the January 2020 level.

The graph is the running 7-day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7-day average for the US is at 105% of the January 2020 level.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This graph shows how much MTA traffic has recovered in each borough (Graph starts at first week in January 2020 and 100 = 2019 average).

Manhattan is at about 35% of normal.

This data is through Friday, February 11th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, February 13, 2022

Sunday Night Futures

by Calculated Risk on 2/13/2022 06:10:00 PM

Weekend:

• Schedule for Week of February 13, 2022

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were up over the last week with WTI futures at $93.10 per barrel and Brent at $94.44 per barrel. A year ago, WTI was at $60, and Brent was at $63 - so WTI oil prices are up about 50% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.47 per gallon. A year ago prices were at $2.50 per gallon, so gasoline prices are up $0.97 per gallon year-over-year.

3rd Look at Local Housing Markets in January

by Calculated Risk on 2/13/2022 10:37:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in January

A brief excerpt:

Adding Albuquerque, Atlanta, Colorado, Georgia, Jacksonville, Minnesota, Sacramento, Santa Clara and South CarolinaThere is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

Here is a summary of active listings for these housing markets in January. Inventory was down 10.3% in January month-over-month (MoM) from December, and down 27.9% year-over-year (YoY).

Inventory almost always declines seasonally during the Winter, so the MoM decline is not a surprise. Last month, these markets were down 26.5% YoY, so the YoY decline in January is slightly larger than in December. This isn’t indicating a slowing market

Notes for all tables:

1. New additions to table in BOLD.

2. Northwest (Seattle), North Texas (Dallas), and Santa Clara (San Jose), Jacksonville, Source: Northeast Florida Association of REALTORS®

3. Totals do not include Denver and Atlanta (included in state totals).

Saturday, February 12, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 2/12/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• The Impact on Housing of Higher Mortgage Rates

• 2nd Look at Local Housing Markets in January Adding Houston, Memphis, Nashville, New Hampshire, North Texas and Portland

• Black Knight Mortgage Monitor for December "Worst affordability levels since 2008"

• 1st Look at Local Housing Markets in January Denver: "the market ended with ... over 10 times less inventory than normal"

This is usually published several times a week, and provides more in-depth analysis of the housing market.

The blog will continue as always!

You can subscribe at https://calculatedrisk.substack.com/ Most content is available for free, but please subscribe!.

You can subscribe at https://calculatedrisk.substack.com/ Most content is available for free, but please subscribe!.

Schedule for Week of February 13, 2022

by Calculated Risk on 2/12/2022 08:11:00 AM

The key reports this week are January Housing Starts, Retail sales and Existing Home sales.

For manufacturing, the January Industrial Production report, and the February NY and Philly Fed manufacturing surveys will be released this week.

No major economic releases scheduled.

8:30 AM ET: The Producer Price Index for December from the BLS. The consensus is for a 0.5% increase in PPI, and a 0.5% increase in core PPI.

8:30 AM: The New York Fed Empire State manufacturing survey for February. The consensus is for a reading of 12.0, up from -0.7.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

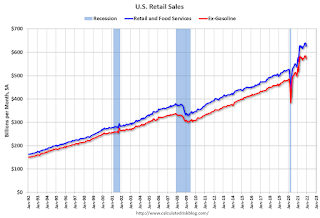

8:30 AM: Retail sales for January is scheduled to be released. The consensus is for a 1.8% increase in retail sales.

8:30 AM: Retail sales for January is scheduled to be released. The consensus is for a 1.8% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were down 2.0% in December.

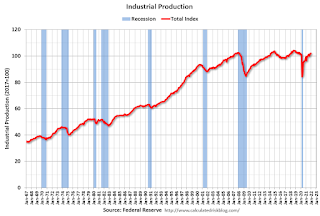

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.This graph shows industrial production since 1967.

The consensus is for a 0.4% increase in Industrial Production, and for Capacity Utilization to increase to 76.7%.

10:00 AM: The February NAHB homebuilder survey. The consensus is for a reading of 82, down from 83. Any number above 50 indicates that more builders view sales conditions as good than poor.

2:00 PM: FOMC Minutes, Meeting of Jan. 25-26

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a decrease to 222 thousand from 223 thousand last week.

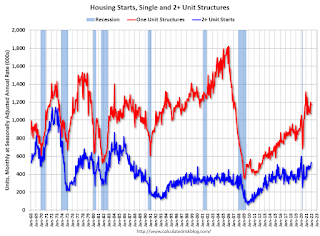

8:30 AM: Housing Starts for January.

8:30 AM: Housing Starts for January. This graph shows single and multi-family housing starts since 1968.

The consensus is for 1.700 million SAAR, down from 1.702 million SAAR.

8:30 AM: the Philly Fed manufacturing survey for February. The consensus is for a reading of 20.0, down from 23.2.

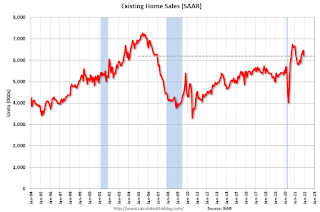

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 6.12 million SAAR, down from 6.18 million.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 6.12 million SAAR, down from 6.18 million.The graph shows existing home sales from 1994 through the report last month.

Friday, February 11, 2022

COVID Update: February 11, 2022: Falling Cases, Deaths and Hospitalizations

by Calculated Risk on 2/11/2022 10:03:00 PM

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 64.3% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 213.6 | --- | ≥2321 | |

| New Cases per Day3 | 190,401 | 344,320 | ≤5,0002 | |

| Hospitalized3 | 95,642 | 121,845 | ≤3,0002 | |

| Deaths per Day3 | 2,305 | 2,419 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of positive tests reported.

Lawler: Deaths by Age

by Calculated Risk on 2/11/2022 05:01:00 PM

From housing economist Tom Lawler: (CR Note: This is valuable demographic data)

Provisional data from the CDC indicate that there have been 3,427,882 US deaths reported for 2021 as of 2/9/2022, up from 3,383,729 deaths in 2020. Because of reporting delays in some parts of the country the 2021 final death numbers will be a little bit higher that the numbers in the 2/9 report.

CDC also reports provisional death counts by age groups, and below is a table showing 2021 deaths reported so far by age compared to final death counts by age for 2020 and 2019.

Missing Workers by Age Group

by Calculated Risk on 2/11/2022 02:09:00 PM

Note: This is an update to an earlier post.

Back in November, Goldman Sachs economists put out a research note on the labor force participation rate: Why Isn’t Labor Force Participation Recovering?

Here are few excerpts from the note:

Click on graph for larger image.

Click on graph for larger image.

This data is comparing January 2022 to January 2020, using Not Seasonally Adjusted (NSA) data (I compared to January 2020 to minimize the seasonal impact when using NSA data).

While the unemployment rate continues to fall quickly, labor force participation has made no progress since August 2020. ... Most of the 5.0mn persons who have exited the labor force since the start of the pandemic are over age 55 (3.4mn), largely reflecting early (1.5mn) and natural (1mn) retirements that likely won’t reverse. The outlook for prime-age persons who have exited the labor force (1.7mn) is more positive, since very few are discouraged and most still view their exits as temporary.

First, there are two important monthly surveys from the BLS. The participation rate (and unemployment rate) comes from the Current Population Survey (CPS: commonly called the household survey), a monthly survey of about 60,000 households.

The jobs number comes from Current Employment Statistics (CES: payroll survey), a sample of approximately 634,000 business establishments nationwide.

These are very different surveys: the CPS gives the total number of employed (and unemployed including the alternative measures), and the CES gives the total number of positions (excluding some categories like the self-employed, and a person working two jobs counts as two positions).

The jobs number comes from Current Employment Statistics (CES: payroll survey), a sample of approximately 634,000 business establishments nationwide.

These are very different surveys: the CPS gives the total number of employed (and unemployed including the alternative measures), and the CES gives the total number of positions (excluding some categories like the self-employed, and a person working two jobs counts as two positions).

Currently the payroll survey shows there are 2.9 million fewer jobs than in February 2020 (pre-pandemic).

The household survey shows there are 1.7 million fewer people employed than in February 2020.

Note: The 5 million number for the labor force, probably assumes some normal labor force growth; however, overall population growth has been dismal over the last 2 years (little immigration and large number of deaths). I'm not confident in Goldman's 5-million-person estimate.

Here is a graph of the number of missing people by age group (from the CPS household survey).

Click on graph for larger image.This data is comparing January 2022 to January 2020, using Not Seasonally Adjusted (NSA) data (I compared to January 2020 to minimize the seasonal impact when using NSA data).

Positive numbers are missing workers.

Almost all of the missing employed workers - by this method - are in the 25 to 29 and 45 to 49 age groups, and most are women.

Note: this is over a 2-year period, and there have been some demographic shifts between cohorts.

This data would suggest most of the missing workers are prime age (or some took early retirement).

Almost all of the missing employed workers - by this method - are in the 25 to 29 and 45 to 49 age groups, and most are women.

Note: this is over a 2-year period, and there have been some demographic shifts between cohorts.

This data would suggest most of the missing workers are prime age (or some took early retirement).