RSS Feed

RSS Feed by Calculated Risk on 3/04/2022 08:44:00 AM

Friday, March 04, 2022

February Employment Report: 678 thousand Jobs, 3.8% Unemployment Rate

From the BLS:

Total nonfarm payroll employment rose by 678,000 in February, and the unemployment rate edged down to 3.8 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, health care, and construction.

The change in total nonfarm payroll employment for December was revised up by 78,000, from +510,000 to +588,000, and the change for January was revised up by 14,000, from +467,000 to +481,000. With these revisions, employment in December and January combined is 92,000 higher than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the year-over-year change in total non-farm employment since 1968.

In February, the year-over-year change was 6.67 million jobs. This was up significantly year-over-year.

Total payrolls increased by 678 thousand in February. Private payrolls increased by 654 thousand, and public payrolls increased 24 thousand.

Payrolls for December and January were revised up 92 thousand, combined.

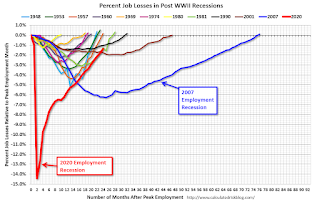

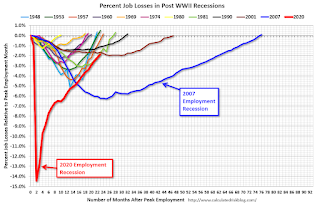

The second graph shows the job losses from the start of the employment recession, in percentage terms.

The second graph shows the job losses from the start of the employment recession, in percentage terms.The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 24 months after the onset, is now significantly better than the worst of the "Great Recession".

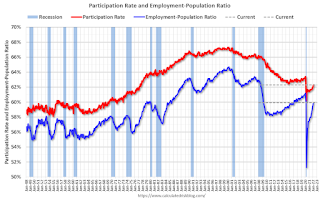

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.3% in February, from 62.2% in January. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.3% in February, from 62.2% in January. This is the percentage of the working age population in the labor force. The Employment-Population ratio increased to 59.9% from 59.7% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

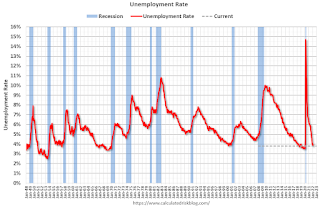

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate decreased in February to 3.8% from 4.0% in January.

This was above consensus expectations; and November and December payrolls were revised up by 92,000 combined.

I'll have more later ...

Thursday, March 03, 2022

Friday: February Employment Report

by Calculated Risk on 3/03/2022 09:08:00 PM

My February Employment Preview

Goldman February Payrolls Preview

Friday:

• At 8:30 AM ET, Employment Report for February. The consensus is for 400,000 jobs added, and for the unemployment rate to decrease to 3.9%.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 65.0% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 215.9 | --- | ≥2321 | |

| New Cases per Day3 | 53,016 | 74,143 | ≤5,0002 | |

| Hospitalized3 | 38,175 | 54,307 | ≤3,0002 | |

| Deaths per Day3 | 1,558 | 1,711 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

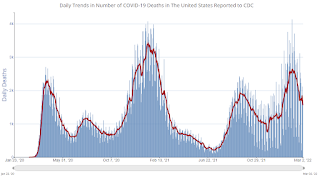

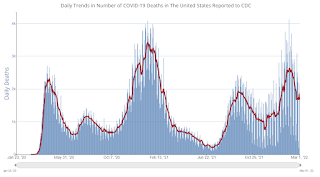

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Goldman February Payrolls Preview

by Calculated Risk on 3/03/2022 04:28:00 PM

A few brief excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls rose by 500k in February (mom sa), above consensus of +400k. Our forecast assumes the return of roughly 200k payroll workers who missed work in January due to Omicron. ... We estimate a two-tenths drop in the unemployment rate to 3.8%—compared to consensus of 3.9%.CR Note: The consensus is for 400 thousand jobs added, and for the unemployment rate to decline to 3.9%.

emphasis added

Hotels: Occupancy Rate Down 5% Compared to Same Week in 2019

by Calculated Risk on 3/03/2022 01:35:00 PM

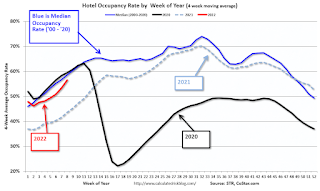

U.S. hotel performance increased from the previous week and showed significant improvement against 2019 comparables, according to STR‘s latest data through Feb. 26.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Feb. 20-26, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 62.2% (-4.7%)

• Average daily rate (ADR): $143.83 (+13.1%)

• Revenue per available room (RevPAR): $89.45 (+7.7%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021.

The 4-week average of the occupancy rate is below the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase seasonally over the next few months.

February Employment Preview

by Calculated Risk on 3/03/2022 11:25:00 AM

On Friday at 8:30 AM ET, the BLS will release the employment report for February. The consensus is for 400,000 jobs added, and for the unemployment rate to decrease to 3.9%.

Click on graph for larger image.

Click on graph for larger image.• First, currently there are still about 2.9 million fewer jobs than in February 2020 (before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 23 months after the onset, is now significantly better than the worst of the "Great Recession".

• ADP Report: The ADP employment report showed a gain of 475,000 private sector jobs, well above the consensus estimates of 320,000 jobs added. The ADP report hasn't been very useful in predicting the BLS report, but this suggests the BLS report could be above expectations.

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in February to 52.9%, down from 54.5% last month. This would suggest no change in manufacturing employment in February. ADP showed 30,000 manufacturing jobs gained.

The ISM® Services employment index decreased in February to 48.5%, down from 52.3% last month. This would suggest a 30 thousand increase in service employment in February. Combined, the ISM indexes suggest employment well below the consensus estimate.

• Unemployment Claims: The weekly claims report showed a decrease in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 290,000 in January to 249,000 in February. This would usually suggest fewer layoffs in February than in January, although this might not be very useful right now. In general, weekly claims were close to expectations in February.

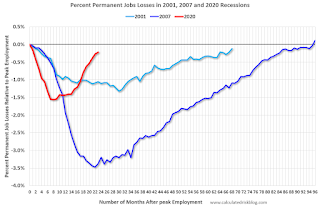

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the January report.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the January report.This data is only available back to 1994, so there is only data for three recessions. In January, he number of permanent job losers decreased to 1.630 million from 1.703 million the previous month.

These jobs will likely be the hardest to recover, so it is a positive that the number of permanent job losers is declining fairly rapidly.

• COVID: As far as the pandemic, the number of daily cases during the reference week in February was around 200,000, down sharply from around 800,000 in January. The current wave peaked during the January reference week, and declined in February

• Conclusion: There is optimism concerning the February employment report due to the sharp decline in COVID cases. Overall, the ADP report was solid, and unemployment claims decreased during the reference week. However, the ISM employment surveys were weak in February. My sense is the report will be below consensus expectations.

ISM® Services Index Decreased to 56.5% in February

by Calculated Risk on 3/03/2022 10:04:00 AM

(Posted with permission). The ISM® Services index was at 56.5%, down from 59.9% last month. The employment index decreased to 48.5%, from 52.3%. Note: Above 50 indicates expansion, below 50 in contraction.

From the Institute for Supply Management: Services PMI® at 56.5% February 2022 Services ISM® Report On Business®

Economic activity in the services sector grew in February for the 21st month in a row — with the Services PMI® registering 56.5 percent — say the nation’s purchasing and supply executives in the latest Services ISM® Report On Business®.The employment index decreased to 48.5%, from 52.3% the previous month.

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee: “In February, the Services PMI® registered 56.5 percent, 3.4 percentage points below January's reading of 59.9 percent. The Business Activity Index registered 55.1 percent, a decrease of 4.8 percentage points compared to the reading of 59.9 percent in January, and the New Orders Index figure of 56.1 percent is 5.6 percentage points lower than the January reading of 61.7 percent.

emphasis added

Weekly Initial Unemployment Claims Decrease to 215,000

by Calculated Risk on 3/03/2022 08:35:00 AM

The DOL reported:

In the week ending February 26, the advance figure for seasonally adjusted initial claims was 215,000, a decrease of 18,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 232,000 to 233,000. The 4-week moving average was 230,500, a decrease of 6,000 from the previous week's revised average. The previous week's average was revised up by 250 from 236,250 to 236,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 230,500.

The previous week was revised up.

Weekly claims were lower than the consensus forecast.

Wednesday, March 02, 2022

Thursday: Fed Chair Powell Testimony, Unemployment Claims, ISM Services

by Calculated Risk on 3/02/2022 08:32:00 PM

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for a decrease to 230 thousand from 232 thousand last week.

• At 10:00 AM, Testimony, Fed Chair Jerome Powell, Semiannual Monetary Policy Report to the Congress, Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate

• Also at 10:00 AM, the ISM Services Index for February.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 65.0% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 215.8 | --- | ≥2321 | |

| New Cases per Day3 | 56,253 | 81,212 | ≤5,0002 | |

| Hospitalized3 | 40,190 | 56,955 | ≤3,0002 | |

| Deaths per Day3 | 1,674 | 1,687 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Fed's Beige Book: "Supply chain issues and low inventories continued to restrain growth"

by Calculated Risk on 3/02/2022 02:03:00 PM

Fed's Beige Book "This report was prepared at the Federal Reserve Bank of St. Louis based on information collected on or before February 18, 2022. "

Economic activity has expanded at a modest to moderate pace since mid-January. Many Districts reported that the surge in COVID-19 cases temporarily disrupted business activity as firms faced heighted absenteeism. Some Districts attributed a temporary weakening in demand in the hospitality sector to the rise in cases. Severe winter weather was also cited as disrupting activity. As a result, consumer spending was generally weaker than in the prior report. Reports on auto sales were mixed. Manufacturing activity continued to grow at a modest pace. All Districts noted that supply chain issues and low inventories continued to restrain growth, particularly in the construction sector. Reports from banking contacts indicated some weakening of financial conditions, although loan demand was generally unchanged. Demand for residential real estate was generally strong, although many Districts reported no change in home sales due to seasonal trends and low inventories. Agriculture reports were somewhat mixed, as some Districts experienced difficult growing conditions while others benefited from higher crop prices. Reports on the energy sector indicated modest growth. Among reporting Districts, the overall economic outlook over the next six months remained stable and generally optimistic, although reports highlighted an elevated degree of uncertainty.

...

Employment increased at a modest to moderate pace. Widespread strong demand for workers remained hampered by equally widespread reports of worker scarcity, though some Districts reported scattered signs of improving labor supply. Many firms had difficulty maintaining their staffing levels due to high turnover; this challenge was exacerbated by COVID-19 disruptions in January, though workers and firms recovered more quickly than during previous waves. Firms continued to increase compensation and introduce workplace flexibility to attract workers—especially in historically low-wage positions—with mixed success. Contacts reported they expect the tight labor market and consequent strong wage growth to continue, though a few Districts reported signs of wage growth moderating.

emphasis added

The War and Mortgage Rates

by Calculated Risk on 3/02/2022 12:57:00 PM

Today, in the Calculated Risk Real Estate Newsletter: The War and Mortgage Rates

A brief excerpt:

The invasion of Ukraine has clouded the economic outlook (of course, the economic outlook is inconsequential compared to the ongoing human suffering in Ukraine). Fed Chair Pro Tempore Powell said today:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/The near-term effects on the U.S. economy of the invasion of Ukraine, the ongoing war, the sanctions, and of events to come, remain highly uncertain.And in the Q&A, Powell said about the March FOMC meeting:"I am inclined to propose and support a 25 basis point rate hike"...Key points:

• The invasion is leading to significant uncertainty.

• Mortgage rates haven’t fallen as fast as Treasury yields.

• The Fed is still going to raise rates in March.