RSS Feed

RSS Feed by Calculated Risk on 4/14/2022 08:45:00 AM

Thursday, April 14, 2022

Retail Sales Increased 0.5% in March

On a monthly basis, retail sales were increased 0.5% from February to March (seasonally adjusted), and sales were up 6.9 percent from March 2021.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for March 2022, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $665.7 billion, an increase of 0.5 percent from the previous month, and 6.9 percent above March 2021. ... The January 2022 to February 2022 percent change was revised from up 0.3 percent to up 0.8 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were down 0.3% in March.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 4.4% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 4.4% on a YoY basis.Sales growth in March was slightly below expectations, however, sales in January and February were revised up, combined.

Weekly Initial Unemployment Claims Increase to 185,000

by Calculated Risk on 4/14/2022 08:34:00 AM

The DOL reported:

In the week ending April 9, the advance figure for seasonally adjusted initial claims was 185,000, an increase of 18,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 166,000 to 167,000. The 4-week moving average was 172,250, an increase of 2,000 from the previous week's revised average. The previous week's average was revised up by 250 from 170,000 to 170,250.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 170,000.

The previous week was revised up.

Weekly claims were well above the consensus forecast.

Wednesday, April 13, 2022

Thursday: Retail Sales, Unemployment Claims

by Calculated Risk on 4/13/2022 09:46:00 PM

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for a increase to 175 thousand from 166 thousand last week.

• At 8:30 AM, Retail sales for March is scheduled to be released. The consensus is for a 0.6% increase in retail sales.

• At 10:00 AM, University of Michigan's Consumer sentiment index (Preliminary for April).

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 65.8% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 218.5 | --- | ≥2321 | |

| New Cases per Day3🚩 | 29,401 | 26,563 | ≤5,0002 | |

| Hospitalized3 | 9,674 | 10,590 | ≤3,0002 | |

| Deaths per Day3 | 452 | 517 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

New cases are increasing.

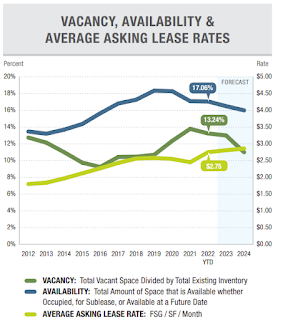

Office Vacancy Rates for Two SoCal Counties

by Calculated Risk on 4/13/2022 02:05:00 PM

Voit released their Q1 CRE reports today. These reports are for several cities in the west (these are for several categories of CRE - offices, retail, industrial). There is plenty of detail for those interested in Commercial Real Estate.

Overall vacancy rates are not that much higher than prior to the pandemic and asking lease rates have continued to increase.

The following graphs show vacancy rate and lease rates for offices in Orange County and San Diego.

Click on graph for larger image.

Click on graph for larger image.

The first graph is from Voit for Orange County (not labeled). From Voit: The 2nd graph is for San Diego.

The 2nd graph is for San Diego.

From Voit:

The following graphs show vacancy rate and lease rates for offices in Orange County and San Diego.

Click on graph for larger image.

Click on graph for larger image.The first graph is from Voit for Orange County (not labeled). From Voit:

The office market really suffered during the worst of the pandemic, as the initial lockdown essentially shut it down in Q2 of 2020 and the majority of office workers scrambled to adapt to technologies that allowed them to work from home. Ongoing safety protocols made it is especially difficult for building owners and office-centric business owners to get people back in the office. Even today, with the worst of the health crisis behind us, less than half of office workers are back at their desks on a regular basis. High-rise and mid-rise buildings are facing the biggest challenge because of employee density and dependence on elevators for access to individual spaces. Add the fact that many businesses are considering long-term adoption of a work-from-home or hybrid model for their workforces, and it is easy to see that the office market still has some major challenges to overcome.

...

After two years of consistent upward pressure on vacancy, the overall rate in Q1 actually declined by a substantial margin, shedding 55 basis points to end the period at 13.24%. That’s just 9 basis points higher than it was in Q1 of 2021, further evidence that the market is stabilizing.

The 2nd graph is for San Diego.

The 2nd graph is for San Diego.From Voit:

The office market started 2022 on a bright note with leasing in line with historical norms for the first time since the onset of COVID. Fundamental metrics point towards a healthy office market in 1Q with positive net absorption, rising rental rates, and a decrease in the availability rate. The current health of the office market is being buoyed by the rapid expansion of San Diego’s biotech industry.

How High will Mortgage Rates Rise?

by Calculated Risk on 4/13/2022 11:05:00 AM

Today, in the Calculated Risk Real Estate Newsletter: How High will Mortgage Rates Rise?

A brief excerpt:

Currently most forecasts are for the Fed Funds rate to rise to around 3.25%. Goldman Sach’s chief economist Jan Hatzius recently said he thinks the Fed may have to raise rates above 4%, although their baseline forecast is just about 3%.There is much more in the article. You can subscribe at Calculated Risk Real Estate Newsletter

When the Fed Funds rate peaks in this cycle, the yield curve will likely be fairly flat - meaning the 10-year treasury yield will be at about the same level as the Fed Funds rate. Based on the current estimate for the peak Fed Funds rate (3.25% to 4.0%), the 30-year fixed mortgage will likely peak at between 5.0% and 5.7%. There is some variability in the relationship, so we might see rates as high as the low 6% range. (This all depends on inflation and the Fed Funds rate - but I don’t expect rates to move much higher than the current rate - although 6% is possible).

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 4/13/2022 07:00:00 AM

Mortgage applications decreased 1.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 8, 2022.

... The Refinance Index decreased 5 percent from the previous week and was 62 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 6 percent lower than the same week one year ago.

“Mortgage rates across all loan types continued to move higher, with the 30-year fixed rate exceeding the 5-percent mark to 5.13 percent – the highest since November 2018. Refinance activity as a result declined to the slowest weekly pace since 2019,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “Higher rates are increasing borrower interest in ARMs. Their share of applications last week was at 7.4 percent, which was the highest share since June 2019. In a promising sign of strong purchase demand amidst affordability challenges, both conventional and government purchase applications increased.”

Given the faster than expected increase in mortgage rates, and the likelihood of more aggressive actions from the Federal Reserve to curb inflation, MBA’s April 2022 forecast now calls for mortgage originations to total $2.58 trillion in 2022 – a 35.5 percent decline from 2021. Purchase originations are still forecasted to reach a record $1.72 trillion this year – a 4 percent increase from 2021. Refinance originations are now expected to fall 64 percent to $841 billion.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.13 percent from 4.90 percent, with points increasing to 0.63 from 0.53 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply over the last several months.

The refinance index is at the lowest level since March 2019.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 6% year-over-year unadjusted.

According to the MBA, purchase activity is down 6% year-over-year unadjusted.Note: Red is a four-week average (blue is weekly).

Tuesday, April 12, 2022

Wednesday: PPI

by Calculated Risk on 4/12/2022 09:41:00 PM

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, The Producer Price Index for March from the BLS. The consensus is for a 1.1% increase in PPI, and a 0.5% increase in core PPI.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 65.8% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 218.5 | --- | ≥2321 | |

| New Cases per Day3🚩 | 30,496 | 25,208 | ≤5,0002 | |

| Hospitalized3 | 9,704 | 10,807 | ≤3,0002 | |

| Deaths per Day3 | 507 | 540 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

New cases are increasing again.

2nd Look at Local Housing Markets in March

by Calculated Risk on 4/12/2022 03:02:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in March

A brief excerpt:

Here is a summary of active listings for these housing markets in March. Note: Inventory usually increases seasonally in March, so the month-over-month (MoM) increase is not surprising.There is much more in the article. You can subscribe at Calculated Risk Real Estate Newsletter

Inventory was up 9.3% in March MoM from February, and down 13.4% year-over-year (YoY). Inventory in about half of these markets was up YoY.

It appears inventory bottomed in February. Last month, these markets were down 23.3% YoY, so this is a significant change from February. This is the first step towards a more balanced market, but inventory levels are still very low.

Notes for all tables:

1) New additions to table in BOLD.

2) Northwest (Seattle) and Santa Clara (San Jose), Jacksonville, Source: Northeast Florida Association of REALTORS®

3) Totals do not include Atlanta or Denver (included in state totals).

Cleveland Fed: Median CPI increased 0.5% and Trimmed-mean CPI increased 0.5% in March

by Calculated Risk on 4/12/2022 11:09:00 AM

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.5% in March. The 16% trimmed-mean Consumer Price Index also increased 0.5% in March. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Note: The Cleveland Fed released the median CPI details here: "Used Cars" were down 37% annualized in March, and this will likely show further declines in coming months. Motor fuel was up 648% annualized in March!

Note that Owners' Equivalent Rent and Rent of Primary Residence account for almost 1/3 of median CPI, and these measures were up around 5% to 6% annualized in March.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation.

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 4.9%, the trimmed-mean CPI rose 6.1%, and the CPI less food and energy rose 6.5%. Core PCE is for February and increased 5.4% year-over-year.

BLS: CPI increased 1.2% in March; Core CPI increased 0.3%

by Calculated Risk on 4/12/2022 08:33:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 1.2 percent in March on a seasonally adjusted basis after rising 0.8 percent in February, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 8.5 percent before seasonal adjustment.CPI was at expectations and core CPI was lower than expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

Increases in the indexes for gasoline, shelter, and food were the largest contributors to the seasonally adjusted all items increase. The gasoline index rose 18.3 percent in March and accounted for over half of the all items monthly increase; other energy component indexes also increased. The food index rose 1.0 percent and the food at home index rose 1.5 percent.

The index for all items less food and energy rose 0.3 percent in March following a 0.5-percent increase the prior month. The shelter index was by far the biggest factor in the increase, with a broad set of other indexes also contributing, including those for airline fares, household furnishings and operations, medical care, and motor vehicle insurance. In contrast, the index for used cars and trucks fell 3.8 percent over the month.

The all items index continued to accelerate, rising 8.5 percent for the 12 months ending March, the largest 12-month increase since the period ending December 1981. The all items less food and energy index rose 6.5 percent, the largest 12-month change since the period ending August 1982. The energy index rose 32.0 percent over the last year, and the food index increased 8.8 percent, the largest 12-month increase since the period ending May 1981.

emphasis added