RSS Feed

RSS Feed by Calculated Risk on 5/02/2022 10:05:00 AM

Monday, May 02, 2022

ISM® Manufacturing index Decreased to 55.4% in April

(Posted with permission). The ISM manufacturing index indicated expansion. The PMI® was at 55.4% in April, down from 57.1% in March. The employment index was at 50.9%, down from 56.3% last month, and the new orders index was at 53.5%, down from 53.8%.

From ISM: Manufacturing PMI® at 55.4% April 2022 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector grew in April, with the overall economy achieving a 23rd consecutive month of growth, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.This suggests manufacturing expanded at a slower pace in April than in March. This was below the consensus forecast, and the employment index was weak in April.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee:

“The April Manufacturing PMI® registered 55.4 percent, a decrease of 1.7 percentage points from the March reading of 57.1 percent. This figure indicates expansion in the overall economy for the 23rd month in a row after a contraction in April and May 2020. This is the lowest reading since July 2020 (53.9 percent). The New Orders Index registered 53.5 percent, down 0.3 percentage point compared to the March reading of 53.8 percent. The Production Index reading of 53.6 percent is a 0.9-percentage point decrease compared to March’s figure of 54.5 percent. The Prices Index registered 84.6 percent, down 2.5 percentage points compared to the March figure of 87.1 percent. The Backlog of Orders Index registered 56 percent, 4 percentage points lower than the March reading of 60 percent. The Employment Index figure of 50.9 percent is 5.4 percentage points lower than the 56.3 percent recorded in March. The Supplier Deliveries Index registered 67.2 percent, an increase of 1.8 percentage points compared to the March figure of 65.4 percent. The Inventories Index registered 51.6 percent, 3.9 percentage points lower than the March reading of 55.5 percent. The New Export Orders Index reading of 52.7 percent is down 0.5 percentage point compared to March’s figure of 53.2 percent. The Imports Index registered 51.4 percent, a 0.4-percentage point decrease from the March reading of 51.8 percent.”

emphasis added

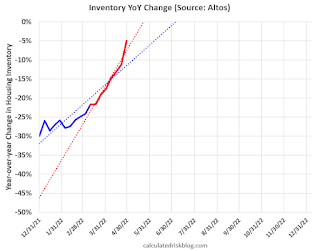

Housing Inventory May 2nd Update: Inventory Down 4.9% Year-over-Year

by Calculated Risk on 5/02/2022 08:41:00 AM

Tracking existing home inventory is very important in 2022.

Inventory usually declines in the winter, and then increases in the spring. Inventory bottomed seasonally at the beginning of March 2022 and is now up 21.2% since then.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of April 29th, inventory was at 292 thousand (7-day average), compared to 275 thousand the prior week. Inventory was up 6.2% from the previous week.

Last year inventory bottomed seasonally in April 2021 - very late in the year. This year, by this measure, inventory bottomed seasonally at the beginning of March.

Inventory is still very low. Compared to the same week in 2021, inventory is down 4.9% from 307 thousand, but compared to the same week in 2020, and inventory is down 60.4% from 738 thousand.

Last year inventory bottomed seasonally in April 2021 - very late in the year. This year, by this measure, inventory bottomed seasonally at the beginning of March.

Inventory is still very low. Compared to the same week in 2021, inventory is down 4.9% from 307 thousand, but compared to the same week in 2020, and inventory is down 60.4% from 738 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (already happened on March 4th for Altos)✅

2. Inventory up year-over-year (likely very soon)

3. Inventory up compared to two years ago (currently down 60% according to Altos)

4. Inventory back to 1999 levels (currently down 67%).

For the second milestone, here is a table of the year-over-year change by week since the beginning of the year.

1. The seasonal bottom (already happened on March 4th for Altos)✅

2. Inventory up year-over-year (likely very soon)

3. Inventory up compared to two years ago (currently down 60% according to Altos)

4. Inventory back to 1999 levels (currently down 67%).

For the second milestone, here is a table of the year-over-year change by week since the beginning of the year.

| Week Ending | YoY Change |

|---|---|

| 12/31/2021 | -30.0% |

| 1/7/2022 | -26.0% |

| 1/14/2022 | -28.6% |

| 1/21/2022 | -27.1% |

| 1/28/2022 | -25.9% |

| 2/4/2022 | -27.9% |

| 2/11/2022 | -27.5% |

| 2/18/2022 | -25.8% |

| 2/25/2022 | -24.9% |

| 3/4/2022 | -24.2% |

| 3/11/2022 | -21.7% |

| 3/18/2022 | -21.7% |

| 3/25/2022 | -19.0% |

| 4/1/2022 | -17.6% |

| 4/8/2022 | -14.8% |

| 4/15/2022 | -13.1% |

| 4/22/2022 | -11.2% |

| 4/29/2022 | -4.9% |

Here is a graph of the year-over-year change in the Altos data.

The blue trend line is from the beginning of the year, and the red trend line is over the last 8 weeks.

Currently it appears inventory will be up year-over-year soon.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 5/02/2022 08:07:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Note: Apple has discontinued "Apple mobility", and restaurant traffic is mostly back to normal.

The TSA is providing daily travel numbers.

This data is as of May 1st.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 9.7% from the same day in 2019 90.3% of 2019). (Dashed line)

Air travel has been moving sideways over the last month, off about 10% from 2019.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through April 28th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $121 million last week, down about 23% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $121 million last week, down about 23% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021.

This data is through April 23rd. The occupancy rate was down 4.2% compared to the same week in 2019.

The 4-week average of the occupancy rate is at the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will now mostly move sideways seasonally until the summer.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider. This graph shows how much MTA traffic has recovered in each borough (Graph starts at first week in January 2020 and 100 = 2019 average).

Manhattan is at about 38% of normal.

This data is through Friday, April 29th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, May 01, 2022

Monday: ISM Mfg, Construction Spending

by Calculated Risk on 5/01/2022 06:40:00 PM

Weekend:

• Schedule for Week of May 1, 2022

• FOMC Preview: 50bp Rate Hike, Announce "commencement of balance sheet runoff"

• Housing: "What Killed the Home ATM in 2006?"

Monday:

• At 10:00 AM ET, ISM Manufacturing Index for April. The consensus is for the ISM to be at 57.6, up from 57.1 in March.

• Also at 10:00 AM, Construction Spending for March. The consensus is for a 0.7% increase in construction spending.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are down slightly (fair value).

Oil prices were up over the last week with WTI futures at $104.58 per barrel and Brent at $106.73 per barrel. A year ago, WTI was at $64 and Brent was at $68 - so WTI oil prices are up over 60% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $4.17 per gallon. A year ago prices were at $2.89 per gallon, so gasoline prices are up $1.28 per gallon year-over-year.

Housing: "What Killed the Home ATM in 2006?"

by Calculated Risk on 5/01/2022 02:21:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Housing: "What Killed the Home ATM in 2006?"

Excerpt:

A reader (ht SV) asked an interesting question: What killed the Home ATM in 2006?

First, the “Home ATM” is a joking reference to mortgage equity withdrawal (MEW), where homeowners extract equity from their homes - like a cash-out refinance or with a Home Equity Line of Credit (HELOC).

In this post, I’ll compare MEW for the current period to both the housing bubble and the 1978 to 1982 period. In Housing: Don't Compare the Current Housing Boom to the Bubble and Bust, I pointed out that demographics, lending standards, and the Fed fighting inflation are similar to the 1978 to 1982 period, and dissimilar to the housing bubble - and I suggested that we look to the 1980 for parallels to the current boom and coming housing slowdown (not the bubble).

...

The following graph shows the net equity extraction, or mortgage equity withdrawal (MEW), results, using the Flow of Funds (and BEA data) compared to the Kennedy-Greenspan method.

Note that MEW (as a percent of DPI) was at about the same level in 1980 as today and is well below the peak bubble years.

...

So, this is another reason - along with similar demographics, lending standards, and concerns about inflation - to compare the current housing market to the 1978 to 1982 period, and not to the housing bubble. (Of course, there are differences too).

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

FOMC Preview: 50bp Rate Hike, Announce "commencement of balance sheet runoff"

by Calculated Risk on 5/01/2022 08:11:00 AM

Expectations are the FOMC will announce a 50bp rate increase in the federal funds rate at the meeting this week and probably also announce the "commencement of balance sheet runoff".

From Merrill Lynch:

1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 3.6% in March. The question is: Will the slowdown in economic growth push up the unemployment rate? Or will the rate continue to decline?

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of March 2022, PCE inflation was up 6.6% from March 2021. This was a new cycle high. With the ongoing negative impacts on the supply chain, and on energy and food costs from the war, inflation might stay elevated longer than expected.

PCE core inflation was up 5.2% in March year-over-year. This was slightly below the February YoY increase, but it is too early to say the core inflation has peaked.

"The Fed has signaled a major hawkish shift at this meeting, and we expect them to deliver, with a 50bp rate increase and the announcement of Quantitative Tightening (QT) starting in June.From Goldman Sachs:

...

On QT, the minutes of the March FOMC meeting detailed the plans for reducing the size of the balance sheet, indicating general agreement behind monthly caps of $60bn for Treasuries and $35bn for agency MBS phased in over three months or more. These finalized details clear the way for QT to be announced at this meeting, with starting monthly caps of $20bn for Treasuries and $10bn for agency MBS. Importantly, our US rates strategy team believes QT implementation will actually begin with a lag in June."

"Policy actions at the May FOMC meeting seem set after Chair Powell and other FOMC members strongly suggested that they intend to raise the policy rate by 50bp and announce the start of balance sheet reduction.

The key question is therefore what comes next. We forecast another 50bp hike in June followed by a deceleration to a 25bp/meeting pace of tightening for the rest of 2022, but see reasonably high chances that the FOMC will continue to hike in 50bp increments until reaching their median neutral rate estimate of 2.25-2.5%. We will therefore be paying close attention to any comments from Chair Powell at the press conference that suggest the FOMC intends to hike in 50bp increments beyond June."

Analysts will be looking for comments on the size of future rate hikes, the pace of the runoff of assets (not reinvesting), and comments on selling MBS in the future.

Note: No projections will be released at this meeting. However, for review, here are the March projections. In March, most participants expected seven rate hikes in 2022.

Wall Street forecasts are being revised down for 2022 due to the ongoing negative supply chain impacts from the pandemic (see China), and the war in Ukraine. For example, Goldman Sachs is now forecasting a 1.6% increase in real GDP, Q4-over-Q4 for 2022, well below the FOMC projections in March.

Wall Street forecasts are being revised down for 2022 due to the ongoing negative supply chain impacts from the pandemic (see China), and the war in Ukraine. For example, Goldman Sachs is now forecasting a 1.6% increase in real GDP, Q4-over-Q4 for 2022, well below the FOMC projections in March.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 2.5 to 3.0 | 2.1 to 2.5 | 1.8 to 2.0 | |

| Dec 2021 | 3.6 to 4.5 | 2.0 to 2.5 | 1.8 to 2.0 | |

The unemployment rate was at 3.6% in March. The question is: Will the slowdown in economic growth push up the unemployment rate? Or will the rate continue to decline?

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 3.4 to 3.6 | 3.3 to 3.6 | 3.2 to 3.7 | |

| Dec 2021 | 3.4 to 3.7 | 3.2 to 3.6 | 3.2 to 3.7 | |

As of March 2022, PCE inflation was up 6.6% from March 2021. This was a new cycle high. With the ongoing negative impacts on the supply chain, and on energy and food costs from the war, inflation might stay elevated longer than expected.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 4.1 to 4.7 | 2.3 to 3.0 | 2.1 to 2.4 | |

| Dec 2021 | 2.2 to 3.0 | 2.1 to 2.5 | 2.0 to 2.2 | |

PCE core inflation was up 5.2% in March year-over-year. This was slightly below the February YoY increase, but it is too early to say the core inflation has peaked.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 3.9 to 4.4 | 2.4 to 3.0 | 2.1 to 2.4 | |

| Dec 2021 | 2.5 to 3.0 | 2.1 to 2.4 | 2.0 to 2.2 | |

Saturday, April 30, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 4/30/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Realtor.com Reports Weekly Inventory down only 6% Year-over-year

• Real House Prices, Price-to-Rent Ratio and Price-to-Median Income in February Worst "Affordability" since Housing Bubble

• March New Home Sales: Little Completed Inventory, High Number of Homes Under Construction

• Case-Shiller National Index up 19.8% Year-over-year in February; New Record Monthly Increase

• Housing and Demographics

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

The blog will continue as always!

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of May 1, 2022

by Calculated Risk on 4/30/2022 08:11:00 AM

The key report scheduled for this week is the April employment report.

Other key reports include April vehicle sales, and the March trade balance.

The FOMC meets this week, and the FOMC is expected to raise rates 50bp.

For manufacturing, the April ISM manufacturing index will be released.

10:00 AM ET: ISM Manufacturing Index for April. The consensus is for the ISM to be at 57.6, up from 57.1 in March.

10:00 AM: Construction Spending for March. The consensus is for a 0.7% increase in construction spending.

8:00 AM ET: Corelogic House Price index for March.

10:00 AM ET: Job Openings and Labor Turnover Survey for March from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for March from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings decreased slightly in February to 11.266 million from 11.283 million in January. The number of job openings (yellow) were up 43% year-over-year.

All day: Light vehicle sales for April. The expectation is for light vehicle sales to be 13.8 million SAAR in April, up from 13.36 million in March (Seasonally Adjusted Annual Rate).

All day: Light vehicle sales for April. The expectation is for light vehicle sales to be 13.8 million SAAR in April, up from 13.36 million in March (Seasonally Adjusted Annual Rate).This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the sales rate for the previous month.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for April. This report is for private payrolls only (no government). The consensus is for 395,000 payroll jobs added in April, down from 455,000 added in March.

8:30 AM: Trade Balance report for March from the Census Bureau.

8:30 AM: Trade Balance report for March from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $107.0 billion. The U.S. trade deficit was at $89.2 Billion in February.

10:00 AM: the ISM Services Index for April. The consensus is for a reading of 58.5, up from 58.3.

2:00 PM: FOMC Meeting Announcement. The FOMC is expected to raise the Fed Funds rate by 50bp at this meeting and announce "commencement of balance sheet runoff".

2:30 PM: Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 180 thousand unchanged from 180 thousand last week.

8:30 AM: Employment Report for April. The consensus is for 400,000 jobs added, and for the unemployment rate to be unchanged at 3.6%.

8:30 AM: Employment Report for April. The consensus is for 400,000 jobs added, and for the unemployment rate to be unchanged at 3.6%.There were 431,000 jobs added in February, and the unemployment rate was at 3.6%.

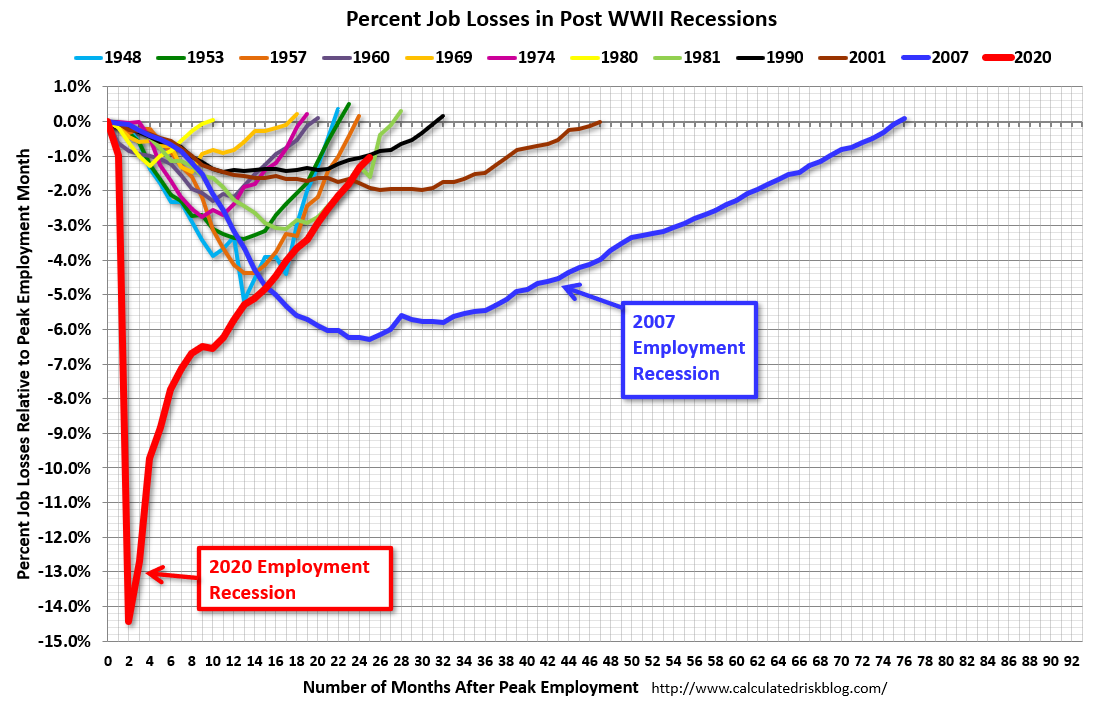

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 25 months after the onset, has recovered quicker than the previous two recessions.

Friday, April 29, 2022

COVID Update: Hospitalizations and New Cases Increasing

by Calculated Risk on 4/29/2022 10:17:00 PM

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.1% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 219.6 | --- | ≥2321 | |

| New Cases per Day3🚩 | 54,696 | 40,713 | ≤5,0002 | |

| Hospitalized3🚩 | 10,991 | 9,997 | ≤3,0002 | |

| Deaths per Day3 | 311 | 340 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Fannie Mae: Mortgage Serious Delinquency Rate Decreased in March

by Calculated Risk on 4/29/2022 04:09:00 PM

Fannie Mae reported that the Single-Family Serious Delinquency decreased to 1.01% in March from 1.11% in February. The serious delinquency rate is down from 2.58% in March 2021.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

Click on graph for larger image

Click on graph for larger image

By vintage, for loans made in 2004 or earlier (1% of portfolio), 3.12% are seriously delinquent (down from 3.30% in February).

For loans made in 2005 through 2008 (2% of portfolio), 5.14% are seriously delinquent (down from 5.46%),

For recent loans, originated in 2009 through 2021 (97% of portfolio), 0.81% are seriously delinquent (down from 0.89%). So, Fannie is still working through a few poor performing loans from the bubble years.

Mortgages in forbearance are counted as delinquent in this monthly report, but they will not be reported to the credit bureaus.

The pandemic related increase in delinquencies was very different from the increase in delinquencies following the housing bubble. Lending standards had been fairly solid over the previous decade, and most of these homeowners had equity in their homes - and the vast majority of these homeowners have been able to restructure their loans once they were employed.

Freddie Mac reported earlier.

Mortgages in forbearance are counted as delinquent in this monthly report, but they will not be reported to the credit bureaus.

The pandemic related increase in delinquencies was very different from the increase in delinquencies following the housing bubble. Lending standards had been fairly solid over the previous decade, and most of these homeowners had equity in their homes - and the vast majority of these homeowners have been able to restructure their loans once they were employed.

Freddie Mac reported earlier.