RSS Feed

RSS Feed by Calculated Risk on 6/23/2022 08:42:00 PM

Thursday, June 23, 2022

Friday: New Home Sales

Mortgage rates have fallen from 6.28% just over one week ago to 5.75% today.

Mortgage rates have fallen from 6.28% just over one week ago to 5.75% today.

Friday:

• At 10:00 AM ET, New Home Sales for May from the Census Bureau. The consensus is for 580 thousand SAAR, down from 591 thousand in April.

• Also, at 10:00 AM, University of Michigan's Consumer sentiment index (Final for June). The consensus is for a reading of 50.2.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.8% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.9 | --- | ≥2321 | |

| New Cases per Day3 | 97,430 | 103,175 | ≤5,0002 | |

| Hospitalized3🚩 | 24,831 | 24,358 | ≤3,0002 | |

| Deaths per Day3 | 255 | 285 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Fed: Banks Pass Annual Stress Test

by Calculated Risk on 6/23/2022 04:40:00 PM

From the Federal Reserve: Federal Reserve Board releases results of annual bank stress test, which show that banks continue to have strong capital levels, allowing them to continue lending to households and businesses during a severe recession

The Federal Reserve Board on Thursday released the results of its annual bank stress test, which showed that banks continue to have strong capital levels, allowing them to continue lending to households and businesses during a severe recession.Test results here.

All banks tested remained above their minimum capital requirements, despite total projected losses of $612 billion. Under stress, the aggregate common equity capital ratio—which provides a cushion against losses—is projected to decline by 2.7 percentage points to a minimum of 9.7 percent, which is still more than double the minimum requirement.

Realtor.com Reports Weekly Inventory Up 21% Year-over-year

by Calculated Risk on 6/23/2022 03:01:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released yesterday from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending June 18, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• New listings–a measure of sellers putting homes up for sale–were up 6% above one year ago. Home sellers in many markets across the country continue to benefit from rising home prices and fast-selling homes. That’s prompted a growing number of homeowners to sell homes this year compared to last, giving home shoppers much needed options. We’ve seen more homes come up for sale this year compared to last year in 11 of the last 12 weeks.

• Active inventory continued to grow, rising 21% above one year ago. Inventory was roughly even with last year’s levels at the beginning of May and the gains have mounted each week. Still, our May Housing Trends Report showed that the active listings count remained nearly 50 percent below its level at the beginning of the pandemic. In other words, we’re starting to add more options, but the market needs even more before home shoppers have a selection that’s roughly equivalent to the pre-pandemic housing market.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change, from down 30% at the beginning of the year, to up 21% YoY now. It will be important to watch if that trend continues.

Also note the possible pickup in new listings. This is something I highlighted in Final Look at Local Housing Markets in May

New Home Sales and Cancellations

by Calculated Risk on 6/23/2022 12:02:00 PM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales and Cancellations

Brief excerpt:

Here is a table of selected public builders and the currently reported cancellation rate (I’m still gathering data). There is some seasonality to cancellation rates. The only builder that reported a sharp increase recently was KB Home comparing the three months ended May 31, 2022, with the three months ended May 31, 2021.There is much more in the newsletter.“The cancellation rate as a percentage of gross orders was 17%, compared to 9%.”However, as KB Home noted on their conference call yesterday, a large portion of the increase in cancellations were on “unstarted homes”.

...

Currently cancellation rates are below normal for the home builders. As an example, Toll Brothers recently announced a cancellation rate of 3.8%, down from 4.3% the previous quarter, and well below their historical rate of 7%. During the housing bust, Toll Brothers cancellation rates peaked close to 40%.

You can subscribe at https://calculatedrisk.substack.com/.

June Vehicle Sales Forecast: Increase to 13.3 million SAAR

by Calculated Risk on 6/23/2022 10:11:00 AM

From WardsAuto: June U.S. Light-Vehicle Sales to Improve on May; Stay Softer than January-April (pay content). Brief excerpt:

"If the June forecast holds firm, volume will rise in Q2 from Q1, but the quarter will end at a 13.5-million-unit annualized rate, a drop from January-March’s 14.1 million ..."

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for June (Red).

The Wards forecast of 13.4 million SAAR, would be up about 5% from last month, and down 14% from a year ago (sales were starting to weaken in June 2021, due to supply chain issues).

Vehicle sales is usually a transmission mechanism for Federal Open Market Committee (FOMC) policy (far behind housing). However, this time, vehicle sales have been suppressed by supply chain issues, and will probably not be significantly impacted by higher interest rates.

Weekly Initial Unemployment Claims at 229,000

by Calculated Risk on 6/23/2022 08:36:00 AM

The DOL reported:

In the week ending June 18, the advance figure for seasonally adjusted initial claims was 229,000, a decrease of 2,000 from the previous week's revised level. The previous week's level was revised up by 2,000 from 229,000 to 231,000. The 4-week moving average was 223,500, an increase of 4,500 from the previous week's revised average. The previous week's average was revised up by 500 from 218,500 to 219,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 223,500.

The previous week was revised up.

Weekly claims were higher than the consensus forecast.

Wednesday, June 22, 2022

Thursday: Unemployment Claims, Fed Chair Powell Testimony, Bank Stress Tests

by Calculated Risk on 6/22/2022 08:13:00 PM

Thursday:

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 225 thousand down from 229 thousand last week.

• At 10:00 AM, Testimony, Fed Chair Jerome Powell, Semiannual Monetary Policy Report to Congress, Before the Committee on Financial Services, U.S. House of Representatives

• At 4:30 PM, The Fed will release the annual Bank Stress Tests results.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.8% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.9 | --- | ≥2321 | |

| New Cases per Day3 | 99,365 | 103,646 | ≤5,0002 | |

| Hospitalized3🚩 | 24,470 | 24,213 | ≤3,0002 | |

| Deaths per Day3 | 248 | 295 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

AIA: "Architecture Billings Index slows but remains strong" in May

by Calculated Risk on 6/22/2022 03:01:00 PM

Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: Architecture Billings Index slows but remains strong

Architecture firms reported increasing demand for design services in May, according to a new report today from The American Institute of Architects (AIA).

The ABI score for May was 53.5. While this score is down from April’s score of 56.5, it still indicates very strong business conditions overall (any score above 50 indicates an increase in billings from the prior month). Also in May, both the new project inquiries and design contracts indexes expanded, posting scores of 63.9 and 56.9 respectively.

“The strength in design activity over the past three months has produced a broader base of gains. The Northeast region and Institutional sector have struggled with slow billings activity, but now have posted consecutive months of positive scores.” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “With the improvement in inquiries and new design projects, demand for design services will likely remain high for the next several months, despite strong economic headwinds.”

...

• Regional averages: West (59.3); Midwest (56.8); South (52.3); Northeast (51.4)

• Sector index breakdown: commercial/industrial (57.7); mixed practice (56.2); multi-family residential (54.5); institutional (51.7)

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Architecture Billings Index since 1996. The index was at 53.5 in May, down from 56.5 in April. Anything above 50 indicates expansion in demand for architects' services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index has been positive for sixteen consecutive months. This index usually leads CRE investment by 9 to 12 months, so this index suggests a pickup in CRE investment in 2022 and into 2023.

Final Look at Local Housing Markets in May, Inventory Up, Sales Down, New Listings Picking Up

by Calculated Risk on 6/22/2022 12:03:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Final Look at Local Housing Markets in May

A brief excerpt:

This is the final look at local markets in May. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I update these tables throughout each month as additional data is released.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

We are seeing a significant change in inventory, and maybe a pickup in new listings. So far, most of the increase in inventory has been due to softer demand - likely because of higher mortgage rates - but we need to keep an eye on new listings too.

...

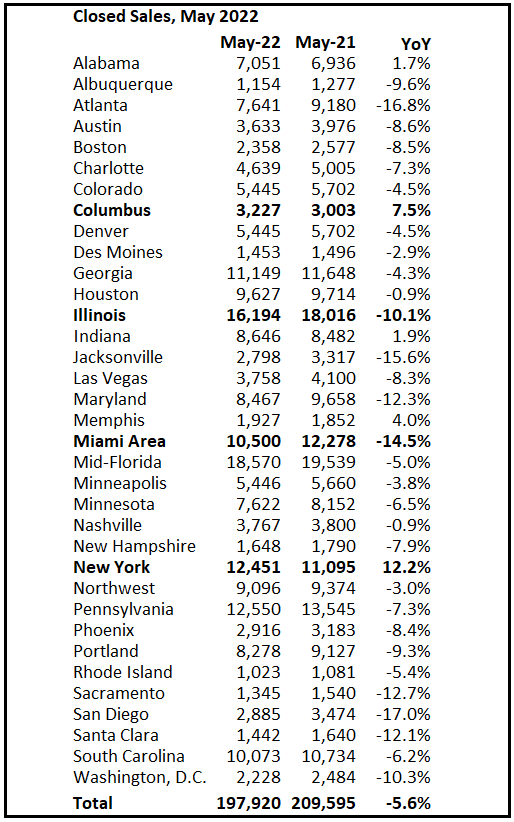

And a table of May sales. Sales in these areas were down 5.6% YoY, Not Seasonally Adjusted (NSA). The NAR reported sales NSA in May (498,000) were 5.7% below sales in May 2021 (528,000). So, this sample of local markets is similar to the NAR report.

The table doesn’t include California where sales were down 15.2% year-over-year.

Fed Chair Powell: Semiannual Monetary Policy Report to the Congress

by Calculated Risk on 6/22/2022 09:33:00 AM

This testimony will be live here at 9:30 AM ET.

Report here.

From Fed Chair Powell: Semiannual Monetary Policy Report to the Congress. An excerpt on inflation:

I will begin with one overarching message. At the Fed, we understand the hardship high inflation is causing. We are strongly committed to bringing inflation back down, and we are moving expeditiously to do so. We have both the tools we need and the resolve it will take to restore price stability on behalf of American families and businesses. It is essential that we bring inflation down if we are to have a sustained period of strong labor market conditions that benefit all.

...

Over coming months, we will be looking for compelling evidence that inflation is moving down, consistent with inflation returning to 2 percent. We anticipate that ongoing rate increases will be appropriate; the pace of those changes will continue to depend on the incoming data and the evolving outlook for the economy. We will make our decisions meeting by meeting, and we will continue to communicate our thinking as clearly as possible. Our overarching focus is using our tools to bring inflation back down to our 2 percent goal and to keep longer-term inflation expectations well anchored.