RSS Feed

RSS Feed by Calculated Risk on 8/13/2022 02:11:00 PM

Saturday, August 13, 2022

Real Estate Newsletter Articles this Week

At the Calculated Risk Real Estate Newsletter this week:

• Current State of the Housing Market

• Homebuyers Hit Brakes in July, Sellers Hold Back

• Realtor.com Reports Weekly Inventory Up 28% Year-over-year

• 1st Look at Local Housing Markets in July

• Housing Inventory Growth Has Slowed in Recent Weeks

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of August 14, 2022

by Calculated Risk on 8/13/2022 08:11:00 AM

The key reports this week are July Housing Starts, Existing Home Sales and Retail sales.

For manufacturing, the Industrial Production report will be released.

8:30 AM: The New York Fed Empire State manufacturing survey for August. The consensus is for a reading of 5.5, down from 11.1.

10:00 AM: The August NAHB homebuilder survey. The consensus is for a reading of 55, unchanged from 55. Any number above 50 indicates that more builders view sales conditions as good than poor.

8:30 AM ET: Housing Starts for July.

8:30 AM ET: Housing Starts for July. This graph shows single and multi-family housing starts since 1968.

The consensus is for 1.540 million SAAR, down from 1.559 million SAAR in June.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for July.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for July.This graph shows industrial production since 1967.

The consensus is for a 0.3% increase in Industrial Production, and for Capacity Utilization to increase to 80.1%.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Retail sales for July is scheduled to be released. The consensus is for 0.1% increase in retail sales.

8:30 AM: Retail sales for July is scheduled to be released. The consensus is for 0.1% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline)

2:00 PM: FOMC Minutes, Meeting of July 26-27, 2022

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 265 thousand up from 262 thousand last week.

8:30 AM: the Philly Fed manufacturing survey for August. The consensus is for a reading of -5.0, up from -12.3.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 4.88 million SAAR, down from 5.12 million last month.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 4.88 million SAAR, down from 5.12 million last month.The graph shows existing home sales from 1994 through the report last month.

10:00 AM: State Employment and Unemployment (Monthly) for July 2022

Friday, August 12, 2022

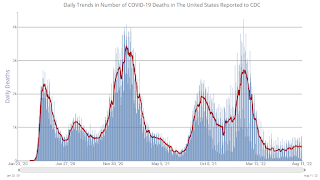

COVID August 12, 2022, Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 8/12/2022 09:11:00 PM

On COVID (focus on hospitalizations and deaths):

Hospitalizations have almost quadrupled from the lows in April 2022.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) and 7-day average (line) of deaths reported.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Day2 | 103,105 | 118,550 | ≤5,0001 | |

| Hospitalized2 | 36,063 | 37,539 | ≤3,0001 | |

| Deaths per Day2 | 413 | 439 | ≤501 | |

| 1my goals to stop daily posts, 27-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Lawler: American Homes 4 Rent Slashing MLS Purchases of Single Family Homes

by Calculated Risk on 8/12/2022 04:38:00 PM

From housing economist Tom Lawler: American Homes 4 Rent Slashing MLS Purchases of Single Family Homes

In American Homes 4 Rent (AMH) earnings conference call last week, officials said that the company was slashing its MLS-based purchases of single-family homes in the second half of 2022. Here are a few excerpts:

“Now, turning to our investment strategy more broadly. Interest rates have risen, while home prices have yet to react in a meaningful way. In addition, these are uncertain times in the capital markets.

As such, we have temporarily scaled back one-off MLS transactions to allow the market time to recalibrate and stabilize. This will preserve dry powder for future investment.”

Here is a response to a question of whether or not the company was “entirely out” of the MLS market or third-party homebuilder purchases.

“Yes. Thanks Brad. We're not 100% out. We're still acquiring, but it has had a very significant or very reduced level, probably more than 80% reduction from what we were seeing earlier this year. It is based on what the attractive opportunities are when you're underwriting many homes, and we're starting to see a growing list of opportunities on the MLS. The MLS has many more homes today available, the times that they're sitting there is much greater. We're starting to see opportunities.”

“With respect to other acquisition channels, it is a very interesting time. We are receiving many inbound telephone calls that we were not receiving previously, whether it's from owners of small portfolios or even national homebuilders with excess inventory. Where we are, though, in those -- in that process is we still have a gap in our bid to ask expectations between buyer and seller.”

The company noted that it has not lowered its projections for its “wholly owned development activities” (or its “build to rent”) program. AMH has been very aggressive in acquiring lots for its build to rent program, increasing the number of lots it owns or controls (and most owns) from 2,000 at the end of 2017 to 9,000 at the end of 2020, 18,000 at the end of 2021, and well over 20,000 at the end of this June.

You can read the transcript of the AMH earnings conference call here.

If you are interested in this topic, an article published today by Bloomberg (link shown below) is worth reading: Housing Slowdown Chills Investors Who Supercharged US Market

Realtor.com Reports Weekly Inventory Up 28% Year-over-year; Inventory growth is slowing

by Calculated Risk on 8/12/2022 11:29:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Realtor.com Reports Weekly Inventory Up 28% Year-over-year

Excerpt:

As I noted earlier, Inventory will Tell the Tale about the housing market. And housing inventory is increasing, but the pace of growth has slowed in recent weeks.

As the housing market slows, we need to watch inventory very closely. This will give us a hint on what will happen with house prices.

...

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released yesterday from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending August 6, 2022.. Note: They have data on list prices, new listings and more, but this focus is on inventory.• Active inventory continued to grow, but the pace slipped to 28% above one year ago. The rate of improvement actually slipped this week as the number of new listings continues to come in lower. The big positive for today’s shoppers is that they have more homes to consider than last year’s shoppers did. Nevertheless, our July Housing Trends Report showed that the active listings count still trails its 2020 and 2019 levels by more than 15% and 45%, respectively. More improvement in active inventory is likely needed to bring balance, but the recent trend may be at-risk if homeowner attitudes toward selling now continue to deteriorate....Here is a graph of the year-over-year change in inventory according to realtor.com.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Early Q3 GDP Forecasts

by Calculated Risk on 8/12/2022 10:09:00 AM

From BofA:

Looking ahead to next week, we will initiate our US GDP tracking for Q3 following the release of July retail sales. ... If our forecast for July retail sales prove accurate, it would suggest that household spending is off to a fast start in Q3 and pose upside risk to our forecast for another modest decline in real GDP in the quarter. [-0.5 percent Q3, perliminary estimate]From Goldman:

emphasis added

We left our Q3 GDP tracking estimate unchanged at +0.9% (qoq ar). [August 10 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 2.5 percent on August 10, up from 1.4 percent on August 4. [August 10 estimate]

Second Home Market: South Lake Tahoe in July

by Calculated Risk on 8/12/2022 08:57:00 AM

With the pandemic, there was a surge in 2nd home buying.

I'm looking at data for some second home markets - and I'm tracking those markets to see if there is an impact from lending changes, rising mortgage rates or the easing of the pandemic.

This graph is for South Lake Tahoe since 2004 through July 2022, and shows inventory (blue), and the year-over-year (YoY) change in the median price (12-month average).

Note: The median price is distorted by the mix, but this is the available data.

Click on graph for larger image.

Click on graph for larger image.

Following the housing bubble, prices declined for several years in South Lake Tahoe, with the median price falling about 50% from the bubble peak.

Currently inventory is still very low, but up almost 6-fold from the record low set in February 2022, and up 44% year-over-year. Prices are up 9.9% YoY (but the YoY change has been trending down).

Thursday, August 11, 2022

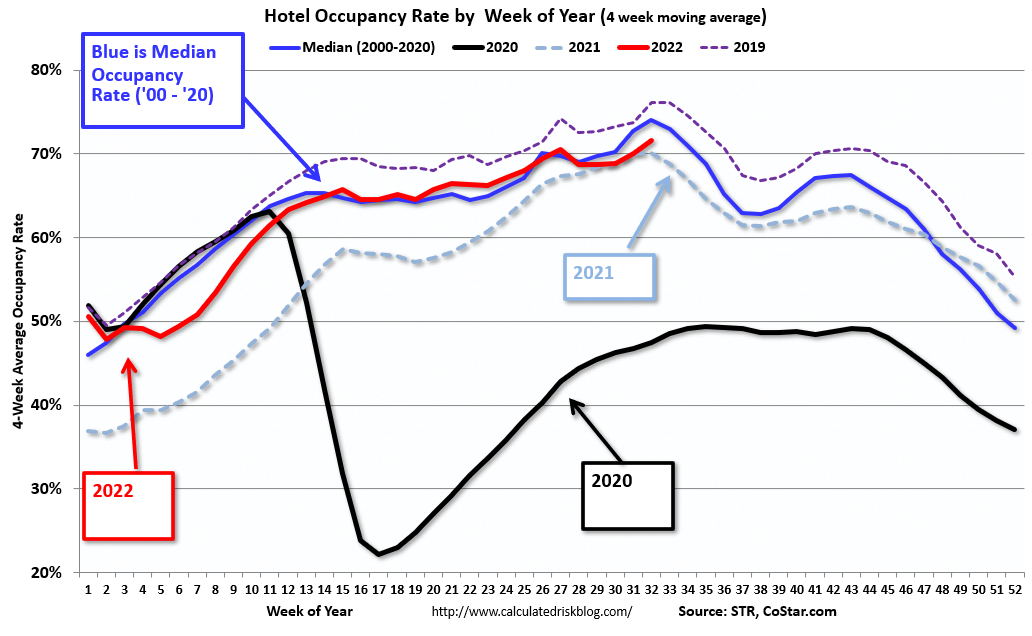

Hotels: Occupancy Rate Down 5.7% Compared to Same Week in 2019

by Calculated Risk on 8/11/2022 03:59:00 PM

Following seasonal patterns, U.S. hotel performance fell slightly from the previous week, according to STR‘s latest data through Aug. 6.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

July 31 through Aug. 6, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 69.9% (-5.7%)

• Average daily rate (ADR): $154.48 (+15.1%)

• Revenue per available room (RevPAR): $108.04 (+8.5%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is just below the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will peak in seasonally in a few weeks.

Current State of the Housing Market

by Calculated Risk on 8/11/2022 12:33:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Current State of the Housing Market

A brief excerpt:

This is a market overview for mid-August.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

The early local market reports for July show inventory up over 46% YoY for these markets! These same markets were up 20% YoY in May, so the NAR report for July will show further increases in inventory.

It is important to realize inventory is both increasing and still very low. Here is a graph from Realtor.com’s July Housing Trends Report. This shows their estimate of active inventory over the last six years. Currently inventory is rising, but still far below normal.

Since inventory was declining rapidly for most of 2020, and it is very likely that inventory will be up in August or September compared to 2020.

...

We are seeing a sharp slowdown in the housing market, with more price reductions, more inventory, and fewer sales. It will take some time to see the impact on house price growth, but that is coming too. However, inventory growth has slowed recently, and inventory is key for predicting house prices.

Next week, existing home sales will likely show a sharp year-over-year decline in sales for July - with sales below 5 million SAAR for the first time since the first few months of the pandemic. Housing starts will probably show further declines (and still a record number of homes under construction).

It is important to remember that housing is a key transmission mechanism for Federal Open Market Committee (FOMC) policy. As long as inflation remains elevated, the Fed will keep raising rates - and that will impact the housing market (although mortgage rates have already jumped in anticipation of the FOMC actions).

MBA: "Mortgage Delinquencies Decrease in the Second Quarter of 2022"

by Calculated Risk on 8/11/2022 10:45:00 AM

From the MBA: Mortgage Delinquencies Decrease in the Second Quarter of 2022

The delinquency rate for mortgage loans on one-to-four-unit residential properties decreased to a seasonally adjusted rate of 3.64 percent of all loans outstanding at the end of the second quarter of 2022, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

For the purposes of the survey, MBA asks servicers to report loans in forbearance as delinquent if the payment was not made based on the original terms of the mortgage. The delinquency rate was down 47 basis points from the first quarter of 2022 and down 183 basis points from one year ago.

“At 3.64 percent, the mortgage delinquency rate in the second quarter fell to its lowest level since MBA’s survey began in 1979 – even beating out the previous pre-pandemic, survey low of 3.77 percent in the fourth quarter of 2019,” said Marina Walsh, MBA’s Vice President of Industry Analysis. “Most of the improvement across all product types – FHA, VA, and conventional loans - resulted from a decline in the loans that were 90 days or more delinquent but not in the foreclosure process.”

According to Walsh, of all the economic indicators that can lead to mortgage delinquencies, the U.S. unemployment rate seems to be the best gauge of loan performance. Despite inflationary pressures, stock market volatility, increases in mortgage rates, and two quarters of economic contraction – often defined as a recession – the job market remains incredibly strong. The unemployment rate was 3.5 percent in July – a half-century low that tracks closely with the record-low mortgage delinquency rate.

Added Walsh, “Foreclosure inventory levels and foreclosure starts remain well below historical averages for the survey – a strong indication that servicers are able to help delinquent borrowers find alternatives to foreclosure. Such alternatives include curing, loan workouts, home sales - with possible equity to spare, or cash-for-keys and deed-in-lieu options.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of loans delinquent by days past due. Overall delinquencies decreased in Q2 to a record low.

From the MBA:

Compared to last quarter, the seasonally adjusted mortgage delinquency rate decreased for all loans outstanding to 3.64 percent, the lowest level in the history of the survey dating back to 1979. By stage, the 30-day delinquency rate increased 7 basis points to 1.66 percent, the 60-day delinquency rate decreased 7 basis points to 0.49 percent, and the 90-day delinquency bucket decreased 47 basis points to 1.49 percent.This sharp increase in 2020 in the 90-day bucket was due to loans in forbearance (included as delinquent, but not reported to the credit bureaus).

...

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the second quarter was 0.59 percent, up 6 basis points from the first quarter of 2022 and 8 basis points higher than one year ago. The foreclosure inventory rate remains below the quarterly average of 1.43 percent dating back to 1979.

The percent of loans in the foreclosure process increased in Q2 with the end of the foreclosure moratoriums.