RSS Feed

RSS Feed by Calculated Risk on 8/15/2022 05:08:00 PM

Monday, August 15, 2022

MBA Survey: "Share of Mortgage Loans in Forbearance Decreases to 0.74% in July"

Note: This is as of July 31st.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.74% in July

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 7 basis points from 0.81% of servicers’ portfolio volume in the prior month to 0.74% as of July 31, 2022. According to MBA’s estimate, 370,000 homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 1 basis point to 0.34%. Ginnie Mae loans in forbearance remained the same relative to the previous month at 1.26%, and the forbearance share for portfolio loans and private-label securities (PLS) declined 34 basis points to 1.34%.

“July continued the ongoing trend in recent months of most of the forbearance exits coming from borrowers with portfolio loans and private label security loans,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “There has been very little change in the forbearance rate for Fannie Mae, Freddie Mac, and Ginnie Mae loans during the past three months, perhaps indicating that we have reached a floor, with loans entering forbearance about equal to loans exiting forbearance for these loan types.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time.

The share of forbearance plans is decreasing, and, at the end of July, there were about 370,000 homeowners in forbearance plans.

3rd Look at Local Housing Markets in July, Sales Down Sharply

by Calculated Risk on 8/15/2022 02:38:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in July, Sales Down Sharply

A brief excerpt:

The big story for July existing home sales is the sharp year-over-year (YoY) decline in sales. Another key story is that new listings are down YoY in July. Of course, active listings are up sharply.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

Last month, all local markets I track were down 15.9% YoY, NSA. This appears to be another step down in sales, although there was one less selling day in July this year than in July 2021.

Here is a table comparing the year-over-year Not Seasonally Adjusted (NSA) declines in sales this year from the National Association of Realtors® (NAR) with the local markets I track. So far, these measures have tracked closely, and the preliminary data below suggests a sharp decline in sales in July.

Sales in some of the hottest markets are down 30% or more YoY, whereas in other markets, sales are only down in the high teens YoY.

...

More local markets to come!

NAHB: Builder Confidence Turns Slightly Negative in August

by Calculated Risk on 8/15/2022 10:06:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 49, down from 55 in July. Any number below 50 indicates that more builders view sales conditions as poor than good.

From the NAHB: Builder Confidence Underwater After Falling for Eighth Consecutive Month

Builder confidence fell for the eighth straight month in August as elevated interest rates, ongoing supply chain problems and high home prices continue to exacerbate housing affordability challenges. In another sign that a declining housing market has failed to bottom out, builder confidence in the market for newly built single-family homes fell six points in August to 49, marking the first time since May 2020 that the index fell below the key break-even measure of 50, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today.

“Ongoing growth in construction costs and high mortgage rates continue to weaken market sentiment for single-family home builders,” said NAHB Chairman Jerry Konter, a home builder and developer from Savannah, Ga. “And in a troubling sign that consumers are now sitting on the sidelines due to higher housing costs, the August buyer traffic number in our builder survey was 32, the lowest level since April 2014 with the exception of the spring of 2020 when the pandemic first hit.”

“Tighter monetary policy from the Federal Reserve and persistently elevated construction costs have brought on a housing recession,” said NAHB Chief Economist Robert Dietz. “The total volume of single-family starts will post a decline in 2022, the first such decrease since 2011. However, as signs grow that the rate of inflation is near peaking, long-term interest rates have stabilized, which will provide some stability for the demand-side of the market in the coming months.”

Roughly one-in-five (19%) home builders in the HMI survey reported reducing prices in the past month to increase sales or limit cancellations. The median price reduction was 5% for those reporting using such incentives. Meanwhile, 69% of builders reported higher interest rates as the reason behind falling housing demand, the top impact cited in the survey.

...

All three HMI components posted declines in August and each fell to their lowest level since May 2020. Current sales conditions dropped seven points to 57, sales expectations in the next six months declined two points to 47 and traffic of prospective buyers fell five points to 32.

Looking at the three-month moving averages for regional HMI scores, the Northeast fell nine points to 56, the Midwest dropped three points to 49, the South fell seven points to 63 and the West posted an 11-point decline to 51.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the NAHB index since Jan 1985.

This was well below the consensus forecast, and just below 50.

The "traffic of prospective buyers" is now well below breakeven at 32 (below 50).

Housing Inventory August 15th Update: Up 30.3% Year-over-year

by Calculated Risk on 8/15/2022 08:57:00 AM

Inventory is still increasing, but the inventory build has slowed somewhat over the last several weeks. Still, inventory is increasing faster than in 2019 at this time of year (both in percentage terms and in total inventory added). Here are the same week inventory changes for the last four years:

2022: +6.3K

2021: +10.4K

2020: -10.9K

2019: -0.1K

Inventory bottomed seasonally at the beginning of March 2022 and is now up 128% since then. More than double! Altos reports inventory is up 30.3% year-over-year and is now 25.8% above the peak last year.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of August 12th, inventory was at 560 thousand (7-day average), compared to 554 thousand the prior week. Inventory was up 1.2% from the previous week.

Inventory is still historically low. Compared to the same week in 2021, inventory is up 30.3% from 422 thousand, however compared to the same week in 2020 inventory is down 8.6% from 602 thousand. Compared to 3 years ago, inventory is down 43.0% from 966 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 8.6% according to Altos)

4. Inventory up compared to 2019 (currently down 43.0%).

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 8.6% according to Altos)

4. Inventory up compared to 2019 (currently down 43.0%).

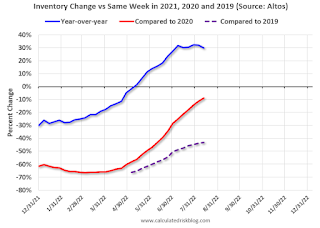

Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

Two years ago (in 2020) inventory was declining all year, so the two-year comparison will get easier all year.

Based on the recent increases in inventory, my current estimate is inventory will be up compared to 2020 in September of this year, and it is possible inventory will be back to 2019 levels in the first half of 2023. However, if inventory growth stalls, then it might take much longer to reach normal inventory levels..

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 8/15/2022 08:20:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Notes: I've added back gasoline supplied to see if there is an impact from higher gasoline prices.

The TSA is providing daily travel numbers.

This data is as of August 14th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 9.9% from the same day in 2019 (90.1% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has been moving sideways over the last several months, off about 10% from 2019 - with some ups and downs, usually related to the timing of holidays.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through August 11th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $136 million last week, down about 39% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $136 million last week, down about 39% from the median for the week.

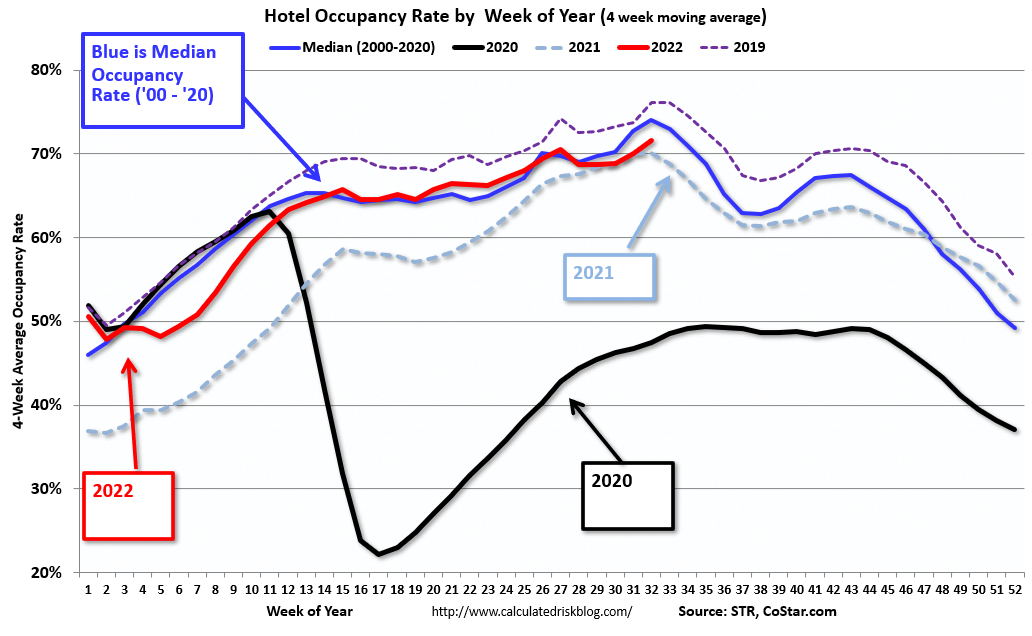

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through August 6th. The occupancy rate was down 5.7% compared to the same week in 2019.

The 4-week average of the occupancy rate is below the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of Augustth, gasoline supplied was down 5.5% compared to the same week in 2019.

Recently gasoline supplied has been running somewhat below 2019 levels.

Sunday, August 14, 2022

Monday: NY Fed Mfg, Homebuilder Survey

by Calculated Risk on 8/14/2022 07:05:00 PM

Weekend:

• Schedule for Week of August 14, 2022

Monday:

• At 8:30 AM ET, The New York Fed Empire State manufacturing survey for August. The consensus is for a reading of 5.5, down from 11.1.

• At 10:00 AM, The August NAHB homebuilder survey. The consensus is for a reading of 55, unchanged from 55. Any number above 50 indicates that more builders view sales conditions as good than poor.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 8 and DOW futures are down 62 (fair value).

Oil prices were up over the last week with WTI futures at $91.68 per barrel and Brent at $97.73 per barrel. A year ago, WTI was at $68, and Brent was at $71 - so WTI oil prices are up 35% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.91 per gallon. A year ago, prices were at $3.16 per gallon, so gasoline prices are up $0.75 per gallon year-over-year.

Summer Teen Employment

by Calculated Risk on 8/14/2022 10:57:00 AM

Here is a look at the change in teen employment over time.

The graph below shows the employment-population ratio for teens (6 to 19 years old) since 1948.

The graph is Not Seasonally Adjusted (NSA), to show the seasonal hiring of teenagers during the summer.

A few observations:

1) Although teen employment has recovered some since the great recession, overall teen employment had been trending down. This is probably because more people are staying in school (a long term positive for the economy).

2) Teen employment was significantly impacted in 2020 by the pandemic.

Click on graph for larger image.

Click on graph for larger image.

3) A smaller percentage of teenagers are obtaining summer employment. The seasonal spikes are smaller than in previous decades.

The teen employment-population ratio was 38.4% in July 2022, down from 38.9% in July 2021. The teen participation rate was 43.6% in July 2022, down from 43.8% the previous July.

So, a smaller percentage of teenagers are joining the labor force during the summer as compared to previous years. This could be because of fewer employment opportunities, or because teenagers are pursuing other activities during the summer.

3) The decline in teenager participation is one of the reasons the overall participation rate has declined (of course, the retiring baby boomers is the main reason the overall participation rate has declined over the last 20+ years).

3) The decline in teenager participation is one of the reasons the overall participation rate has declined (of course, the retiring baby boomers is the main reason the overall participation rate has declined over the last 20+ years).

Saturday, August 13, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 8/13/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Current State of the Housing Market

• Homebuyers Hit Brakes in July, Sellers Hold Back

• Realtor.com Reports Weekly Inventory Up 28% Year-over-year

• 1st Look at Local Housing Markets in July

• Housing Inventory Growth Has Slowed in Recent Weeks

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of August 14, 2022

by Calculated Risk on 8/13/2022 08:11:00 AM

The key reports this week are July Housing Starts, Existing Home Sales and Retail sales.

For manufacturing, the Industrial Production report will be released.

8:30 AM: The New York Fed Empire State manufacturing survey for August. The consensus is for a reading of 5.5, down from 11.1.

10:00 AM: The August NAHB homebuilder survey. The consensus is for a reading of 55, unchanged from 55. Any number above 50 indicates that more builders view sales conditions as good than poor.

8:30 AM ET: Housing Starts for July.

8:30 AM ET: Housing Starts for July. This graph shows single and multi-family housing starts since 1968.

The consensus is for 1.540 million SAAR, down from 1.559 million SAAR in June.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for July.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for July.This graph shows industrial production since 1967.

The consensus is for a 0.3% increase in Industrial Production, and for Capacity Utilization to increase to 80.1%.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Retail sales for July is scheduled to be released. The consensus is for 0.1% increase in retail sales.

8:30 AM: Retail sales for July is scheduled to be released. The consensus is for 0.1% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline)

2:00 PM: FOMC Minutes, Meeting of July 26-27, 2022

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 265 thousand up from 262 thousand last week.

8:30 AM: the Philly Fed manufacturing survey for August. The consensus is for a reading of -5.0, up from -12.3.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 4.88 million SAAR, down from 5.12 million last month.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 4.88 million SAAR, down from 5.12 million last month.The graph shows existing home sales from 1994 through the report last month.

10:00 AM: State Employment and Unemployment (Monthly) for July 2022

Friday, August 12, 2022

COVID August 12, 2022, Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 8/12/2022 09:11:00 PM

On COVID (focus on hospitalizations and deaths):

Hospitalizations have almost quadrupled from the lows in April 2022.

Click on graph for larger image.

Click on graph for larger image.

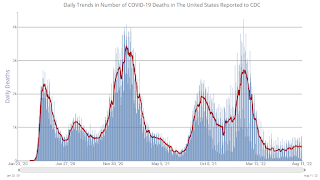

This graph shows the daily (columns) and 7-day average (line) of deaths reported.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Day2 | 103,105 | 118,550 | ≤5,0001 | |

| Hospitalized2 | 36,063 | 37,539 | ≤3,0001 | |

| Deaths per Day2 | 413 | 439 | ≤501 | |

| 1my goals to stop daily posts, 27-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.