RSS Feed

RSS Feed by Calculated Risk on 9/29/2022 08:39:00 AM

Thursday, September 29, 2022

Weekly Initial Unemployment Claims decrease to 193,000

The DOL reported:

In the week ending September 24, the advance figure for seasonally adjusted initial claims was 193,000, a decrease of 16,000 from the previous week's revised level. The previous week's level was revised down by 4,000 from 213,000 to 209,000. The 4-week moving average was 207,000, a decrease of 8,750 from the previous week's revised average. The previous week's average was revised down by 1,000 from 216,750 to 215,750.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 207,000.

The previous week was revised down.

Weekly claims were lower than the consensus forecast.

Q2 GDP Growth Unrevised at minus 0.6% Annual Rate

by Calculated Risk on 9/29/2022 08:35:00 AM

From the BEA: Gross Domestic Product (Third Estimate), GDP by Industry, and Corporate Profits (Revised), 2nd Quarter 2022 and Annual Update

Real gross domestic product (GDP) decreased at an annual rate of 0.6 percent in the second quarter of 2022, according to the "third" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 1.6 percent (same as previously published).Here is a Comparison of Third and Second Estimates. PCE growth was revised up from 1.5% to 2.0%. Residential investment was revised down from -16.2% to -17.8%.

The “third” estimate of GDP released today is based on more complete source data than were available for the "second" estimate issued last month. In the second estimate, the decrease in real GDP was also 0.6 percent. The update primarily reflected an upward revision to consumer spending that was offset by a downward revision to exports. Imports, which are a subtraction in the calculation of GDP, were revised down

...

Real gross domestic income (GDI) increased 0.1 percent in the second quarter, a downward revision of 1.3 percentage points from the previous estimate. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, decreased 0.3 percent in the second quarter, a downward revision of 0.7 percentage point.

emphasis added

Wednesday, September 28, 2022

Thursday: Unemployment Claims, GDP

by Calculated Risk on 9/28/2022 09:04:00 PM

Thursday:

Thursday:

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for an increase to 218 thousand from 213 thousand last week.

• Also, at 8:30 AM, Gross Domestic Product (Third Estimate), GDP by Industry, and Corporate Profits (Revised), 2nd Quarter 2022 and Annual Update The consensus is that real GDP decreased 0.6% annualized in Q2, unchanged from the second estimate of -0.6%.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Day2 | 50,397 | 55,529 | ≤5,0001 | |

| Hospitalized2 | 23,531 | 25,768 | ≤3,0001 | |

| Deaths per Day2 | 354 | 379 | ≤501 | |

| 1my goals to stop daily posts, 27-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

NOTE: Cases have declined by more than half, and deaths lag cases - so we might see average daily deaths in the 200s soon (better, but still too high).

Average daily deaths bottomed in July 2021 at 214 per day.

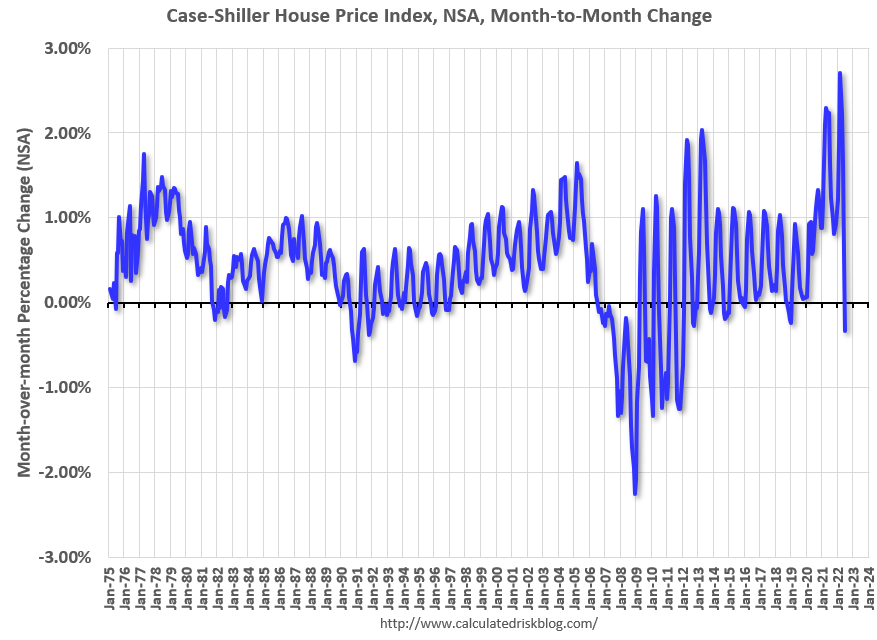

A few comments on the Seasonal Pattern for House Prices

by Calculated Risk on 9/28/2022 04:17:00 PM

Two key points:

1) There is a clear seasonal pattern for house prices.

2) The surge in distressed sales during the housing bust distorted the seasonal pattern.

For in depth description of these issues, see Jed Kolko's article from 2014 "Let’s Improve, Not Ignore, Seasonal Adjustment of Housing Data"

Note: I was one of several people to question the change in the seasonal factor (here is a post in 2009) - and this led to S&P Case-Shiller questioning the seasonal factor too (from April 2010). I still use the seasonal factor (I think it is better than using the NSA data).

Click on graph for larger image.

Click on graph for larger image.

This graph shows the month-to-month change in the NSA Case-Shiller National index since 1987 (through July 2022). The seasonal pattern was smaller back in the '90s and early '00s and increased once the bubble burst.

The seasonal swings declined following the bust, however the recent price surge changed the month-over-month pattern.

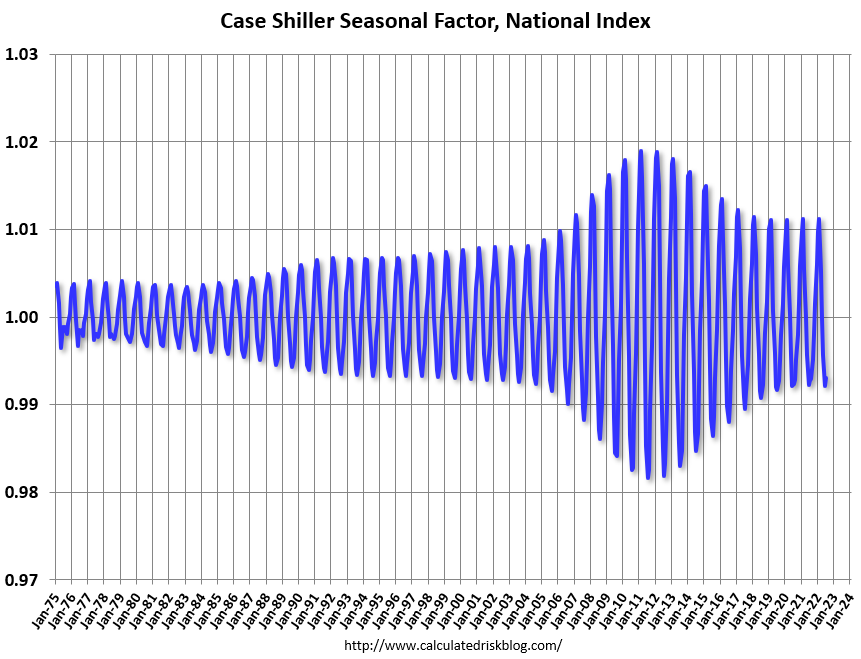

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year.

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year.

The swings in the seasonal factors have decreased, and the seasonal factors had been moving back towards more normal levels.

Note that the recent price surge hasn't distorted the seasonal factors. Unless there is a wave of distressed sales (unlikely due to mostly solid lending), the seasonal pattern won't be distorted like during the housing bust.

Pace of Rent Increases Continues to Slow

by Calculated Risk on 9/28/2022 11:15:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Pace of Rent Increases Continues to Slow

A brief excerpt:

Here is a graph of the year-over-year (YoY) change for these measures since January 2015. All of these measures are through August 2022 (Apartment List through September 2022).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note that new lease measures (Zillow, Apartment List) dipped early in the pandemic, whereas the BLS measures were steady. Then new leases took off, and the BLS measures are picking up.

...

The Zillow measure is up 12.3% YoY in August, down from 13.8% YoY in July. This is down from a peak of 17.2% YoY in February.

The ApartmentList measure is up 7.5% YoY as of September, down from 9.8% in August. This is down from the peak of 18.0% YoY last November.

Rents are still increasing, and we should expect this to continue to spill over into measures of inflation. The Owners’ Equivalent Rent (OER) was up 6.3% YoY in August, from 5.8% YoY in July - and will likely increase further in the coming months.

...

My suspicion is rent increases will slow further over the coming months as the pace of household formation slows, and more supply comes on the market.

NAR: Pending Home Sales Decreased 2.0% in August

by Calculated Risk on 9/28/2022 10:03:00 AM

From the NAR: Pending Home Sales Dropped 2.0% in August

Pending home sales sagged for the third straight month in August, according to the National Association of REALTORS®. Three out of four major regions experienced month-over-month decreases in transactions, however, the West saw a modest gain. Year-over-year, all four regions posted double-digit declines.This was a larger decline than expected for this index. Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in September and October.

The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, fell 2.0% to 88.4 in August. Year-over-year, pending transactions dwindled by 24.2%. An index of 100 is equal to the level of contract activity in 2001.

"The direction of mortgage rates – upward or downward – is the prime mover for home buying, and decade-high rates have deeply cut into contract signings," said NAR Chief Economist Lawrence Yun. "If mortgage rates moderate and the economy continues adding jobs, then home buying should also stabilize."

...

The Northeast PHSI decreased 3.4% from last month to 76.6, down 19.0% from August 2021. The Midwest index fell 5.2% to 88.4 in August, a 21.1% drop from the previous year.

The South PHSI slid 0.9% to 105.4 in August, a decline of 24.2% from a year ago. The West index rose by 1.4% in August to 71.0, down 31.3% from August 2021.

emphasis added

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 9/28/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 23, 2022.

... The Refinance Index decreased 11 percent from the previous week and was 84 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 0.4 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 29 percent lower than the same week one year ago.

“Applications for both purchase and refinances declined last week as mortgage rates continued to increase to multi-year highs following more aggressive policy measures from the Federal Reserve to bring down inflation. Additionally, ongoing uncertainty about the impact of the Fed’s reduction of its MBS and Treasury holdings is adding to the volatility in mortgage rates. The 30-year fixed rate was 6.52 percent, its highest level since mid-2008. After a brief pause in July, mortgage rates have increased more than a percentage point over the past six weeks,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “With rates now more than double what they were a year ago, the pace of refinancing is running at a 22-year low and last week was more than 80 percent below last year’s level. Similarly, purchase activity was 29 percent lower than a year ago, with higher rates and economic uncertainty weighing on buyers’ decisions.”

Added Kan, “With the recent jump in rates, the ARM share reached 10 percent of applications and almost 20 percent of dollar volume. ARM loans remain a viable option for qualified borrowers in this rising rate environment.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 6.52 percent from 6.25 percent, with points increasing to 1.15 from 0.71 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

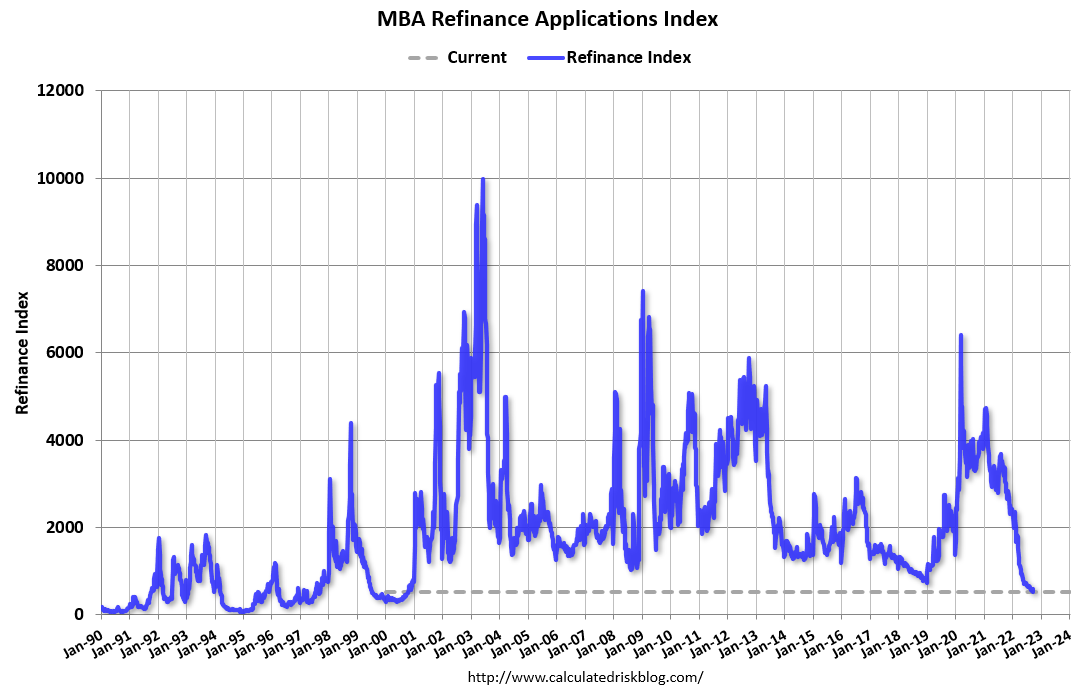

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is at the lowest level since the year 2000.

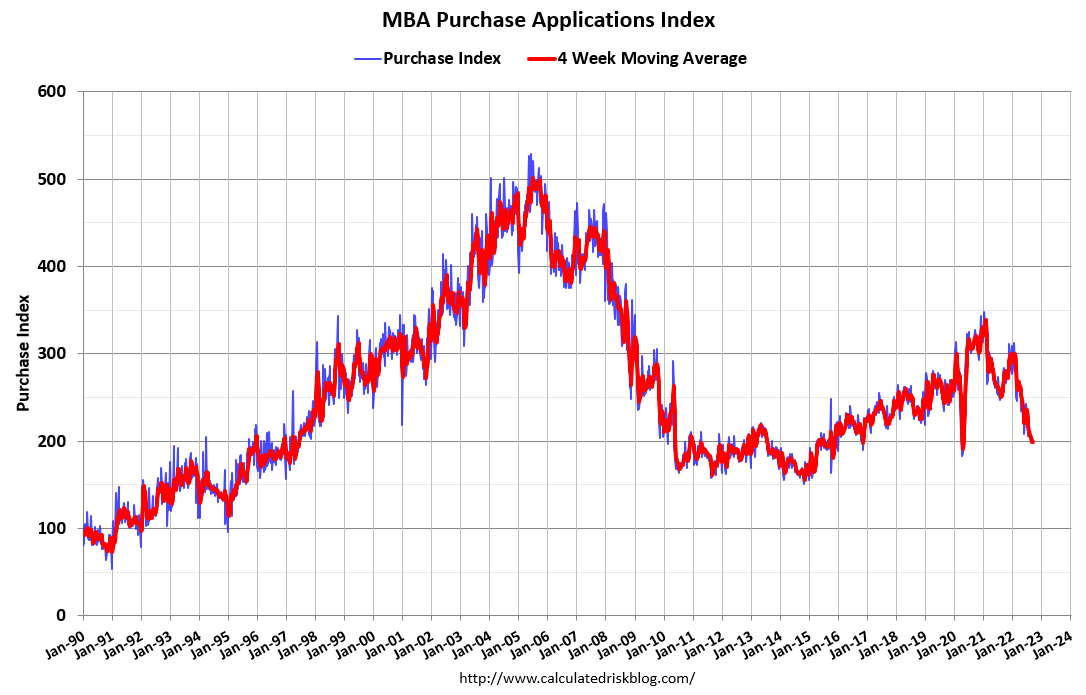

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 29% year-over-year unadjusted.

According to the MBA, purchase activity is down 29% year-over-year unadjusted.The purchase index is only 9% above the pandemic low.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, September 27, 2022

Wednesday: Pending Home Sales

by Calculated Risk on 9/27/2022 08:53:00 PM

From Matthew Graham at Mortgage News Daily: Yes, Mortgage Rates Are Now Over 7%, But It's Complicated

From Matthew Graham at Mortgage News Daily: Yes, Mortgage Rates Are Now Over 7%, But It's Complicated

That brings us to the bottom line on 7% not necessarily being 7%. Most rate quotes and most major rate indices include upfront "points" or other cost assumptions (and in larger amounts than normal). The presence of points means you could definitely still get 6.625% today. You'd just be paying more for it upfront. [30 year fixed 7.08%]Wednesday:

emphasis added

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 10:00 AM, Pending Home Sales Index for August. The consensus is 1.0% decrease in the index.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Day2 | 49,808 | 56,844 | ≤5,0001 | |

| Hospitalized2 | 23,355 | 26,111 | ≤3,0001 | |

| Deaths per Day2 | 353 | 385 | ≤501 | |

| 1my goals to stop daily posts, 27-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

NOTE: Cases have declined by more than half, and deaths lag cases - so we might see average daily deaths in the 200s soon (better, but still too high).

Average daily deaths bottomed in July 2021 at 214 per day.

New Home Sales Increased in August; Completed Inventory Increased

by Calculated Risk on 9/27/2022 03:54:00 PM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales Increased in August; Completed Inventory Increased

Brief excerpt:

The next graph shows the months of supply by stage of construction. “Months of supply” is inventory at each stage, divided by the sales rate.You can subscribe at https://calculatedrisk.substack.com/.

There are 0.86 months of completed supply (red line). This is about 60% of the normal level.

The inventory of new homes under construction is at 5.36 months (blue line). This elevated level of homes under construction is due to supply chain constraints.

And a record 106 thousand homes have not been started - about 1.86 months of supply (grey line) - about double the normal level. Homebuilders are probably waiting to start some homes until they have a firmer grasp on prices and demand.

...

First, as I discussed yesterday, the Census Bureau overestimates sales, and underestimates inventory when cancellation rates are rising, see: New Home Sales and Cancellations: Net vs Gross Sales. So, take the headline sales number with a large grain of salt - the actual negative impact on the homebuilders is greater than the headline number suggests!

There are a large number of homes under construction, and this suggests we will see a sharp increase in completed inventory over the next several months - and that will put pressure on new home prices.

New Home Sales Increase to 685,000 Annual Rate in August

by Calculated Risk on 9/27/2022 10:09:00 AM

The Census Bureau reports New Home Sales in August were at a seasonally adjusted annual rate (SAAR) of 685 thousand.

The previous three months were revised up, combined.

Sales of new single‐family houses in August 2022 were at a seasonally adjusted annual rate of 685,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 28.8 percent above the revised July rate of 532,000, but is 0.1 percent below the August 2021 estimate of 686,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are now at pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply decreased in August to 8.1 months from 10.4 months in July.

The months of supply decreased in August to 8.1 months from 10.4 months in July. The all-time record high was 12.1 months of supply in January 2009. The all-time record low was 3.5 months, most recently in October 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of August was 461,000. This represents a supply of 8.1 months at the current sales rate."

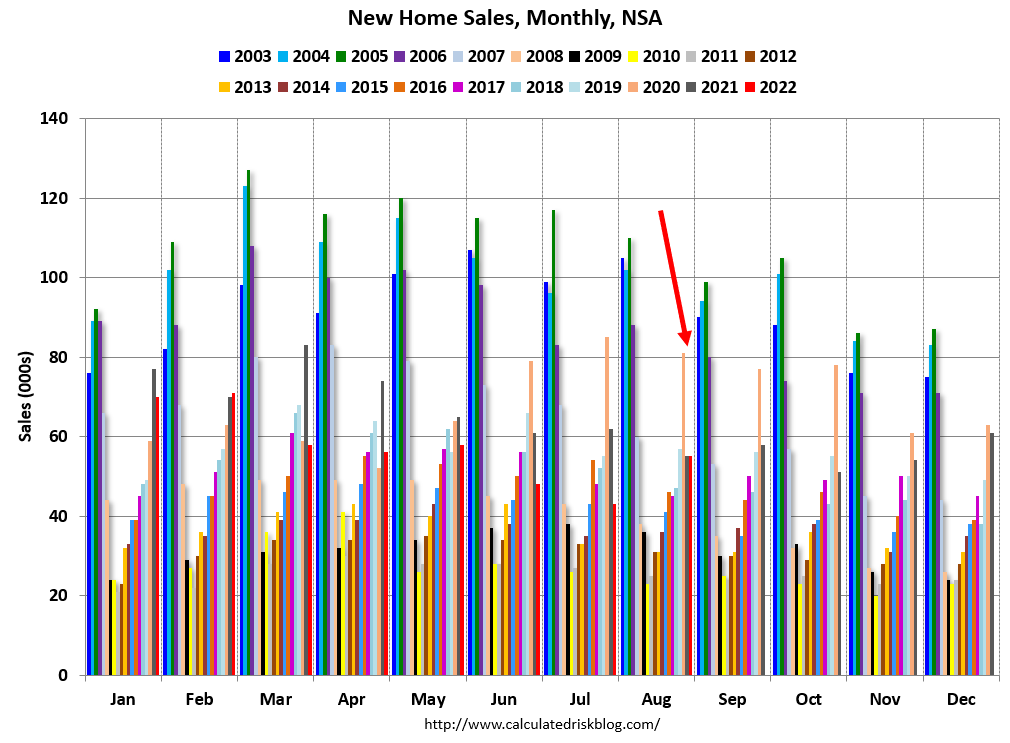

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).In August 2022 (red column), 55 thousand new homes were sold (NSA). Last year, 55 thousand homes were sold in August.

The all-time high for August was 110 thousand in 2005, and the all-time low for August was 23 thousand in 2010.

This was well above expectations, and sales in the three previous months were revised up, combined. I'll have more later today.