RSS Feed

RSS Feed by Calculated Risk on 10/06/2022 02:16:00 PM

Thursday, October 06, 2022

September Employment Preview

On Friday at 8:30 AM ET, the BLS will release the employment report for September. The consensus is for 250,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.

Click on graph for larger image.

Click on graph for larger image.• First, as of August there are 240 thousand more jobs than in February 2020 (the month before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms. As of August 2022, all of the jobs have returned.

This doesn't include the preliminary benchmark revision that showed there were 462 thousand more jobs than originally reported in March 2022.

• ADP Report: The ADP employment report showed 208,000 private sector jobs were added in September. This is the second release of ADP's new methodology, and this suggests job gains inline with consensus expectations.

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in September to 48.7%, down from 54.2% last month. This would suggest 25,000 jobs lost in manufacturing.

The ISM® services employment index increased in September to 53.0%, down from 50.2% last month. This would suggest service employment increased 155,000 in September.

Combined, the ISM surveys suggest 130,000 jobs added in September (below the consensus forecast).

• Unemployment Claims: The weekly claims report showed a decrease in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 245,000 in August to 209,000 in September. This would usually suggest fewer layoffs in September than in August. In general, weekly claims were lower than expectations in September.

• COVID: As far as the pandemic, the number of daily cases during the reference week in September was around 70,000, down from 115,000 in August.

• Conclusion: The consensus is for job growth to slow to 250,000 jobs added in September. The ADP report was in line with expectations, and weekly claims were positive. However, it seems likely that education will disappoint seasonally adjusted, so I expect the headline jobs number to be at or below the consensus forecast.

Hotels: Occupancy Rate Down 2.4% Compared to Same Week in 2019

by Calculated Risk on 10/06/2022 01:50:00 PM

As expected with the Rosh Hashanah holiday, U.S. hotel performance dropped from the previous week and showed mixed comparisons with 2019, according to STR‘s latest data through Oct. 1.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Sept. 25 through Oct. 1, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 66.4% (-2.4%)

• Average daily rate (ADR): $149.71 (+15.7%)

• Revenue per available room (RevPAR): $99.36 (+12.9%)

In addition to the Rosh Hashanah impact on business travel and groups in the major markets, there were demand shifts in the southeast region due to Hurricane Ian. ...

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is close to the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase over the next few weeks during the Fall business travel period, and then decline into the Winter.

"For many [home] sellers, it likely feels like the rug has been pulled out from underneath them"

by Calculated Risk on 10/06/2022 10:34:00 AM

Today, in the Calculated Risk Real Estate Newsletter: "For many [home] sellers, it likely feels like the rug has been pulled out from underneath them"

A brief excerpt:

A few early reporting markets …There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

This is the first look at local markets in September. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.

...

From Denver Metro Association of Realtors® (DMAR): DMAR Real Estate Market Trends ReportUsing months of inventory as a metric indicates that Denver Metro is moving toward a balanced market. … However, for many sellers, it likely feels like the rug has been pulled out from underneath them.In September, sales were down 33.1%. In August, these same markets were down 32.4% YoY Not Seasonally Adjusted (NSA).

Note that in September 2022, there were the same number of selling days as in September 2021, so the SA decline will be similar to the NSA decline. Last month, in August 2022, there was one more selling day than in August 2021 - so seasonally adjusted, the decline in sales in August was larger than in September for these markets.

Many more local markets to come!

Weekly Initial Unemployment Claims increase to 219,000

by Calculated Risk on 10/06/2022 08:33:00 AM

The DOL reported:

In the week ending October 1, the advance figure for seasonally adjusted initial claims was 219,000, an increase of 29,000 from the previous week's revised level. The previous week's level was revised down by 3,000 from 193,000 to 190,000. The 4-week moving average was 206,500, an increase of 250 from the previous week's revised average. The previous week's average was revised down by 750 from 207,000 to 206,250.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 206,500.

The previous week was revised down.

Weekly claims were higher than the consensus forecast.

Wednesday, October 05, 2022

Thursday: Unemployment Claims

by Calculated Risk on 10/05/2022 09:01:00 PM

Thursday:

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for an increase to 203 thousand from 193 thousand last week.

Reis: Office Vacancy Rate Unchanged in Q3, Mall Vacancy Rate Unchanged

by Calculated Risk on 10/05/2022 03:44:00 PM

From Moody’s Analytics Senior Economist Lu Chen: Office continues its bumpy ride, and Retail remains flat

Office vacancy has been persistently stuck at over 18% since early 2021, a consequence of excess inventories and strains on companies’ expansion plans. Net absorption rose in June and July, in line with the return to office sentiment, but that trend was short-lived as economic uncertainties pressured the sector’s fundamentals. The 3rd quarter ended with an increase in office demand, but the 1.75 million square feet (sqft) total net absorption was less than a third of the total construction delivery of around 6 million sqft. Office vacancy moved slightly upwards last quarter, but due to rounding remained at an elevated 18.4%, near its pandemic peak. Asking rent exceeded $35/sqft ($35.04), which is equivalent of 0.4% growth compared to last quarter. Effective rent kept pace, but that’s only half its rate in Q2.

emphasis added

Reis reported the office vacancy rate was at 18.4% in Q3 2022, unchanged from 18.4% in Q2, and up from 18.2% in Q3 2021.

Q2 2021 at 18.5% was the highest vacancy rate for offices since the early '90s (following the S&L crisis)

NOTE: This says nothing about how many people are in the offices (related to the increase in work-from-home), just whether or not the office space is leased.

Click on graph for larger image.

Click on graph for larger image.This graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

The office vacancy rate was elevated prior to the pandemic and moved up during the pandemic.

Reis also reported that office effective rents increased 0.4% in Q3; rents are about at the same level as before the pandemic.

And from Reis on Retail:

Our data shows the national vacancy for neighborhood and community shopping center has stayed flat at 10.3% since a year ago, while asking/effective rent kept virtually unchanged in the 3rd quarter. Trend data on regional and super regional malls tells a similar story. Vacancy ticked up 10 basis-point to 11.1% and effective rent was up 0.1% this quarter. Despite some signs of stabilization, regional mall properties continue to be the most at-risk retail subtype according to our commercial mortgage delinquency data, and they are driving overall delinquency behavior among retail assets.

Reis reported that the vacancy rate for regional malls was 11.1% in Q3 2022, up from 11.0% in Q1 2021, and down from 11.3% in Q3 2021. The regional mall vacancy rate peaked at 11.5% in Q2 2021.

For Neighborhood and Community malls (strip malls), the vacancy rate was 10.3% in Q3, unchanged from 10.3% in Q2, and down from 10.4% in Q3 2021. For strip malls, the vacancy rate peaked during the pandemic at 10.6% in both Q1 and Q2 2021.

This graph shows the strip mall vacancy rate starting in 1980 (prior to 2000 the data is annual). The regional mall data starts in 2000. Back in the '80s, there was overbuilding in the mall sector even as the vacancy rate was rising. This was due to the very loose commercial lending that led to the S&L crisis.

This graph shows the strip mall vacancy rate starting in 1980 (prior to 2000 the data is annual). The regional mall data starts in 2000. Back in the '80s, there was overbuilding in the mall sector even as the vacancy rate was rising. This was due to the very loose commercial lending that led to the S&L crisis. In the mid-'00s, mall investment picked up as mall builders followed the "roof tops" of the residential boom (more loose lending). This led to the vacancy rate moving higher even before the recession started. Then there was a sharp increase in the vacancy rate during the recession and financial crisis.

In the last several years, even prior to the pandemic, the regional mall vacancy rates increased significantly from an already elevated level.

Effective rents have been mostly unchanged for regional malls over the last 4+ years, and flat for strip malls for 3+ years.

All vacancy data courtesy of Moody’s Analytics Reis

Apartments: Net Absorption Very Low in Q3, New Construction Deliveries Even Lower

by Calculated Risk on 10/05/2022 11:54:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Apartments: Net Absorption Very Low in Q3, New Construction Deliveries Even Lower

A brief excerpt:

Moody’s Analytics also reported the effective rents were up 1.7% in Q3 from Q2, and up 10.2% year-over-year (YoY). This is a sharp slowdown from Q2 when rents were up 16.9% YoY.There is more in the article. You can subscribe at https://calculatedrisk.substack.com/

Click on graph for larger image.

Last week, I posted a graph of the year-over-year change for various measures of rent. The Zillow measure is up 12.3% YoY in August, down from 13.8% YoY in July. This is down from a peak of 17.2% YoY in February. The ApartmentList measure is up 7.5% YoY as of September, down from 9.8% in August. This is down from the peak of 18.0% YoY last November.

Reis’ survey (dashed red) is quarterly and shows a similar slowdown in effective rents.

...

The bottom line is apartment demand was soft in Q3, household formation has slowed sharply, and there are a large number of apartments in the pipeline. We should see completions above net absorption soon, and the completion of all these units under construction should help with rent pressure.

ISM® Services Index Decreased to 56.7% in September

by Calculated Risk on 10/05/2022 10:04:00 AM

(Posted with permission). The ISM® Services index was at 56.7%, down from 56.9% last month. The employment index increased to 53.0%, from 50.2%. Note: Above 50 indicates expansion, below 50 in contraction.

From the Institute for Supply Management: Services PMI® at 56.7% September 2022 Services ISM® Report On Business®

Economic activity in the services sector grew in September for the 28th month in a row — with the Services PMI® registering 56.7 percent — say the nation’s purchasing and supply executives in the latest Services ISM® Report On Business®.This was above expectations.

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee: “In September, the Services PMI® registered 56.7 percent, 0.2 percentage point lower than August’s reading of 56.9 percent. The Business Activity Index registered 59.1 percent, a decrease of 1.8 percentage points compared to the reading of 60.9 percent in August. The New Orders Index figure of 60.6 percent is 1.2 percentage points lower than the August reading of 61.8 percent.

emphasis added

Trade Deficit decreased to $67.4 Billion in August

by Calculated Risk on 10/05/2022 08:38:00 AM

From the Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $67.4 billion in August, down $3.1 billion from $70.5 billion in July, revised.

August exports were $258.9 billion, $0.7 billion less than July exports. August imports were $326.3 billion, $3.7 billion less than July imports.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Exports increased and imports decreased in August.

Exports are up 20% year-over-year; imports are up 14% year-over-year.

Both imports and exports decreased sharply due to COVID-19 and have now bounced back.

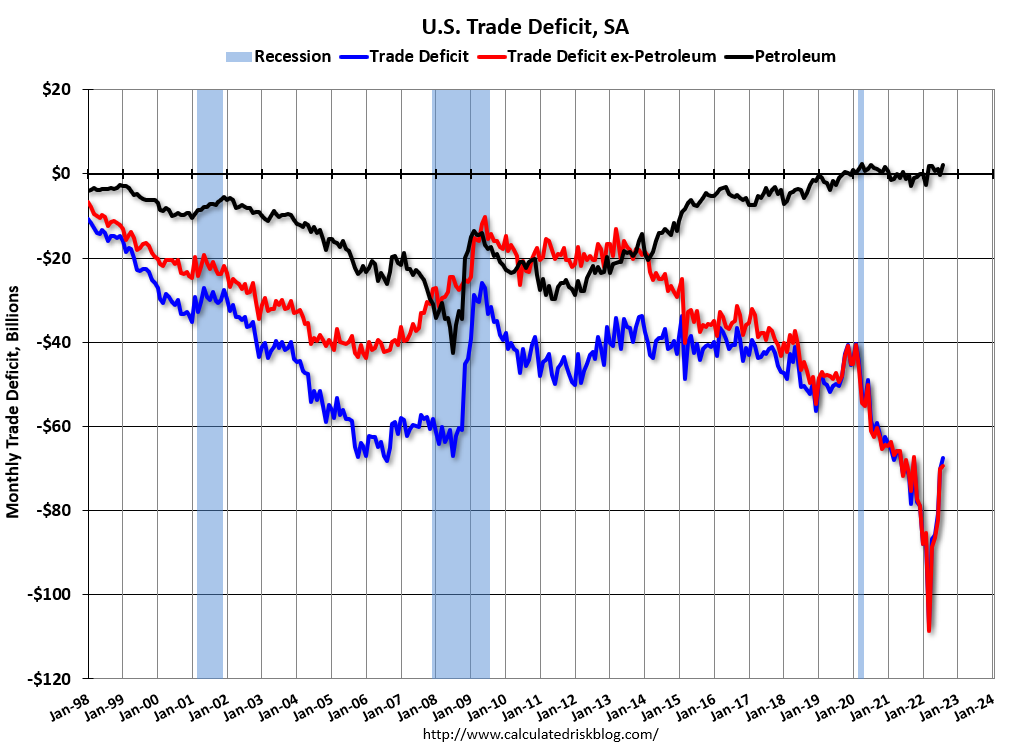

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Note that net, imports and exports of petroleum products are close to zero.

The trade deficit with China increased to $37.4 billion in August, from $21.7 billion a year ago.

The trade deficit was slightly lower than the consensus forecast.

ADP: Private Employment Increased 208,000 in September

by Calculated Risk on 10/05/2022 08:20:00 AM

Note: This is the second release of a new methodology. Historical data based on the new methodology is available.

From ADP: ADP National Employment Report: Private Sector Employment Increased by

208,000 Jobs in September; Annual Pay was Up 7.8%

Private sector employment increased by 208,000 jobs in September and annual pay was up 7.8% year-over-year, according to the September ADP® National Employment ReportTM produced by the ADP Research Institute® in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”).This was close to the consensus forecast of 205,000. The BLS report will be released Friday, and the consensus is for 250 thousand non-farm payroll jobs added in September.

The jobs report and pay insights use ADP’s fine-grained anonymized and aggregated payroll data of over 25 million U.S. employees to provide a representative picture of the labor market. The report details the current month’s total private employment change, and weekly job data from the previous month. ADP’s pay measure uniquely captures the earnings of a cohort of almost 10 million employees over a 12-month period.

“We are continuing to see steady job gains,” said Nela Richardson, chief economist, ADP. “While job stayers saw a pay increase, annual pay growth for job changers in September is down from August.”

emphasis added