RSS Feed

RSS Feed by Calculated Risk on 10/11/2022 08:10:00 PM

Tuesday, October 11, 2022

Wednesday: PPI, FOMC Minutes

From Matthew Graham at Mortgage News Daily: Mortgage Rates Escape Harsher Fate as Bonds Fight to Hold Ground

From Matthew Graham at Mortgage News Daily: Mortgage Rates Escape Harsher Fate as Bonds Fight to Hold Ground

Treasury futures took a beating on Monday as the UK bond market once again traded in panic mode. The high rate implications were still in place as of Tuesday's overnight trading. 10yr Treasury yields broke above 4.0% yet again and continued struggling to move much lower until later in the trading day. ... The weaker opening levels resulted in mortgage rates remaining at long term highs, but they would have been higher highs had it not been for an admirable show of support in the bond market. In fact, by the afternoon hours, Treasuries and MBS were both very close to the same territory seen on Friday afternoon ... [30 year fixed 7.14%]Wednesday:

emphasis added

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, The Producer Price Index for September from the BLS. The consensus is for a 0.2% increase in PPI, and a 0.3% increase in core PPI.

• At 2:00 PM, FOMC Minutes, Meeting of September 20-21, 2022

MBA: Mortgage Credit Availability was Never Excessive During the Recent Housing Boom

by Calculated Risk on 10/11/2022 10:39:00 AM

Today, in the Calculated Risk Real Estate Newsletter: MBA: Mortgage Credit Availability was Never Excessive During the Recent Housing Boom

A brief excerpt:

Although mortgage credit availability decreased in September (the MBA headline below), the most important point is mortgage credit availability was never excessive during the boom. Here is the expanded series from the MBA of mortgage credit availability that includes the bubble years (2004 - 2006).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

Look at that huge increase in mortgage credit availability back in the 2004 - 2006 period (remember “fog a mirror, get a loan”, NINJA loans: No Income, No Job or Assets?). In the recent boom, lending was reasonably solid, and most homeowners have substantial equity in their homes. Although I expect an increase in foreclosures from record low levels, there will not be a huge wave of foreclosures as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.

Here is the article from the MBA: Mortgage Credit Availability Decreased in September

Second Home Market: South Lake Tahoe in September

by Calculated Risk on 10/11/2022 08:15:00 AM

With the pandemic, there was a surge in 2nd home buying.

I'm looking at data for some second home markets - and I'm tracking those markets to see if there is an impact from lending changes, rising mortgage rates or the easing of the pandemic.

This graph is for South Lake Tahoe since 2004 through September 2022, and shows inventory (blue), and the year-over-year (YoY) change in the median price (12-month average).

Note: The median price is distorted by the mix, but this is the available data.

Click on graph for larger image.

Click on graph for larger image.

Following the housing bubble, prices declined for several years in South Lake Tahoe, with the median price falling about 50% from the bubble peak.

Currently inventory is still very low, but still up 4-fold from the record low set in February 2022, and up 38% year-over-year. Prices are up 2.3% YoY (and the YoY change has been trending down).

It is possible that the YoY change will turn negative soon - even with inventory at historically fairly low levels.

Monday, October 10, 2022

Leading Index for Commercial Real Estate "Rises" in September

by Calculated Risk on 10/10/2022 03:08:00 PM

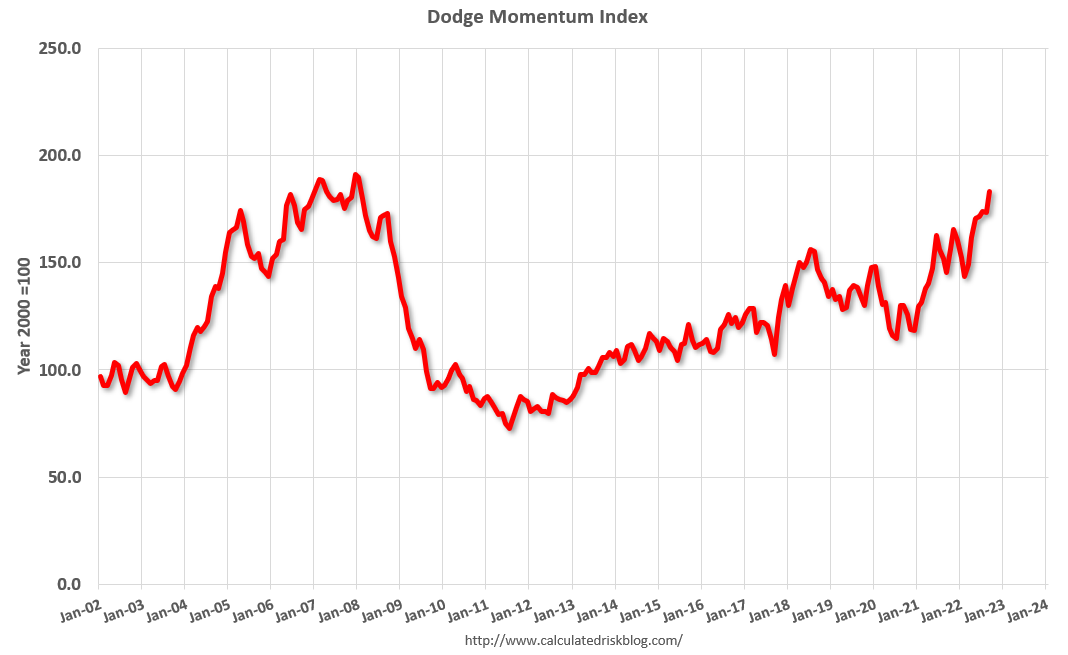

From Dodge Data Analytics: Dodge Momentum Index Rises In September

The Dodge Momentum Index (DMI), issued by Dodge Construction Network, improved 5.7% (2000=100) in September to 183.2 from the revised August reading of 173.4. The DMI is a monthly measure of the initial report for nonresidential building projects in planning, shown to lead construction spending for nonresidential buildings by a full year. In September, the commercial component of the Momentum Index rose 2.9%, while the institutional component also increased, seeing a double-digit gain of 11.7%.

After a solid performance in September, the DMI landed less than 5% below an all-time high. On the commercial side, the figure was primarily bolstered by an influx of data centers entering the planning queue. The institutional component saw a notable increase in research and development laboratory projects in the education sector, with solid contributions from healthcare and recreation projects entering the planning process. On a year-over-year basis, the DMI was 26% higher than September in 2021; the commercial component was up 25%, and institutional planning was 28% higher.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Dodge Momentum Index since 2002. The index was at 183.2 in September, up from 173.4 in August.

According to Dodge, this index leads "construction spending for nonresidential buildings by a full year". This index suggests a solid pickup in commercial real estate construction at the end of this year and into 2023.

Current State of the Housing Market; Overview for mid-October

by Calculated Risk on 10/10/2022 11:35:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Current State of the Housing Market

A brief excerpt:

Over the last month …There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

1. New listings have declined further year-over-year.

2. Mortgage rates have increased further pushing monthly payments up sharply.

3. House prices have started to decline month-over-month (MoM) as measured by the repeat sales indexes.

...

The following graph from MortgageNewsDaily.com shows mortgage rates over the last 12 months.

Currently mortgage rates are at a 20-year high. The payment on a $500,000 house with 20% last year, with 3.2% 30-year mortgage rates, would be around $1,730 for principal and interest. The payment for the same house, with prices up 15% and mortgage rates at 7.1%, would be $3,091 - an increase of 79%!

...

A week from Thursday, the NAR will release existing home sales for September. This report will likely show another sharp year-over-year decline in sales for September.

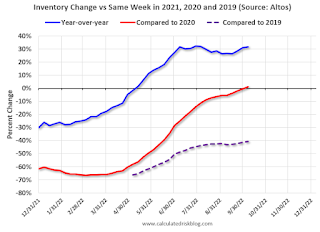

Housing October 10th Weekly Update: Inventory Increased Slightly; Now Above Same Week in 2020

by Calculated Risk on 10/10/2022 08:45:00 AM

Inventory is now above the levels for the same week in 2020 (milestone 3 below).

2022: +0.1K

2021: -2.2K

2020: -7.7K

2019: -8.4K

Inventory bottomed seasonally at the beginning of March 2022 and is now up 133% since then. Altos reports inventory is up 31.8% year-over-year.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of October 7th, inventory was at 561 thousand (7-day average), compared to 561 thousand the prior week.

Compared to the same week in 2021, inventory is up 31.8% from 426 thousand, and compared to the same week in 2020 inventory is up 1.1% from 555 thousand. Compared to 3 years ago, inventory is down 40.7% from 947 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 13, 2022, for Altos) ✅

3. Inventory up compared to two years ago (happened on October 9, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 40.7%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 13, 2022, for Altos) ✅

3. Inventory up compared to two years ago (happened on October 9, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 40.7%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

Two years ago (in 2020) inventory was declining all year. Inventory is now up compared to the same week in 2020!

A key will be if inventory increases in the Fall this year.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 10/10/2022 08:21:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides.

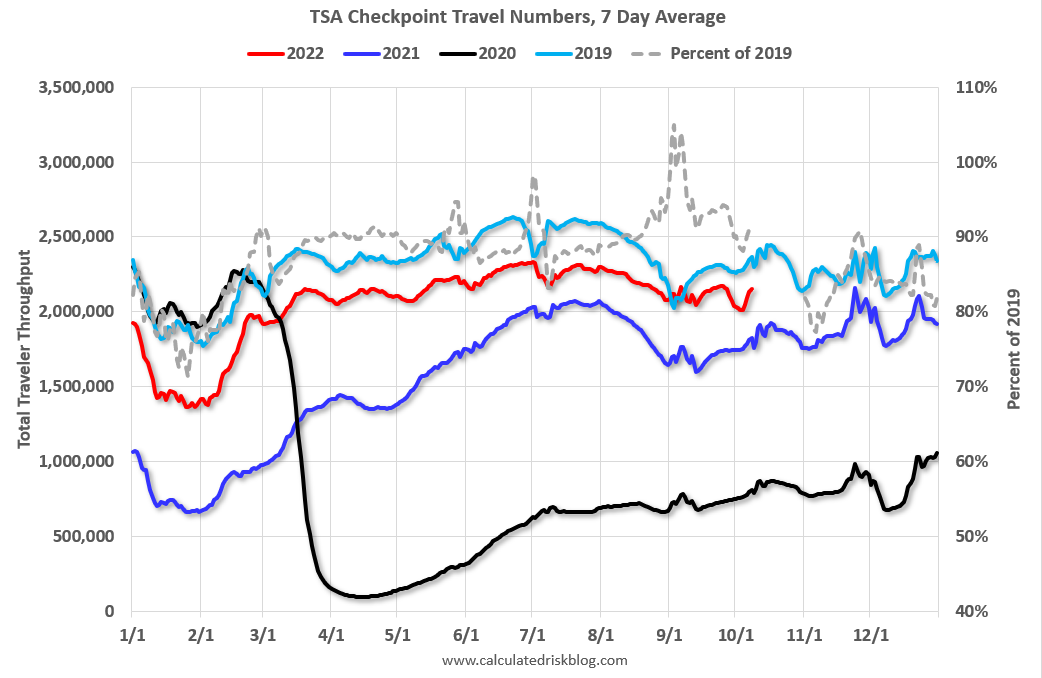

The TSA is providing daily travel numbers.

This data is as of October 8th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 9.1% from the same day in 2019 (90.9% of 2019). (Dashed line)

Air travel - as a percent of 2019 - had picked up towards the end of Summer, but is now, off about 10% from 2019 like earlier in the year.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through October 6th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $88 million last week, down about 35% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $88 million last week, down about 35% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Oct 1st. The occupancy rate was down 2.4% compared to the same week in 2019.

The 4-week average of the occupancy rate is close to the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

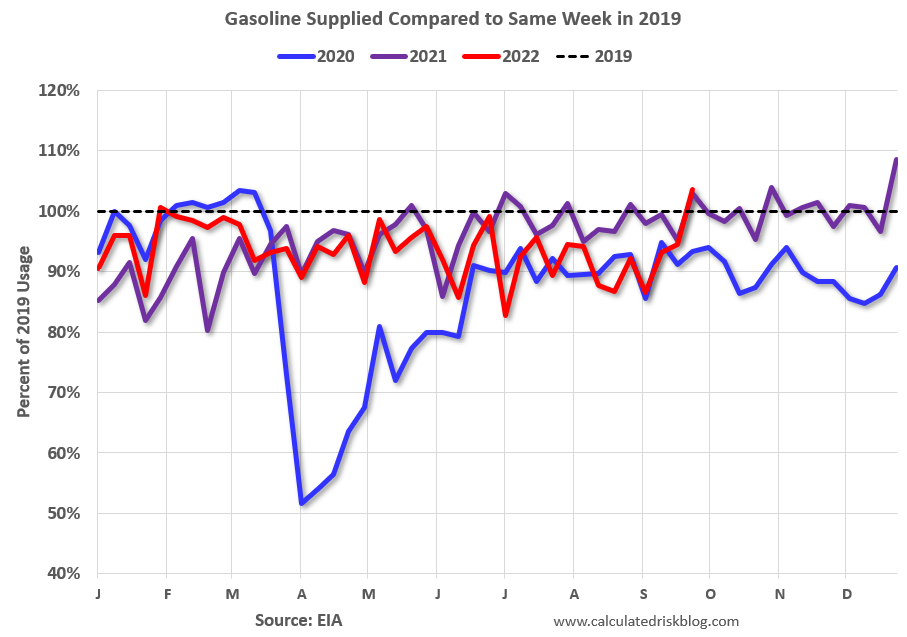

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of September 30th, gasoline supplied was up 3.6% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020. This is only the 2nd week this year that gasoline supplied was above 2019 levels.

Sunday, October 09, 2022

Sunday Night Futures

by Calculated Risk on 10/09/2022 06:55:00 PM

Weekend:

• Schedule for Week of October 9, 2022

Monday:

• Columbus Day Holiday: Banks will be closed in observance of Columbus Day. The stock market will be open. No economic releases are scheduled.

• At 1:35 PM ET, Speech, Fed Vice Chair Lael Brainard, Restoring Price Stability in an Uncertain Economic Environment, At the National Association for Business Economics (NABE) Annual Meeting, Chicago, Ill.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 26 and DOW futures are down 174 (fair value).

Oil prices were up over the last week with WTI futures at $92.64 per barrel and Brent at $97.92 per barrel. A year ago, WTI was at $80, and Brent was at $82 - so WTI oil prices are up 15% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.91 per gallon. A year ago, prices were at $3.25 per gallon, so gasoline prices are up $0.66 per gallon year-over-year. NOTE: Gasoline prices in Los Angeles have spiked to a near record $6.40 per gallon due to refinery issues.

Housing Discussion with Fortune's Lance Lambert

by Calculated Risk on 10/09/2022 11:37:00 AM

On Friday, Fortune’s Lance Lambert and I discussed the US housing market.

Click here for audio

One of the key topics was household formation. Here is an excellent summary article by Katie McKellar at desert.com: The most ‘underreported’ factor influencing housing market, according to Calculated Risk

Bill McBride, author of the economics blog Calculated Risk, said there’s a key reason why both rent and home price growth is slowing amid the U.S. housing correction playing out today.

In a live Twitter Space hosted by Fortune Magazine on Friday, McBride called it the most “underreported” factor.

What is it? Household formation — both because of how much it accelerated amid the COVID-19 pandemic and how it’s slowing down now.

Wholesale Used Car Prices Declined in September; Prices Down Slightly Year-over-year

by Calculated Risk on 10/09/2022 08:11:00 AM

From Manheim Consulting on Friday: Wholesale Used-Vehicle Prices See Large Decline Again in September

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) decreased 3.0% in September from August. The Manheim Used Vehicle Value Index declined to 204.5 and is now down 0.1% from a year ago. The non-adjusted price change in September was a decline of 2.1% compared to August, moving the unadjusted average price down 2.3% year over year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices decreased in September and were down 0.1% year-over-year (YoY).

This also suggests the consumer price index for used cars and trucks will be down again in September.

It is likely this index will be down more than 10% YoY in October.