RSS Feed

RSS Feed by Calculated Risk on 11/15/2022 08:08:00 PM

Tuesday, November 15, 2022

Wednesday: Retail Sales, Industrial Production, Homebuilder Survey

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, Retail sales for October will be released. The consensus is for a 0.9% increase in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for October. The consensus is for a 0.2% increase in Industrial Production, and for Capacity Utilization to increase to 80.4%.

• At 10:00 AM, The November NAHB homebuilder survey. The consensus is for a reading of 36, down from 38. Any number below 50 indicates that more builders view sales conditions as poor than good.

• During the day: The AIA's Architecture Billings Index for October (a leading indicator for commercial real estate).

Inflation: Comparing to 1980, and Core CPI ex-Shelter

by Calculated Risk on 11/15/2022 03:47:00 PM

Earlier this year I wrote: Housing: Don't Compare the Current Housing Boom to the Bubble and Bust. I argued the 1978 to 1982 period was a more similar period for housing.

One of the graphs I presented was of year-over-year inflation.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change in inflation since 1959.

The black arrows point to the pickup in 1979 and in 2021.

Also note that recessions usually follow spikes in inflation as the Fed raises rates.

Although not a perfect comparison, I think the 1978 to 1982 is better than comparing to the housing bubble period with all the loose lending.

The second graph shows the year-over-year change in Core CPI ex-Shelter (blue), and the one month change annualized (red).

Also note that recessions usually follow spikes in inflation as the Fed raises rates.

Although not a perfect comparison, I think the 1978 to 1982 is better than comparing to the housing bubble period with all the loose lending.

The second graph shows the year-over-year change in Core CPI ex-Shelter (blue), and the one month change annualized (red).

The year-over-year change was at 5.9% in October, down from 6.7% in September. And the annualized one-month change was negative in October!

I think this is important since there is growing evidence that rents are falling (more than seasonally). This is likely due to the sharp slowdown in household formation (since household formation surged during the pandemic, partially related to work-from-home), and will likely continue with the record number of housing units under construction.

I think this is important since there is growing evidence that rents are falling (more than seasonally). This is likely due to the sharp slowdown in household formation (since household formation surged during the pandemic, partially related to work-from-home), and will likely continue with the record number of housing units under construction.

NY Fed Q3 Report: Household Debt Increases, Delinquencies "very low"

by Calculated Risk on 11/15/2022 11:15:00 AM

From the NY Fed: Total Household Debt Reaches $16.51 trillion in Q3 2022; Mortgage and Auto Loan Originations Decline

The Federal Reserve Bank of New York's Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit. The Report shows an increase in total household debt in the third quarter of 2022, increasing by $351 billion (2.2%) to $16.51 trillion. Balances now stand $2.36 trillion higher than at the end of 2019, before the pandemic recession. The report is based on data from the New York Fed's nationally representative Consumer Credit Panel.

Mortgage balances rose by $282 billion in the third quarter of 2022 and stood at $11.67 trillion at the end of September, representing a $1 trillion increase from the previous year. Credit card balances also increased by $38 billion. The 15% year-over-year increase in credit card balances represents the largest in more than 20 years. Auto loan balances increased by $22 billion in the third quarter, consistent with the upward trajectory seen since 2011. Student loan balances slightly declined and now stand at $1.57 trillion. In total, non-housing balances grew by $66 billion.

Mortgage originations, which include refinances, stood at $633 billion in the third quarter, representing a $126 billion decline from the second quarter and a return to pre-pandemic volumes. The volume of newly originated auto loans was $185 billion, a slight reduction from the previous quarter but still elevated compared to the average volumes seen through the 2018-2019 period. Aggregate limits on credit card accounts increased by $82 billion and now stand at $4.3 trillion.

"Credit card, mortgage, and auto loan balances continued to increase in the third quarter of 2022 reflecting a combination of robust consumer demand and higher prices," said Donghoon Lee, Economic Research Advisor at the New York Fed. "However, new mortgage originations have slowed to pre-pandemic levels amid rising interest rates."

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here are three graphs from the report:

The first graph shows aggregate consumer debt increased in Q3. Household debt previously peaked in 2008 and bottomed in Q3 2013. Unlike following the great recession, there wasn't a huge decline in debt during the pandemic.

From the NY Fed:

Aggregate household debt balances increased by $351 billion in the third quarter of 2022, a 2.2% rise from 2022Q2. Balances now stand at $16.51 trillion and have increased by $2.36 trillion since the end of 2019, just before the pandemic recession.

The second graph shows the percent of debt in delinquency.

The second graph shows the percent of debt in delinquency.The overall delinquency rate was unchanged in Q3. From the NY Fed:

Aggregate delinquency rates were unchanged in the third quarter of 2022 and remained very low, after declining sharply through the beginning of the pandemic. As of September, 2.7% of outstanding debt was in some stage of delinquency, a 2.1 percentage point decrease from the last quarter of 2019, just before the COVID-19 pandemic hit the United States

The third graph shows Mortgage Originations by Credit Score.

The third graph shows Mortgage Originations by Credit Score.From the NY Fed:

Mortgage originations, measured as appearances of new mortgages on consumer credit reports, declined to $633 billion in 2022Q3, ending the period of high volumes of origination through the pandemic. ... The median credit score of newly originated mortgages declined again, to 768, down from a series high in 2021Q1 of 788 and returning to pre-covid levels which remain very high and reflect continuing high lending standards.There is much more in the report.

Lawler: Are US Rents Falling?

by Calculated Risk on 11/15/2022 09:42:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Are US Rents Falling?

A brief excerpt:

After increasing at a pace unseen in US history from the Spring of 2021 to the middle of 2022, it appears as if US rent growth has slowed sharply over the past few months. Indeed, the most “high frequency” data (meaning most timely) suggest that US rents may have stopped increasing this Fall, and may actually have begun to decline.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

Below is a table showing the monthly % changes in these rent indexes NOT adjusted for seasonal fluctuations.

CR Note: The CoreLogic index was negative in September (released this morning).

Note that the Apartment List Index, which is not smoothed, has shown two consecutive monthly declines, while the Zillow Index, which IS smoothed, fell for the [first] time in over two years last month. Note also that the CoreLogic Index, available only through August and which is smoothed, decelerated sharply during “August.”

The above table can be a bit misleading, however, because all three rent indexes display relatively modest but statistically significant seasonal fluctuations ...

While none of these rent indexes is perfect, the latest data suggest that US rent growth has slowed sharply in recent months, and at best has been growing in the low single digits and quite possibly may have actually turned slightly negative last month. If so, that is certainly no surprise, and as I said in an earlier report, I expect that US rents in 2023 will be lower than rents during this Summer and Fall.

CoreLogic: Annual Single-Family Rent Growth Decelerates

by Calculated Risk on 11/15/2022 09:21:00 AM

From CoreLogic: Annual Single-Family Rent Growth Decelerates for Fifth Consecutive Month and Seasonal Patterns Return

Consistent evidence of a single-family rental market cooldown follows nearly two years of above-trend rental price hikes. Single-family rent growth in September 2022 slowed for the fifth consecutive month to 10.2% from a high of 13.9% in April 2022. Additionally, rent growth this September was slightly below that of September 2021. The rent increase slowdown comes as inflation stretches tenants’ pocketbooks.

“Annual single-family rent growth decelerated for the fifth consecutive month in September but remained at more than twice the pre-pandemic growth rate,” said Molly Boesel, principal economist at CoreLogic. “High mortgage interest rates may be causing potential homebuyers to hit pause and remain renters, keeping pressure on rent prices. However, the monthly rent change was negative in September, resuming the typical seasonal pattern for the first time since 2019, which could signal the beginning of rent price growth normalization.”

Click on graph for larger image.

Click on graph for larger image.This graph from CoreLogic shows the YoY change in single-family rents.

Year-over-year rent growth slowed to 10.2% in September - and the month-over-month change was negative in September.

Monday, November 14, 2022

Tuesday: PPI, NY Fed Mfg, Q3 Household Debt and Credit

by Calculated Risk on 11/14/2022 08:01:00 PM

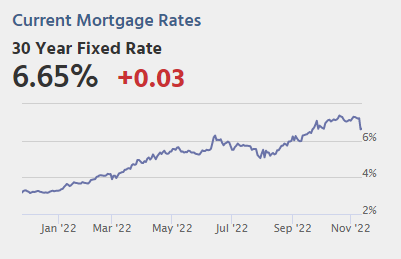

From Matthew Graham at Mortgage News Daily: Mortgage Rates Roughly Unchanged After Last Week's Huge Drop

From Matthew Graham at Mortgage News Daily: Mortgage Rates Roughly Unchanged After Last Week's Huge Drop

If you're just getting caught up, last Thursday was one for the record books--at least when it comes to the daily records that exist going back to 2009. No other day has seen as big of a drop in the average 30yr fixed mortgage rate (0.60%).Tuesday:

The bonds that dictate mortgage rates lost quite a bit of ground today, but that didn't translate to any meaningful damage. This speaks to the 'uncertainty premium' that oftentimes prevents lenders from dropping rates as much as the market might suggest at the end of any given week. It's usually more noticeable before 3-day weekends, but was easily lost in the shuffle given the scope of the movement. ... [30 year fixed 6.65%]

emphasis added

• At 8:30 AM ET, The Producer Price Index for October from the BLS. The consensus is for a 0.5% increase in PPI, and a 0.4% increase in core PPI.

• Also, at 8:30 AM, The New York Fed Empire State manufacturing survey for November. The consensus is for a reading of -7.0, up from -9.1.

• At 11:00 AM: NY Fed, Q3 Quarterly Report on Household Debt and Credit

2nd Look at Local Housing Markets in October

by Calculated Risk on 11/14/2022 12:23:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in October

A brief excerpt:

This is the second look at local markets in October. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Closed sales in October were mostly for contracts signed in August and September. Mortgage rates moved higher in September, and that impacted closed sales in October.

The further sharp increase in mortgage rates in October - with the 30-year mortgage over 7% - will impact closed sales in November and December.

...

In October, sales were down 29.2%. In September, these same markets were down 24.1% YoY Not Seasonally Adjusted (NSA).

Note that in October 2022, there were the same number of selling days as in October 2021, so the SA decline will be similar to the NSA decline. And this suggests another step down in sales!

Many more local markets to come!

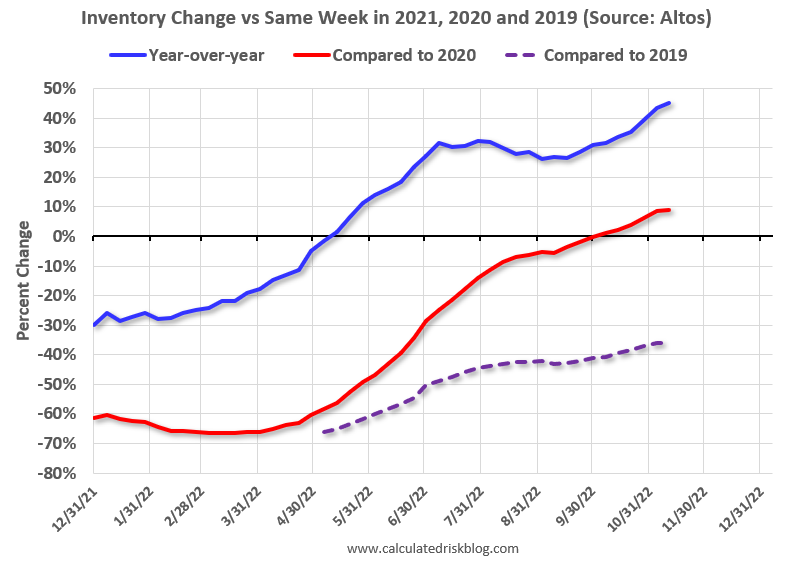

Housing November 14th Weekly Update: Inventory Decreased Slightly Week-over-week

by Calculated Risk on 11/14/2022 09:00:00 AM

Active inventory decreased slightly. Here are the same week inventory changes for the last four years (usually inventory declines seasonally through the Winter):

2022: -3.5K (smaller than usual decrease in inventory)

2021: -6.9K

2020: -5.1K

2019: -6.3K

Altos reports inventory is down 0.6% week-over-week.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of November 11th, inventory was at 572 thousand (7-day average), compared to 575 thousand the prior week.

Compared to the same week in 2021, inventory is up 45.1% from 394 thousand, and compared to the same week in 2020 inventory is up 8.9% from 525 thousand. Compared to 3 years ago (2019), inventory is down 35.9% from 892 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 35.9%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 35.9%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory declines slower than usual during the winter months.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 11/14/2022 08:29:00 AM

These indicators are mostly for travel and entertainment. It was interesting to watch these sectors recover as the pandemic impact subsided.

The TSA is providing daily travel numbers.

This data is as of November 13th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is 5.5% below the same week in 2019 (94.5% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has picked up recently.

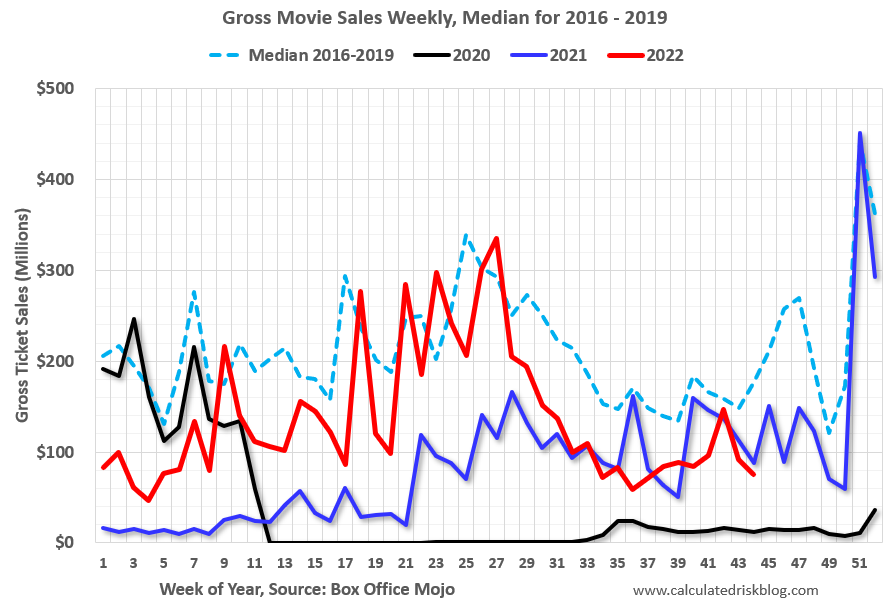

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through November 10th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $75 million last week, down about 58% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $75 million last week, down about 58% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Nov 5th. The occupancy rate was down 9.2% compared to the same week in 2019.

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue) and close to 2019 levels.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of November 4th, gasoline supplied was down 1.5% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020.

Sunday, November 13, 2022

Sunday Night Futures

by Calculated Risk on 11/13/2022 08:13:00 PM

Weekend:

• Schedule for Week of November 13, 2022

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 11 and DOW futures are down 70 (fair value).

Oil prices were down over the last week with WTI futures at $88.96 per barrel and Brent at $5.99 per barrel. A year ago, WTI was at $81, and Brent was at $83 - so WTI oil prices are up 10% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.78 per gallon. A year ago, prices were at $3.40 per gallon, so gasoline prices are up $0.38 per gallon year-over-year.