RSS Feed

RSS Feed by Calculated Risk on 12/02/2022 08:46:00 PM

Friday, December 02, 2022

COVID Dec 2, 2022: Update on Cases, Hospitalizations and Deaths

NOTE: This was a holiday week, and cases and deaths reporting always declines during holiday weeks.

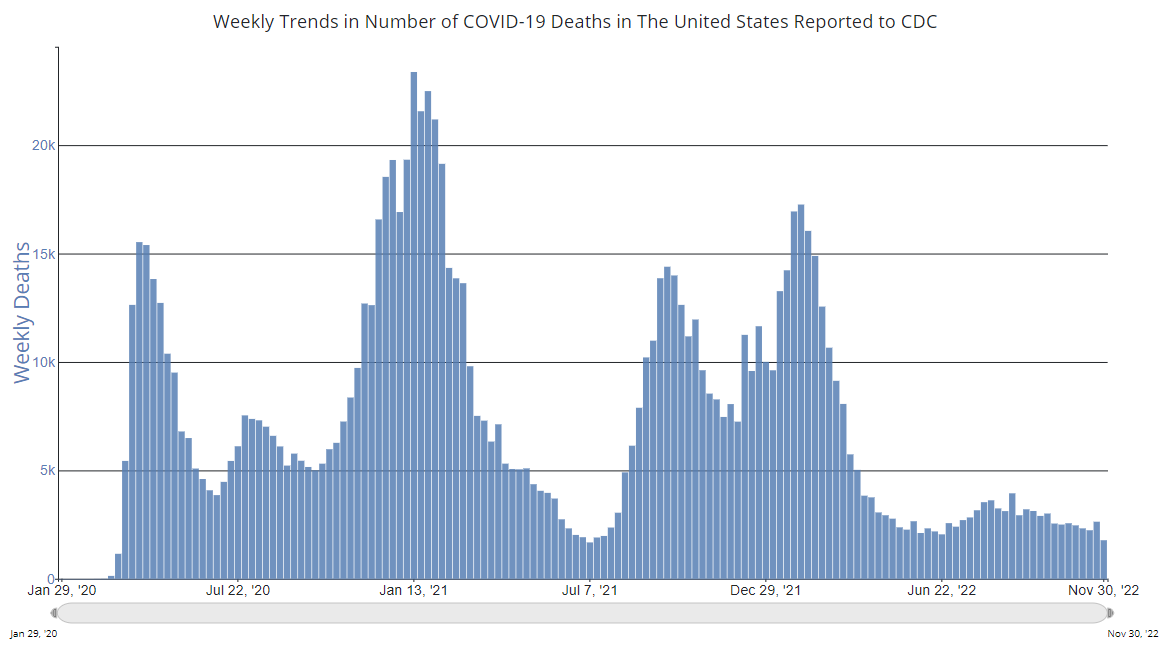

On COVID (focus on hospitalizations and deaths). Data has switched to weekly.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 303,101 | 306,856 | ≤35,0001 | |

| Hospitalized2🚩 | 25,603 | 22,011 | ≤3,0001 | |

| Deaths per Week2 | 1,780 | 2,634 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Hotels: Occupancy Rate Down 0.5% Compared to Same Week in 2019

by Calculated Risk on 12/02/2022 03:09:00 PM

Due to the Thanksgiving holiday, U.S. hotel performance came in lower than the previous week and showed mixed comparisons to 2019, according to STR‘s latest data through Nov. 26.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Nov. 20-26, 2022 (percentage change from comparable week in 2019*

• Occupancy: 50.4% (-0.5%)

• Average daily rate (ADR): US$135.49 (+20.4%)

• Revenue per available room (RevPAR): US$68.27 (+19.9%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue) and close to 2019 levels.

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate continue to decline into the Winter.

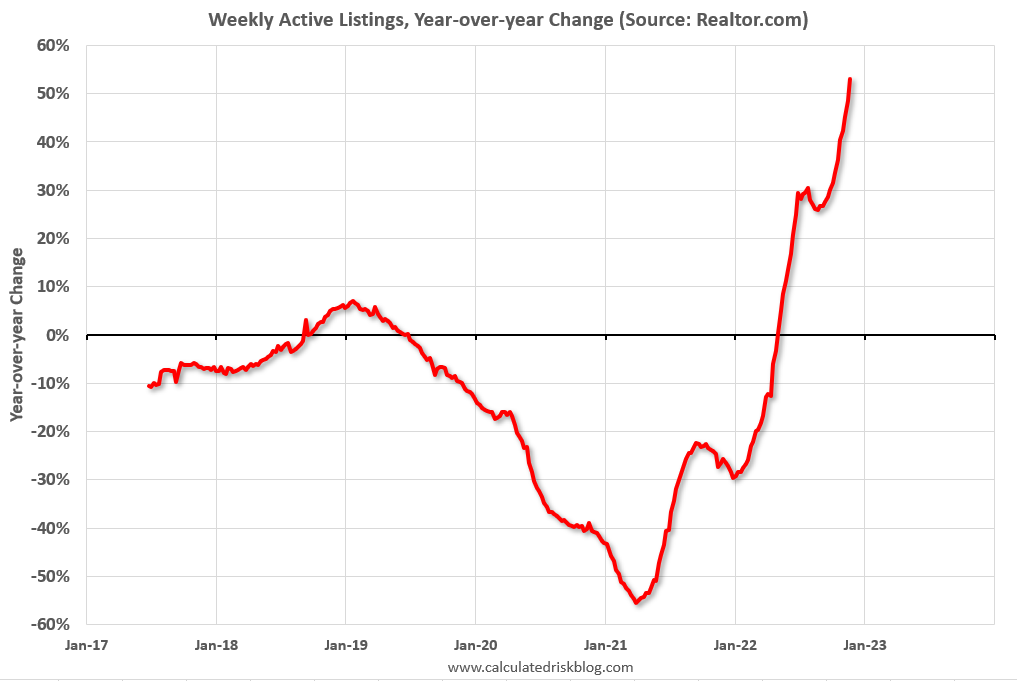

Realtor.com Reports Weekly Active Inventory Up 53% Year-over-year; New Listings Down 17%

by Calculated Risk on 12/02/2022 01:44:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Nov 26, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, increasing 53% above one year ago. Inventory accelerated again, notching a seventh week in a row with yearly trend growth roughly at or above 2% higher than the previous week.

...

• New listings–a measure of sellers putting homes up for sale–were again down, dropping 17% from one year ago. This marks the twenty-first consecutive week of year-over-year declines in homeowners listing their home for sale.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change earlier this year, from down 30% at the beginning of the year, to up 29% YoY at the beginning of July.

Then the Realtor.com data was stuck at up around 26% to 30% YoY for 14 weeks in a row. This was due to the slowdown in new listings, even as sales had fallen sharply.

Now YoY inventory is increasing again with even higher mortgage rates, suggesting sales are off more than new listings.

Comments on November Employment Report

by Calculated Risk on 12/02/2022 09:33:00 AM

The headline jobs number in the November employment report was above expectations, however employment for the previous two months was revised down by 23,000, combined. The participation rate decreased, and the unemployment rate was unchanged at 3.7%.

Leisure and hospitality gained 88 thousand jobs in November. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.2 million jobs, and are now down 980 thousand jobs since February 2020. So, leisure and hospitality has now added back about 88% all of the jobs lost in March and April 2020.

Construction employment increased 20 thousand and is now 126 thousand above the pre-pandemic level.

Manufacturing added 14 thousand jobs and is now 149 thousand above the pre-pandemic level.

In November, the year-over-year employment change was 4.90 million jobs.

Seasonal Retail Hiring

Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.Retailers hired 257 thousand workers Not Seasonally Adjusted (NSA) net in November.

This was seasonally adjusted (SA) to a loss of 29.9 thousand jobs in November.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 participation rate decreased in November to 82.4% from 82.5% in October, and the 25 to 54 employment population ratio decreased to 79.7% from 79.8% the previous month.

Both have declined recently - but both are close to the pre-pandemic levels and indicate almost all of the prime age workers have returned to the labor force.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 6.7% from 6.8% in the previous month. This is down from the record high in April 22.9% and ties the lowest level on record (series started in 1994). This measure is below the level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more.

According to the BLS, there are 1.230 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.165 million the previous month.

This is close to pre-pandemic levels.

Summary:

The headline monthly jobs number was above expectations; however, employment for the previous two months was revised down by 23,000, combined.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons was about unchanged at 3.7 million in November. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons increased in November to 3.685 million from 3.660 million in October. This is below pre-recession levels and near the fewest part time workers (for economic reasons) in over 20 years.

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 6.7% from 6.8% in the previous month. This is down from the record high in April 22.9% and ties the lowest level on record (series started in 1994). This measure is below the level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.230 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.165 million the previous month.

This is close to pre-pandemic levels.

Summary:

The headline monthly jobs number was above expectations; however, employment for the previous two months was revised down by 23,000, combined.

The headline unemployment rate was unchanged at 3.7%, and U-6 declined to tie a record low at 6.7%.

Overall, this was another solid employment report.

November Employment Report: 263 thousand Jobs, 3.7% Unemployment Rate

by Calculated Risk on 12/02/2022 08:44:00 AM

From the BLS:

Total nonfarm payroll employment increased by 263,000 in November, and the unemployment rate was unchanged at 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, health care, and government. Employment declined in retail trade and in transportation and warehousing.

...

The change in total nonfarm payroll employment for September was revised down by 46,000, from +315,000 to +269,000, and the change for October was revised up by 23,000, from +261,000 to +284,000. With these revisions, employment gains in September and October combined were 23,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms.

However, as of August 2022, the total number of jobs had returned and are now 1.044 million above pre-pandemic levels. I'll post this graph through the January 2023 report (includes the annual revision).

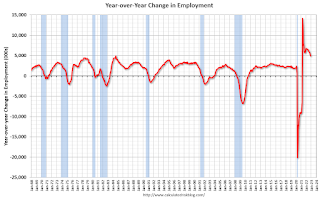

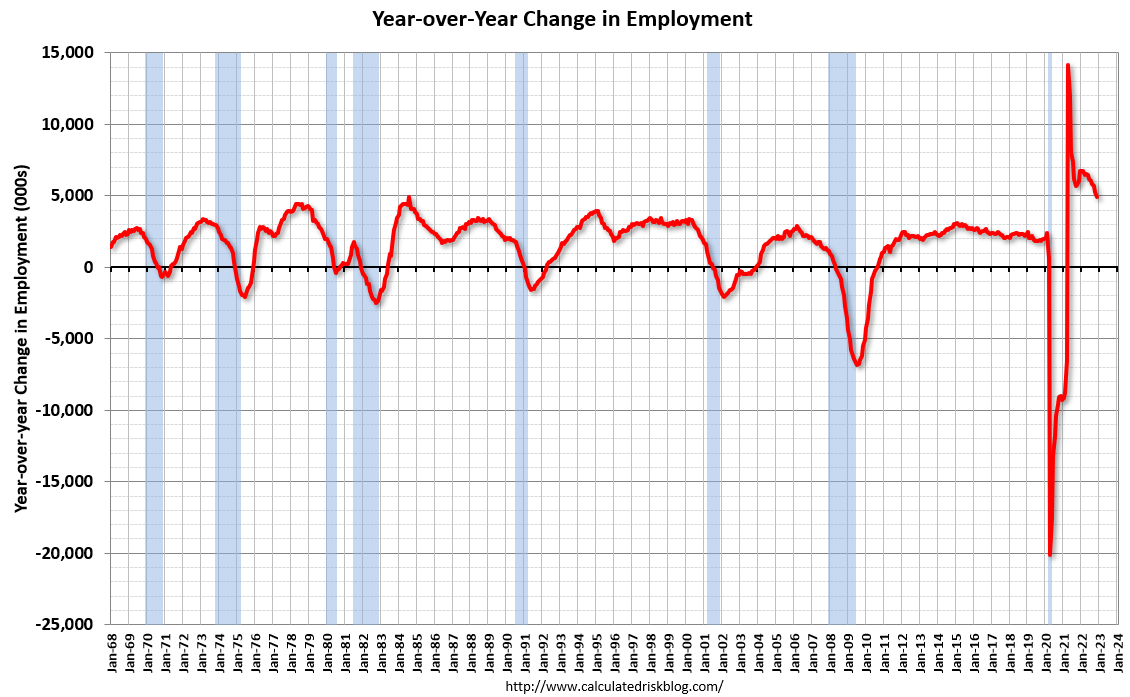

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.

In November, the year-over-year change was 4.90 million jobs. Employment was up significantly year-over-year.

Total payrolls increased by 263 thousand in November. Private payrolls increased by 221 thousand, and public payrolls increased 42 thousand.

Payrolls for September and October were revised down 23 thousand, combined.

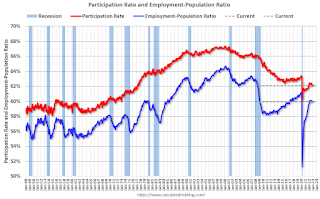

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.1% in November, from 62.2% in October. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.1% in November, from 62.2% in October. This is the percentage of the working age population in the labor force.

The Employment-Population ratio decreased to 59.9% from 60.0% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

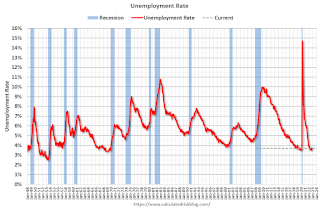

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate.

The unemployment rate was unchanged in November at 3.7% from 3.7% in October.

This was above consensus expectations; however, September and October payrolls were revised down by 23,000 combined.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In November, the year-over-year change was 4.90 million jobs. Employment was up significantly year-over-year.

Total payrolls increased by 263 thousand in November. Private payrolls increased by 221 thousand, and public payrolls increased 42 thousand.

Payrolls for September and October were revised down 23 thousand, combined.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.1% in November, from 62.2% in October. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.1% in November, from 62.2% in October. This is the percentage of the working age population in the labor force. The Employment-Population ratio decreased to 59.9% from 60.0% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was unchanged in November at 3.7% from 3.7% in October.

This was above consensus expectations; however, September and October payrolls were revised down by 23,000 combined.

I'll have more later ...

Thursday, December 01, 2022

Friday: Employment Report

by Calculated Risk on 12/01/2022 09:08:00 PM

Mortgage rates are down a full percentage point in just over 3 weeks.

Mortgage rates are down a full percentage point in just over 3 weeks.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

My November Employment Preview

Friday:

• At 8:30 AM ET, Employment Report for November. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.

Vehicles Sales Declined to 14.14 million SAAR in November

by Calculated Risk on 12/01/2022 07:24:00 PM

Wards Auto released their estimate of light vehicle sales for November. Wards Auto estimates sales of 14.14 million SAAR in November 2022 (Seasonally Adjusted Annual Rate), down 5.1% from the October sales rate, and up 7.9% from November 2021.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for November (red).

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic). However, sales decreased late last year due to supply issues. It appears the "supply chain bottom" was in September 2021.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967. November Employment Preview

by Calculated Risk on 12/01/2022 06:08:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for November. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.

Click on graph for larger image.

Click on graph for larger image.• First, as of October there are 804 thousand more jobs than in February 2020 (the month before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms. As of August 2022, the total number of jobs had returned.

This doesn't include the preliminary benchmark revision that showed there were 462 thousand more jobs than originally reported in March 2022.

• A few brief excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls rose by 175k in November (mom sa), below consensus of +200k and a slowdown from the +261k pace in October. ... We estimate the unemployment rate was unchanged at 3.7%• ADP Report: The ADP employment report showed 127,000 private sector jobs were added in November. This is the fourth release of ADP's new methodology, and this suggests job gains below consensus expectations.

emphasis added

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in November to 48.4%, down from 50.0% last month. This would suggest 30,000 jobs lost in manufacturing.

The ISM® services employment index for November has not been released yet.

• Unemployment Claims: The weekly claims report showed an increase in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 214,000 in October to 223,000 in November. This would usually suggest above the same number of layoffs in October as in September. In general, weekly claims were slightly higher than expectations in November.

• COVID: As far as the pandemic, the number of weekly cases during the reference week in November was around 282,000, up slightly from 265,000 in October.

• Conclusion: The consensus is for job growth to slow to 200,000 jobs added in November. The ADP report was below expectations, and weekly claims were slightly negative. My guess is the report will be below consensus.

Fannie Mae: Mortgage Serious Delinquency Rate Decreased in October

by Calculated Risk on 12/01/2022 03:09:00 PM

Fannie Mae reported that the Single-Family Serious Delinquency decreased to 0.67% in October from 0.69% in September. The serious delinquency rate is down from 1.46% in October 2021. This is close to pre-pandemic levels.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

Click on graph for larger image

Click on graph for larger image

By vintage, for loans made in 2004 or earlier (1% of portfolio), 2.34% are seriously delinquent (down from 2.41% in September).

For loans made in 2005 through 2008 (1% of portfolio), 3.71% are seriously delinquent (down from 3.83%),

For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (down from 0.55%). So, Fannie is still working through a handful of poor performing loans from the bubble years.

Mortgages in forbearance were counted as delinquent in this monthly report, but they were not reported to the credit bureaus.

Freddie Mac reported earlier.

Mortgages in forbearance were counted as delinquent in this monthly report, but they were not reported to the credit bureaus.

Freddie Mac reported earlier.

Rents Falling Faster than "Seasonality Alone"

by Calculated Risk on 12/01/2022 12:16:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Rents Falling Faster than "Seasonality Alone"

A brief excerpt:

Here is a graph of the year-over-year (YoY) change for these measures since January 2015. All of these measures are through October 2022 (Apartment List through November 2022).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note that new lease measures (Zillow, Apartment List) dipped early in the pandemic, whereas the BLS measures were steady. Then new leases took off, and the BLS measures are picking up.

...

The Zillow measure is up 9.6% YoY in October, down from 10.8% YoY in September. This is down from a peak of 17.1% YoY in February.

The ApartmentList measure is up 4.5% YoY as of November, down from 5.6% in October. This is down from the peak of 18.1% YoY last December.

Rents are still increasing YoY, and we should expect this to continue to spill over into measures of inflation. The Owners’ Equivalent Rent (OER) was up 6.9% YoY in October, from 6.7% YoY in September - and will likely increase further in the coming months even as rents slow sharply.

...

My suspicion is rent increases will slow further over the coming months as the pace of household formation slows, and more supply comes on the market. Housing economist Tom Lawler recently wrote: "An actual decline in rents next year would be a reasonable base case". This is important for monetary policy.