RSS Feed

RSS Feed by Calculated Risk on 2/03/2023 09:44:00 AM

Friday, February 03, 2023

Comments on January Employment Report

This was a strong report, and the revisions show job growth was stronger over the last year than originally reported. With revisions: The 4.81 million jobs added, 2022 was the 2nd best year for job growth in US history behind only 2021 with 7.27 million.

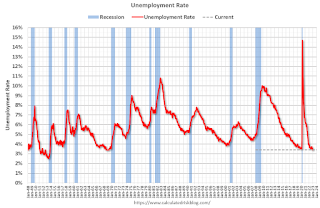

The headline jobs number in the January employment report was well above expectations, and employment for the previous two months was revised up by 71,000, combined. The participation rate increased, and the unemployment rate decreased to 3.4% - the lowest rate since May 1969 (over 50 years ago!)

Leisure and hospitality gained 128 thousand jobs in January. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.2 million jobs, and are now down 495 thousand jobs since February 2020. So, leisure and hospitality has now added back about 94% all of the jobs lost in March and April 2020.

Construction employment increased 25 thousand and is now 276 thousand above the pre-pandemic level.

Manufacturing added 19 thousand jobs and is now 214 thousand above the pre-pandemic level.

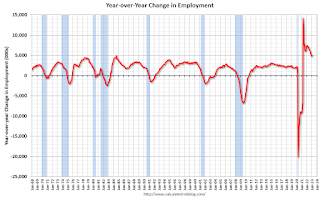

In January, the year-over-year employment change was 4.97 million jobs.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 participation rate increased in January to 82.7% from 82.4% in December, and the 25 to 54 employment population ratio increased to 80.2% from 80.1% the previous month.

Both are close to the pre-pandemic levels and indicate almost all of the prime age workers have returned to the labor force.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.4% YoY in January, down from 4.6% in December.

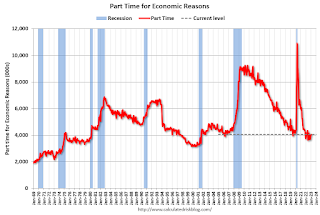

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 6.6% from 6.5% in the previous month. This is down from the record high in April 22.9% and last month was the lowest level on record (seasonally adjusted) (series started in 1994). This measure is below the level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more.

According to the BLS, there are 1.111 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.069 million the previous month.

This is at pre-pandemic levels.

Summary:

The headline monthly jobs number was well above expectations and employment for the previous two months was revised up by 71,000, combined. The annual benchmark revision indicated job growth was significantly stronger than originally reported.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.4% YoY in January, down from 4.6% in December.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons, at 4.1 million, was little changed in January. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons increased in January to 4.050 million from 3.878 million in December. This is at pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 6.6% from 6.5% in the previous month. This is down from the record high in April 22.9% and last month was the lowest level on record (seasonally adjusted) (series started in 1994). This measure is below the level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.111 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.069 million the previous month.

This is at pre-pandemic levels.

Summary:

The headline monthly jobs number was well above expectations and employment for the previous two months was revised up by 71,000, combined. The annual benchmark revision indicated job growth was significantly stronger than originally reported.

The headline unemployment rate decreased to 3.4%, the lowest rate since 1969.

Overall, this was a strong employment report.

January Employment Report: 517 thousand Jobs, 3.4% Unemployment Rate

by Calculated Risk on 2/03/2023 08:49:00 AM

From the BLS:

Total nonfarm payroll employment rose by 517,000 in January, and the unemployment rate changed little at 3.4 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, and health care. Employment also increased in government, partially reflecting the return of workers from a strike.

...

The change in total nonfarm payroll employment for November was revised up by 34,000, from +256,000 to +290,000, and the change for December was revised up by 37,000, from +223,000 to +260,000. With these revisions, employment gains in November and December combined were 71,000 higher than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms.

Total jobs are now 2.70 million above pre-pandemic levels. This is the last update for this graph this employment cycle.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.

In January, the year-over-year change was 4.97 million jobs. Employment was up significantly year-over-year.

Total payrolls increased by 517 thousand in January. Private payrolls increased by 443 thousand, and public payrolls increased 74 thousand.

Payrolls for November and December were revised up 71 thousand, combined.

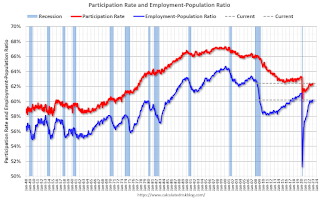

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.4% in January, from 62.3% in December. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.4% in January, from 62.3% in December. This is the percentage of the working age population in the labor force.

The Employment-Population ratio increased to 60.2% from 60.1% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

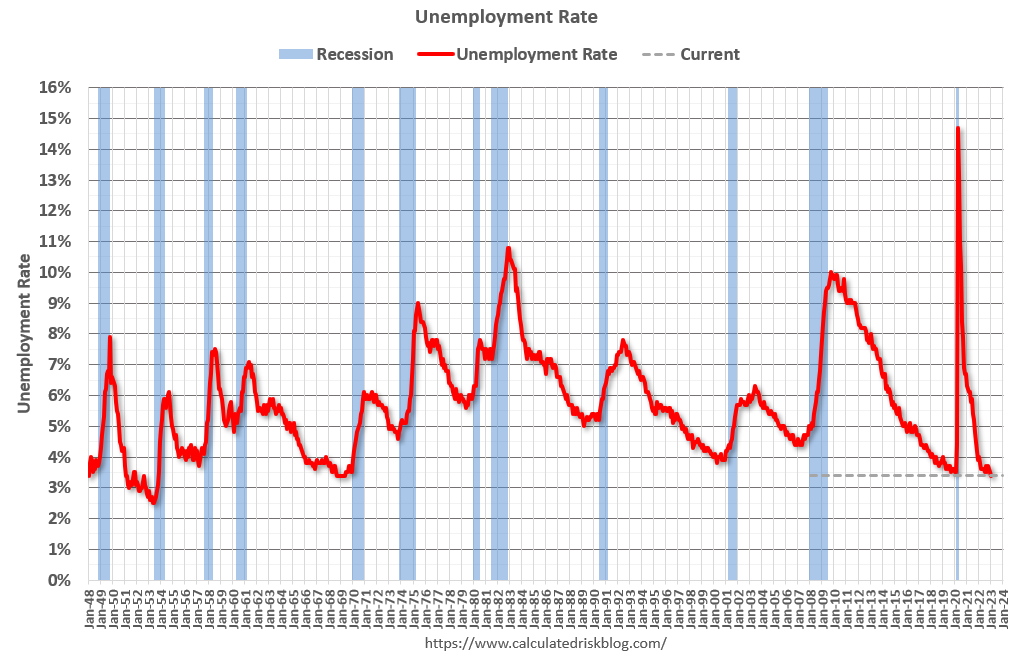

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate.

The unemployment rate decreased in January to 3.4% from 3.5% in December.

This was well above consensus expectations; and November and December payrolls were revised up by 71,000 combined.

On the annual benchmark revision:I'll have more later ...

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In January, the year-over-year change was 4.97 million jobs. Employment was up significantly year-over-year.

Total payrolls increased by 517 thousand in January. Private payrolls increased by 443 thousand, and public payrolls increased 74 thousand.

Payrolls for November and December were revised up 71 thousand, combined.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.4% in January, from 62.3% in December. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.4% in January, from 62.3% in December. This is the percentage of the working age population in the labor force. The Employment-Population ratio increased to 60.2% from 60.1% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate decreased in January to 3.4% from 3.5% in December.

This was well above consensus expectations; and November and December payrolls were revised up by 71,000 combined.

The total nonfarm employment level for March 2022 was revised upward by 568,000 (+506,000 on a not seasonally adjusted basis, or +0.3 percent). The average not seasonally adjusted benchmark revision (in absolute terms) over the past 10 years is 0.1 percent.

Thursday, February 02, 2023

Friday: Employment Report

by Calculated Risk on 2/02/2023 08:56:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 8:30 AM ET, Employment Report for December. The consensus is for 185,000 jobs added, and for the unemployment rate to increase to 3.6%.

• At 10:00 AM, ISM Services Index for January.

January Employment Preview

by Calculated Risk on 2/02/2023 12:41:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for January. The consensus is for 185,000 jobs added, and for the unemployment rate to increase to 3.6%.

From BofA economists:

"Nonfarm payrolls likely rose by 225k in January, little changed from the December increase. Payrolls were likely boosted by the end of the strike by University of California workers in late December. The strike affected 36k workers according to the BLS and likely largely explained the ~24k drop in state education employment in December. These workers should return to payrolls in January."From Goldman Sachs:

"We continue to expect a strong employment report, and we left our nonfarm payroll forecast unchanged at +300k (mom sa)."

Click on graph for larger image.

Click on graph for larger image.• First, as of December there were 1.24 million more jobs than in February 2020 (the month before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms. As of August 2022, the total number of jobs had returned.

• Annual Benchmark Revision: The benchmark revision for 2021 will be released with the January employment report. The above graph doesn't include the preliminary benchmark revision that showed there were 462 thousand more jobs than originally reported in March 2022.

• ADP Report: The ADP employment report showed 106,000 private sector jobs were added in January. This suggests job gains below consensus expectations. ADP chief economist Nela Richardson noted: "In January, we saw the impact of weather-related disruptions on employment during our reference week. Hiring was stronger during other weeks of the month, in line with the strength we saw late last year."

• ISM Surveys: Note that the ISM indexes are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in January to 50.6%, down from 50.8% last month. This would suggest the number of manufacturing jobs was mostly unchanged in January.

The ISM® services employment index for January has not been released yet.

• Unemployment Claims: The weekly claims report showed a decrease in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 216,000 in December to 192,000 in January. This would usually suggest fewer layoffs in January than in December. In general, weekly claims were below expectations in January.

• COVID: As far as the pandemic, the number of weekly cases during the reference week in January was around 332,000, down from 458,000 in December.

• Weather: As ADP noted, there was severe weather during the reference week. After the release, I'll check the San Francisco Fed estimate of Weather-Adjusted Change in Total Nonfarm Employment.

• Conclusion: This employment report is especially hard to predict. There is a significant seasonal adjustment for January (there are always a large number of jobs lost in January NSA). And there are other factors - severe weather, end of a strike - that will likely impact hiring. My guess is the report will be below consensus.

Inflation Adjusted House Prices 3.6% Below Peak

by Calculated Risk on 2/02/2023 09:45:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 3.8% Below Peak; Price-to-rent index is 6.1% below recent peak

Excerpt:

It has been 17 years since the bubble peak. In the November Case-Shiller house price index released on Tuesday, the seasonally adjusted National Index (SA), was reported as being 61% above the bubble peak in 2006. However, in real terms, the National index (SA) is about 12% above the bubble peak (and historically there has been an upward slope to real house prices). The composite 20, in real terms, is about 2% above the bubble peak.

Both indexes have declined for six consecutive months in real terms (inflation adjusted).

People usually graph nominal house prices, but it is also important to look at prices in real terms. As an example, if a house price was $200,000 in January 2000, the price would be almost $339,000 today adjusted for inflation (69.5% increase). That is why the second graph below is important - this shows "real" prices. ...

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

Note that OER is lagging behind other measures of rent.

Here is a similar graph using the Case-Shiller National and Composite 20 House Price Indexes. This graph shows the price to rent ratio (January 2000 = 1.0). The price-to-rent ratio had been moving more sideways but picked up significantly following the onset of the pandemic.

On a price-to-rent basis, the Case-Shiller National and Composite 20 indexes declined again in November for the sixth consecutive month. The price-to-rent index for the National index is off 6.1% from the recent peak, and the Composite 20 based index is off 7.7%.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Weekly Initial Unemployment Claims decrease to 183,000

by Calculated Risk on 2/02/2023 08:33:00 AM

The DOL reported:

In the week ending January 28, the advance figure for seasonally adjusted initial claims was 183,000, a decrease of 3,000 from the previous week's unrevised level of 186,000. The 4-week moving average was 191,750, a decrease of 5,750 from the previous week's unrevised average of 197,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 191,750.

The previous week was unrevised.

Weekly claims were below the consensus forecast.

Wednesday, February 01, 2023

Vehicles Sales Increased to 15.74 million SAAR in January

by Calculated Risk on 2/01/2023 09:41:00 PM

Wards Auto released their estimate of light vehicle sales for January: U.S. Light-Vehicle Sales Record Fifth Consecutive Increase in January (pay site).

Wards Auto estimates sales of 15.74 million SAAR in January 2023 (Seasonally Adjusted Annual Rate), up 17.6% from the December sales rate, and up 4.2% from January 2022.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for January (red).

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic). However, sales decreased late last year due to supply issues. It appears the "supply chain bottom" was in September 2021.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967. BLS: Job Openings Increased to 11.0 million in December

by Calculated Risk on 2/01/2023 04:00:00 PM

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings increased to 11.0 million on the last business day of December, the U.S. Bureau of Labor Statistics reported today. Over the month, the number of hires and total separations changed little at 6.2 million and 5.9 million, respectively. Within separations, quits (4.1 million) and layoffs and discharges (1.5 million) changed little.The following graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for December the employment report this Friday will be for January.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are usually pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data.

Jobs openings increased in December to 11.012 million from 10.440 million in November.

The number of job openings (black) were down 4% year-over-year.

Quits were down 7% year-over-year. These are voluntary separations. (See light blue columns at bottom of graph for trend for "quits").

FOMC Statement: Raise Rates 25 bp; "Ongoing increases appropriate"

by Calculated Risk on 2/01/2023 02:01:00 PM

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

FOMC Statement:

Recent indicators point to modest growth in spending and production. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation has eased somewhat but remains elevated.

Russia's war against Ukraine is causing tremendous human and economic hardship and is contributing to elevated global uncertainty. The Committee is highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-1/2 to 4-3/4 percent. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lael Brainard; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

emphasis added

Rents Continue to Decline; "Apartment Market Loosens"

by Calculated Risk on 2/01/2023 11:39:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Rents Continue to Decline; "Apartment Market Loosens"

A brief excerpt:

The rental market has changed rapidly. This index from the National Multifamily Housing Council (NMHC) has been an excellent leading indicator for rents and vacancy rates, and this suggests higher vacancy rates and falling asking rents in the coming months.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

From the NMHC: Rents Continue to Fall as Apartment Market Loosens, Transactions Pull Back Due to Higher Interest Rates

• The Market Tightness Index came in at 14 this quarter—well below the breakeven level (50)—indicating looser market conditions for the second consecutive quarter. Over three-quarters of respondents (78%) reported markets to be looser than three months ago, while only 5% thought markets have become tighter. Another 16% of respondents thought that market conditions were unchanged over the past three months.