RSS Feed

RSS Feed by Calculated Risk on 2/26/2023 11:24:00 AM

Sunday, February 26, 2023

High Frequency Indicators: Airlines Back to Pre-Pandemic Levels, Movie Tickets Still Down

I stopped the weekly updates of high frequency indicators at the end of 2022. Here is a look at two indicators that were still below pre-recession levels as of last December.

The TSA is providing daily travel numbers.

This data is as of February 24th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue), 2022 (Orange) and 2023 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is at the same level as the same week in 2019 (99.7% of 2019). (Dashed line)

Air travel - as a percent of 2019 - is back to pre-pandemic levels.

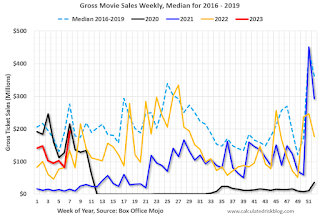

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021, Orange is 2022 and Red is 2023.

The data is from BoxOfficeMojo through February 23rd.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales are running about 30% below the pre-pandemic levels.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales are running about 30% below the pre-pandemic levels.

Saturday, February 25, 2023

Real Estate Newsletter Articles this Week: "New Home Average Prices Down 5.3% Year-over-year"

by Calculated Risk on 2/25/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• New Home Sales Increase to 670,000 Annual Rate in January New Home Average Prices Down 5.3% Year-over-year

• NAR: Existing-Home Sales Decreased to 4.00 million SAAR in January

• Final Look at Local Housing Markets in January

• First time ever more "Built-for-Rent" Units started Quarterly than "Built-for-Sale"

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of February 26, 2023

by Calculated Risk on 2/25/2023 08:11:00 AM

The key reports this week are Case-Shiller house prices and February vehicle sales.

For manufacturing, the January ISM Index, and the February Dallas and Richmond Fed manufacturing surveys will be released.

8:30 AM: Durable Goods Orders for January from the Census Bureau. The consensus is for a 4.0% decrease in durable goods orders.

10:00 AM: Pending Home Sales Index for January. The consensus is for a 1.0% increase in the index.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for February.

9:00 AM: FHFA House Price Index for December 2022. This was originally a GSE only repeat sales, however there is also an expanded index.

9:00 AM: S&P/Case-Shiller House Price Index for December.

9:00 AM: S&P/Case-Shiller House Price Index for December.This graph shows the year-over-year change for the Case-Shiller National, Composite 10 and Composite 20 indexes, through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 6.0% year-over-year increase in the Comp 20 index for December, down from 6.8% in November.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for February.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

10:00 AM: ISM Manufacturing Index for January. The consensus is for the ISM to be at 48.0, up from 47.4 in January.

10:00 AM: Construction Spending for December. The consensus is for a 0.2% increase in construction spending.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 197 thousand initial claims, up from 192 thousand last week.

All day: Light vehicle sales for February. The consensus is for light vehicle sales to be 15.0 million SAAR in February, down from 15.7 million in January (Seasonally Adjusted Annual Rate).

All day: Light vehicle sales for February. The consensus is for light vehicle sales to be 15.0 million SAAR in February, down from 15.7 million in January (Seasonally Adjusted Annual Rate).This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the January sales rate.

10:00 AM: the ISM Services Index for February.

Friday, February 24, 2023

COVID Feb 24, 2023: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 2/24/2023 09:27:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

On COVID (focus on hospitalizations and deaths). Data is now weekly.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 235,131 | 259,947 | ≤35,0001 | |

| Hospitalized2 | 21,731 | 23,050 | ≤3,0001 | |

| Deaths per Week2 | 2,407 | 2,838 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

The pandemic low for weekly deaths was the week of July 7, 2021, at 1,690 deaths.

Black Knight: Mortgage Delinquencies Decreased in January

by Calculated Risk on 2/24/2023 04:24:00 PM

• January performance data showed a slight decrease (-10 basis points) in the national delinquency rate month-over-month, which is now down 15.1% year over yearAccording to Black Knight's First Look report, the percent of loans delinquent decreased 2.3% in January compared to December and decreased 15% year-over-year.

• Foreclosure starts saw a fourth straight increase, but remain 37% below pre-pandemic levels; active foreclosures are up 20% since January 2022, but they too remain nearly 20% below pre-pandemic levels

• As purchase and refinance lending continue to face interest rate headwinds, prepayment activity hit yet another record low in January, dating back to at least 2000 when Black Knight began reporting the metric

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 3.38% in January, down from 3.48% in December.

The percent of loans in the foreclosure process increased slightly in December to 0.45%, from 0.44% in December.

The number of delinquent properties, but not in foreclosure, is down 289,000 properties year-over-year, and the number of properties in the foreclosure process is up 48,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| Jan 2023 | Dec 2022 | Jan 2022 | Jan 2021 | |

| Delinquent | 3.38% | 3.48% | 3.98% | 7.08% |

| In Foreclosure | 0.45% | 0.44% | 0.37% | 0.41% |

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,775,000 | 1,827,000 | 2,063,000 | 3,701,000 |

| Number of properties in foreclosure pre-sale inventory: | 238,000 | 232,000 | 190,000 | 212,000 |

| Total Properties | 2,012,000 | 2,058,000 | 2,254,000 | 3,913,000 |

Q1 GDP Tracking: Close to 2%

by Calculated Risk on 2/24/2023 12:59:00 PM

From BofA:

Our GDP tracking estimate fell by two-tenths to 1.3% q/q saar since our last update [Feb 23rd estimate] (estimate before personal spending and New Home sales reports).From Goldman:

emphasis added

Following stronger-than-expected personal spending and new home sales in January, we boosted our Q1 GDP tracking estimate by 0.4pp to +1.8% (qoq ar) and our domestic final sales forecast by the same amount to +2.3%. [Feb 24th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2023 is 2.7 percent on February 24, up from 2.5 percent on February 16. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, the US Bureau of Labor Statistics, and the National Association of Realtors, the nowcasts of first-quarter real personal consumption expenditures growth and first-quarter real gross private domestic investment growth increased from 3.6 percent and -6.0 percent, respectively, to 3.8 percent and -5.3 percent. [Feb 24th estimate]

New Home Sales Increase to 670,000 Annual Rate in January; New Home Average Prices Down 5.3% Year-over-year

by Calculated Risk on 2/24/2023 10:50:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales Increase to 670,000 Annual Rate in January

Brief excerpt:

And on prices, from the Census Bureau:You can subscribe at https://calculatedrisk.substack.com/.The median sales price of new houses sold in January 2023 was $427,500. The average sales price was $474,400.The following graph shows the median and average new home prices. The average price in January 2023 was $474,400 down 5.3% year-over-year. The median price was $427,500 down 0.7% year-over-year. This suggests a year-over-year decrease in prices, although both the median and the average are impacted by the mix of homes sold.

...

This was for contracts signed in January when mortgage rates were lower - and builders were buying down rates. Mortgage rates increased again in February, and that will likely impact sales.

As previously discussed, the Census Bureau overestimates sales, and underestimates inventory when cancellation rates are rising, see: New Home Sales and Cancellations: Net vs Gross Sales. So, take the headline sales number with a large grain of salt - the actual negative impact on the homebuilders is greater than the headline number suggests (until cancellations start declining)!

This will reverse when cancellation rates start declining. When a previously cancelled home is resold, the home builder counts it as a sale, but the Census Bureau does not (since it was already counted).

There are a large number of homes under construction, and this suggests we will see a further sharp increase in completed inventory over the next several months - and that will keep pressure on new home prices.

New Home Sales at 670,000 Annual Rate in January

by Calculated Risk on 2/24/2023 10:07:00 AM

The Census Bureau reports New Home Sales in January were at a seasonally adjusted annual rate (SAAR) of 670 thousand.

The previous three months were revised down, combined.

Sales of new single‐family houses in January 2023 were at a seasonally adjusted annual rate of 670,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.2 percent above the revised December rate of 625,000, but is 19.4 percent below the January 2022 estimate of 831,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are close to pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply decreased in January to 7.9 months from 8.7 months in December.

The months of supply decreased in January to 7.9 months from 8.7 months in December. The all-time record high was 12.1 months of supply in January 2009. The all-time record low was 3.5 months, most recently in October 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of January was 439,000. This represents a supply of 7.9 months at the current sales rate."Sales were well above expectations of 620 thousand SAAR, however sales in the three previous months were revised down, combined. I'll have more later today.

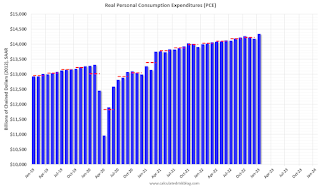

Personal Income increased 0.6% in January; Spending increased 1.8%

by Calculated Risk on 2/24/2023 08:40:00 AM

The BEA released the Personal Income and Outlays report for January:

Personal income increased $131.1 billion (0.6 percent) in January, according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $387.4 billion (2.0 percent) and personal consumption expenditures (PCE) increased $312.5 billion (1.8 percent).The January PCE price index increased 5.4 percent year-over-year (YoY), up from 5.3 percent YoY in December, and down from the recent peak of 7.0 percent in June 2022.

The PCE price index increased 0.6 percent in January. Excluding food and energy, the PCE price index also increased 0.6 percent. Real DPI increased 1.4 percent and Real PCE increased 1.1 percent; goods increased 2.2 percent and services increased 0.6 percent.

emphasis added

The PCE price index, excluding food and energy, increased 4.7 percent YoY, up from 4.6 percent in December, and down from the recent peak of 5.4 percent in February 2022.

The following graph shows real Personal Consumption Expenditures (PCE) through January 2023 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

Personal income was below expectations, and the increase in PCE was above expectations.

The following graph shows real Personal Consumption Expenditures (PCE) through January 2023 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income was below expectations, and the increase in PCE was above expectations.

Inflation was above expectations.

Thursday, February 23, 2023

Friday: Personal Income & Outlays, New Home Sales

by Calculated Risk on 2/23/2023 08:47:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 8:30 AM ET, Personal Income and Outlays for January. The consensus is for a 0.9% increase in personal income, and for a 1.3% increase in personal spending. And for the Core PCE price index to increase 0.4%. PCE prices are expected to be up 4.9% YoY, and core PCE prices up 4.3% YoY.

• At 10:00 AM, New Home Sales for January from the Census Bureau. The consensus is that new home sales increased to 620 thousand SAAR, down from 616 thousand in December.

• Also at 10:00 AM, University of Michigan's Consumer sentiment index (Final for February). The consensus is for a reading of 66.4.