RSS Feed

RSS Feed by Calculated Risk on 4/23/2023 06:43:00 PM

Sunday, April 23, 2023

Sunday Night Futures

Weekend:

• Schedule for Week of April 23, 2023

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for March. This is a composite index of other data.

• At 10:30 AM, Dallas Fed Survey of Manufacturing Activity for April.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 6 and DOW futures are down 44 (fair value).

Oil prices were down over the last week with WTI futures at $77.87 per barrel and Brent at $81.66 per barrel. A year ago, WTI was at $103, and Brent was at $105 - so WTI oil prices are down about 24% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.64 per gallon. A year ago, prices were at $4.09 per gallon, so gasoline prices are down $0.45 per gallon year-over-year.

The Normal Seasonal Pattern for Median House Prices

by Calculated Risk on 4/23/2023 10:37:00 AM

Last week, in the CalculatedRisk Real Estate Newsletter on March existing home sales, NAR: Existing-Home Sales Decreased to 4.44 million SAAR in March; Median Prices Declined 0.9% YoY, I noted that median prices were down year-over-year (median prices are distorted by the mix).

Seasonally prices typically peak in June (closed sales are mostly for contracts signed in April and May).

And seasonally prices usually bottom the following January (contracts signed in November and December).

The recent surge in prices started mid-year 2020 and ran through Q1 2022 when mortgage rates started increasing significantly.

The 2023 increase in median prices from January to March was about the same as in 2018 and 2019.

Here is a table of the seasonal percentage increases from January to March, and from March to June (the usual seasonal peak) over the last several years. The third row is the total percentage increase from January to June.

The last row shows the seasonal decline from June to December. Note: In 2019, prices only declined 3.8% in the 2nd half of the year as mortgage rates declined into the mid-3s (pre-pandemic low was 3.5% on a 30-year mortgage according to Freddie MAC PMMS).

In 2020, prices continued to increase in the 2nd half of the year and didn't peak seasonally until October. And prices only declined slightly in the 2nd half of 2021.

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|

| Jan to Mar | 3.7% | 4.1% | 5.4% | 7.5% | 7.1% | 4.0% |

| Mar to Jun | 9.6% | 9.9% | 4.9% | 12.4% | 9.1% | NA |

| Total Jan to Jun | 13.7% | 14.4% | 10.6% | 20.8% | 16.8% | NA |

| Jun to Dec | -7.0% | -3.8% | 5.0% | -2.2% | -11.4% | NA |

The 2023 increase in median prices from January to March was about the same as in 2018 and 2019.

Normally we'd expect median prices to increase 9% to 10% over the next three months, before declining in the 2nd half of the year. The seasonal pattern will be interesting this year.

Saturday, April 22, 2023

Real Estate Newsletter Articles this Week: "Most Multi-family Under Construction Since 1973"

by Calculated Risk on 4/22/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• NAR: Existing-Home Sales Decreased to 4.44 million SAAR in March; Median Prices Declined 0.9% YoY

• March Housing Starts: Most Multi-family Under Construction Since 1973

• Lawler on Demographics: New Population Estimates Incorporate Unprecedented Methodological Changes

• Why Measures of Existing Home Inventory appear Different

• 4th Look at Local Housing Markets: California Home Sales down 34% YoY in March; Prices Down 7.0% YoY

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of April 23, 2023

by Calculated Risk on 4/22/2023 08:11:00 AM

The key reports scheduled for this week are the advance estimate of Q1 GDP and March New Home sales.

Other key reports include February Case-Shiller house prices and Personal Income and Outlays for March.

For manufacturing, the April Dallas, Richmond and Kansas City manufacturing surveys will be released.

8:30 AM ET: Chicago Fed National Activity Index for March. This is a composite index of other data.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for April.

9:00 AM: S&P/Case-Shiller House Price Index for February.

9:00 AM: S&P/Case-Shiller House Price Index for February.This graph shows the nominal seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 2.5% year-over-year increase in the Comp 20 index for February.

9:00 AM: FHFA House Price Index for February. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: New Home Sales for March from the Census Bureau.

10:00 AM: New Home Sales for March from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 630 thousand SAAR, down from 640 thousand in February.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for April.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for March from the Census Bureau. The consensus is for a 0.9% increase in durable goods orders.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 250 thousand initial claims, up from 245 thousand last week.

8:30 AM: Gross Domestic Product, 1st quarter 2023 (Advance estimate). The consensus is that real GDP increased 2.0% annualized in Q1, down from 2.6% in Q4.

10:00 AM: Pending Home Sales Index for March. The consensus is for a 1.0% increase in the index.

11:00 AM: the Kansas City Fed manufacturing survey for April. This is the last of regional manufacturing surveys for April.

8:30 AM ET: Personal Income and Outlays, March 2023. The consensus is for a 0.2% increase in personal income, and for a 0.1% decrease in personal spending. And for the Core PCE price index to increase 0.3%. PCE prices are expected to be up 4.1% YoY, and core PCE prices up 4.5% YoY.

9:45 AM: Chicago Purchasing Managers Index for April. The consensus is for a reading of 43.5, down from 43.8 in March.

10:00 AM: University of Michigan's Consumer sentiment index (Final for April). The consensus is for a reading of 63.5.

Friday, April 21, 2023

COVID Apr 21, 2023: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 4/21/2023 09:00:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

On COVID (focus on hospitalizations and deaths). Data is now weekly.

After the first few weeks, the pandemic low for weekly deaths had been the week of July 7, 2021, at 1,690 deaths (until recently).

For cases, the low was 82,186 (getting close).

For COVID hospitalizations, the low was 9,821 (also getting close).

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 94,142 | 101,598 | ≤35,0001 | |

| Hospitalized2 | 11,097 | 12,418 | ≤3,0001 | |

| Deaths per Week2 | 1,160 | 1,333 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths decreased this week and set a new pandemic low of 1,160 deaths in the most recent week.

Q1 GDP Tracking: Around 2%

by Calculated Risk on 4/21/2023 01:31:00 PM

The advance estimate of Q1 GDP will be released this coming Thursday, April 27th. The consensus is that real GDP increased 2.0% annualized in Q1, down from 2.6% in Q4.

From BofA:

On net, the data lowered our tracking estimate a tenth to 1.5% q/q saar. ... Our tracking estimate for personal consumption expenditures (PCE) increased from 3.5% q/q saar to 4.0% q/q saar owing to slightly stronger than expected retail sales and a surge in utitilities production. [Apr 21st estimate]From Goldman:

emphasis added

We have left our Q1 GDP tracking estimate unchanged at +2.2% (qoq ar). Our domestic final sales growth forecast stands at +3.9%. [Apr 20th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2023 is 2.5 percent on April 18, unchanged from April 14 after rounding. After this morning's housing starts report from the US Census Bureau, the nowcast of first-quarter real residential investment growth increased from -5.8 percent to -5.5 percent. [Apr 18th estimate]

Why Measures of Existing Home Inventory appear Different

by Calculated Risk on 4/21/2023 09:57:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Why Measures of Existing Home Inventory appear Different

A brief excerpt:

Here is a graph comparing the year-over-year change in Realtor.com’s active inventory, the NAR’s inventory, and Realtor.com inventory including pending sales. Note that the blue line (NAR) and dashed black line (Realtor including pending sales) track.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

As Lawler noted, including pending sales understated the decline in active inventory in 2020 and 2021, and is now understating the increase in active inventory.

But what about Redfin? Redfin takes a very different approach. Their active inventory number for any month includes homes that came on the market and sold quickly during the month, whereas the other measures are a snapshot at the end of the month (or week).

Black Knight: "Mortgage Delinquencies Hit Record Low in March"

by Calculated Risk on 4/21/2023 08:30:00 AM

From Black Knight: Black Knight’s First Look: Mortgage Delinquencies Hit Record Low in March, While Prepayments Rose on Easing Rates and Seasonal Tailwinds

• The national delinquency rate dropped 53 basis points (-15%) in March, falling below 3% for the first time on record, ending the month at just 2.92%According to Black Knight's First Look report, the percent of loans delinquent decreased 15% in March compared to February and decreased 13% year-over-year.

• While delinquency rates almost always fall in March – as borrowers utilize tax refunds and other seasonal revenues to pay down past-due debt – the drop marked the second largest decline in the past 17 years

• Factoring in March’s decline, the total number of past-due mortgages (including active foreclosures) has fallen to its lowest level in nearly 23 years, dating all the way back to April 2000

• Serious delinquencies (90+ days past due) showed marked improvement, falling by 51K to their lowest level since March 2020, with volumes shrinking in every state

• Likewise, every state saw overall delinquencies fall in March, with improvements ranging from 11.9% in Washington to 21.5% in Vermont

• Both foreclosure starts (+9.0%) and sales (+4.6%) rose in the month but still remain well below pre-pandemic volumes at the national level

• Active foreclosure inventory held steady, but remains 31K (12%) below March 2020 levels

• The prepayment rate (SMM) rose to 0.50% (+44% month over month) driven, as anticipated, by seasonal tailwinds in sale-related prepayments and an increased demand for refis due to falling rates

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 2.92% in March, down from 3.45% the previous month.

The percent of loans in the foreclosure process was essentially unchanged in March at 0.46%, from 0.46% the previous month.

The number of delinquent properties, but not in foreclosure, is down 209,000 properties year-over-year, and the number of properties in the foreclosure process is up 31,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| Mar 2023 | Feb 2023 | |||

| Delinquent | 2.92% | 3.45% | ||

| In Foreclosure | 0.46% | 0.46% | ||

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,539,000 | 1,811,000 | ||

| Number of properties in foreclosure pre-sale inventory: | 240,000 | 240,000 | ||

| Total Properties | 1,779,000 | 2,050,000 | ||

Thursday, April 20, 2023

Hotels: Occupancy Rate Up 3.7% Year-over-year

by Calculated Risk on 4/20/2023 03:39:00 PM

U.S. hotel performance increased from the previous week, according to STR‘s latest data through April 15.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

April 9-15, 2023 (percentage change from comparable week in 2022):

• Occupancy: 64.2% (+3.7%)

• Average daily rate (ADR): $155.33 (+4.7%)

• Revenue per available room (RevPAR): $99.67 (+8.6%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2023, black is 2020, blue is the median, and dashed light blue is for 2022. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is close to the median rate for the period 2000 through 2020 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will move more sideways until the summer travel season.

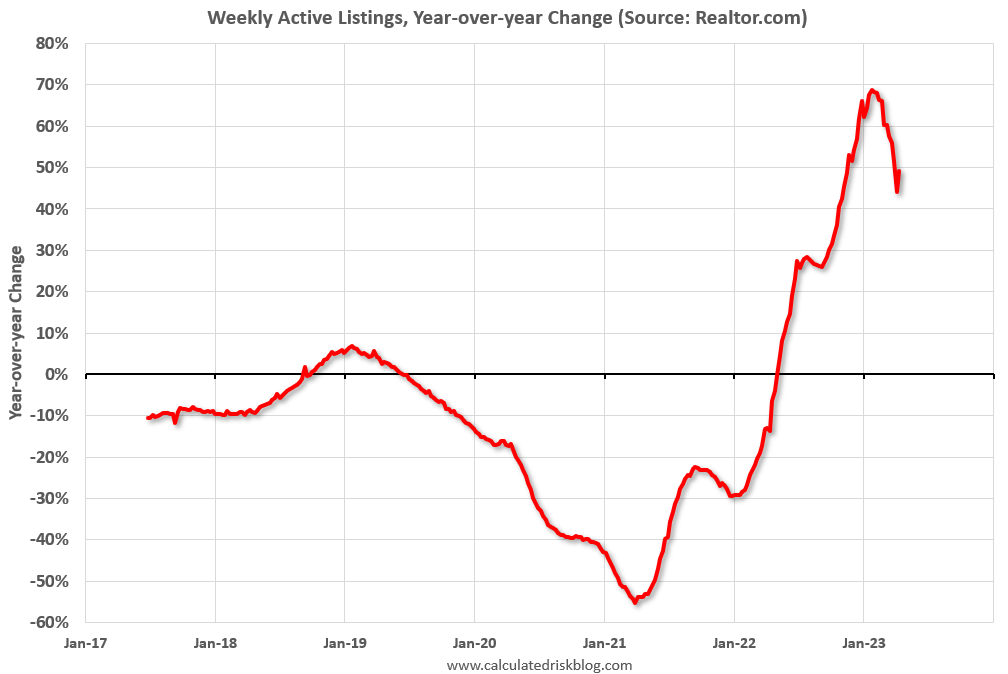

Realtor.com Reports Weekly Active Inventory Up 49% YoY; New Listings Down 5% YoY

by Calculated Risk on 4/20/2023 01:32:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from chief economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Apr 15, 2023

• Active inventory growth continued to climb, with for-sale homes up 49% above one year ago. The number of homeowners shifting home listing timelines around spring holidays helped push active inventory growth up this week. Despite the big surge, the number of homes for-sale continues to trail pre-pandemic levels, keeping many cards in the hands of sellers sitting on very high levels of home equity.

...

• New listings–a measure of sellers putting homes up for sale–were down again this week, but only by 5% from one year ago. The number of newly listed homes has been lower than the same time the previous year for the past 41 weeks and while this week continued that trend, the magnitude shifted in a big way. Shifts in religious holidays that fell earlier in 2023 are likely responsible for last week’s big drop and this week’s significantly smaller decline. On average across the two weeks, the decline in new listings is roughly on track with what we’ve seen so far this year.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory is still up year-over-year - from record lows - however, the YoY increase has slowed recently, although this was a pickup from up 44% YoY last week.