RSS Feed

RSS Feed by Calculated Risk on 6/25/2023 08:12:00 AM

Sunday, June 25, 2023

A Very Early Look at 2024 Cost-Of-Living Adjustments and Maximum Contribution Base

The BLS reported on June 13th:

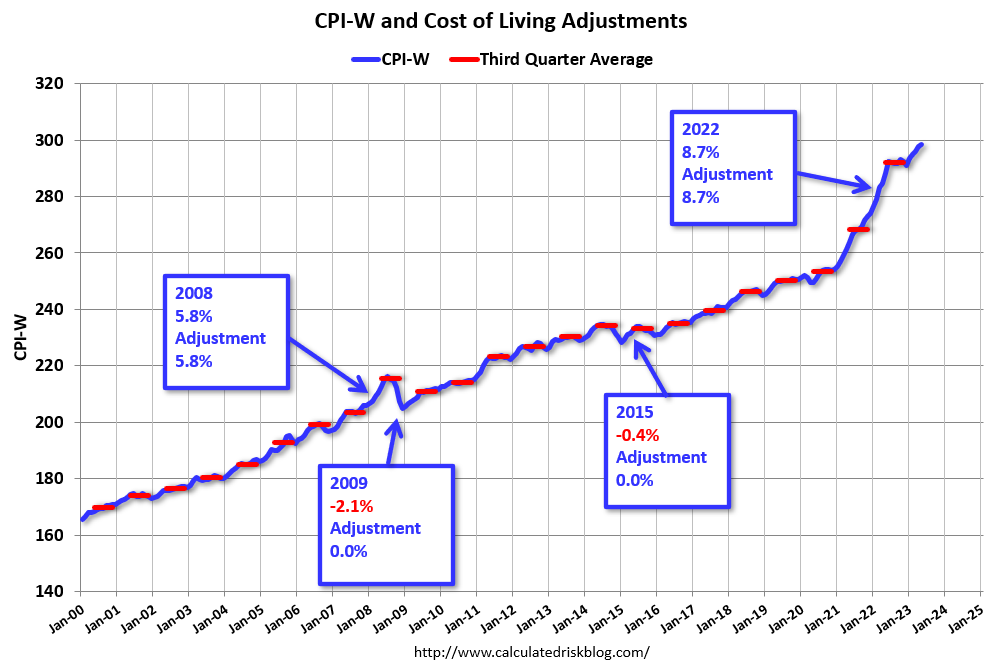

The Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) increased 3.6 percent over the last 12 months to an index level of 298.382 (1982-84=100). For the month, the index increased 0.2 percent prior to seasonal adjustment.CPI-W is the index that is used to calculate the Cost-Of-Living Adjustments (COLA). The calculation dates have changed over time (see Cost-of-Living Adjustments), but the current calculation uses the average CPI-W for the three months in Q3 (July, August, September) and compares to the average for the highest previous average of Q3 months. Note: this is not the headline CPI-U and is not seasonally adjusted (NSA).

• In 2022, the Q3 average of CPI-W was 291.901.

The 2022 Q3 average was the highest Q3 average, so we only have to compare Q3 this year to last year.

Click on graph for larger image.

Click on graph for larger image.This graph shows CPI-W since January 2000. The red lines are the Q3 average of CPI-W for each year.

Note: The year labeled is for the calculation, and the adjustment is effective for December of that year (received by beneficiaries in January of the following year).

CPI-W was up 3.6% year-over-year in May, and although this is very early - we need the data for July, August and September - my very early guess is COLA will probably be close to 3% this year, the smallest increase since 1.3% in 2021.

Contribution and Benefit Base

The contribution base will be adjusted using the National Average Wage Index. This is based on a one-year lag. The National Average Wage Index is not available for 2022 yet, wages increased solidly in 2022. If wages increased 5% in 2022, then the contribution base next year will increase to around $168,200 in 2024, from the current $160,200.

Remember - this is a very early look. What matters is average CPI-W, NSA, for all three months in Q3 (July, August and September).

Saturday, June 24, 2023

Real Estate Newsletter Articles this Week: Record Number of Multi-Family Housing Units Under Construction

by Calculated Risk on 6/24/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• NAR: Existing-Home Sales Increased to 4.30 million SAAR in May; Median Prices Declined 3.1% YoY in May

• May Housing Starts: Record Number of Multi-Family Housing Units Under Construction

• Some More Good News for Homebuilders

• Final Look at Local Housing Markets in May

• California Home Sales Down 23.6% YoY in May, Median Prices Decline 6.4% YoY

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of June 25, 2023

by Calculated Risk on 6/24/2023 08:11:00 AM

The key reports this week are May New Home sales, the third estimate of Q1 GDP, Personal Income and Outlays for May and April Case-Shiller house prices.

For manufacturing, the June Richmond and Dallas Fed manufacturing surveys will be released.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for June.

8:30 AM: Durable Goods Orders for May from the Census Bureau. The consensus is for a 1.3% decrease in durable goods orders.

9:00 AM: S&P/Case-Shiller House Price Index for April.

9:00 AM: S&P/Case-Shiller House Price Index for April.This graph shows the year-over-year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 1.1% year-over-year decrease in the Comp 20 index for April.

9:00 AM: FHFA House Price Index for April. This was originally a GSE only repeat sales, however there is also an expanded index.

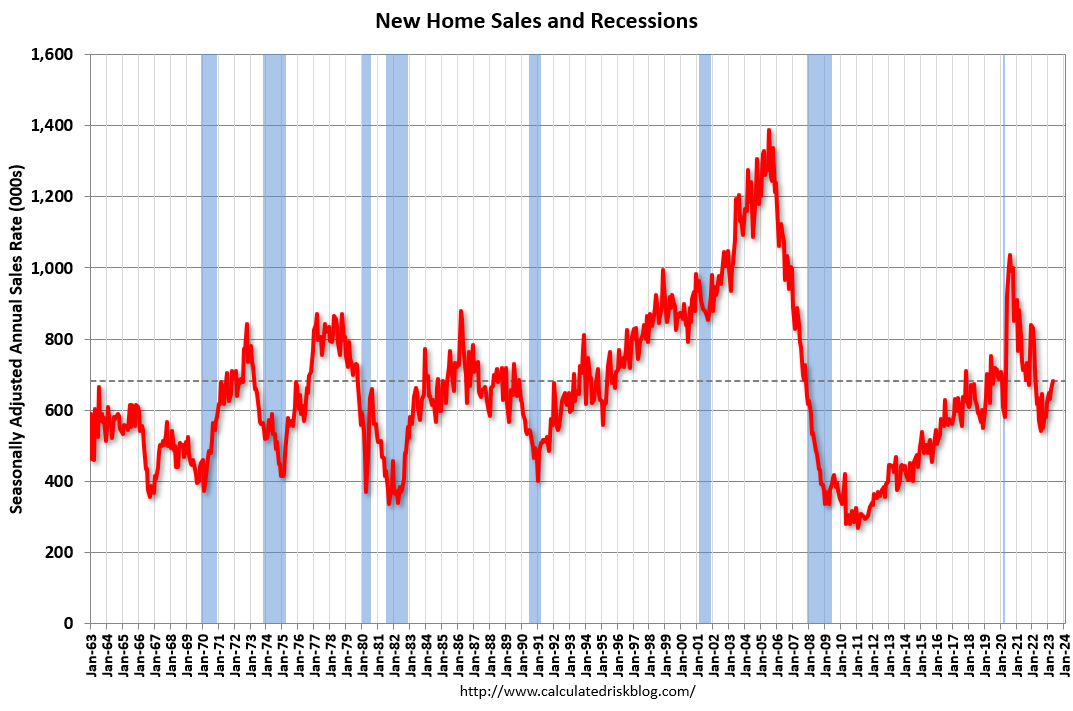

10:00 AM: New Home Sales for May from the Census Bureau.

10:00 AM: New Home Sales for May from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 657 thousand SAAR, down from 683 thousand in April.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for June.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

9:30 AM: Discussion, Fed Chair Jerome Powell, Policy Panel Discussion, At the European Central Bank (ECB) Forum on Central Banking 2023, Sintra, Portugal

4:30 PM: Fed Bank Stress Test Results

2:30 AM: Discussion, Fed Chair Jerome Powell, Dialogue with Bank of Spain Governor Pablo Hernández de Cos, At the Banco de España Fourth Conference on Financial Stability, Madrid, Spain

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 266 thousand initial claims, up from 264 thousand last week.

8:30 AM: Gross Domestic Product, 1st quarter 2023 (Third estimate). The consensus is that real GDP increased 1.4% annualized in Q1, up from the second estimate of a 1.3% increase.

10:00 AM: Pending Home Sales Index for May. The consensus is for a 0.3% decrease in the index.

8:30 AM ET: Personal Income and Outlays, May 2023. The consensus is for a 0.4% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.4%. PCE prices are expected to be up 3.8% YoY, and core PCE prices up 4.7% YoY.

9:45 AM: Chicago Purchasing Managers Index for June.

10:00 AM: University of Michigan's Consumer sentiment index (Final for June). The consensus is for a reading of 63.9.

Friday, June 23, 2023

June 23rd COVID Update: New Pandemic Lows for Deaths and Hospitalizations

by Calculated Risk on 6/23/2023 08:01:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Due to changes at the CDC, weekly cases are no longer updated.

After the first few weeks, the pandemic low for weekly deaths had been the week of July 7, 2021, at 1,690 deaths (until recently).

For COVID hospitalizations, the previous low was 9,821 (until recently).

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Hospitalized2 | 6,133 | 6,642 | ≤3,0001 | |

| Deaths per Week2 | 653 | 709 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Hospitalized and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

For deaths, I'm currently using 3 weeks ago for "now", since the most recent two weeks will be revised significantly.

On Hospitalizations (table data above is from last week):

"COVID-19 hospitalization data will not be updated during the week of June 19, 2023, due to a change in required reporting cadence from daily to weekly, following the expiration of the federal Public Health Emergency (PHE) declaration. COVID-19 hospitalization data will be updated each Monday beginning June 26, 2023."

Philly Fed: State Coincident Indexes Increased in all 50 States in May (3-Month Basis)

by Calculated Risk on 6/23/2023 04:25:00 PM

From the Philly Fed:

The Federal Reserve Bank of Philadelphia has released the coincident indexes for the 50 states for May 2023. Over the past three months, the indexes increased in all 50 states, for a three-month diffusion index of 100. Additionally, in the past month, the indexes increased in 47 states, decreased in one state, and remained stable in two, for a one-month diffusion index of 92. For comparison purposes, the Philadelphia Fed has also developed a similar coincident index for the entire United States. The Philadelphia Fed’s U.S. index increased 0.8 percent over the past three months and 0.1 percent in May.Note: These are coincident indexes constructed from state employment data. An explanation from the Philly Fed:

emphasis added

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Click on map for larger image.

Click on map for larger image.Here is a map of the three-month change in the Philly Fed state coincident indicators. This map was all red during the worst of the Pandemic and also at the worst of the Great Recession.

The map is all positive on a three-month basis.

Source: Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In May, 47 states had increasing activity including minor increases.

In May, 47 states had increasing activity including minor increases.

Q2 GDP Tracking: Around 1.5%

by Calculated Risk on 6/23/2023 01:01:00 PM

From BofA:

Overall, data since our last weekly publication moved up our 2Q GDP tracking estimate from 1.3% q/q saar to 1.4% and our 1Q GDP tracking remained at 1.8% q/q saar. [June 23rd estimate]From Goldman:

emphasis added

[W]e left our Q2 GDP tracking estimate unchanged at +1.8% (qoq ar). [June 22nd estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2023 is 1.9 percent on June 20, up from 1.8 percent on June 15. [June 20th estimate]

Final Look at Local Housing Markets in May

by Calculated Risk on 6/23/2023 09:52:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Final Look at Local Housing Markets in May

A brief excerpt:

Each month I track closed sales, new listings and active inventory in a sample of local markets around the country (over 40 local housing markets) in the US to get an early sense of changes in the housing market. In addition, we can look for regional differences. For example, listings in Texas and Florida are up more than in most other areas, and sales are down less year-over-year.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

And a table of May sales.

In May, sales in these markets were down 17.4%. In April, these same markets were down 26.1% YoY Not Seasonally Adjusted (NSA).

My early expectation is we will see a somewhat similar level of sales in June on a seasonally adjusted annual rate basis (SAAR) as in May. 30-year mortgage rates averaged about 6.4% in March and April (for closed sales in May), and 30-year rates averaged close to 6.4% in April and May.

On a Not Seasonally Adjusted (NSA) basis, June is usually the strongest month of the calendar year for closed sales, followed by July and August.

...

More local data coming in July for activity in June!

Black Knight: "Past-Due Mortgages Approach Recent Record Lows" in May

by Calculated Risk on 6/23/2023 08:21:00 AM

From Black Knight: Black Knight: Past-Due Mortgages Approach Recent Record Lows as Serious Delinquencies Continue Improvement; Prepayments See Seasonal Rise

• Reversing much of April’s calendar-driven spike, the national delinquency rate fell 11 basis points (bps) in May to hit 3.10% – the lowest it’s been other than March 2023’s record of 2.92%According to Black Knight's First Look report, the percent of loans delinquent decreased 6% in May compared to April and decreased 3% year-over-year.

• The number of borrowers a single payment past due improved by 94K (-9.5%), erasing nearly half of the prior month’s increase

• Serious delinquencies (loans 90 or more days past due) continued to improve nationally – falling by 18K (-3.7%) from April, putting this loan population down more than 200K (nearly 30%) since May 2022

• Though foreclosure starts increased to 25.4K for the month (+2.2%), they remain near April’s 6-month low and 41% below the same period in 2019, the last comparable May before the pandemic

• Foreclosure actions were started on 5.1% of serious delinquencies in May, up only marginally from April and still more than a full percentage point below the March 2020 rate at the start of the pandemic

• The number of loans in active foreclosure improved by 4K during the month and is now down 41K (-15%) from March 2020, with foreclosure sales (completions) rising 5.5% from April to 6.8K

• Prepayment activity rose to a 0.54% single-month mortality (SMM) rate – the highest level seen since September 2022, despite interest rates in the 6.7% range – but is still down 40% from May 2022

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 3.10% in May, down from 3.31% the previous month.

The percent of loans in the foreclosure process decreased in May to 0.43%, from 0.44% the previous month.

The number of delinquent properties, but not in foreclosure, is down 20,000 properties year-over-year, and the number of properties in the foreclosure process is up 8,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| May 2023 | Apr 2023 | |||

| Delinquent | 3.10% | 3.31% | ||

| In Foreclosure | 0.43% | 0.44% | ||

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,639,000 | 1,746,000 | ||

| Number of properties in foreclosure pre-sale inventory: | 234,000 | 229,000 | ||

| Total Properties | 1,868,000 | 1,980,000 | ||

Thursday, June 22, 2023

June Vehicle Sales Forecast: 15.9 million SAAR, Up Sharply YoY

by Calculated Risk on 6/22/2023 06:45:00 PM

From WardsAuto: June U.S. Light-Vehicle Sales Pegged for 21% Gain; Q2 to Roll in at 2-Year-High 15.7 Million SAAR (pay content). Brief excerpt:

Deliveries in the second quarter will total 4.1 million units, 18% above like-2022, and stronger than Q1’s 8% gain. First-half 2023 volume will total 7.67 million units, up 13% from January-June 2022’s 6.78 million.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for June (Red).

The Wards forecast of 15.9 million SAAR, would be up 5.7% from last month, and up 21.9% from a year ago.

Vehicle sales are usually a transmission mechanism for Federal Open Market Committee (FOMC) policy, although far behind housing. This time vehicle sales were more suppressed by supply chain issues and have picked up recently.

Realtor.com Reports Weekly Active Inventory Up 5% YoY; New Listings Down 26% YoY

by Calculated Risk on 6/22/2023 03:31:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report from economist Danielle Hale: Weekly Housing Trends View — Data Week Ending June 17, 2023

• Active inventory growth slowed again, with for-sale homes up just 5% above one year ago. The number of homes for sale continues to grow, but the advantage over one year ago is shrinking and likely to slow in the months ahead. As mortgage rates surged in 2022, both buyers and sellers adjusted plans and expectations, and the number of for-sale homes on the market climbed sharply. As we lap the biggest increases in inventory last year, lower interest from homeowners in selling today is eating into the total number of options for buyers, especially with existing home sales largely steadying. This is a contributor to the big shift in expectations we have for inventory in 2023, which will likely decline for the year as a whole.

• New listings–a measure of sellers putting homes up for sale–were down again this week, by 26% from one year ago. The number of newly listed homes has been lower than the same time the previous year for the past 50 weeks. Despite an uptick in seller confidence in May, with an increasing share of consumers saying now is a good time to sell, a smaller number of homeowners are choosing to list homes for sale, limiting the number of cumulative options that home shoppers are likely to see over the course of their search.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory is still up year-over-year - from record lows - however, the YoY increase has slowed sharply recently.

This was the smallest YoY increase since May 2022.

The recent trend suggests active inventory will likely be down YoY in the next couple of weeks!

{kind=link}