RSS Feed

RSS Feed by Calculated Risk on 7/03/2023 08:21:00 AM

Monday, July 03, 2023

Housing July 3rd Weekly Update: Inventory Increased 1.3% Week-over-week; Down Year-over-year

Altos reports that active single-family inventory was up 1.3% week-over-week.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of June 30th, inventory was at 466 thousand (7-day average), compared to 460 thousand the prior week.

Year-to-date, inventory is down 5.1%. And inventory is up 14.9% from the seasonal bottom eleven weeks ago.

The red line is for 2023. The black line is for 2019. Note that inventory is up from the record low for the same week in 2021, but below last year and still well below normal levels.

Inventory was down 1.3% compared to the same week in 2022 (last week it was up 4.3%), and down 51.9% compared to the same week in 2019 (last week down 51.8%).

It appears likely same week inventory will be below 2022 levels for the remainder of the year, but above 2021 levels - and possibly above 2020 levels late in the year.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, July 02, 2023

Sunday Night Futures

by Calculated Risk on 7/02/2023 07:48:00 PM

Weekend:

• Schedule for Week of July 2, 2023

Monday:

• At 10:00 AM ET, ISM Manufacturing Index for June. The consensus is for the ISM to be at 47.2, up from 46.9 in May.

• Also, at 10:00 AM, Construction Spending for May. The consensus is for a 0.5% increase in construction spending.

• Late in the day, Light vehicle sales for June. The consensus is for light vehicle sales to be 15.3 million SAAR in June, up from 15.1 million in May (Seasonally Adjusted Annual Rate). Wards Auto is forecasting sales of 15.9 million SAAR in June.

• US markets will close at 1:00 PM ET prior to the Independence Day Holiday.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are unchanged (fair value).

Oil prices were up over the last week with WTI futures at $70.64 per barrel and Brent at $75.41 per barrel. A year ago, WTI was at $110, and Brent was at $119 - so WTI oil prices are down about 36% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.50 per gallon. A year ago, prices were at $4.81 per gallon, so gasoline prices are down $1.31 per gallon year-over-year.

Update: Lumber Prices Down About 35% YoY

by Calculated Risk on 7/02/2023 08:21:00 AM

Here is another monthly update on lumber prices.

This graph shows CME random length framing futures through May 16th (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red).

LBR is currently at $528.50 per 1000 board feet.

Click on graph for larger image.

Click on graph for larger image.The year-over-year change is estimated using the previous series.

There is somewhat of a seasonal demand for lumber, and lumber prices usually peak in April or May.

We didn't see a significant runup in prices this Spring due to the housing slowdown.

Saturday, July 01, 2023

Real Estate Newsletter Articles this Week: New Home Sales Increase in May

by Calculated Risk on 7/01/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• New Home Sales increase to 763,000 Annual Rate in May

• Case-Shiller: National House Price Index Decreased 0.2% year-over-year in April

• Inflation Adjusted House Prices 3.8% Below Peak

• Fannie and Freddie Serious Delinquencies in May: Single Family Declined, Multi-Family Increased

• Freddie Mac House Price Index Increased Slightly in May; Up 0.4% Year-over-year

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of July 2, 2023

by Calculated Risk on 7/01/2023 08:11:00 AM

The key report scheduled for this week is the June employment report to be released on Friday.

Other key reports include the June ISM Manufacturing survey, June Vehicle Sales, May Job Openings and the Trade Deficit for May.

10:00 AM: ISM Manufacturing Index for June. The consensus is for the ISM to be at 47.2, up from 46.9 in May.

10:00 AM: Construction Spending for May. The consensus is for a 0.5% increase in construction spending.

Late in the day: Light vehicle sales for June.

Late in the day: Light vehicle sales for June.The consensus is for light vehicle sales to be 15.3 million SAAR in June, up from 15.1 million in May (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the sales rate for last month.

Wards Auto is forecasting sales of 15.9 million SAAR in June.

US markets will close at 1:00 PM ET prior to the Independence Day Holiday.

All US markets will be closed in observance of Independence Day

8:00 AM: Corelogic House Price index for May.

2:00 PM: FOMC Minutes, Meeting of June 13-14, 2023

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for June. This report is for private payrolls only (no government). The consensus is for 236,000 payroll jobs added in June, down from 278,000 in May.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 245 thousand initial claims, up from 239 thousand last week.

8:30 AM: Trade Balance report for May from the Census Bureau.

8:30 AM: Trade Balance report for May from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $69.8 billion. The U.S. trade deficit was at $74.6 billion the previous month.

10:00 AM ET: Job Openings and Labor Turnover Survey for May from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for May from the BLS. This graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in April to 10.1 million from 9.7 million in March.

The number of job openings (yellow) were down 14% year-over-year and quits were down 16% year-over-year.

10:00 AM: the ISM Services Index for June. The consensus is for a reading of 50.5, up from 50.3.

8:30 AM: Employment Report for June. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.

8:30 AM: Employment Report for June. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.There were 339,000 jobs added in May, and the unemployment rate was at 3.7%.

This graph shows the jobs added per month since January 2021.

Friday, June 30, 2023

June 30th COVID Update: New Pandemic Lows for Deaths and Hospitalizations

by Calculated Risk on 6/30/2023 07:11:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Due to changes at the CDC, weekly cases are no longer updated.

After the first few weeks, the pandemic low for weekly deaths had been the week of July 7, 2021, at 1,690 deaths (until recently).

For COVID hospitalizations, the previous low was 9,821 (until recently).

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Hospitalized2 | 5,758 | 6,233 | ≤3,0001 | |

| Deaths per Week2 | 522 | 624 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Hospitalized and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

For deaths, I'm currently using 3 weeks ago for "now", since the most recent two weeks will be revised significantly.

Freddie Mac House Price Index Increased Slightly in May; Up 0.4% Year-over-year

by Calculated Risk on 6/30/2023 12:52:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Freddie Mac House Price Index Increased Slightly in May; Up 0.4% Year-over-year

A brief excerpt:

On a year-over-year basis, the National FMHPI was up 0.4% in May, from up 0.7% YoY in April. The YoY increase peaked at 19.2% in July 2021. ...There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

In May, 15 states and D.C. were below their 2022 peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peak were in D.C. (-9.1%), Idaho (-7.2%), Nevada (-7.1%), Hawaii (-5.5%), Arizona (-5.2%), Utah (-4.9%), Washington (-4.3%), California (-3.7%), Oregon (-3.6%) and Wyoming (-5.0%).

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted.

...

The FMHPI is suggesting the YoY change in the Case-Shiller index will be close to unchanged for the next couple of months.

The big question is “Will house prices decline further later this year?” And I’ll post some thoughts on this next week.

Q2 GDP Tracking: Around 2%

by Calculated Risk on 6/30/2023 12:00:00 PM

From BofA:

Personal spending came in slight below expectations and with a downward revision in April. Overall, this decreased our personal consumption expenditure tracking estimate for 2Q. After rounding, it left our 2Q US GDP tracking estimate unchanged at 1.5%. [June 30th estimate]From Goldman:

emphasis added

[W]e left our Q2 GDP tracking estimate unchanged at +2.2% (qoq ar). [June 30th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2023 is 2.2 percent on June 30, up from 1.8 percent on June 27. [June 30th estimate]

PCE Measure of Shelter Finally Slowing YoY

by Calculated Risk on 6/30/2023 08:47:00 AM

Here is a graph of the year-over-year change in shelter from the CPI report and housing from the PCE report this morning, both through May 2023.

CPI Shelter was up 8.0% year-over-year in May, down from 8.1% in April, and down from the cycle peak of 8.2% in March 2023.

CPI Shelter was up 8.0% year-over-year in May, down from 8.1% in April, and down from the cycle peak of 8.2% in March 2023.

Housing (PCE) was up 8.3% YoY in May, down from 8.4% in April (April was the cycle peak).

Since asking rents are soft and Year-over-year Rent Growth Continues to Decelerate these measures will slow further in coming months.

Since asking rents are soft and Year-over-year Rent Growth Continues to Decelerate these measures will slow further in coming months.

Personal Income increased 0.4% in May; Spending increased 0.1%

by Calculated Risk on 6/30/2023 08:37:00 AM

The BEA released the Personal Income and Outlays report for May:

Personal income increased $91.2 billion (0.4 percent at a monthly rate) in May, according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI), personal income less personal current taxes, increased $86.7 billion (0.4 percent) and personal consumption expenditures (PCE) increased $18.9 billion (0.1 percent).The May PCE price index increased 3.8 percent year-over-year (YoY), down from 4.3 percent YoY in April, and down from the recent peak of 7.0 percent in June 2022.

The PCE price index increased 0.1 percent. Excluding food and energy, the PCE price index increased 0.3 percent. Real DPI increased 0.3 percent in May and real PCE decreased by less than 0.1 percent; goods decreased 0.4 percent and services increased 0.2 percent

emphasis added

The PCE price index, excluding food and energy, increased 4.6 percent YoY, down from 4.7 percent in April, and down from the recent peak of 5.4 percent in February 2022.

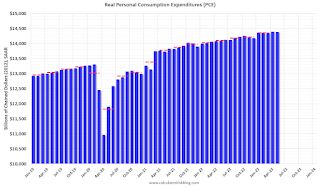

The following graph shows real Personal Consumption Expenditures (PCE) through May 2023 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

Personal income was at expectations, and PCE was slightly below expectations.

The following graph shows real Personal Consumption Expenditures (PCE) through May 2023 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income was at expectations, and PCE was slightly below expectations.

Inflation was slightly below expectations.

Using the two-month method to estimate Q2 real PCE growth, real PCE was increasing at a 0.7% annual rate in Q2 2023. (Using the mid-month method, real PCE was increasing at 0.8%). This suggests weak PCE growth in Q2.