RSS Feed

RSS Feed by Calculated Risk on 7/14/2023 08:25:00 AM

Friday, July 14, 2023

Q2 GDP Tracking: Around 2%

From BofA:

Data since our last weekly publication moved up our 2Q GDP tracking estimate from 1.4% q/q saar to 1.5%. [July 14th estimate]From Goldman:

emphasis added

We boosted our Q2 GDP tracking estimate by one tenth to +2.3% (qoq ar). Our Q2 domestic final sales growth forecast stands at +2.6%. [July 10th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2023 is 2.3 percent on July 10, up from 2.1 percent on July 6. After recent releases from the US Bureau of Economic Analysis, the US Bureau of Labor Statistics, and the US Census Bureau, the nowcast of second-quarter real gross private domestic investment growth increased from 9.6 percent to 10.5 percent. [July 10th estimate]

Thursday, July 13, 2023

Realtor.com Reports Weekly Active Inventory Down 5% YoY; New Listings Down 27% YoY

by Calculated Risk on 7/13/2023 03:50:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report from analyst Hannah Jones: Weekly Housing Trends View — Data Week Ending July 8, 2023

• Active inventory declined, with for-sale homes lagging behind year ago levels by 5%. A year into weekly new listing declines, active inventory levels have started to mirror the slow down in listing activity. More than 80% of home-shoppers looking to buy and sell a home feel locked in by their current mortgage rate. As a result, buyers are seeing fewer available homes on the market. We expect to see this trend continue as mortgage rates are expected to remain elevated for the time being.

• New listings–a measure of sellers putting homes up for sale–were down again this week, by 27% from one year ago. The number of newly listed homes has been lower than the same time the previous year for the past 53 weeks. This week’s data shows a wider gap than last week, and is bigger than what has been typical year-to-date. The job market’s ongoing resilience has enabled buyers to remain active in today’s market, despite the high cost of homeownership. However, high mortgage rates have convinced many would-be sellers to hold off on listing their home for sale. Buyer demand and lack of existing home inventory has resulted in renewed new home sales energy.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was down 5.0% year-over-year - this was the third consecutive YoY decrease following 58 consecutive weeks with a YoY increase in inventory.

Inventory is still up from the record lows in the 2nd half of 2021 and early 2022, and it is unlikely we will see new record lows this year.

Hotels: Occupancy Rate Down 2.3% Year-over-year

by Calculated Risk on 7/13/2023 01:28:00 PM

Due to constricted business travel during the Fourth of July, U.S. hotel performance fell from the previous week and showed weaker year-over-year comparisons, according to STR‘s latest data through 8 July.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

2-8 July 2023 (percentage change from comparable week in 2022):

• Occupancy: 61.8% (-2.3%)

• Average daily rate (ADR): US$155.81 (+1.2%)

• Revenue per available room (RevPAR): US$96.36 (-1.2%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2023, black is 2020, blue is the median, and dashed light blue is for 2022. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is at the median rate for the period 2000 through 2022 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase during the summer travel season.

Part 2: Current State of the Housing Market; Overview for mid-July

by Calculated Risk on 7/13/2023 10:32:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Part 2: Current State of the Housing Market; Overview for mid-July

A brief excerpt:

Yesterday, in Part 1: Current State of the Housing Market; Overview for mid-July I reviewed home inventory and sales.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

Here is some data from the recently released FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q1 2023.

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 23.3% of loans are under 3%, 61.3% are under 4%, and 81.2% are under 5%.

The percent of outstanding loans under 4% peaked in Q1 2022 at 65.3%, and the percent under 5% peaked at 85.6%.

This is very different from the housing bust, when many homeowners were forced to sell as their teaser rates expired and they could not afford the fully amortized mortgage payment. The current situation is similar to the 1980 period, when rates also increased quickly.

Weekly Initial Unemployment Claims Decrease to 237,000

by Calculated Risk on 7/13/2023 08:34:00 AM

The DOL reported:

In the week ending July 8, the advance figure for seasonally adjusted initial claims was 237,000, a decrease of 12,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 248,000 to 249,000. The 4-week moving average was 246,750, a decrease of 6,750 from the previous week's revised average. The previous week's average was revised up by 250 from 253,250 to 253,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 246,750.

The previous week was revised up.

Weekly claims were below the consensus forecast.

Wednesday, July 12, 2023

Thursday: Unemployment Claims, PPI

by Calculated Risk on 7/12/2023 08:50:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

The better-than-expected inflation data today pushed down mortgage rates.

Thursday:

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for 245 thousand initial claims, down from 248 thousand last week.

• At 8:30 AM, The Producer Price Index for June from the BLS. The consensus is for a 0.2% increase in PPI, and a 0.2% increase in core PPI.

Part 1: Current State of the Housing Market; Overview for mid-July

by Calculated Risk on 7/12/2023 05:54:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-July

A brief excerpt:

Interestingly, new home inventory is close to a record percentage of total inventory. This graph uses Not Seasonally Adjusted (NSA) existing home inventory from the National Association of Realtors® (NAR) and new home inventory from the Census Bureau (only completed and under construction inventory).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note: Mark Fleming, Chief Economist at First American pointed this out in March.

It took a number of years following the housing bust for new home inventory to return to the pre-bubble percent of total inventory. Then, with the pandemic, existing home inventory collapsed and now the percent of new homes is close to 23% of total for sale inventory. The lack of existing home inventory, and few distressed sales, has been a positive for homebuilders.

Fed's Beige Book: "Overall economic activity increased slightly"

by Calculated Risk on 7/12/2023 05:17:00 PM

Fed's Beige Book "This report was prepared at the Federal Reserve Bank of Minneapolis based on information collected on or before June 30, 2023."

Overall economic activity increased slightly since late May. Five Districts reported slight or modest growth, five noted no change, and two reported slight and modest declines. Reports on consumer spending were mixed; growth was generally observed in consumer services, but some retailers noted shifts away from discretionary spending. Tourism and travel activity was robust, and hospitality contacts expected a busy summer season. Auto sales remained unchanged or exhibited moderate growth across most Districts. Manufacturing activity edged up in half of the Districts and declined in the other half. Transportation activity was down or flat in most Districts that reported on it, as some contacts reported reduced demand due to high inventory levels and others noted continued challenges from labor shortages. Banking conditions were mostly subdued, as lending activity continued to soften. Despite higher mortgage rates, demand for residential real estate remained steady, although sales were constrained by low inventories. Construction for both residential and commercial units was slightly lower on balance. Agricultural conditions were mixed geographically but softened slightly on balance, with some contacts expecting further softening for the remainder of 2023. Energy activity decreased. Overall economic expectations for the coming months generally continued to call for slow growth.

Employment increased modestly this period, with most Districts experiencing some job growth. Labor demand remained healthy, though some contacts reported that hiring was getting more targeted and selective. Employers continued to have difficulty finding workers, particularly in health care, transportation, and hospitality, and for high-skilled positions in general. However, many Districts reported that labor availability had improved and that some employers were having an easier time hiring than they were having previously. Employers also reported that the unusually high turnover rates in recent years appear to be returning to pre-pandemic norms. Wages continued to rise, but more moderately. Contacts in multiple Districts reported that wage increases were returning to or nearing pre-pandemic levels.

emphasis added

Early Look at 2024 Cost-Of-Living Adjustments and Maximum Contribution Base

by Calculated Risk on 7/12/2023 03:47:00 PM

The BLS reported this morning:

The Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) increased 2.3 percent over the last 12 months to an index level of 299.394 (1982-84=100). For the month, the index increased 0.3 percent prior to seasonal adjustment.CPI-W is the index that is used to calculate the Cost-Of-Living Adjustments (COLA). The calculation dates have changed over time (see Cost-of-Living Adjustments), but the current calculation uses the average CPI-W for the three months in Q3 (July, August, September) and compares to the average for the highest previous average of Q3 months. Note: this is not the headline CPI-U and is not seasonally adjusted (NSA).

• In 2022, the Q3 average of CPI-W was 291.901.

The 2022 Q3 average was the highest Q3 average, so we only have to compare Q3 this year to last year.

Click on graph for larger image.

Click on graph for larger image.This graph shows CPI-W since January 2000. The red lines are the Q3 average of CPI-W for each year.

Note: The year labeled is for the calculation, and the adjustment is effective for December of that year (received by beneficiaries in January of the following year).

CPI-W was up 2.3% year-over-year in June, and although this is early - we need the data for July, August and September - my very early guess is COLA will probably be close to 3% this year, the smallest increase since 1.3% in 2021.

Note that CPI-W was slightly negative month-over-month in July and August of 2022, so it is likely there will be a larger year-over-year increase in CPI-W over the next few months than in June, hence my 3% early guess.

Contribution and Benefit Base

The contribution base will be adjusted using the National Average Wage Index. This is based on a one-year lag. The National Average Wage Index is not available for 2022 yet, wages increased solidly in 2022. If wages increased 5% in 2022, then the contribution base next year will increase to around $168,200 in 2024, from the current $160,200.

Remember - this is an early look. What matters is average CPI-W, NSA, for all three months in Q3 (July, August and September).

Contribution and Benefit Base

The contribution base will be adjusted using the National Average Wage Index. This is based on a one-year lag. The National Average Wage Index is not available for 2022 yet, wages increased solidly in 2022. If wages increased 5% in 2022, then the contribution base next year will increase to around $168,200 in 2024, from the current $160,200.

Remember - this is an early look. What matters is average CPI-W, NSA, for all three months in Q3 (July, August and September).

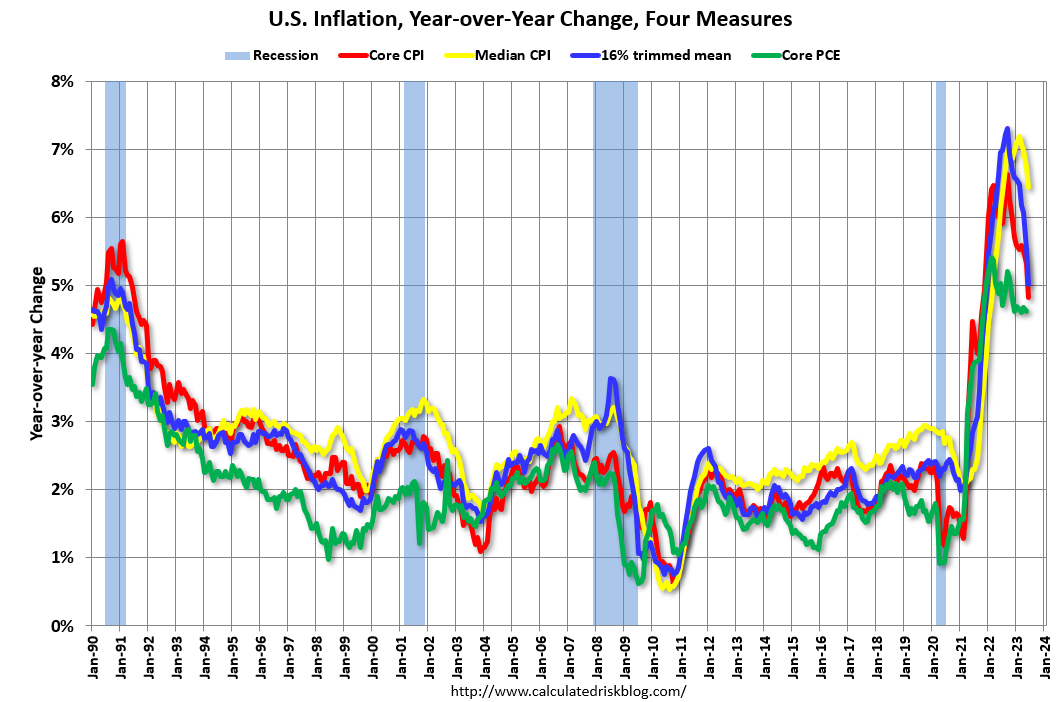

Cleveland Fed: Median CPI increased 0.1% and Trimmed-mean CPI increased 0.1% in June

by Calculated Risk on 7/12/2023 01:06:00 PM

The Cleveland Fed released the median CPI and the trimmed-mean CPI.

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.1% in June. The 16% trimmed-mean Consumer Price Index also increased 0.1% in June. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 6.4%, the trimmed-mean CPI rose 5.5%, and the CPI less food and energy rose 5.0%. Core PCE is for May and increased 4.6% year-over-year.

Note: The Cleveland Fed released the median CPI details. "Motor Vehicle Insurance" increased at a 21% annualized rate in June.