RSS Feed

RSS Feed by Calculated Risk on 9/24/2023 09:51:00 AM

Sunday, September 24, 2023

The Top Ten Job Streaks: Current Streak is in 8th Place

For fun:

Through August 2023, the employment report indicated positive job growth for 32 consecutive months, putting the current streak in 8th place of the longest job streaks in US history (since 1939).

The UAW strike will not impact the September employment report since it started on September 15th, so it seems likely the job streak will move into a tie for 5th place with the next report (if it is actually released - threatened by another shutdown).

| Headline Jobs, Top 10 Streaks | |

|---|---|

| Year Ended | Streak, Months |

| 2019 | 100 |

| 1990 | 48 |

| 2007 | 46 |

| 1979 | 45 |

| 1943 | 33 |

| 1986 | 33 |

| 2000 | 33 |

| 20231 | 32 |

| 1967 | 29 |

| 1995 | 25 |

| 1Currrent Streak | |

Saturday, September 23, 2023

Real Estate Newsletter Articles this Week: Near Record Number of Multi-Family Housing Units Under Construction

by Calculated Risk on 9/23/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• August Housing Starts: Near Record Number of Multi-Family Housing Units Under Construction

• NAR: Existing-Home Sales Decreased to 4.04 million SAAR in August

• Lawler: Early Read on Existing Home Sales in August and Some New Household/Housing Stock Data

• 4th Look at Local Housing Markets in August

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Schedule for Week of September 24, 2023

by Calculated Risk on 9/23/2023 08:11:00 AM

The key reports this week are August New Home sales, the third estimate of Q2 GDP, Personal Income and Outlays for August, and Case-Shiller house prices for July.

For manufacturing, the Richmond, Dallas and Kansas City Fed manufacturing surveys will be released this week.

8:30 AM ET: Chicago Fed National Activity Index for August. This is a composite index of other data.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for September.

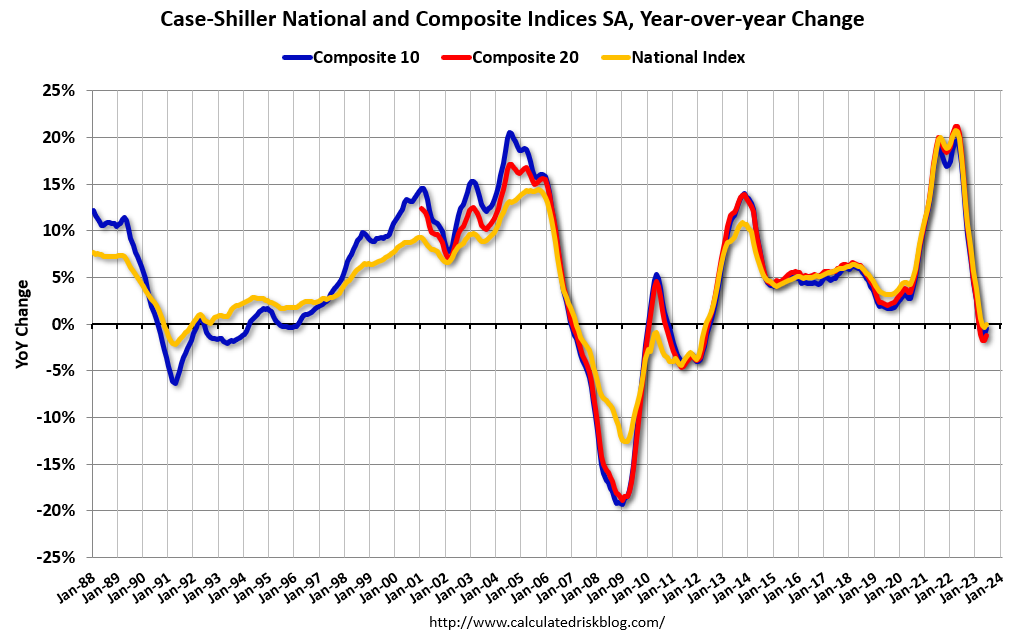

9:00 AM: S&P/Case-Shiller House Price Index for July.

9:00 AM: S&P/Case-Shiller House Price Index for July.This graph shows the year-over-year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 0.5% year-over-year increase in the National index for July.

9:00 AM: FHFA House Price Index for July. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: New Home Sales for August from the Census Bureau.

10:00 AM: New Home Sales for August from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 700 thousand SAAR, down from 714 thousand in July.

10:00 AM: the Richmond Fed manufacturing survey for September.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for August from the Census Bureau. The consensus is for a 1.6% decrease in durable goods orders.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 206 thousand initial claims, up from 201 thousand last week.

8:30 AM: Gross Domestic Product, 2nd Quarter 2023 (Third Estimate), and Corporate Profits (Revised) The consensus is that real GDP increased 2.2% annualized in Q2, up from the second estimate of 2.1%.

10:00 AM: Pending Home Sales Index for August. The consensus is 1.0% decrease in the index.

11:00 AM: the Kansas City Fed manufacturing survey for September. This is the last of the regional surveys for September.

4:00 PM: Conversation with Fed Chair Powell: A Teacher Town Hall Meeting "Federal Reserve Board Chair Jerome H. Powell will host a town hall with educators in Washington, D.C. and nationwide via webcast ... The Chair will respond to questions from the in-person audience and virtual participants from across the country."

8:30 AM: Personal Income and Outlays, August 2023. The consensus is for a 0.5% increase in personal income, and for a 0.4% increase in personal spending. And for the Core PCE price index to increase 0.2%. PCE prices are expected to be up 3.5% YoY, and core PCE prices up 3.9% YoY.

9:45 AM: Chicago Purchasing Managers Index for September. The consensus is for a reading of 47.6, down from 48.7 in August.

10:00 AM: University of Michigan's Consumer sentiment index (Final for September). The consensus is for a reading of 67.7.

Friday, September 22, 2023

Sept 22nd COVID Update: Deaths and Hospitalizations Increased

by Calculated Risk on 9/22/2023 07:17:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Due to changes at the CDC, weekly cases are no longer updated.

For deaths, I'm currently using 3 weeks ago for "now", since the most recent two weeks will be revised significantly.

Recently hospitalizations have tripled from a low of 5,150 in June 2023. Hospitalizations are increasing, but far below the peak of 150,000 in January 2022.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Hospitalized2🚩 | 16,050 | 14,681 | ≤3,0001 | |

| Deaths per Week2🚩 | 1,005 | 959 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Hospitalized and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths have more than doubled from a low of 469 in early July. Weekly deaths are increasing, but far below the weekly peak of 26,000 in January 2021.

Black Knight: Mortgage Delinquency Rate Decreased Slightly in August

by Calculated Risk on 9/22/2023 01:43:00 PM

From Black Knight: Black Knight’s First Look: Mortgage Performance Remains Strong, but Slowing Improvement Suggests Delinquencies May Be Nearing Cycle Lows

• At 3.17%, the U.S. delinquency rate improved by 4 basis points in August and is nearly a full percentage point below its 2015-2019 same-month averageAccording to Black Knight's First Look report, the percent of loans delinquent decreased 1.2% in August compared to July and decreased 0.8% year-over-year.

• However, steady slowing in the annual rate of improvement -- from -40% in early 2022 to -0.8% as of August – suggests delinquency rates may be nearing cycle lows

• Serious delinquencies (90+ days past due) continued to improve, falling 20K from July to 448K – still the lowest level since June 2006 – and down 151K (-25%) year over year

• Early-stage delinquencies, on the other hand, continued to trend upward, with both 30- and 60-day late populations inching up by 2K, marking the third consecutive monthly increase

• The number of loans in active foreclosure declined to 215K – the lowest level since March 2022 following the end of moratoria on such actions – and is down 68K (-24%) from pre-pandemic February 2020

• August’s 31.9K (+21.3% month over month) foreclosure starts – equating to 6.8% of serious delinquencies – were still 21% below August 2019 pre-pandemic levels

• While 6.9K foreclosure sales marked a 13% increase from July, volumes remain at roughly half pre-pandemic levels

• Prepayment activity (SMM) inched up to 0.53% under pressure from seasonal home buying patterns, while interest rates north of 7% continue to hold prepayment speeds at historically low levels

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 3.17% in August, down from 3.21% the previous month.

The percent of loans in the foreclosure process decreased in August to 0.41%, from 0.42% the previous month.

The number of delinquent properties, but not in foreclosure, is up 12,000 properties year-over-year, and the number of properties in the foreclosure process is down 14,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| August 2023 | July 2023 | |||

| Delinquent | 3.17% | 3.21% | ||

| In Foreclosure | 0.41% | 0.42% | ||

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,684,000 | 1,700,000 | ||

| Number of properties in foreclosure pre-sale inventory: | 215,000 | 220,000 | ||

| Total Properties | 1,899,000 | 1,919,000 | ||

Philly Fed: State Coincident Indexes Increased in 40 States in August (3-Month Basis)

by Calculated Risk on 9/22/2023 12:59:00 PM

From the Philly Fed:

The Federal Reserve Bank of Philadelphia has released the coincident indexes for the 50 states for August 2023. Over the past three months, the indexes increased in 40 states, decreased in eight states, and remained stable in two, for a three-month diffusion index of 64. Additionally, in the past month, the indexes increased in 30 states, decreased in 13 states, and remained stable in seven, for a one-month diffusion index of 34. For comparison purposes, the Philadelphia Fed has also developed a similar coincident index for the entire United States. The Philadelphia Fed’s U.S. index increased 0.6 percent over the past three months and 0.1 percent in August.Note: These are coincident indexes constructed from state employment data. An explanation from the Philly Fed:

emphasis added

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Click on map for larger image.

Click on map for larger image.Here is a map of the three-month change in the Philly Fed state coincident indicators. This map was all red during the worst of the Pandemic and also at the worst of the Great Recession.

The map is mostly positive on a three-month basis.

Source: Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In August, 33 states had increasing activity including minor increases.

In August, 33 states had increasing activity including minor increases.

September Vehicle Sales Forecast: 15.4 million SAAR, Up Sharply YoY

by Calculated Risk on 9/22/2023 09:56:00 AM

From WardsAuto: September U.S. Light-Vehicle Sales Heading for Strong Year-Over-Year Gain Despite Strike Impact (pay content). Brief excerpt:

The possibility in September that other automakers will benefit much from buyers defecting from the Detroit 3 brands is negligible. The vehicles currently impacted by shutdowns either are products with high brand loyalty, in segments dominated by the three strike-impacted manufacturers or have plenty of inventory.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for September (Red).

On a seasonally adjusted annual rate basis, the Wards forecast of 15.4 million SAAR, would be up 2% from last month, and up 13% from a year ago.

Vehicle sales are usually a transmission mechanism for Federal Open Market Committee (FOMC) policy, although far behind housing. This time vehicle sales were more suppressed by supply chain issues and have picked up recently.

Q3 GDP Tracking: Around 3%

by Calculated Risk on 9/22/2023 08:28:00 AM

From BofA:

Overall, the data flow since our last report left our 3Q and 2Q US GDP tracking unchanged at 2.9% q/q saar and 2.3% q/q saar, respectively. [Sept 22nd estimate]From Goldman:

emphasis added

We left our Q3 GDP tracking estimate unchanged at +3.2% (qoq ar). [Sept 21st estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2023 is 4.9 percent on September 19, unchanged from September 14 after rounding. After recent releases from the US Census Bureau and the US Bureau of Labor Statistics, the nowcast of third-quarter real residential investment growth decreased from 6.8 percent to 6.3 percent, while the nowcast of the contribution of inventory investment to third-quarter real GDP growth decreased from 1.20 percentage points to 1.05 percentage points. [Sept 19th estimate]

Thursday, September 21, 2023

"Mortgage Rates Jump up to 23-Year Highs"

by Calculated Risk on 9/21/2023 08:15:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Jump up to 23-Year Highs

From Matthew Graham at Mortgage News Daily: Mortgage Rates Jump up to 23-Year Highs

Between the data and the overnight momentum in overseas markets, bonds are at their weakest levels in years. Mortgage-backed securities (the bonds that dictate mortgage rates) didn't swoon quite as much as Treasuries, but as of today, it was just enough to push the average mortgage lender almost perfectly back in line with the highest 30yr fixed rate of the past 23 years. [30 year fixed 7.47%]Friday:

emphasis added

• No major economic releases scheduled.

Hotels: Occupancy Rate Decreased 2.2% Year-over-year

by Calculated Risk on 9/21/2023 05:23:00 PM

U.S. hotel performance increased from the previous week, according to CoStar’s latest data through 16 September. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

10-16 September 2023 (percentage change from comparable week in 2022):

• Occupancy: 67.7% (-2.2%)

• Average daily rate (ADR): US$161.15 (+2.3%)

• Revenue per available room (RevPAR): US$109.07 (+0.1%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2023, black is 2020, blue is the median, and dashed light blue is for 2022. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking just below last year, and slightly above the median rate for the period 2000 through 2022 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will pick up a little during the Fall.

{kind=link}